Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Emerson Electric Company (NYSE:EMR) presented its third-quarter 2025 earnings results on August 6, showing modest growth amid challenging market conditions. Despite reporting a 6% year-over-year increase in adjusted earnings per share, Emerson’s stock tumbled 7.09% in premarket trading to $130.60, suggesting investors may have expected stronger performance or were concerned about specific aspects of the company’s outlook.

The industrial automation giant reported underlying sales growth of 3% for the quarter, which was "meaningfully impacted by reduced pricing actions," according to the company’s presentation. This represents a deceleration from the previous quarter, where Emerson had reported stronger performance that drove a 6.13% stock increase.

Quarterly Performance Highlights

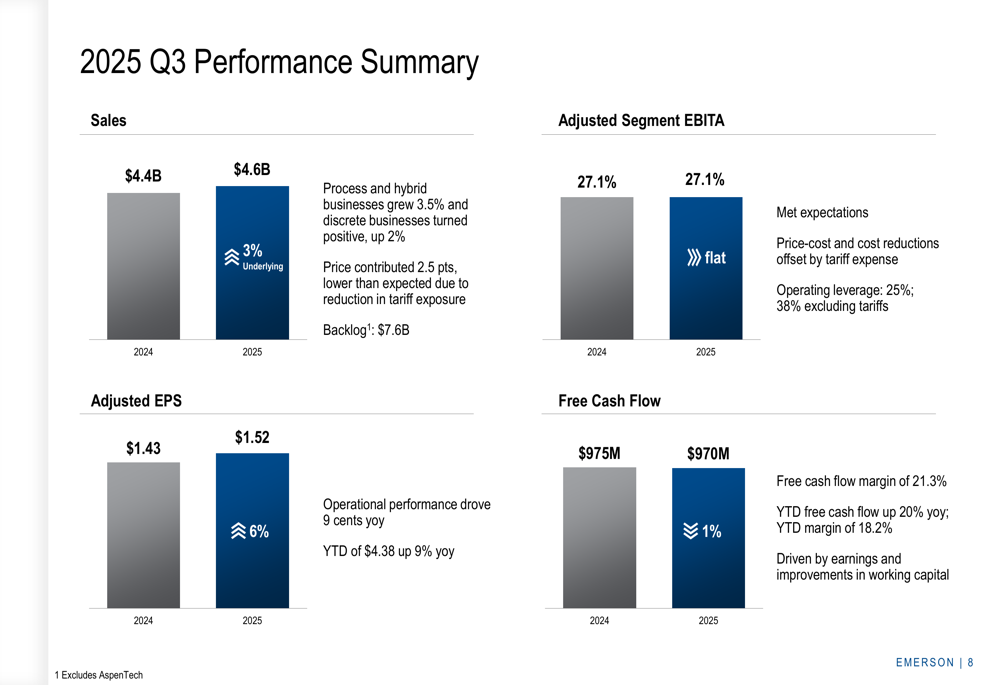

Emerson delivered adjusted earnings per share of $1.52 in Q3 2025, up 6% from $1.43 in the same period last year. Sales reached $4.6 billion, representing a 3% underlying growth compared to Q3 2024. The company maintained its adjusted segment EBITA margin at 27.1%, unchanged from the prior year.

Free cash flow remained relatively stable at $970 million compared to $975 million in Q3 2024, with a free cash flow margin of 21.3%, indicating strong cash generation capabilities.

As shown in the following performance summary:

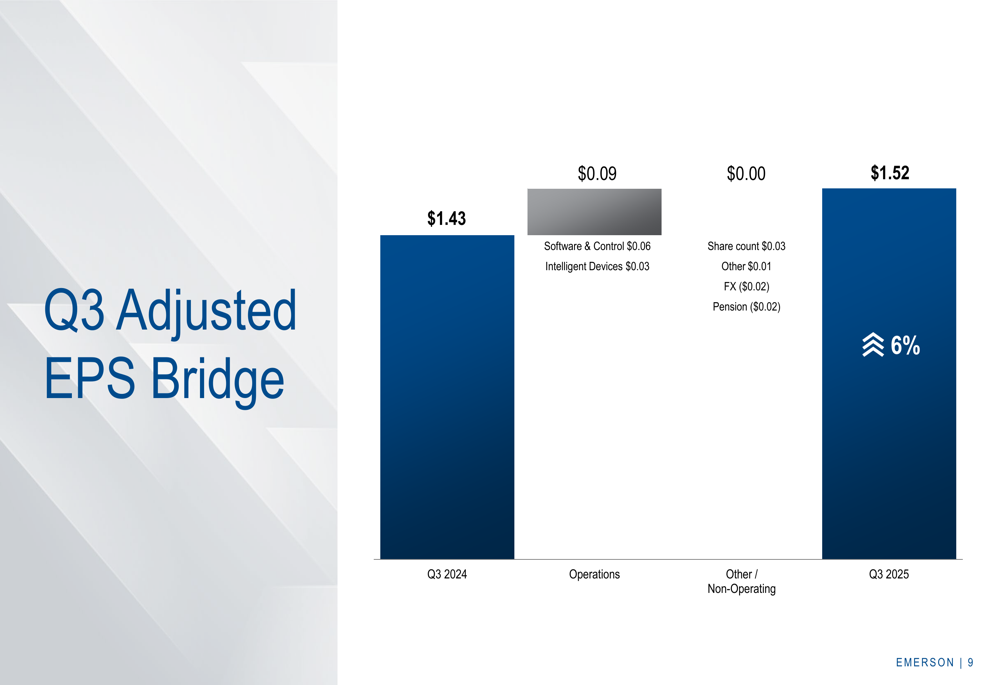

The EPS improvement was primarily driven by operational improvements, with Software (ETR:SOWGn) & Control contributing $0.06 and Intelligent Devices adding $0.03 to the year-over-year increase:

Tariff Mitigation Strategy

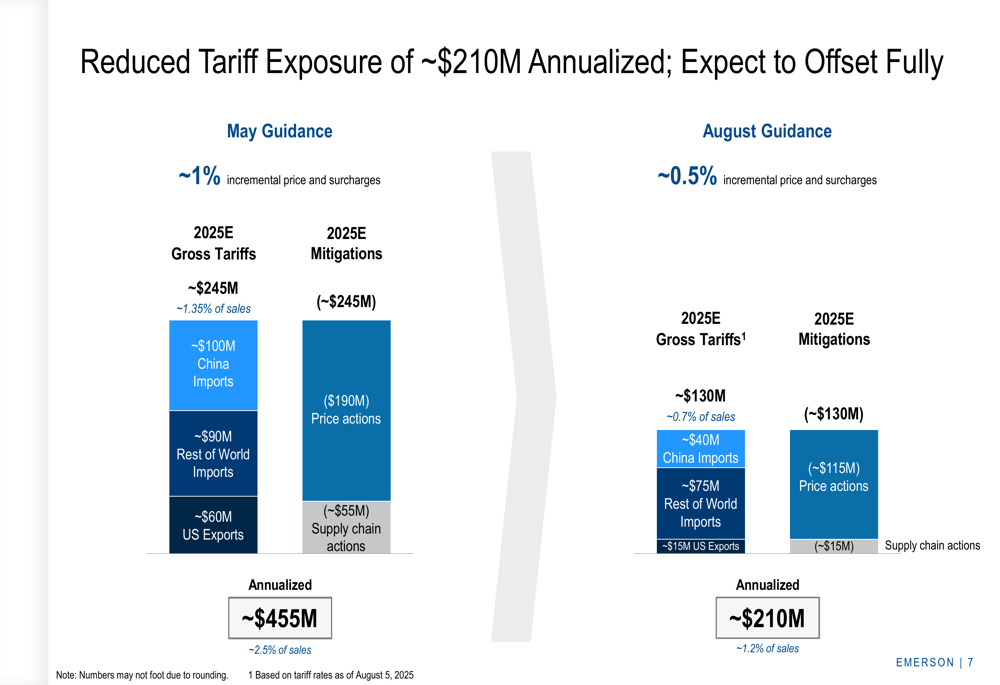

A notable achievement highlighted in the presentation was Emerson’s successful reduction of tariff exposure. The company has managed to cut its tariff exposure by more than half since its May guidance, from approximately $455 million (2.5% of sales) to around $210 million (1.2% of sales).

This reduction was achieved through a combination of price actions and supply chain adjustments, demonstrating the company’s agility in responding to trade challenges. The presentation detailed both the gross tariff amounts and the corresponding mitigation efforts:

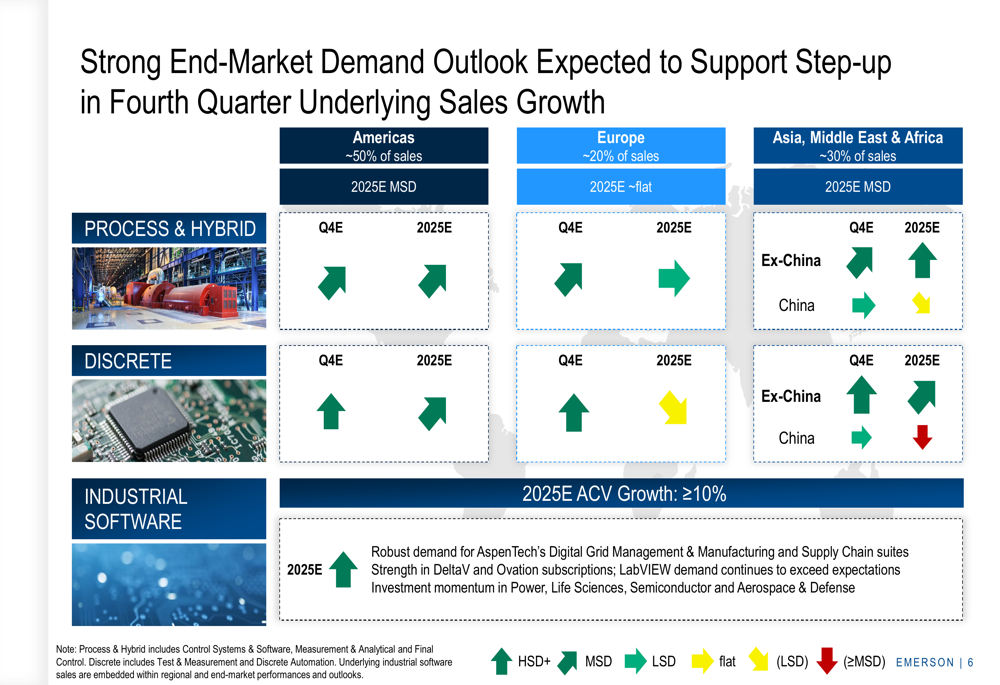

End-Market Outlook

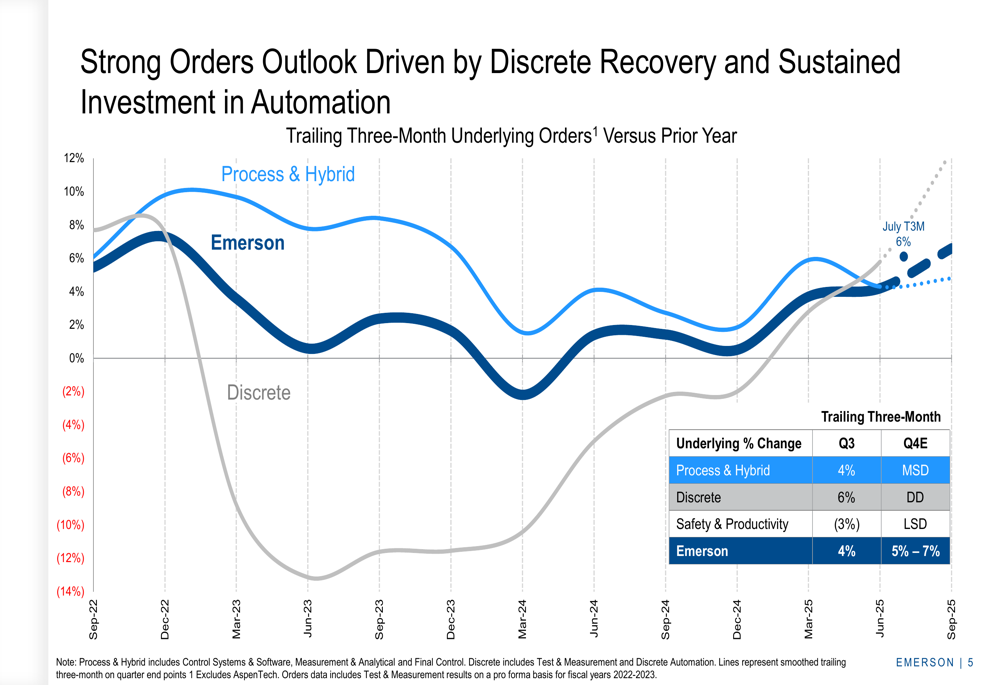

Emerson reported continued momentum in process and hybrid markets, with signs of recovery in discrete markets. The company’s underlying orders grew by 4% in Q3, with Test & Measurement orders showing particularly strong performance at 16% growth.

Regional performance varied significantly, with North America, India, and the Middle East & Africa showing strength, while Europe remained challenged. For 2025, Emerson expects mid-single-digit growth in the Americas (representing about 50% of sales) and Asia/Middle East/Africa (about 30% of sales), while Europe (approximately 20% of sales) is projected to remain flat.

The following chart illustrates the company’s orders outlook across different segments:

The regional breakdown of end-market demand provides further context for Emerson’s growth expectations:

Software Innovation & Growth

Emerson highlighted its progress in industrial software innovation as a key strategic focus. The company’s Annual Contract Value (ACV) for industrial software reached $1.5 billion, up 10% year-over-year, with expectations for continued double-digit growth.

The presentation showcased several significant developments, including a strategic collaboration between AspenTech and TotalEnergies (EPA:TTEF) to implement Inmation as their industrial data fabric for AI applications. Emerson also announced the release of Ovation™ AI Advisor, described as "the first GenAI advisor for power generation control systems," and the launch of Nigel™ AI Advisor in LabVIEW test software.

These innovations were highlighted at the Emerson Exchange 2025 event, which attracted approximately 3,000 attendees from 51 countries:

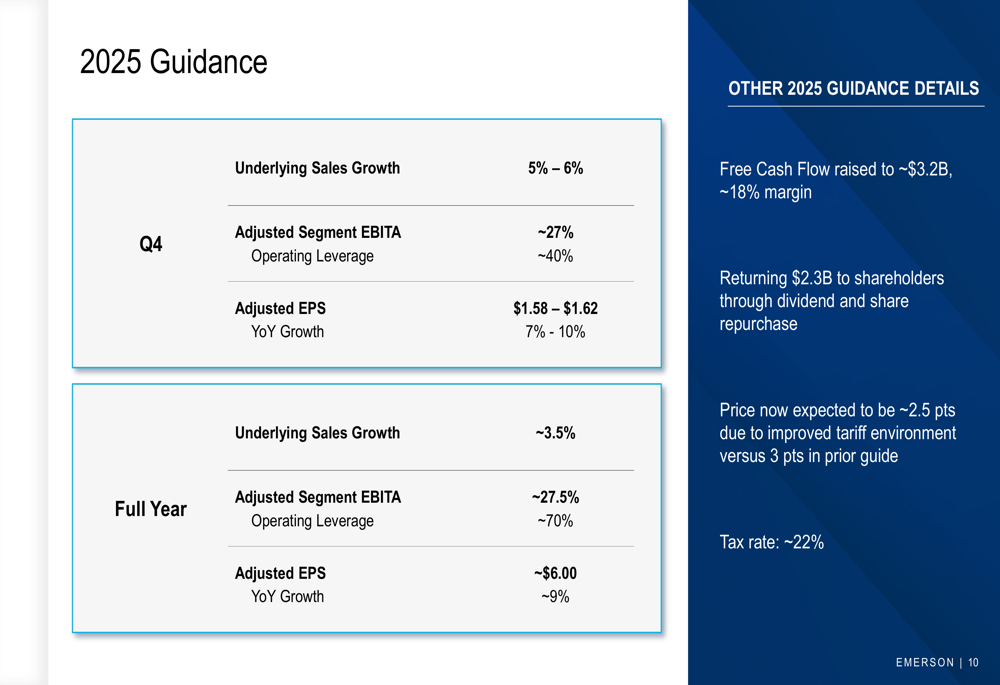

Forward Guidance

For the fourth quarter of fiscal 2025, Emerson projects underlying sales growth of 5%-6%, driven by recovery in Test & Measurement and continued investment in automation. The company expects adjusted segment EBITA margin of approximately 27% and adjusted EPS of $1.58-$1.62, representing 7%-10% year-over-year growth.

For the full fiscal year 2025, Emerson raised its free cash flow guidance to approximately $3.2 billion and maintained its plan to return $2.3 billion to shareholders. The company projects underlying sales growth of about 3.5%, adjusted segment EBITA of approximately 27.5%, and adjusted EPS of around $6.00, up about 9% year-over-year.

The detailed guidance was presented as follows:

Market Reaction & Analysis

Despite the generally positive results and outlook, Emerson’s stock declined significantly in premarket trading. This negative reaction may reflect several factors not immediately apparent in the presentation.

First, the 3% underlying sales growth for Q3 represents a deceleration from previous quarters and may have fallen short of market expectations. Second, while the company highlighted order growth of 4% for Q3, the Safety & Productivity segment showed a 3% decline in orders, potentially raising concerns about specific business areas.

Additionally, the flat adjusted segment EBITA margin of 27.1% year-over-year might suggest challenges in expanding profitability despite growth initiatives. Investors may also be concerned about the company’s exposure to challenging markets like China and Europe, where growth prospects remain limited.

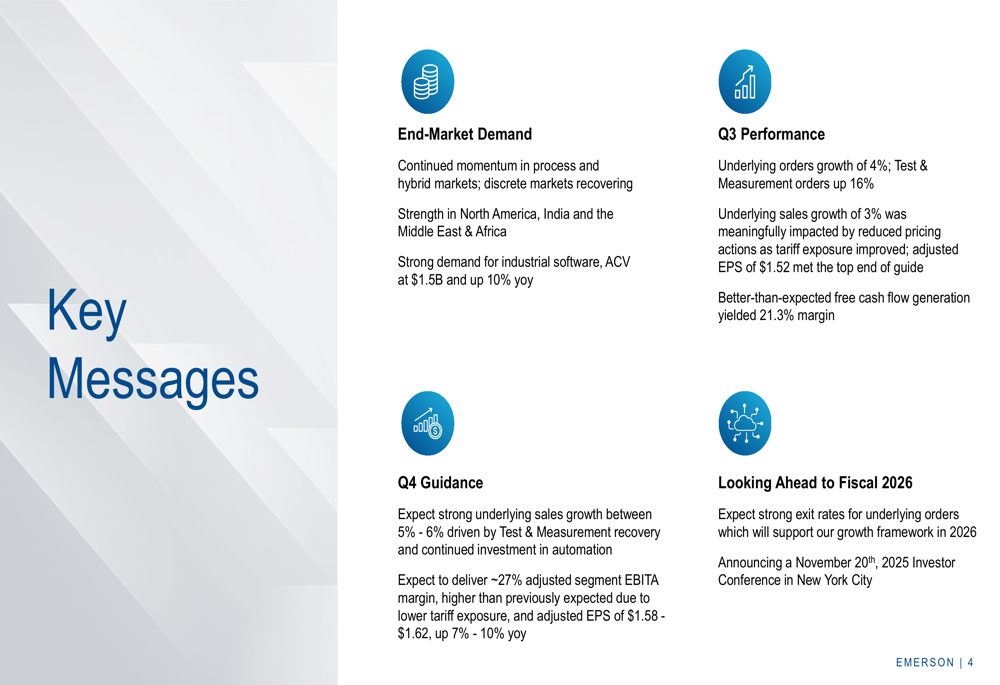

The company’s key messages summarize both the achievements and challenges facing Emerson:

Emerson plans to hold an Investor Conference on November 20, 2025, in New York City, where it will likely provide more detailed insights into its long-term strategy and growth framework. Until then, investors will be watching closely to see if the company can deliver on its projected acceleration in growth for the fourth quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.