U.S. stock futures rise on increased rate cut optimism; Dell’s outlook impresses

Introduction & Market Context

Enbridge Inc (NYSE:ENB) delivered its second quarter 2025 update on August 1, showcasing record quarterly results amid a strategic pivot toward serving growing power demand from data centers and AI infrastructure. The company's stock showed mixed signals, with a minor 0.15% decline in premarket trading despite strong financial performance.

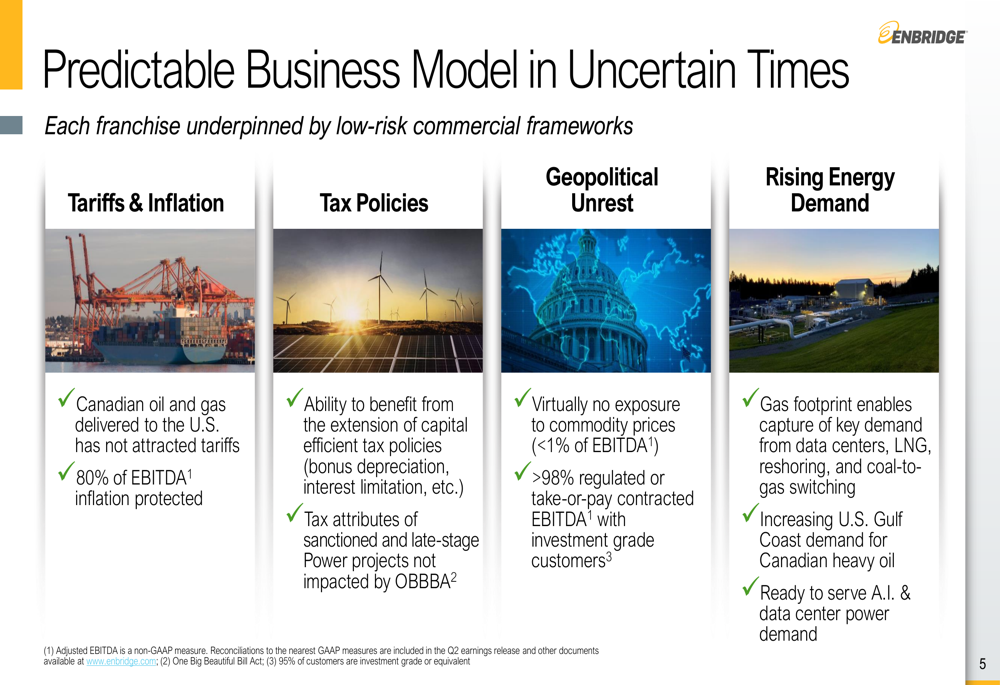

The midstream energy giant emphasized its resilience in uncertain times, highlighting that 98% of its EBITDA comes from regulated or take-or-pay contracted sources with investment-grade customers, while 80% of EBITDA enjoys inflation protection. This stability comes as Enbridge continues to position itself as a utility-like business with predictable cash flows.

As shown in the following slide detailing Enbridge's business model strengths in uncertain times:

Quarterly Performance Highlights

Enbridge reported record second-quarter results with adjusted EBITDA of $4,644 million, representing a 7% increase from $4,335 million in Q2 2024. The company's adjusted earnings per share grew to $0.65 from $0.58 year-over-year, a 12% improvement. Distributable cash flow (DCF) per share was $1.33, slightly down from $1.34 in the same period last year.

The Gas Transmission & Midstream segment showed particularly strong growth, with EBITDA increasing to $1,384 million from $1,082 million in Q2 2024. Similarly, Gas Distribution & Storage saw significant improvement, with EBITDA rising to $840 million from $567 million. However, the Renewable Power Generation segment experienced a decline, with EBITDA falling to $120 million from $147 million in the prior year.

The detailed quarterly financial results are presented in the following slide:

Enbridge maintained a solid balance sheet with a debt-to-EBITDA ratio of 4.7x, within its target range of 4.5x to 5.0x. The company's Mainline system showed strong utilization with volumes of 3.0 million barrels per day during the quarter.

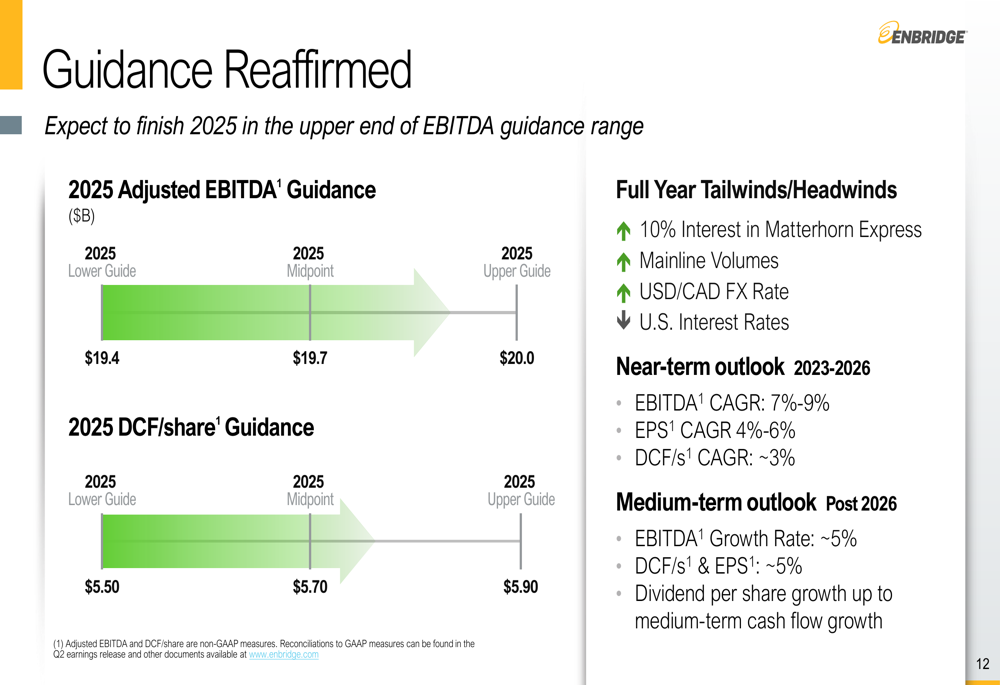

Based on these results, Enbridge expects to finish 2025 in the upper end of its EBITDA guidance range of $19.4 billion to $20.0 billion, while meeting the mid-point of its DCF guidance.

The company's full-year guidance is illustrated in this slide:

Strategic Initiatives

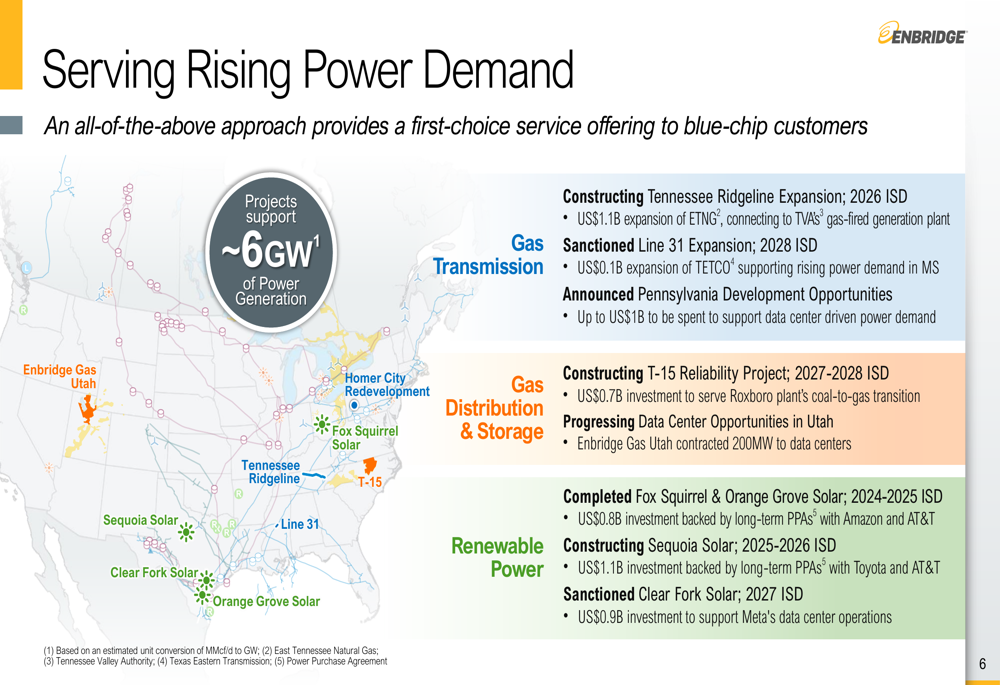

Enbridge is strategically positioning itself to capitalize on rising power demand, particularly from data centers and AI infrastructure. The company has adopted an "all-of-the-above" approach to serving blue-chip customers' energy needs, with projects supporting approximately 6GW of power generation.

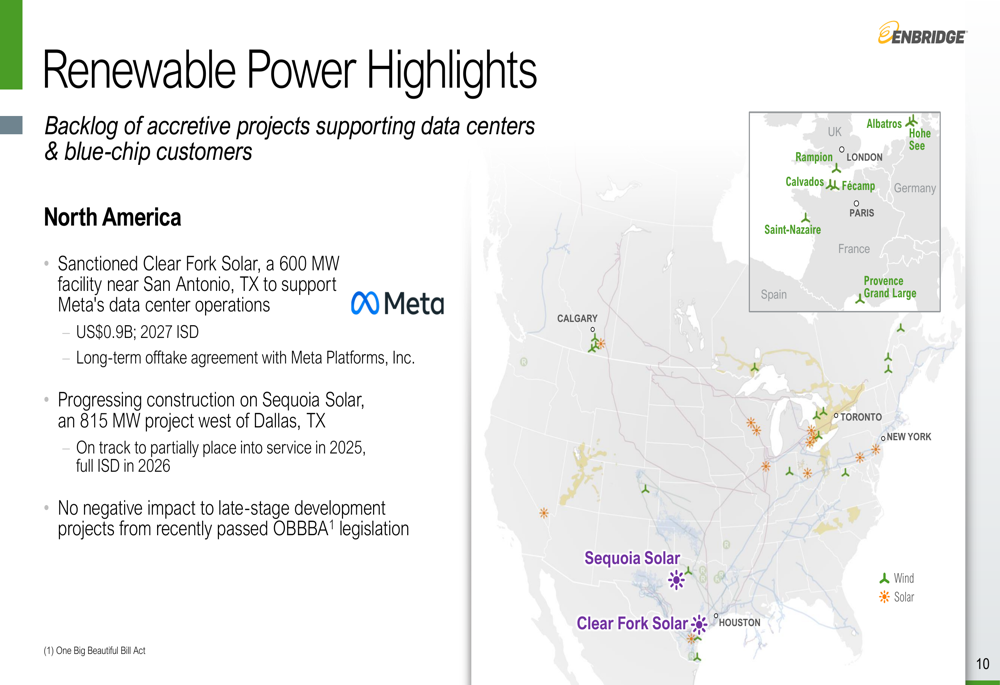

A key development during the quarter was the sanctioning of the Clear Fork Solar project, a 600 MW facility near San Antonio, Texas, representing a $900 million investment with an in-service date of 2027. This project is underpinned by a long-term offtake agreement with Meta Platforms, Inc. Enbridge is also progressing construction on the 815 MW Sequoia Solar project west of Dallas, which is on track for partial service in 2025 and full operation in 2026.

The company's renewable power strategy is illustrated in the following slide:

Enbridge's approach to serving rising power demand across its network is shown here:

On the gas transmission front, Enbridge sanctioned a 160 MMcf/d TETCO Line 31 expansion ($0.1 billion; 2028 ISD) underpinned by 20-year agreements with investment-grade customers. The company also sanctioned a 40 Bcf North Aitken Creek Storage Expansion ($0.3 billion; 2028 ISD) to meet growing storage demands.

In its liquids business, Enbridge reported strong Q2 Mainline volumes of 3.0 MMbpd and is investing up to $2 billion toward Mainline Capital Investment. The company successfully closed an oversubscribed open season on the Flanagan South Pipeline for 100 kbpd of capacity and launched an open season for the Southern Illinois Connector.

Capital Allocation & Forward-Looking Statements

Enbridge outlined its capital allocation priorities, focusing on balance sheet strength, sustainable return of capital, and further growth. The company has completed a 12.5% investment in the Westcoast system by 38 First Nations groups and closed a 10% acquisition of the Matterhorn Express Pipeline.

The company's capital allocation strategy is presented in this slide:

Looking forward, Enbridge is targeting a 5% growth rate through the end of the decade, supported by a secured capital program worth $32 billion. The company plans to invest $9-10 billion annually, prioritizing low-multiple brownfield opportunities with build multiples of 6-8x.

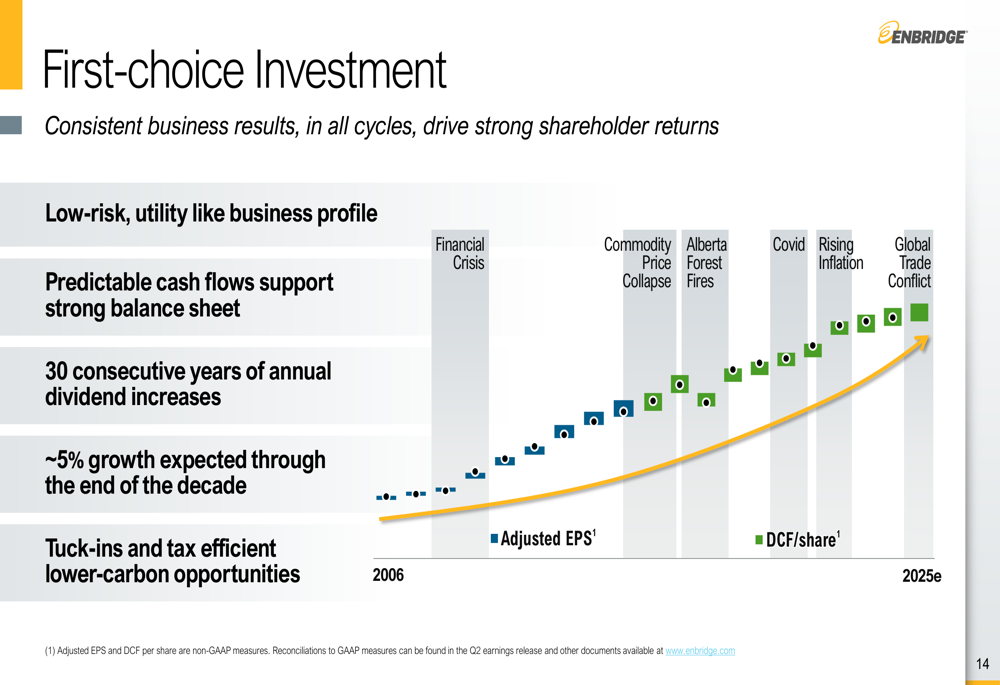

Enbridge emphasized its 30-year history of annual dividend increases, positioning itself as a Dividend Aristocrat with a distributable cash flow payout range of 60-70%. The company's historical performance through various economic cycles is illustrated in the following slide:

CEO Greg Ebel highlighted the company's strategic positioning during the earnings call, stating, "Our low-risk business continues to prove its value to shareholders." He also emphasized the importance of scale in the energy industry, noting that "People want to work with big players."

With its balanced approach to traditional energy infrastructure and renewable power generation, Enbridge appears well-positioned to navigate the energy transition while delivering consistent returns to shareholders. However, the company faces potential challenges from regulatory changes, market volatility, increasing competition in the renewable space, and potential supply chain disruptions that could impact project timelines and costs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.