UBS Points to Two Top European Luxury Stocks Ahead of 2026 Upswing

Introduction & Market Context

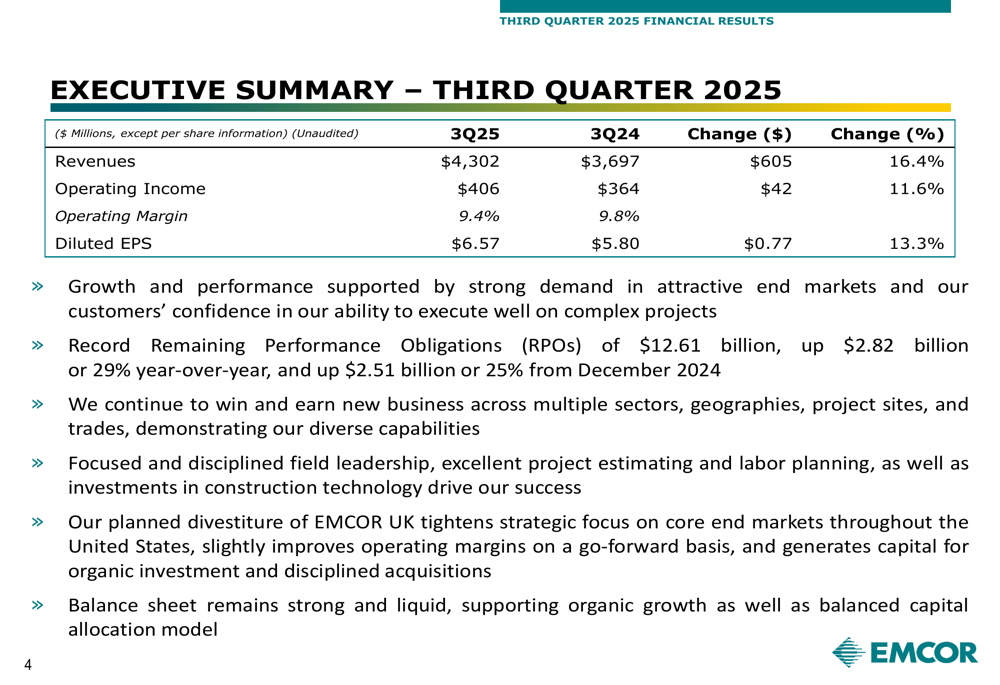

EMCOR Group Inc (NYSE:EME) presented its third quarter 2025 earnings results on October 30, showcasing strong financial performance across key metrics. Despite posting better-than-expected results with revenue and earnings growth, the company's stock tumbled 16.9% in pre-market trading to $697, reflecting broader market concerns that overshadowed the positive financial narrative.

The construction and facilities services provider reported a slight earnings beat with EPS of $6.57 versus analyst expectations of $6.54, while delivering substantial year-over-year growth in both revenue and profitability. The sharp stock decline came despite EMCOR narrowing its full-year guidance toward the higher end of its previous range.

Quarterly Performance Highlights

EMCOR delivered impressive financial results for the third quarter of 2025, with revenue reaching $4.30 billion, representing a 16.4% increase compared to $3.70 billion in the same period last year. Operating income grew to $406 million, up 11.6% year-over-year, though operating margin contracted slightly to 9.4% from 9.8% in Q3 2024.

As shown in the following quarterly performance summary:

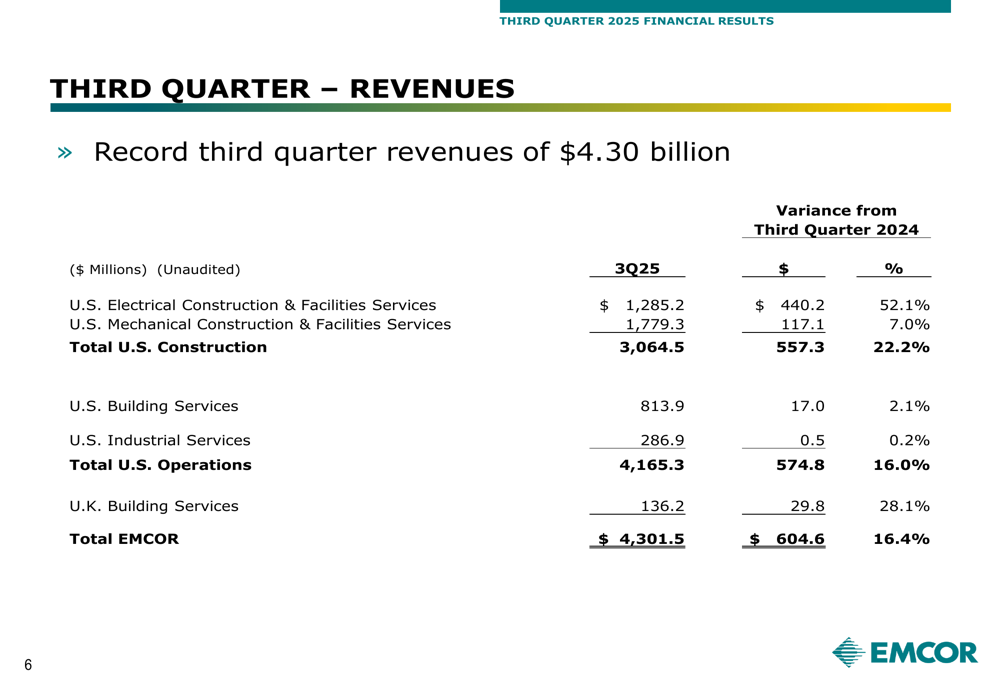

The U.S. Electrical Construction & Facilities Services segment led growth with a remarkable 52.1% revenue increase, reaching $1.29 billion. This was complemented by a 7.0% revenue increase in U.S. Mechanical Construction & Facilities Services to $1.78 billion. The detailed revenue breakdown by segment reveals broad-based growth:

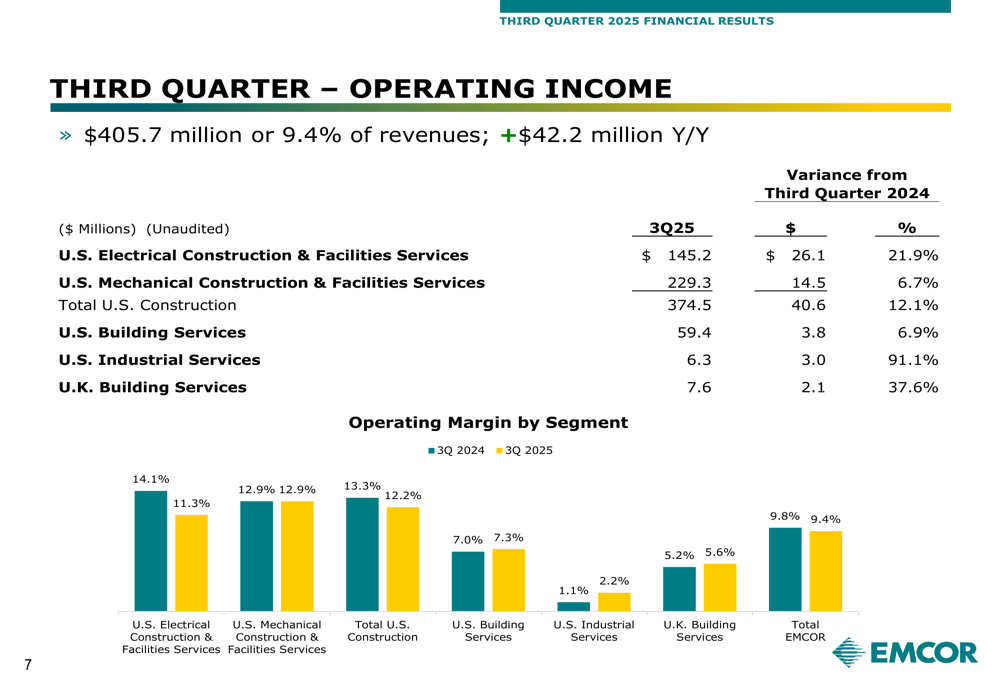

Operating income showed strong performance across segments, with U.S. Industrial Services posting the largest percentage gain at 91.1%, albeit from a smaller base. The company's construction segments continued to drive the majority of profits:

Strategic Initiatives

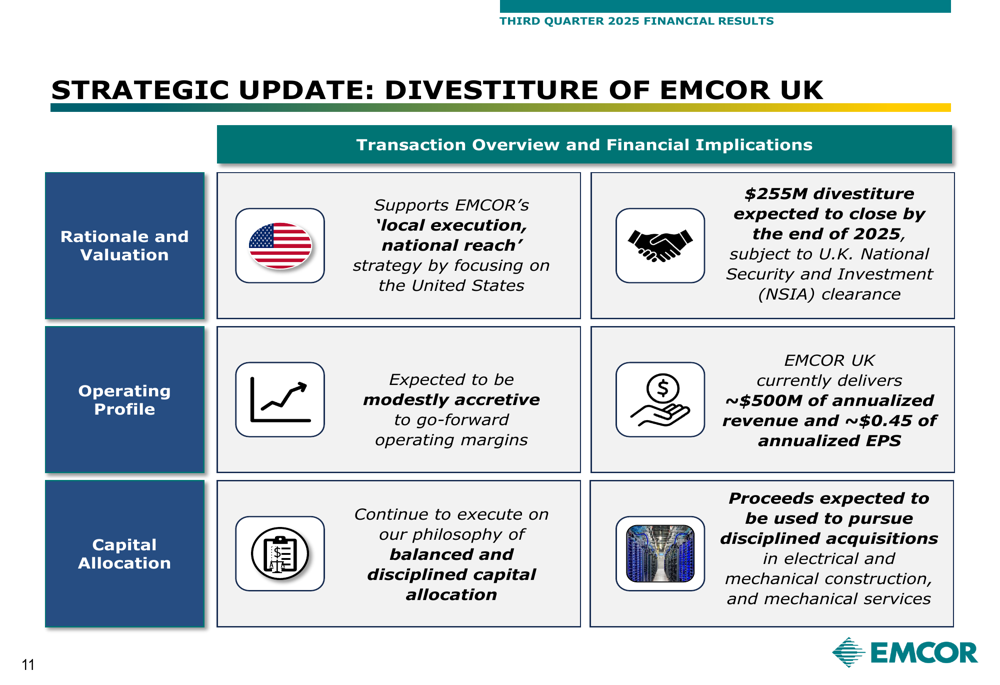

A key strategic announcement in EMCOR's presentation was the planned divestiture of its UK business for $255 million, expected to close by the end of 2025 subject to regulatory approval. The move aligns with the company's "local execution, national reach" strategy, focusing resources on the U.S. market.

The following slide details the strategic rationale behind the divestiture:

EMCOR UK currently contributes approximately $500 million in annualized revenue and $0.45 in annualized EPS. Management indicated the divestiture would be modestly accretive to go-forward operating margins, with proceeds earmarked for disciplined acquisitions in electrical and mechanical construction and mechanical services.

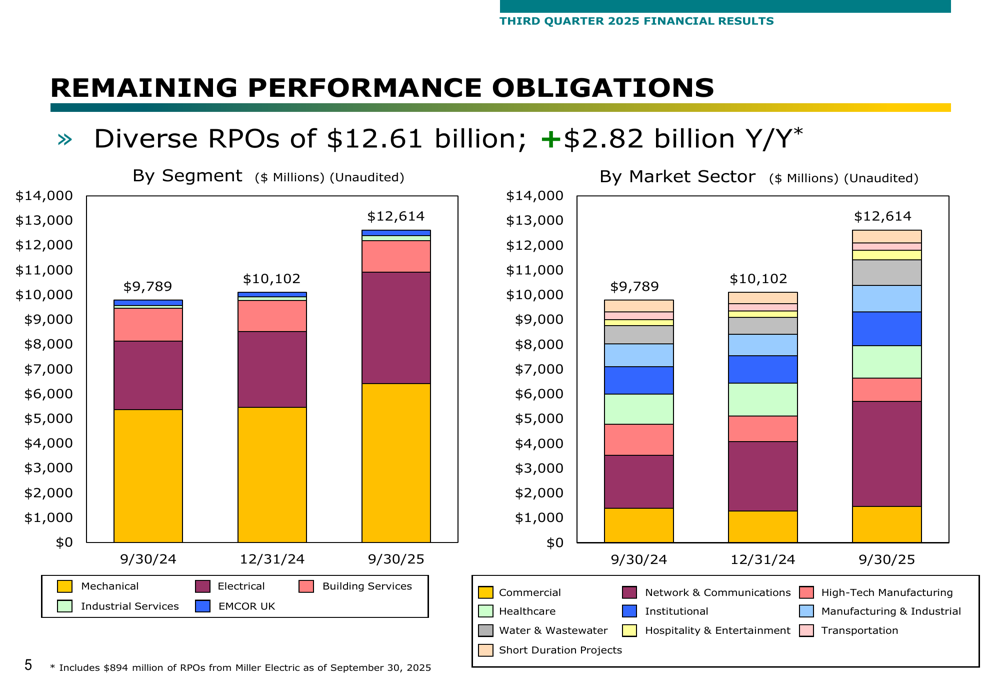

This strategic realignment comes as EMCOR continues to build record backlog levels, with Remaining Performance Obligations (RPOs) reaching $12.61 billion, up $2.82 billion year-over-year. The backlog breakdown shows particular strength in the Mechanical segment:

Forward-Looking Statements

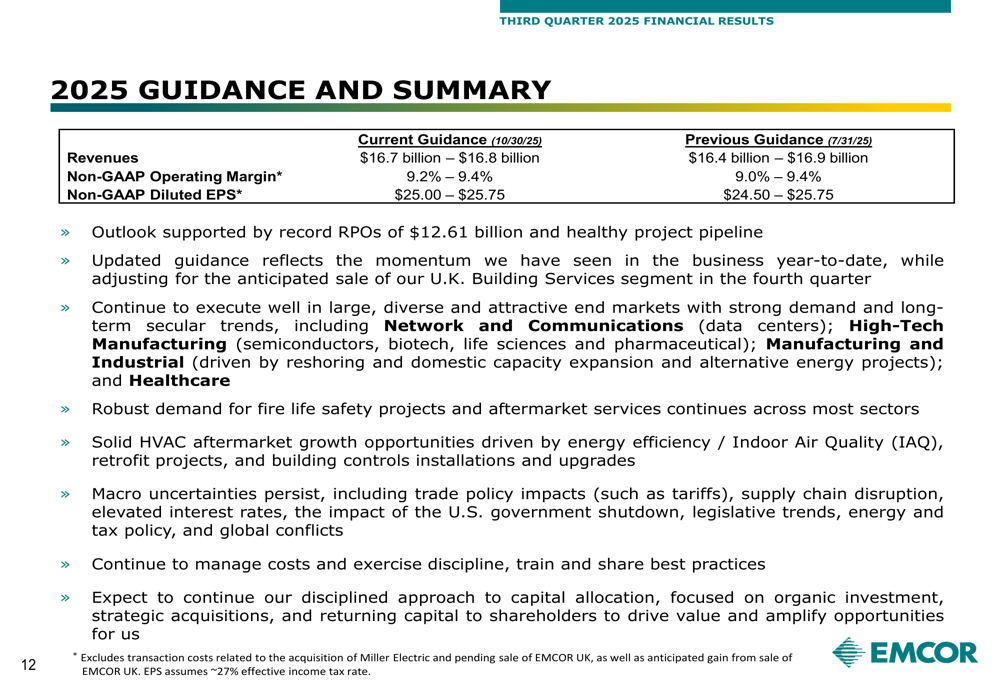

EMCOR narrowed its full-year 2025 guidance, adjusting for the anticipated sale of its UK operations while reflecting strong year-to-date momentum. The company now projects:

The updated guidance suggests confidence in continued strong performance through year-end, supported by the record RPO levels and healthy project pipeline. Management highlighted particular strength in Network and Communications, High-Tech Manufacturing, Manufacturing and Industrial, and Healthcare sectors.

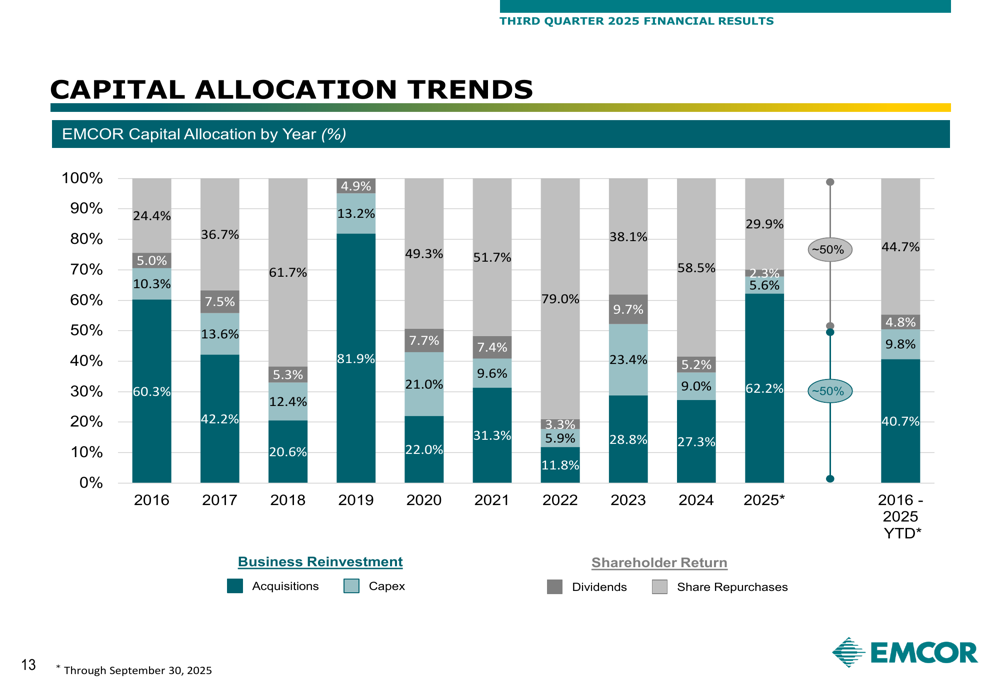

EMCOR's capital allocation strategy continues to balance business reinvestment with shareholder returns, as illustrated in the following chart:

Market Reaction & Analysis

Despite EMCOR's strong financial performance and positive outlook, investors responded negatively, sending the stock down 16.35% during regular trading hours following a 10.3% pre-market decline. The stock closed at $649.96, well off its 52-week high of $778.64.

The disconnect between financial results and stock performance may reflect broader market concerns about the construction sector's future growth prospects amid macroeconomic uncertainties. While EMCOR's backlog provides visibility into future revenue, investors may be questioning the sustainability of growth rates and margins as the company approaches 2026.

The slight compression in operating margin (9.4% vs. 9.8% year-over-year) could also be contributing to investor concerns about cost pressures, despite management's assertion that the UK divestiture would be margin-accretive. Additionally, the significant decrease in cash position from $1.34 billion at the end of 2024 to $655.1 million may have raised questions about capital allocation, though the company maintains a strong balance sheet with minimal debt.

EMCOR's strategic focus on the U.S. market through the UK divestiture represents a significant shift in its international footprint, but appears aligned with its core strengths in construction and facilities services, particularly in high-growth sectors like data centers and healthcare where the company has established competitive advantages.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.