Europe’s Stoxx 600 inches lower amid French political crisis

Introduction & Market Context

EMERGE Commerce Ltd (TSXV:ECOM), a Canadian portfolio company focused on premium brands in the grocery and golf verticals, presented its Q2 2025 results showing significant growth and profitability improvements. The company has successfully transitioned to what it calls "EMERGE 3.0," emphasizing cash flow generation and strategic acquisitions in its core verticals.

Trading at C$0.09 per share, EMERGE has positioned itself to capitalize on two major market opportunities: the growing "Buy Canadian" movement in grocery, which BMO estimates will add $10 billion annually to local consumer spending, and the fragmented golf retail and experiences market.

Quarterly Performance Highlights

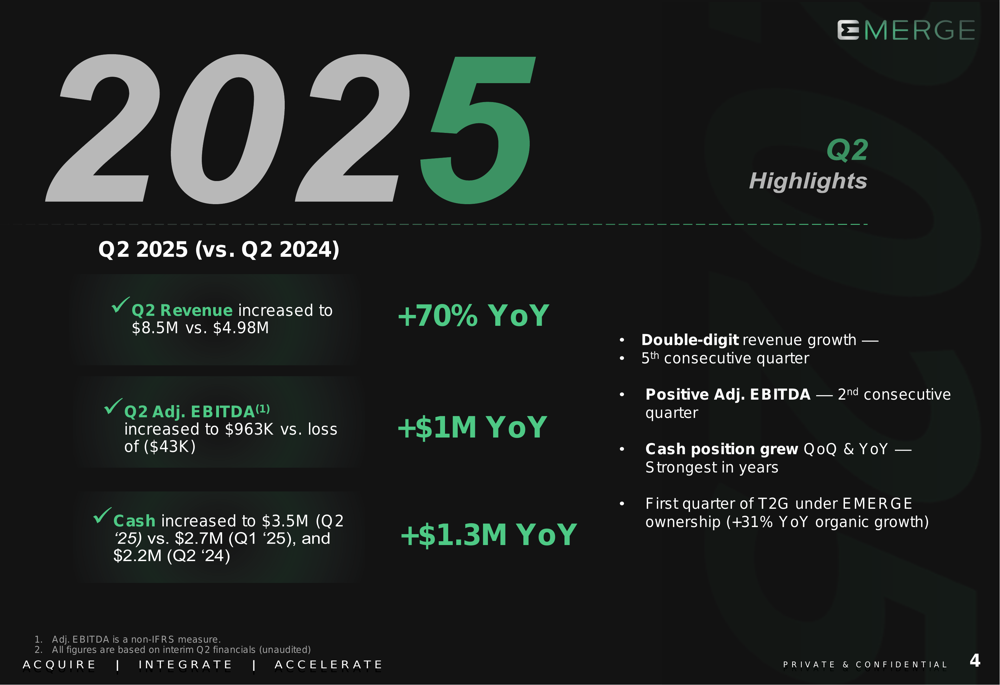

EMERGE reported substantial year-over-year improvements across all key financial metrics for Q2 2025, marking its fifth consecutive quarter of double-digit revenue growth and second consecutive quarter of positive adjusted EBITDA.

Revenue increased 70% year-over-year to $8.5 million compared to $4.98 million in Q2 2024, while adjusted EBITDA reached $963,000, a dramatic improvement from a loss of $43,000 in the same period last year. The company’s cash position strengthened to $3.5 million, up from $2.7 million in Q1 2025 and $2.2 million in Q2 2024.

As shown in the following quarterly performance summary:

These results represent a significant acceleration from Q1 2025, when the company reported $5 million in revenue and $32,000 in adjusted EBITDA, demonstrating sequential growth in both top-line and profitability.

Vertical Performance

EMERGE’s portfolio is built around two main verticals: grocery and golf. The company’s pro forma revenue stands at approximately $27 million with a target gross margin of around 40%.

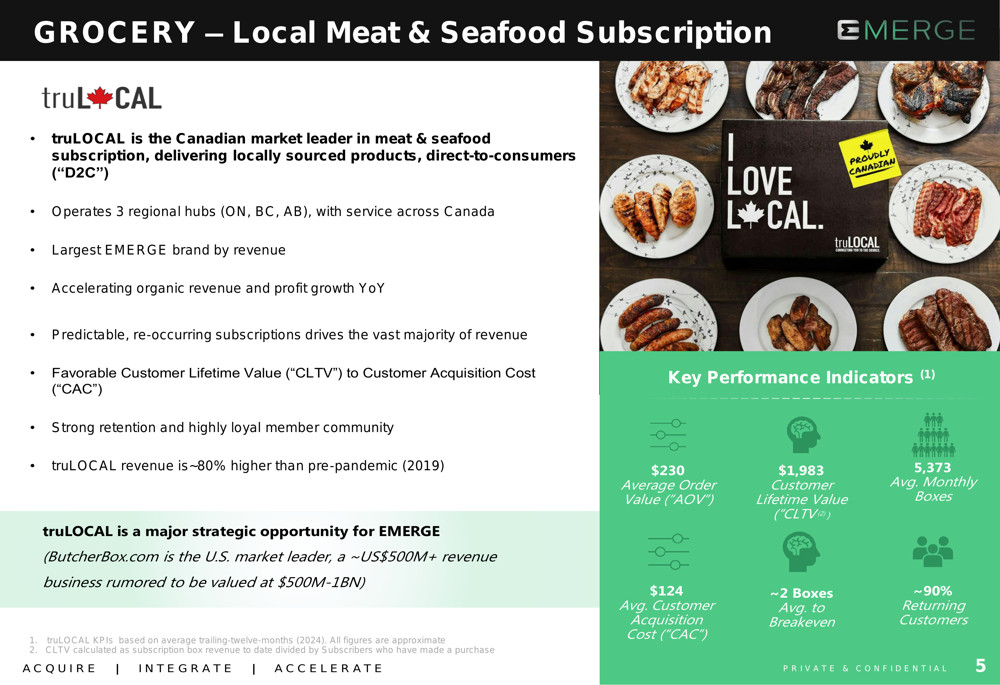

The grocery vertical is anchored by truLOCAL, a subscription service delivering locally sourced meat and seafood directly to consumers. As the largest brand in EMERGE’s portfolio, truLOCAL boasts impressive metrics including a $230 average order value, $1,983 customer lifetime value, and approximately 90% returning customers.

The following slide details truLOCAL’s business model and performance metrics:

truLOCAL has benefited significantly from the "Buy Canadian" movement, with net new subscriptions increasing by 193% in February 2025 alone. The company has also reduced its customer acquisition costs by approximately 20% year-over-year during the same period.

In the golf vertical, EMERGE operates three brands: Tee 2 Green (T2G), JustGolfStuff, and UnderPar, covering equipment, apparel, and experiences. The company’s golf portfolio is illustrated here:

Acquisition Strategy & Integration Success

A key highlight of the quarter was the performance of recently acquired Tee 2 Green (T2G), which completed its first quarter under EMERGE ownership. T2G generated $3.3 million in revenue, up 31% year-over-year, and $797,000 in adjusted EBITDA, a 37% increase from the prior year.

EMERGE acquired T2G for $2.2 million, including $1.1 million cash on closing, $900,000 in deferred consideration over a five-year payment plan, and $200,000 in EMERGE shares. The company also acquired $2.4 million in inventory under an eight-year payment plan.

The T2G acquisition exemplifies EMERGE’s capital-efficient acquisition strategy, which focuses on long-standing, profitable businesses with stable organic revenue growth and recurring customer relationships. The company targets businesses with EBITDA between $750,000 and $2 million, structuring deals with approximately 50% cash at closing, 20% in EMERGE shares, and 30% in deferred payments or earnouts.

Strategic Initiatives

EMERGE has outlined its evolution through three strategic phases, with the current "EMERGE 3.0" focused on centralization, high synergy across brands, and cash flow generation.

The company is pursuing both cost savings and growth initiatives. On the savings side, EMERGE has streamlined its headquarters team (approximately $750,000 in savings) and is optimizing payment processing, email services, warehousing, and customer service. Growth initiatives include cross-selling between brands, enhancing margins, and leveraging data and advertising synergies across the portfolio.

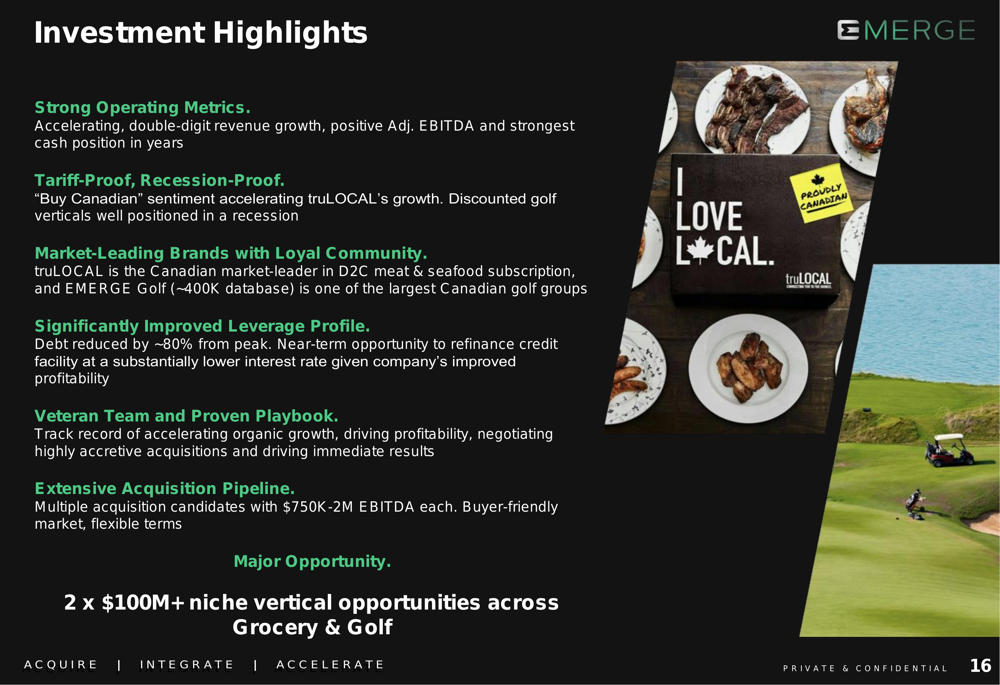

The following investment highlights summarize EMERGE’s value proposition:

Forward-Looking Statements

Looking ahead, EMERGE has outlined three key priorities for 2025: accelerating positive revenue growth trends, reactivating its merger and acquisition program with a focus on cash flow positive acquisitions, and exploring opportunities to enhance cash flow and reduce interest expenses.

The company has identified potential acquisition targets in both its grocery and golf verticals, including food tech/SaaS companies, logistics providers, direct-to-consumer competitors, and pet food businesses in the grocery segment. In golf, targets include equipment and apparel retailers, golf tech companies, offline retail operations, media businesses, and experience providers.

EMERGE believes each vertical represents a $100+ million opportunity, with multiple acquisition candidates in the $750,000 to $2 million EBITDA range. Management emphasized that the current market conditions are buyer-friendly, positioning the company well for its acquisition strategy.

With its strengthened financial position, proven acquisition playbook, and momentum across both verticals, EMERGE appears well-positioned to continue its growth trajectory through both organic initiatives and strategic acquisitions in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.