Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

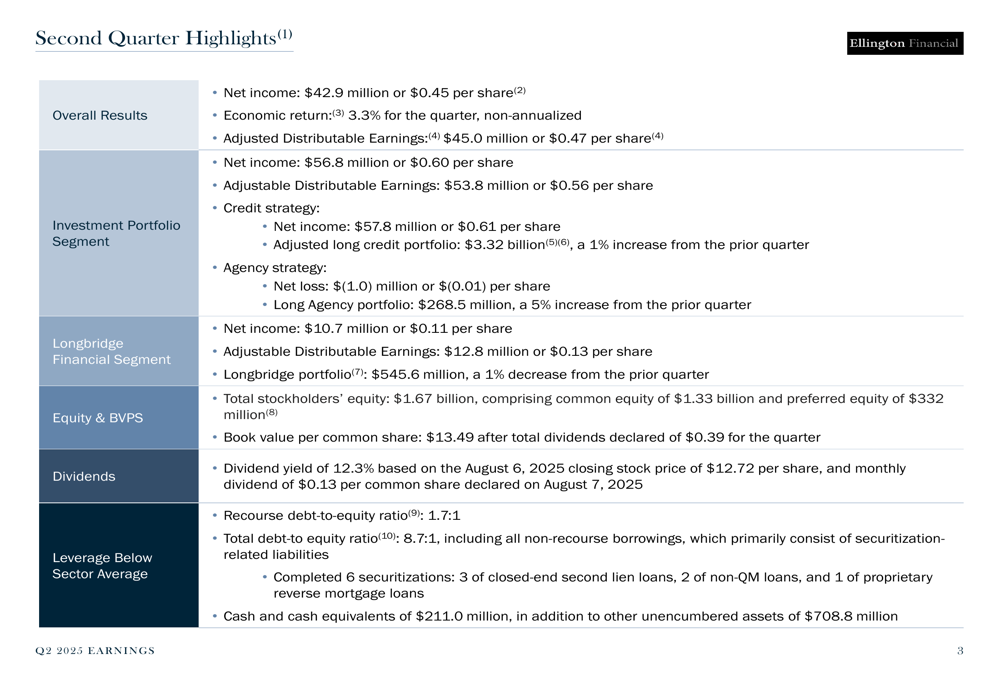

Ellington Financial Inc. (NYSE:EFC) presented its second quarter 2025 earnings results on August 8, 2025, reporting net income of $42.9 million or $0.45 per share. The company’s stock closed at $12.66 on August 7, down 0.47% ahead of the earnings presentation, with shares trading within a 52-week range of $11.12 to $14.40.

The Q2 results show a sequential decline from the first quarter’s EPS of $0.55, though adjusted distributable earnings improved from $0.39 in Q1 to $0.47 in Q2. The company maintained its strong dividend yield of 12.3% based on the August 6 closing price of $12.72 per share.

Quarterly Performance Highlights

Ellington Financial reported an economic return of 3.3% (non-annualized) for the second quarter, with book value per common share standing at $13.49. The company’s total stockholders’ equity reached $1.67 billion, comprising $1.33 billion in common equity and $332 million in preferred equity.

The presentation highlighted strong performance across the company’s three main segments:

1. Investment Portfolio: Generated net income of $56.8 million ($0.60 per share) and adjusted distributable earnings of $53.8 million ($0.56 per share)

2. Credit Strategy: Produced net income of $57.8 million with an adjusted long credit portfolio of $3.32 billion (1% increase)

3. Longbridge Financial: Delivered net income of $10.7 million ($0.11 per share) and adjusted distributable earnings of $12.8 million ($0.13 per share)

As shown in the following comprehensive performance summary:

The company maintained a conservative leverage profile with a recourse debt-to-equity ratio of 1.7:1 and total debt-to-equity ratio of 8.7:1. Cash and cash equivalents stood at $211.0 million, providing ample liquidity for operations and investment opportunities.

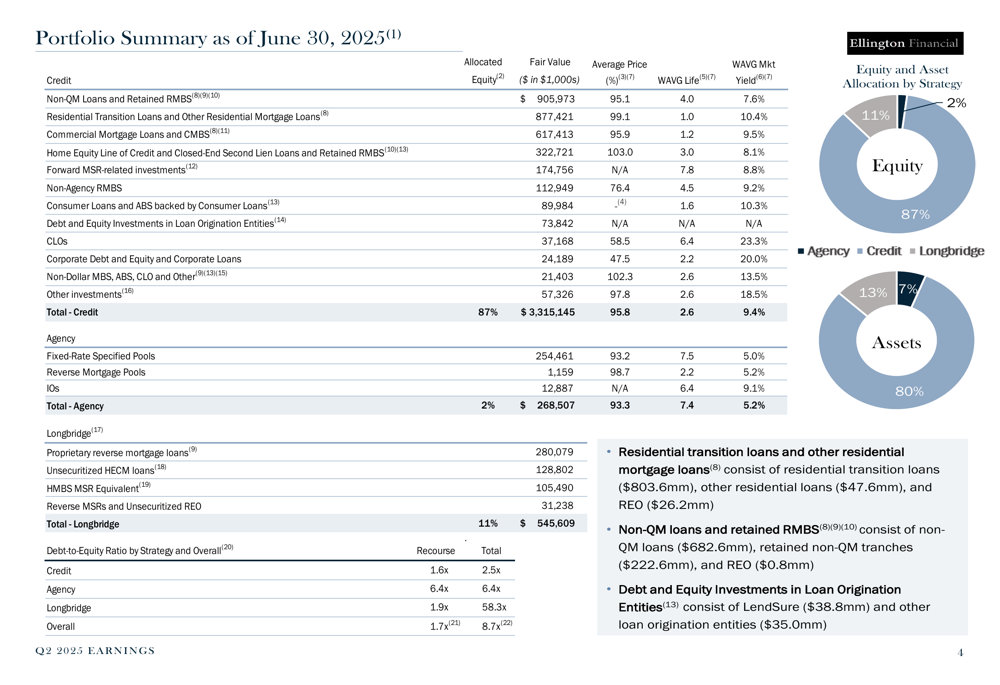

Portfolio Strategy & Composition

Ellington Financial’s portfolio allocation remained heavily weighted toward credit investments, with 87% allocated to credit, 2% to agency, and 11% to Longbridge. The total portfolio fair value reached $4.13 billion as of June 30, 2025.

The detailed breakdown of the company’s portfolio shows significant diversification across asset classes:

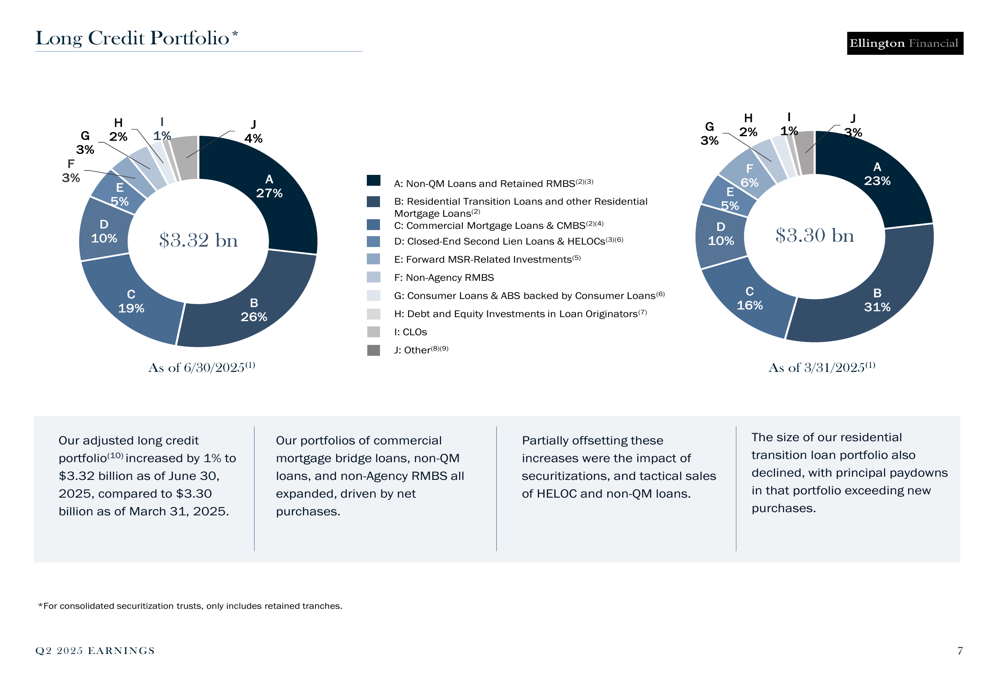

Within the credit portfolio, notable shifts occurred during the quarter. The company increased its allocation to non-QM loans and retained RMBS to 27% (from 23% in the previous quarter) and commercial mortgage loans and CMBS to 19% (from 16%), while reducing exposure to residential transition loans to 26% (from 31%).

As illustrated in the following chart showing the evolution of the long credit portfolio:

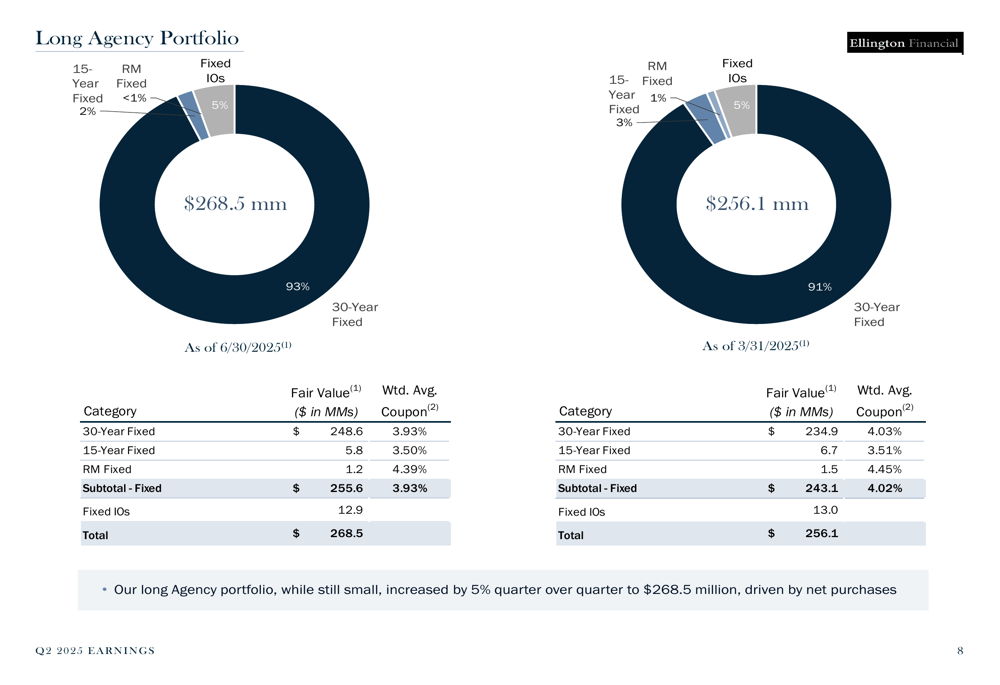

The agency portfolio, while representing just 2% of allocated equity, increased by 5% quarter-over-quarter to $268.5 million, driven by net purchases. The portfolio remained predominantly invested in 30-year fixed-rate securities (93%).

Commercial Mortgage and Loan Origination Strategy

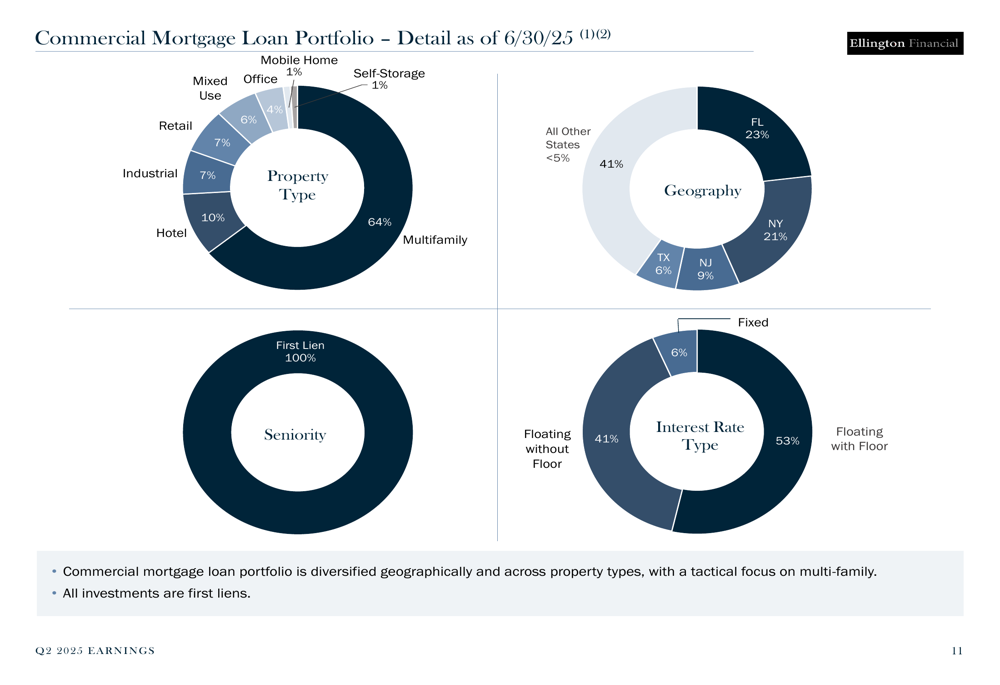

A key strategic focus for Ellington Financial has been its commercial mortgage loan portfolio, which is well-diversified across property types and geography. Multifamily properties represent the largest segment at 64%, followed by hotels (10%) and industrial properties (7%). Geographically, Florida (23%), New York (21%), and New Jersey (9%) account for the largest state exposures.

The following chart illustrates the commercial mortgage loan portfolio composition:

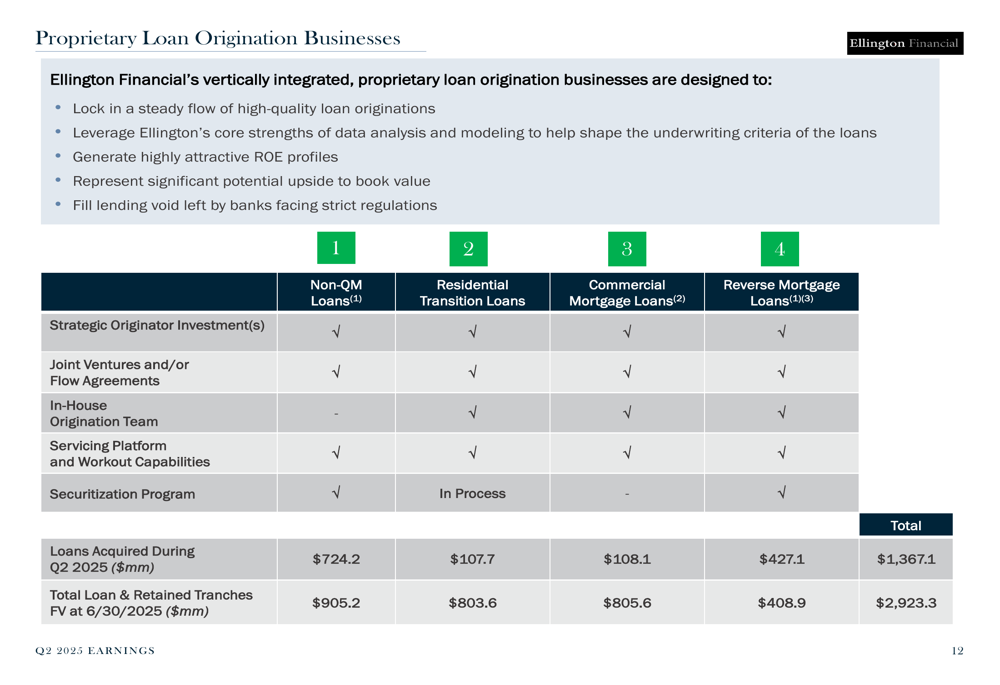

The company’s proprietary loan origination businesses showed strong activity across multiple segments during Q2 2025:

- Non-QM Loans: Acquired $724.2 million

- Residential Transition Loans: Acquired $107.7 million

- Commercial Mortgage Loans: Acquired $108.1 million

- Reverse Mortgage Loans: Acquired $427.1 million

Risk Management & Competitive Position

Ellington Financial emphasized its risk management approach through dynamic interest rate and credit hedging strategies. The company’s interest rate sensitivity analysis shows a relatively balanced exposure to rate movements, with estimated changes in fair value for a 50 basis point move in either direction largely offset by hedging instruments.

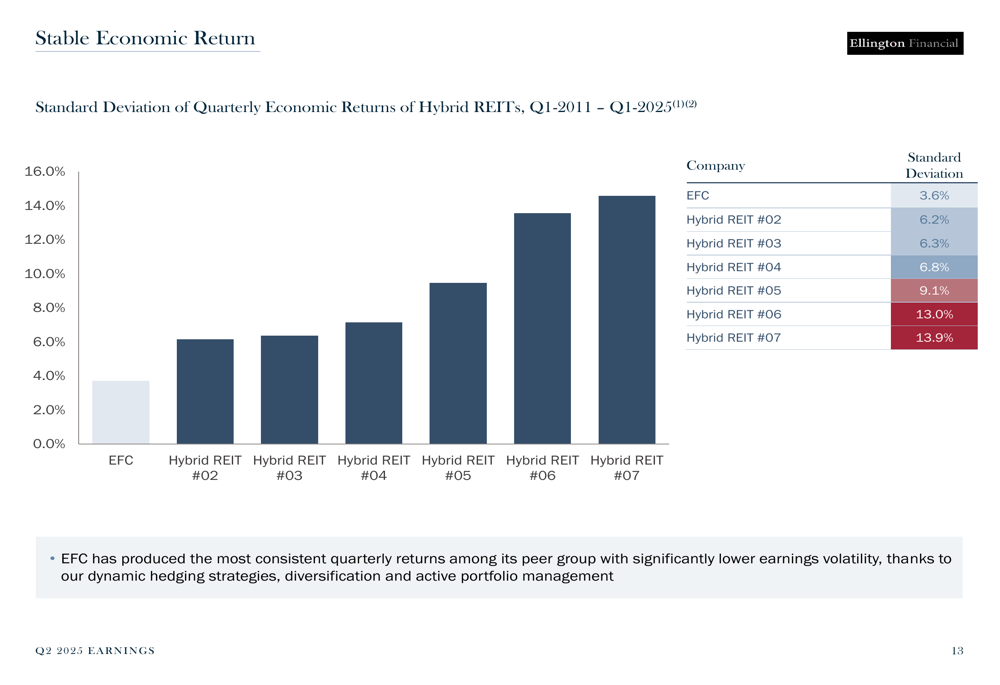

A standout competitive advantage highlighted in the presentation is the company’s stable economic returns compared to peers. With a standard deviation of quarterly economic returns of just 3.6% (from Q1 2011 to Q1 2025), EFC has demonstrated significantly lower volatility than its peer group, where standard deviations range from 6.2% to 13.9%.

The following chart illustrates this competitive advantage:

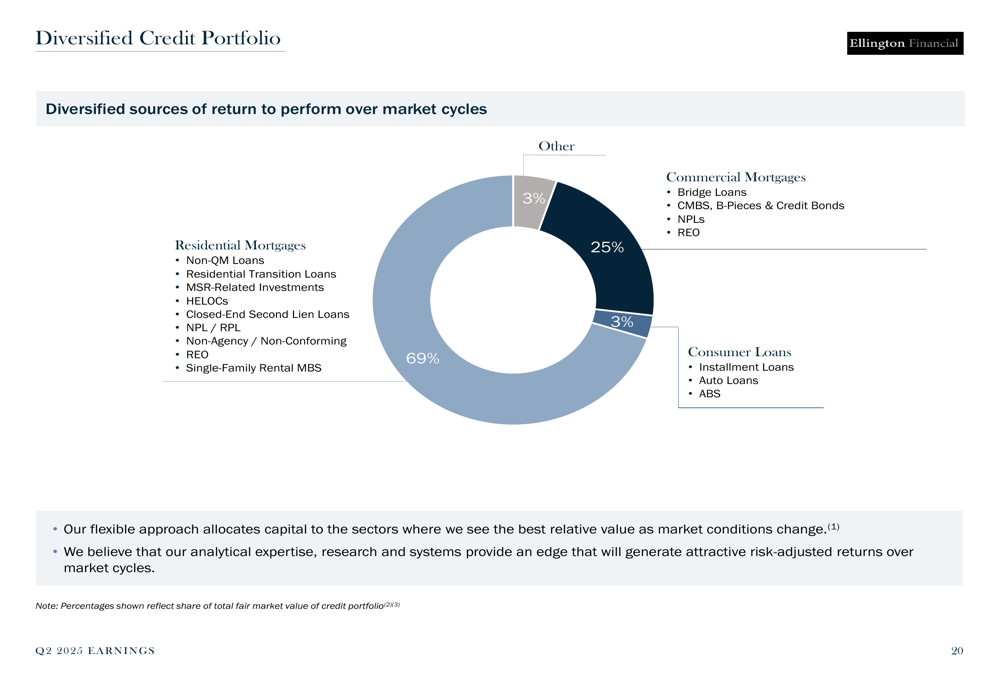

The company’s credit portfolio remains well-diversified, with 69% in residential mortgages, 25% in commercial mortgages, 3% in consumer loans, and 3% in other investments. This diversification strategy has contributed to the stability of returns over market cycles.

Long-Term Performance & Forward Outlook

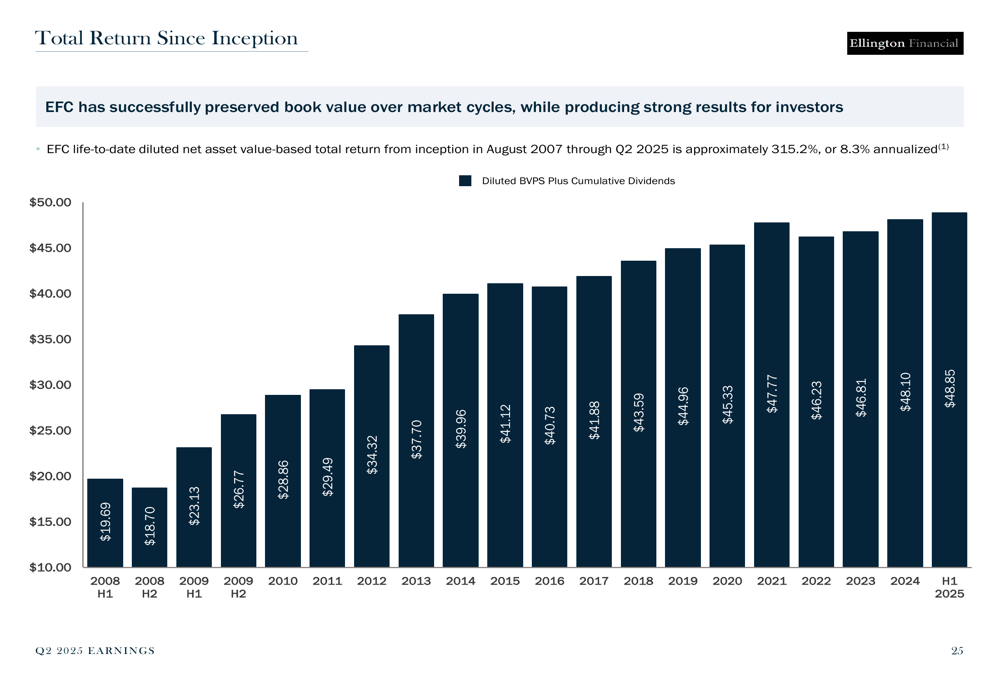

Ellington Financial’s presentation emphasized its track record of preserving book value while delivering strong returns to investors since inception. The company’s book value per share plus cumulative dividends has grown from $19.69 in 2008 to $48.85 in 2025, demonstrating resilience through multiple market cycles including the Credit Crisis, Taper Tantrum, and COVID-19 pandemic.

As shown in the following chart of total return since inception:

Looking forward, the company plans to continue its focus on proprietary loan origination businesses while maintaining its dynamic hedging strategies. Management highlighted opportunities created by market volatility, consistent with comments from the Q1 earnings call where CEO Larry Penn noted that "current high levels of volatility are recharging the opportunity set and creating compelling trading opportunities."

The company’s commitment to ESG principles was also highlighted, with focus areas including mass transportation, energy conservation, investing in home mortgage loans, and operating under a Code of Business Conduct and Ethics with an independent board chairman.

While the presentation maintained an optimistic tone, investors should note the quarter-over-quarter decline in EPS from $0.55 in Q1 to $0.45 in Q2, which may indicate some headwinds in the current operating environment. Nevertheless, the company’s diversified portfolio, consistent dividend yield, and strong risk management approach position it to navigate market uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.