Gold prices dip as hawkish Fed minutes weigh ahead of Jackson Hole

Introduction & Market Context

Elevance Health (NYSE:ELV) presented its second quarter 2025 earnings results on July 17, revealing strong revenue growth offset by margin pressure from elevated medical costs. The healthcare giant’s stock traded down 2.47% in premarket to $336.03, reflecting investor concerns about the revised full-year guidance.

The presentation comes after a strong first quarter when the company beat expectations with an adjusted EPS of $11.97. However, the second quarter results show a significant shift in performance trajectory, with the company now facing industry-wide challenges in its ACA and Medicaid businesses.

Quarterly Performance Highlights

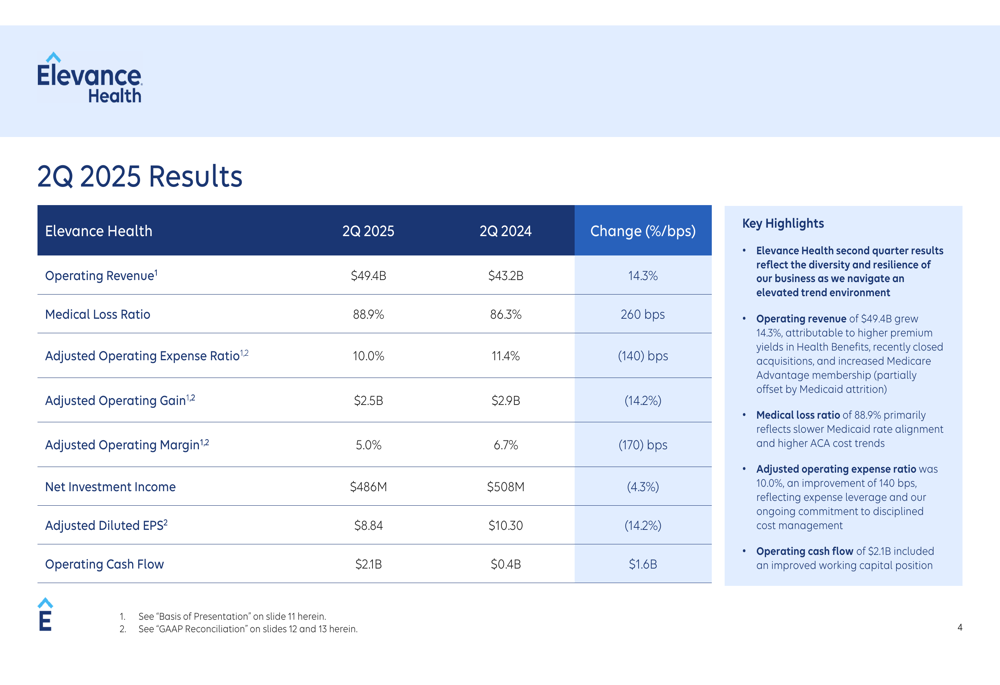

Elevance Health reported second quarter operating revenue of $49.4 billion, representing robust growth of 14.3% compared to the same period in 2024. However, profitability metrics showed considerable pressure, with adjusted diluted earnings per share declining 14.2% year-over-year to $8.84.

As shown in the following financial overview:

The medical loss ratio (MLR) increased 260 basis points to 88.9%, reflecting higher utilization and medical costs. This was partially offset by an improvement in the adjusted operating expense ratio, which decreased 140 basis points to 10.0%. Despite these challenges, operating cash flow showed significant improvement, reaching $2.1 billion compared to $0.4 billion in the prior-year period.

The company has returned $2.0 billion to shareholders year-to-date through dividends and share repurchases, demonstrating its commitment to shareholder returns despite operational headwinds.

Segment Analysis

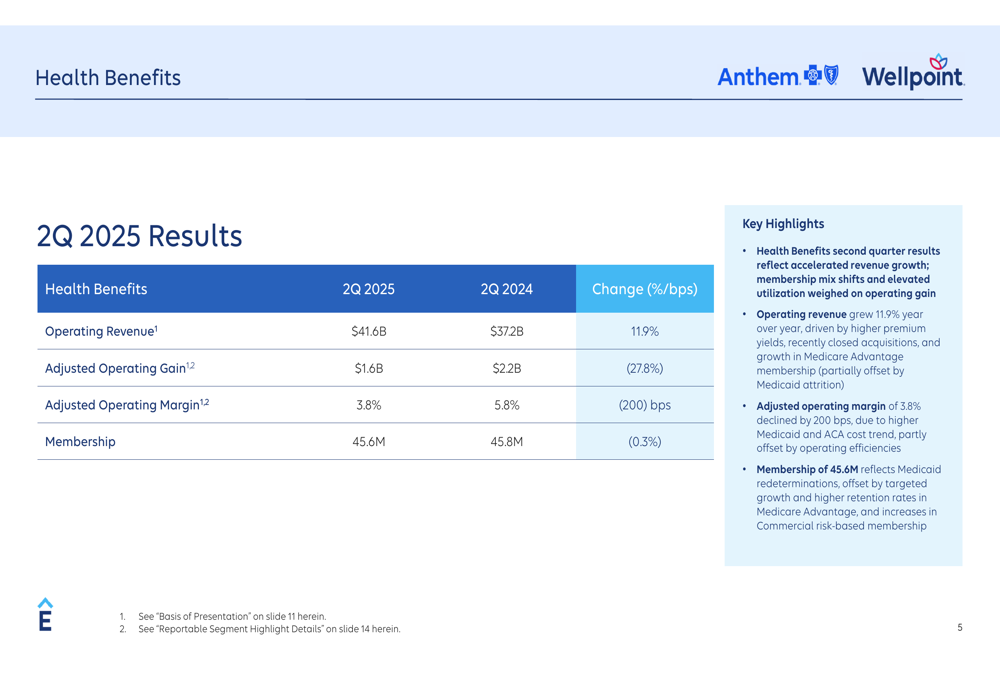

Elevance Health’s results revealed divergent performance between its two main business segments. The Health Benefits segment, which includes commercial, Medicare, and Medicaid plans, experienced pressure on profitability despite revenue growth.

As illustrated in the Health Benefits results:

The segment posted revenue of $41.6 billion, up 11.9% year-over-year, but adjusted operating gain declined sharply by 27.8% to $1.6 billion. The adjusted operating margin contracted by 200 basis points to 3.8%. Membership remained relatively stable at 45.6 million, a slight decrease of 0.3% from the prior year, reflecting the impact of Medicaid redeterminations offset by growth in Medicare Advantage and commercial risk-based membership.

In contrast, the Carelon (Health Services) segment delivered strong performance:

Carelon’s operating revenue surged 35.8% to $18.1 billion, with adjusted operating gain increasing 25.0% to $0.9 billion. The segment’s growth was fueled by scaling of innovative risk-based capabilities and integration of acquisitions, particularly in specialty pharmacy services. Adjusted scripts increased 6.5% to 83.3 million, though the number of consumers served decreased by 4.9% to 97.3 million.

Revised Outlook and Guidance

In a significant development, Elevance Health has revised its full-year 2025 adjusted diluted EPS guidance downward to approximately $30.00. This represents a substantial reduction from the previous guidance range of $34.15 to $34.85 provided during the first quarter earnings call.

The company’s key highlights and outlook are summarized in the following slide:

Management attributed the guidance revision primarily to the ongoing and industry-wide impact of elevated cost trends in ACA and Medicaid businesses. The company now expects the 2025 benefit expense ratio to be approximately 90.0%, reflecting these higher medical costs. Operating cash flow guidance has also been updated to approximately $6.0 billion, primarily due to the revised earnings outlook and unfavorable working capital impacts.

To address these challenges, Elevance Health is accelerating its capabilities through advanced digital and AI tools to personalize the healthcare journey, streamlining prior authorizations (with over half of electronic requests now processed in real time), and investing in advanced analytics to identify and reduce wasteful spending.

Long-Term Strategy and Growth Algorithm

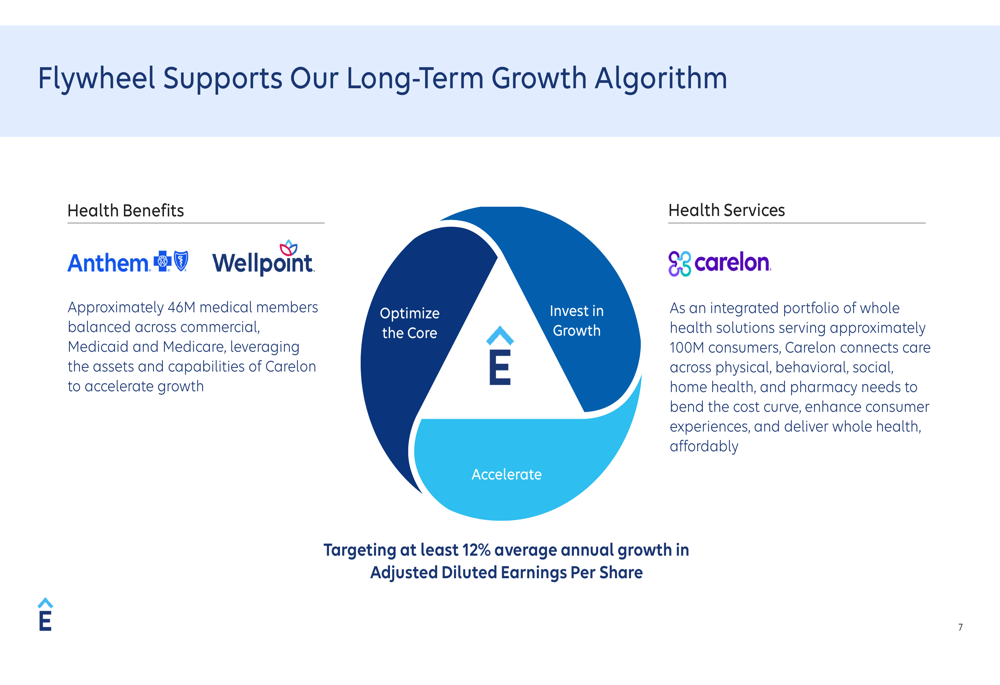

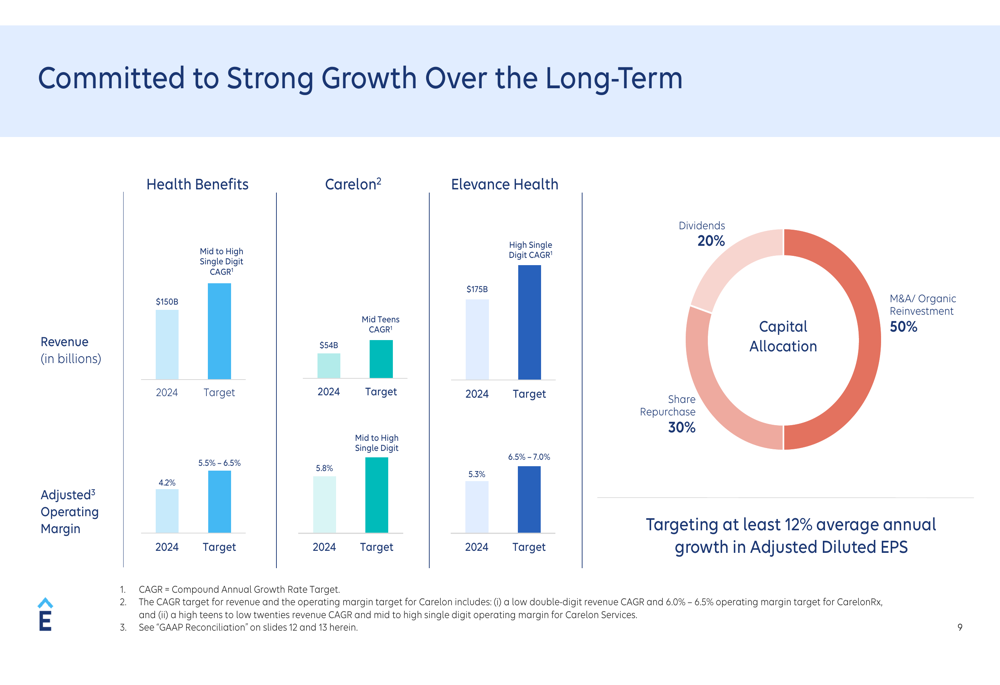

Despite near-term challenges, Elevance Health remains committed to its long-term growth strategy. The company’s growth algorithm targets at least 12% average annual growth in adjusted diluted EPS, supported by its enterprise flywheel approach.

The company’s growth strategy is illustrated in this flywheel model:

This approach leverages the synergies between the Health Benefits segment, serving approximately 46 million medical members, and the Carelon segment, which provides whole health solutions to approximately 100 million consumers. The integration of these segments is designed to enhance consumer experiences while bending the cost curve.

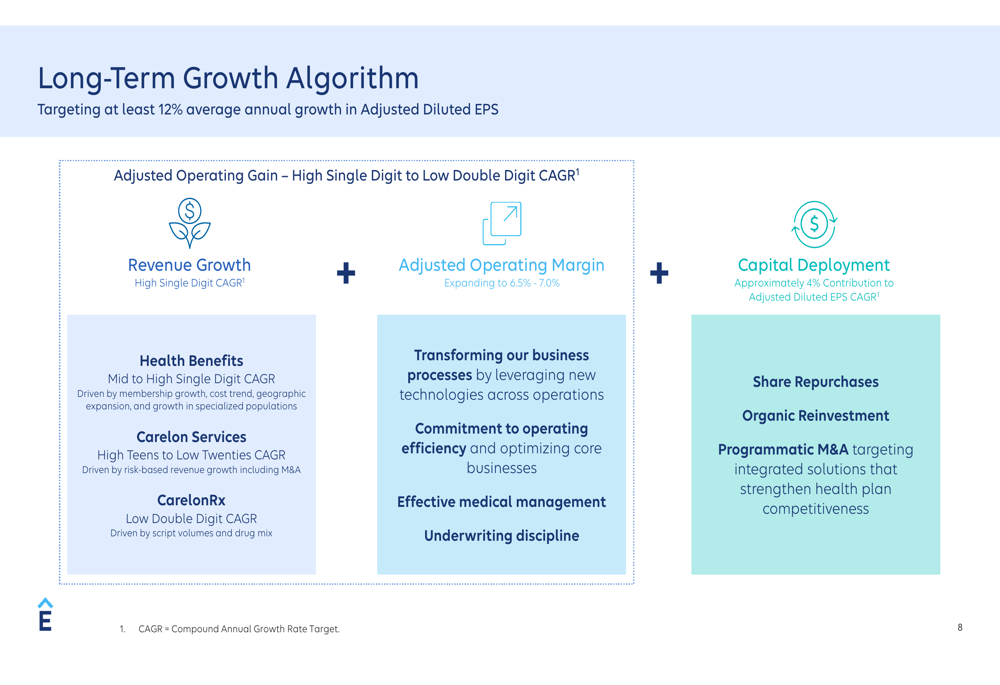

The detailed growth algorithm shows how Elevance Health plans to achieve its targets:

The company expects high single-digit to low double-digit compound annual growth rate (CAGR) in adjusted operating gain, driven by high single-digit revenue growth and expanding operating margins. Capital deployment, including share repurchases and strategic M&A, is expected to contribute approximately 4% to the adjusted diluted EPS CAGR.

Long-term financial targets include:

Elevance Health aims to achieve a high single-digit CAGR in overall revenue, reaching $175 billion, with an adjusted operating margin of 6.5% to 7.0%. The Health Benefits segment targets mid to high single-digit CAGR with revenue of $150 billion and margins of 5.5% to 6.5%, while Carelon aims for mid-teens CAGR with revenue of $54 billion and margins of 5.3% to 5.8%.

The company’s capital allocation strategy balances shareholder returns with growth investments, allocating 20% to dividends, 30% to share repurchases, and 50% to M&A and organic reinvestment.

While Elevance Health’s second quarter results and revised guidance present near-term challenges, management remains focused on executing its long-term strategy to strengthen performance and drive sustainable growth through disciplined pricing, expansion of Carelon, and development of value-based care models.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.