Instacart downgraded as competition tightening grip on online grocery

Introduction & Market Context

Elopak ASA (OB:ELO), the world’s largest player in fresh liquid carton packaging, reported its first quarter 2025 results on May 7, showcasing record revenue performance driven by exceptional growth in the Americas segment. The company, which produces 16 billion cartons annually and sells to over 70 markets globally, continues to execute its strategic expansion in North America while navigating competitive pressures in Europe.

Elopak shares closed at 42.40 NOK on May 6, down 1.4% ahead of the earnings release, and have traded between 33.55 NOK and 47.90 NOK over the past 52 weeks.

Quarterly Performance Highlights

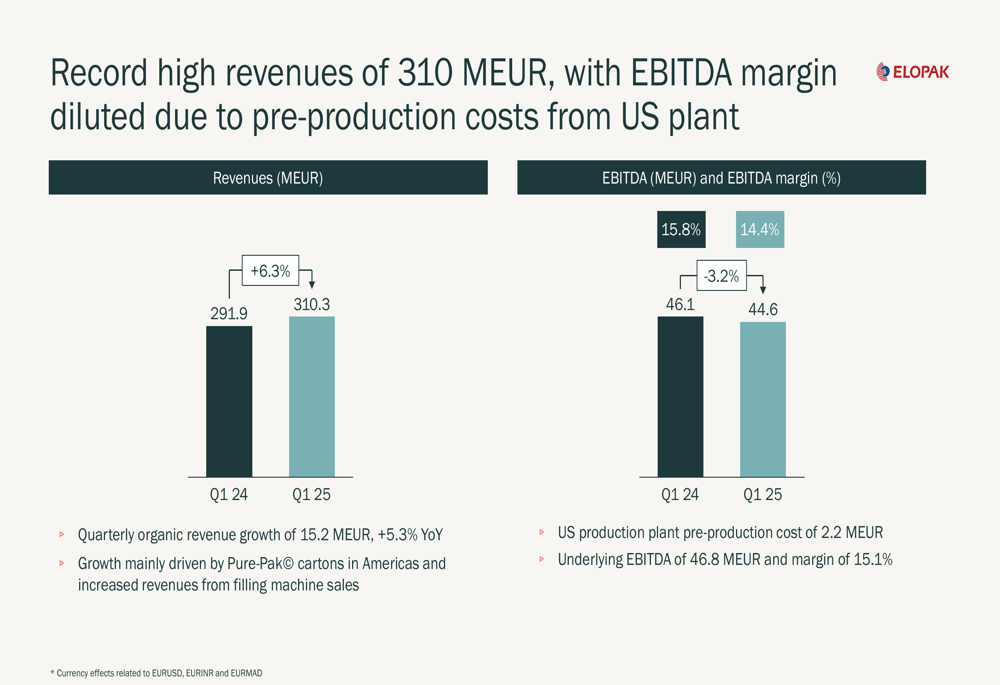

Elopak achieved a significant milestone in Q1 2025, surpassing 300 million euros in quarterly revenue for the first time in company history. Total (EPA:TTEF) revenue reached 310.3 million euros, representing 6.3% reported growth and 5.2% organic growth compared to the same period last year.

Despite the strong top-line performance, EBITDA decreased slightly to 44.6 million euros with a margin of 14.4%, compared to 46.1 million euros and 15.8% margin in Q1 2024. The company attributed this margin pressure primarily to 2.2 million euros in pre-production costs related to its new US plant. Excluding these costs, underlying EBITDA would have been 46.8 million euros with a 15.1% margin.

As shown in the following chart of quarterly revenue and EBITDA performance:

The company’s earnings per share declined 21% year-over-year to 0.06 euros, while ROCE decreased from 17.4% to 15.1%. Cash flow from operations saw a significant drop from 29 million euros to just 5 million euros, primarily due to investments in the US production plant and a temporary build-up of working capital.

Regional Performance Analysis

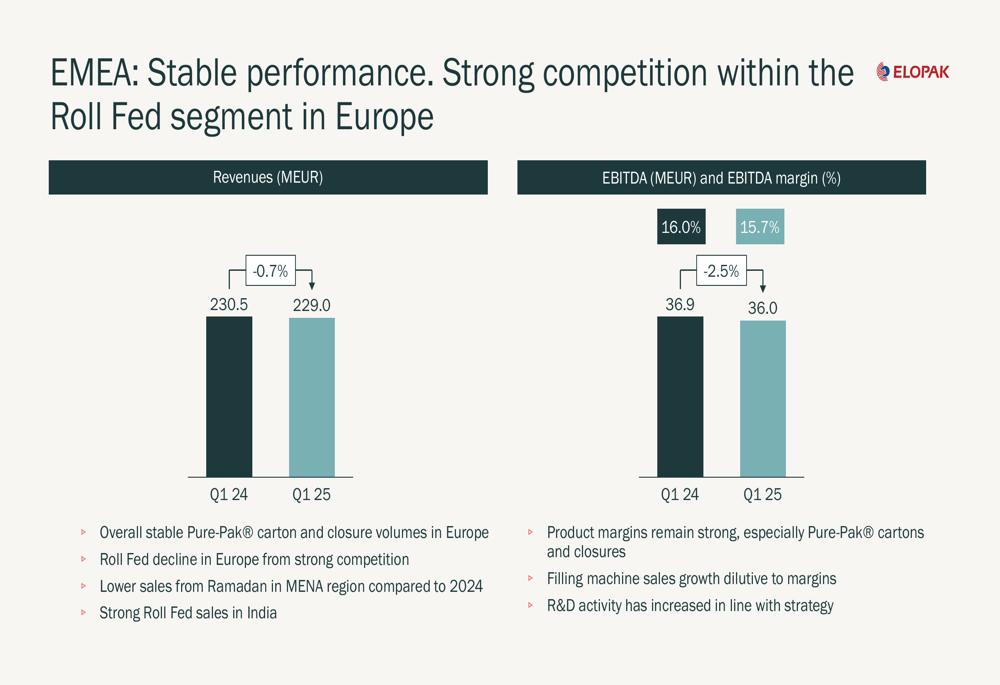

Elopak’s performance showed a stark contrast between its two main regions. The EMEA segment, which accounts for 73% of total revenue, delivered stable results with revenue of 229.0 million euros, down slightly by 0.7% compared to Q1 2024. EBITDA in the region reached 36.0 million euros with a 15.7% margin, representing a 2.5% decrease year-over-year.

The company noted strong competition within the Roll Fed segment in Europe, while Pure-Pak carton and closure volumes remained stable. Lower sales during Ramadan in the MENA region compared to 2024 also impacted regional performance, though this was partially offset by strong Roll Fed sales in India.

As illustrated in the EMEA performance breakdown:

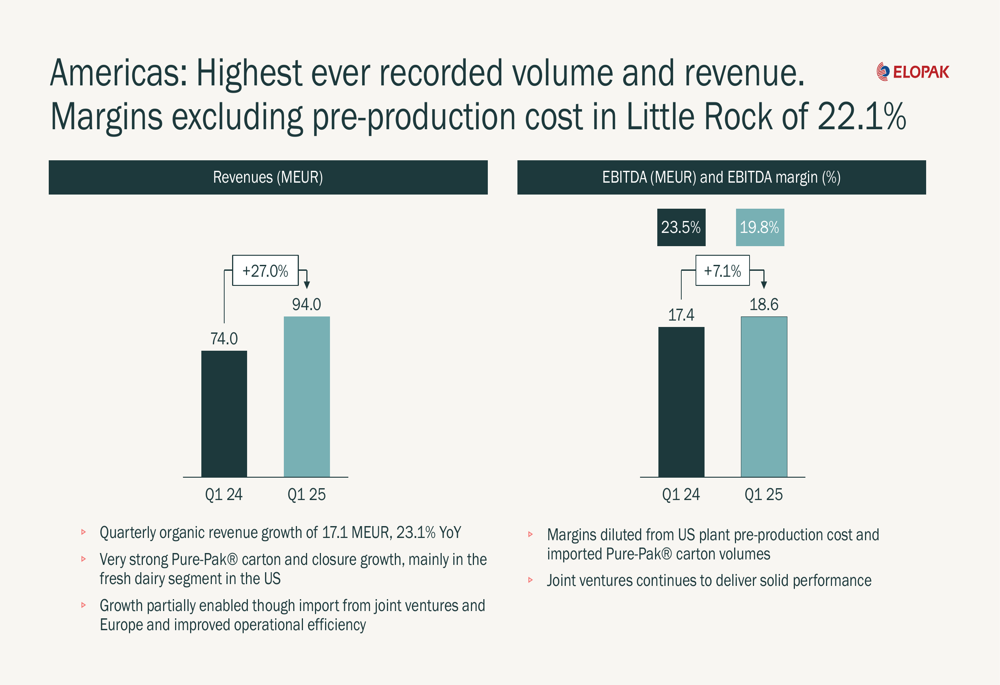

In contrast, the Americas segment delivered exceptional results, achieving its highest ever recorded volume and revenue. Revenue in the region surged 27.0% to 94.0 million euros, with organic growth of 23.1% year-over-year. EBITDA increased 7.1% to 18.6 million euros, though the margin declined to 19.8% from 23.5% in Q1 2024 due to US plant pre-production costs and imported Pure-Pak carton volumes.

The following chart highlights the strong performance in the Americas segment:

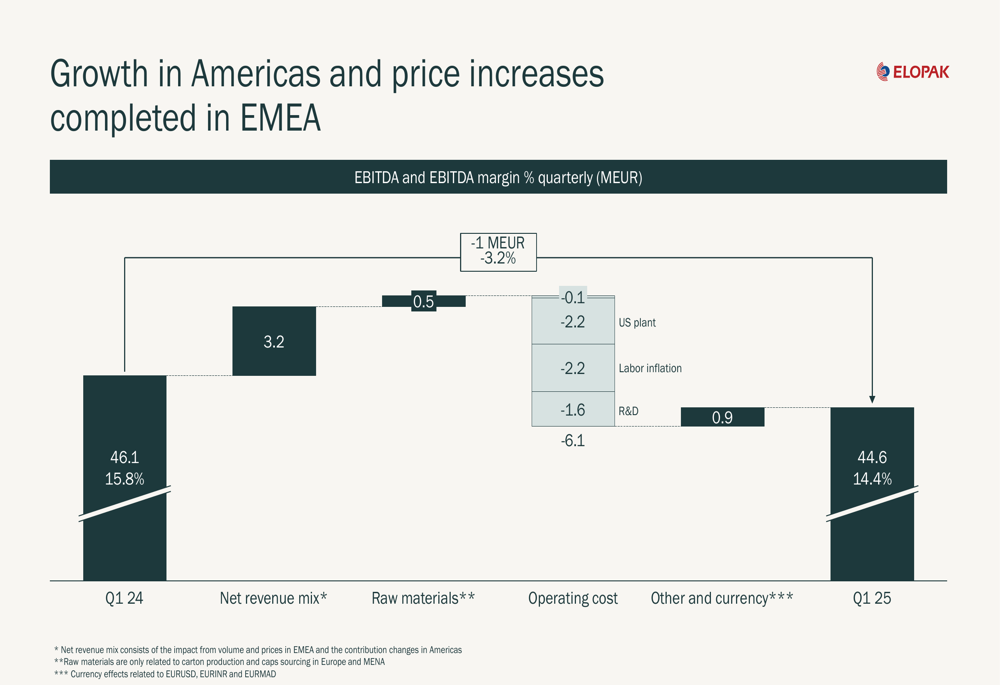

The company’s EBITDA bridge analysis reveals how various factors impacted overall performance, with positive contributions from revenue mix and raw materials offset by increased operating costs:

Strategic Initiatives

A key milestone for Elopak this quarter was the grand opening of its new production plant in Little Rock, Arkansas, on April 30. The facility was completed on time and within budget, with commercial production set to begin in Q2 2025. This expansion represents a significant strategic investment to strengthen Elopak’s position in the North American market.

The company highlighted its unique positioning to navigate potential tariff challenges in North America, noting that its production plants in Canada, USA, and Mexico are all currently exempted from tariffs under the United States-Mexico-Canada Agreement (USMCA). The new Little Rock plant provides additional flexibility to optimize supply to US customers in case of tariff developments.

Elopak also announced a partnership with Blue Ocean Closures, a Swedish technology company that develops fiber-based closures, reinforcing the company’s commitment to sustainable packaging solutions. This aligns with Elopak’s strategic priorities to realize global growth potential, strengthen leadership in core markets, and leverage the shift away from plastic packaging.

Financial Position & Outlook

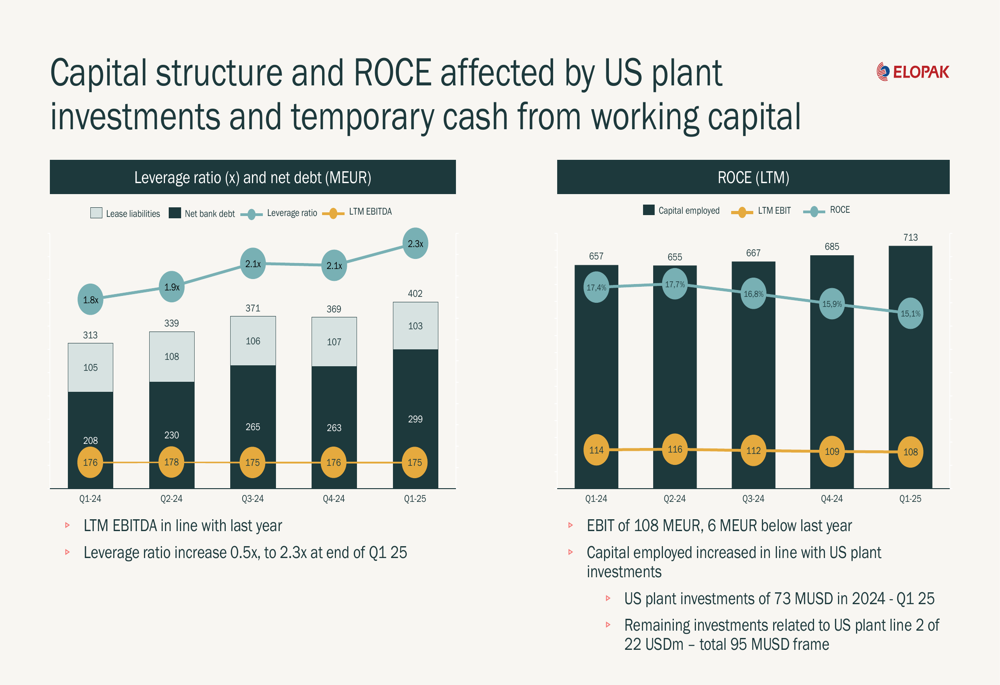

Elopak’s balance sheet has come under pressure as the company continues to invest in its US expansion. Capital expenditures more than doubled year-over-year to 25 million euros, while net debt increased 28% to 402 million euros. The leverage ratio rose to 2.3x at the end of Q1 2025, up from 1.8x a year earlier.

The following chart illustrates the evolution of Elopak’s capital structure and ROCE:

Despite these pressures, management expressed confidence in the company’s financial position, stating that "the balance sheet remains solid, despite continued investments in US plant and temporary build-up of working capital." The company expects to "continue the strong performance from Q1 for the full-year 2025."

Total investments related to the US plant are projected to reach 95 million USD, with 73 million USD already invested through Q1 2025 and the remaining 22 million USD allocated for the second production line.

With its record revenue performance, strategic expansion in the Americas, and continued focus on sustainable packaging solutions, Elopak appears well-positioned for growth despite near-term margin pressures and increased leverage. Investors will be watching closely to see if the company can maintain its revenue momentum while improving profitability as the new US plant begins commercial production in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.