Cigna earnings beat by $0.04, revenue topped estimates

Introduction & Market Context

EMCOR Group Inc . (NYSE:EME) presented its first quarter 2025 financial results during an earnings call on April 30, 2025, showcasing strong performance across most business segments. The company, which specializes in electrical and mechanical construction, industrial and energy infrastructure, and building services, reported significant year-over-year growth in revenue and earnings, primarily driven by its construction segments and the integration of its Miller Electric acquisition.

EMCOR’s stock has shown resilience in 2025, trading at $413.02 as of April 29, 2025, with a 0.67% increase on the day. The company’s shares have been trading in a 52-week range of $319.49 to $545.29, indicating significant volatility but overall strength in the market.

Quarterly Performance Highlights

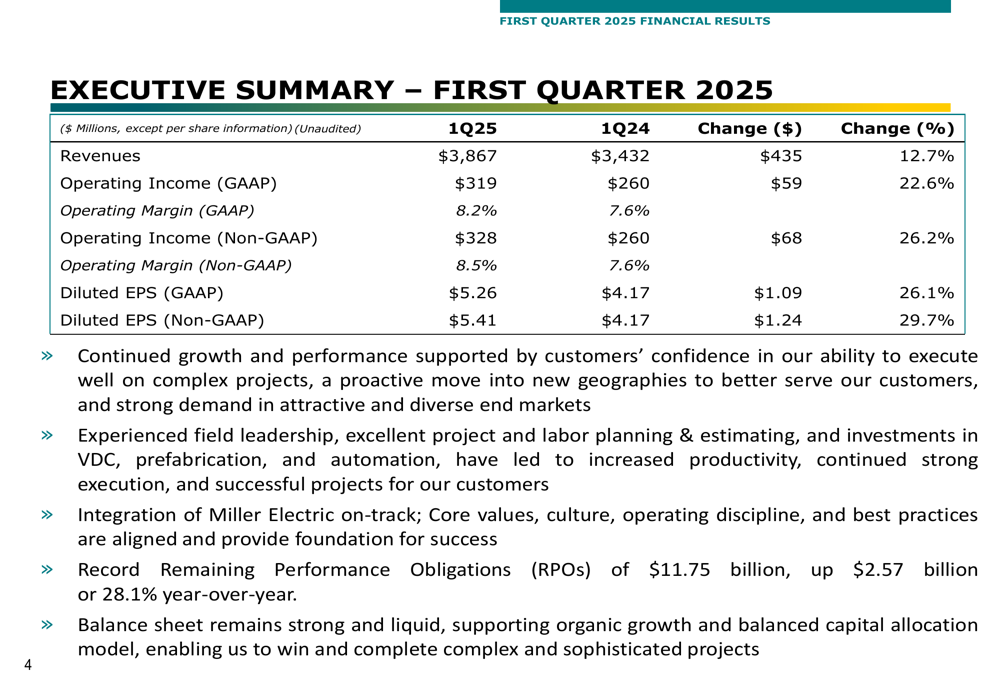

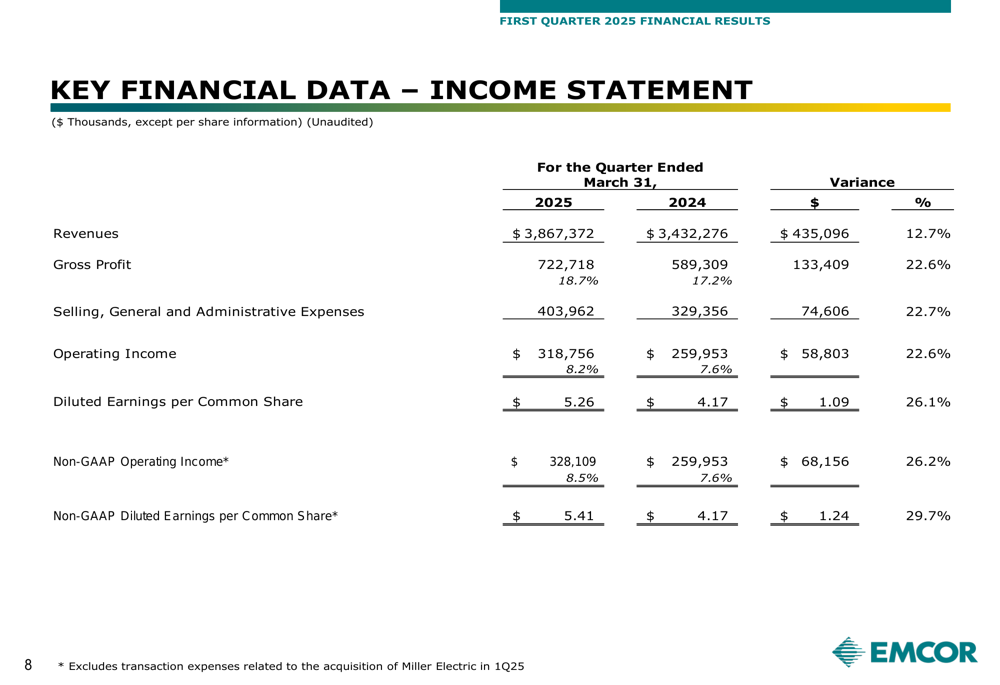

EMCOR reported record consolidated quarterly revenues of $3.87 billion for Q1 2025, representing a 12.7% increase from $3.43 billion in Q1 2024. GAAP operating income rose 22.6% to $319 million, with operating margin expanding to 8.2%. On a non-GAAP basis, which excludes transaction expenses related to the Miller Electric acquisition, operating income increased 26.2% to $328 million with an 8.5% margin.

Diluted earnings per share (EPS) showed impressive growth, with GAAP EPS up 26.1% to $5.26 and non-GAAP EPS up 29.7% to $5.41 compared to $4.17 in the same period last year.

As shown in the following summary of key financial metrics:

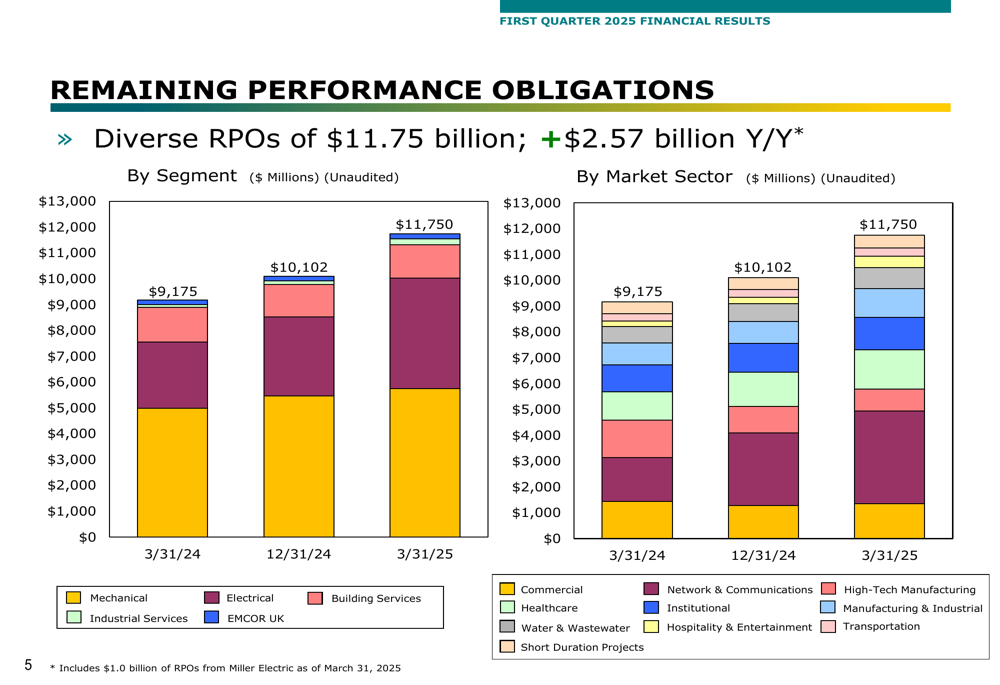

The company’s Remaining Performance Obligations (RPOs) reached a record $11.75 billion, up 28.1% year-over-year, providing strong visibility for future revenues. This includes $1.0 billion of RPOs from the recently acquired Miller Electric.

The following chart breaks down RPOs by segment and market sector:

Segment Performance Analysis

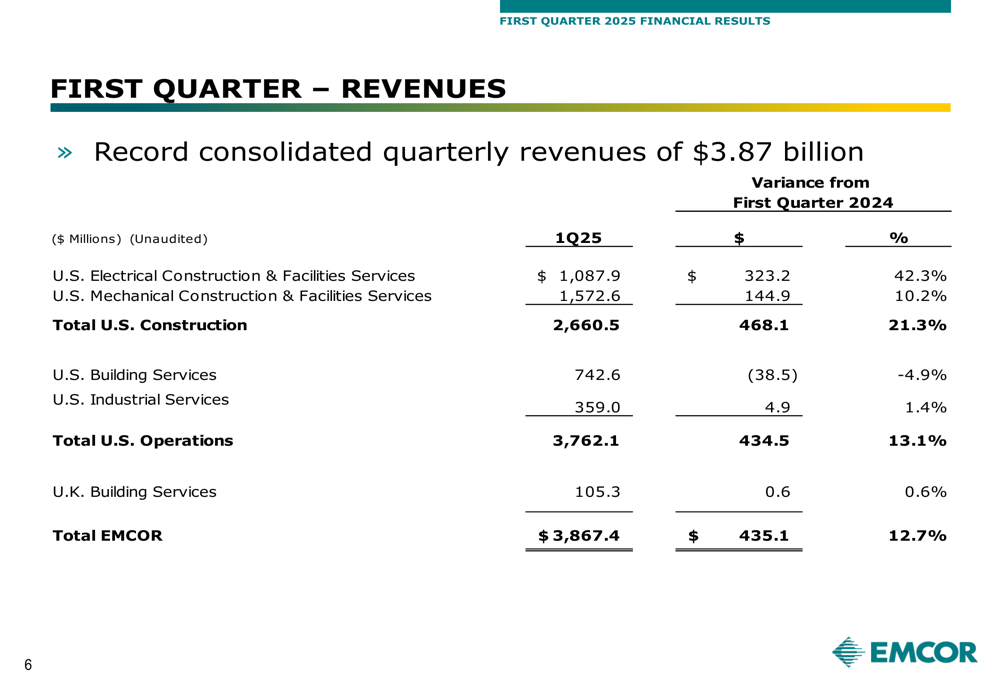

EMCOR’s U.S. Electrical Construction & Facilities Services segment was the standout performer, with revenues surging 42.3% to $1.09 billion, bolstered by the Miller Electric acquisition. The U.S. Mechanical Construction & Facilities Services segment also performed well, with revenues increasing 10.2% to $1.57 billion. Combined, the U.S. Construction segments grew 21.3% to $2.66 billion.

However, not all segments showed growth. U.S. Building Services revenues declined 4.9% to $742.6 million, while U.S. Industrial Services saw a modest 1.4% increase to $359.0 million. The U.K. Building Services segment remained essentially flat with a 0.6% increase to $105.3 million.

The detailed revenue breakdown by segment is illustrated here:

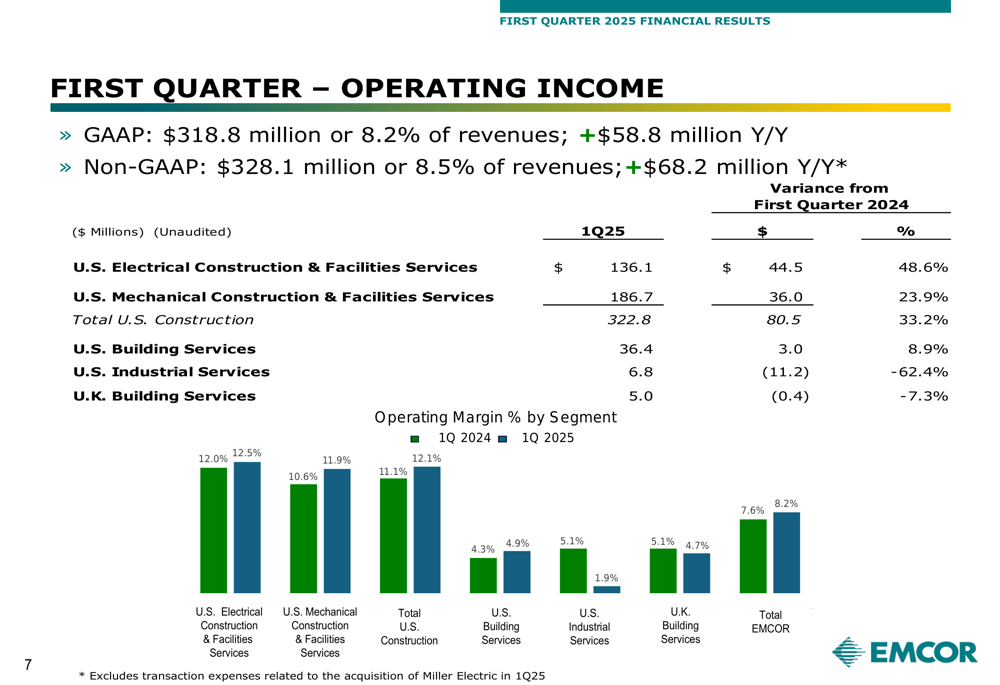

In terms of operating income, the U.S. Construction segments again led the way. U.S. Electrical Construction & Facilities Services operating income increased 48.6% to $136.1 million, while U.S. Mechanical Construction & Facilities Services grew 23.9% to $186.7 million. U.S. Building Services operating income increased 8.9% to $36.4 million despite the revenue decline, indicating improved margins.

However, U.S. Industrial Services operating income declined significantly by 62.4% to $6.8 million, and U.K. Building Services operating income decreased 7.3% to $5.0 million.

The following chart shows operating income by segment and operating margin comparisons:

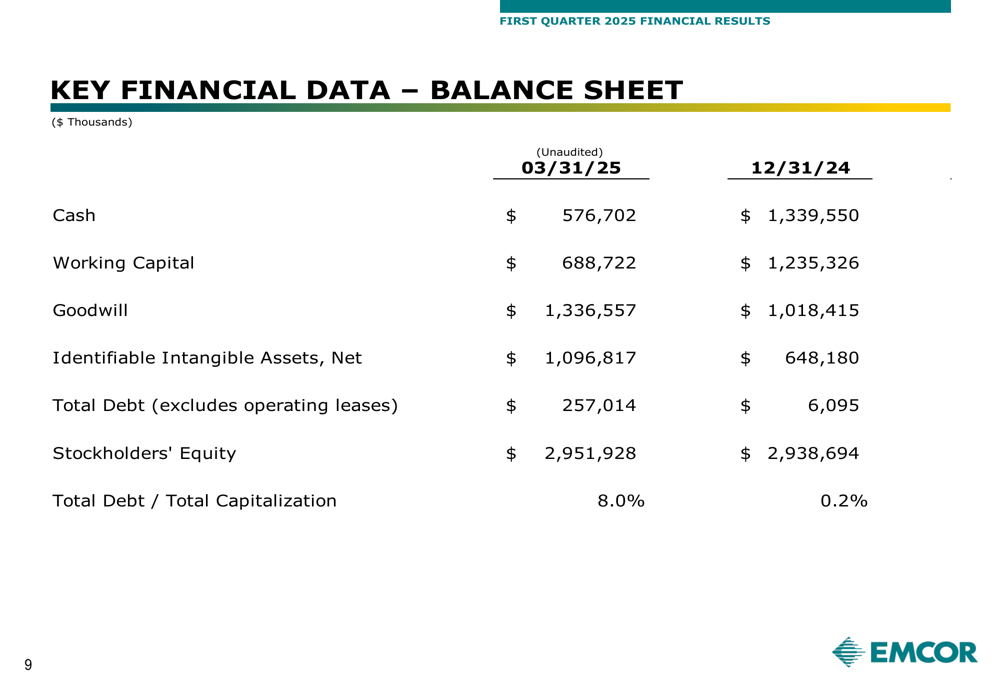

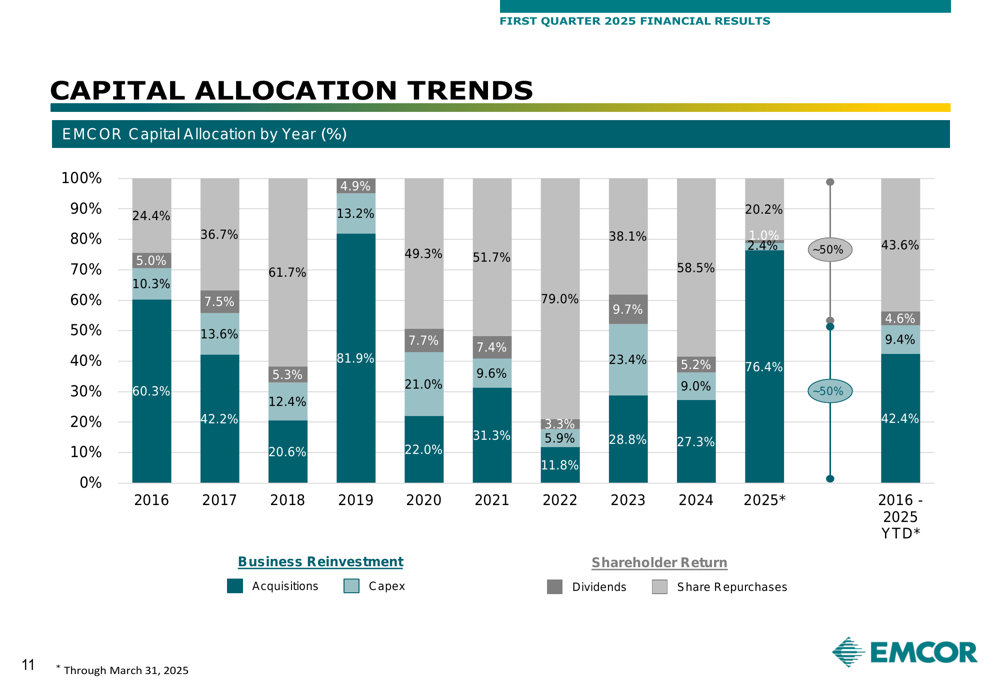

Balance Sheet and Capital Allocation

EMCOR’s balance sheet reflects the impact of the Miller Electric acquisition, with cash decreasing from $1.34 billion at the end of 2024 to $576.7 million as of March 31, 2025. Total (EPA:TTEF) debt (excluding operating leases) increased from $6.1 million to $257.0 million, bringing the total debt to total capitalization ratio to 8.0% from 0.2%.

The acquisition also significantly increased goodwill and identifiable intangible assets, which rose to $1.34 billion and $1.10 billion, respectively.

Key balance sheet figures are presented here:

EMCOR’s capital allocation strategy in 2025 has been heavily weighted toward acquisitions, which represented 76.4% of capital deployment year-to-date through March 31, 2025. This represents a significant shift from the company’s historical allocation patterns, where share repurchases have played a larger role.

The following chart illustrates EMCOR’s capital allocation trends over time:

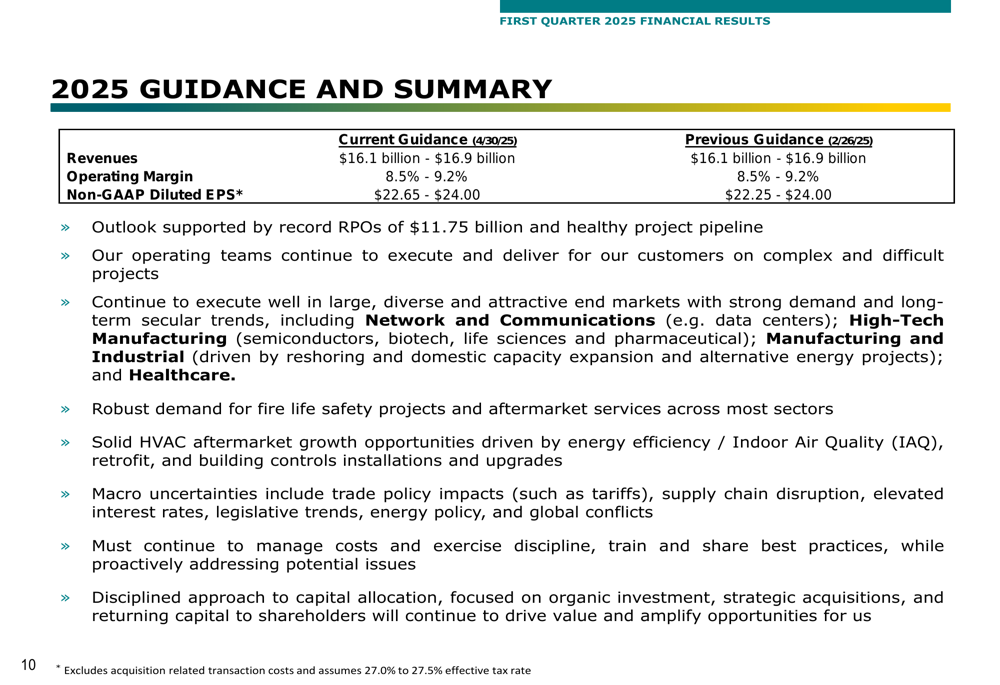

Forward Guidance and Strategic Focus

EMCOR maintained its 2025 revenue guidance of $16.1 billion to $16.9 billion and its operating margin guidance of 8.5% to 9.2%. The company slightly raised the low end of its non-GAAP diluted EPS guidance to $22.65-$24.00, compared to the previous guidance of $22.25-$24.00 provided in February 2025.

The company’s outlook is supported by its record RPOs and healthy project pipeline. EMCOR identified several key strategic focus areas, including Network and Communications, High-Tech Manufacturing, Manufacturing and Industrial, and Healthcare sectors. The company also noted demand for fire life safety projects and aftermarket services, as well as growth opportunities in HVAC.

Management acknowledged macroeconomic uncertainties but emphasized the importance of cost management and a disciplined approach to capital allocation.

The guidance and strategic focus areas are summarized here:

Income Statement Analysis

EMCOR’s condensed income statement shows strong growth across all key metrics. Gross profit increased 22.6% to $722.7 million, outpacing revenue growth and indicating improved project margins. Selling, general and administrative expenses increased 22.7% to $404.0 million, largely in line with gross profit growth.

The detailed income statement comparison is shown below:

Conclusion

EMCOR’s Q1 2025 results demonstrate continued momentum following its strong performance in 2024. The company’s construction segments are driving growth, with the Miller Electric acquisition significantly enhancing its electrical construction capabilities. While some segments faced challenges, particularly U.S. Industrial Services, the overall performance remains robust.

The company’s record RPOs provide visibility for continued growth, though the increased debt levels and reduced cash position following the Miller Electric acquisition will be important to monitor. EMCOR’s maintained guidance suggests management confidence in sustaining performance through 2025 despite acknowledging macroeconomic uncertainties.

With its strategic focus on high-growth sectors and disciplined capital allocation approach, EMCOR appears well-positioned to navigate the current market environment while pursuing long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.