Gold prices steady above $3,400/oz on rate cut bets; PCE data awaited

Introduction & Market Context

Spanish utility giant Endesa SA (BME:ELE) delivered its first quarter 2025 results presentation on May 7, highlighting substantial financial growth despite challenging market conditions characterized by geopolitical instability and commodity price volatility.

CEO José Bogas emphasized that the quarter was marked by "solid performance across all business lines" while navigating an energy context affected by geopolitical tensions that significantly impacted commodity prices. The presentation also noted that regulatory remuneration improvements would be key to addressing new market challenges.

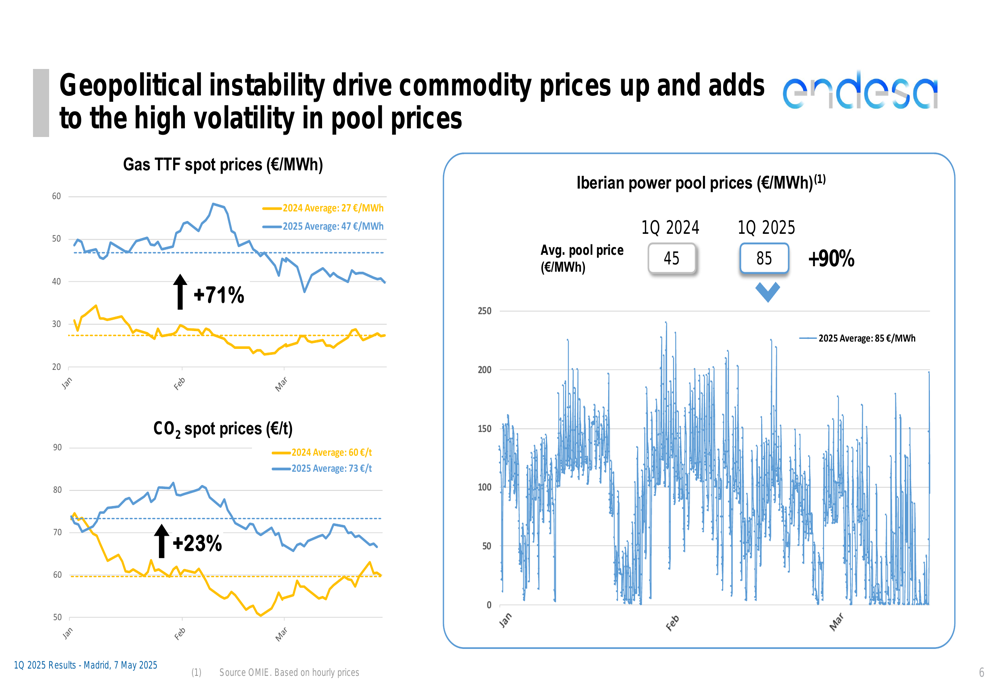

The energy landscape during Q1 2025 saw dramatic price increases across key commodities. Gas TTF spot prices surged 71% year-over-year to an average of 47 €/MWh, while CO2 spot prices increased 23% to 73 €/t. These factors contributed to a 90% jump in Iberian power pool prices, which averaged 85 €/MWh in Q1 2025 compared to 45 €/MWh in Q1 2024.

As shown in the following chart of commodity and pool price volatility:

Quarterly Performance Highlights

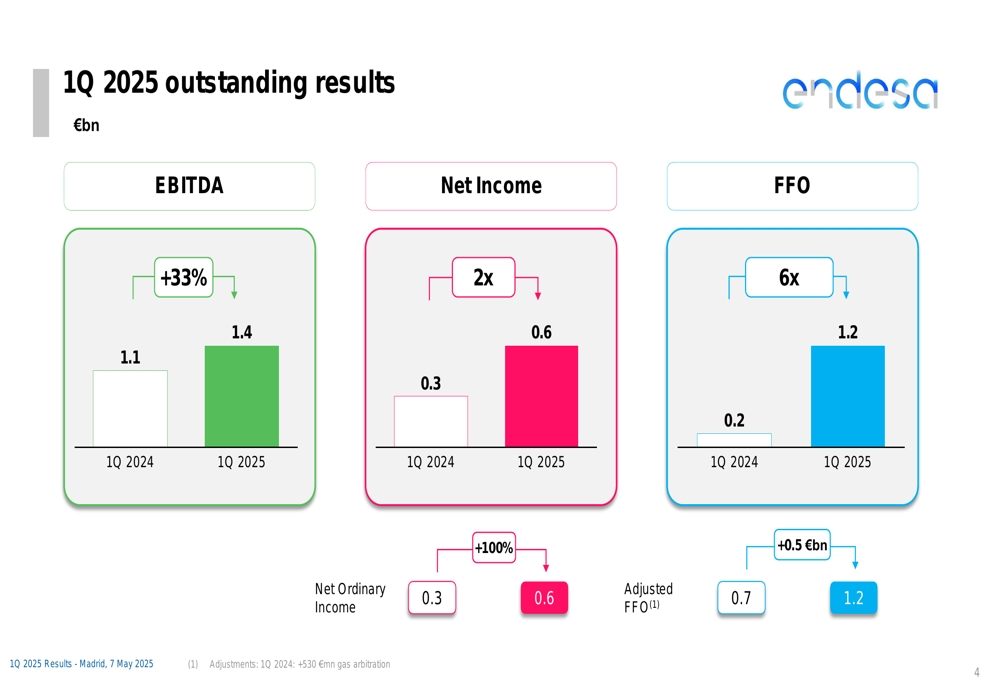

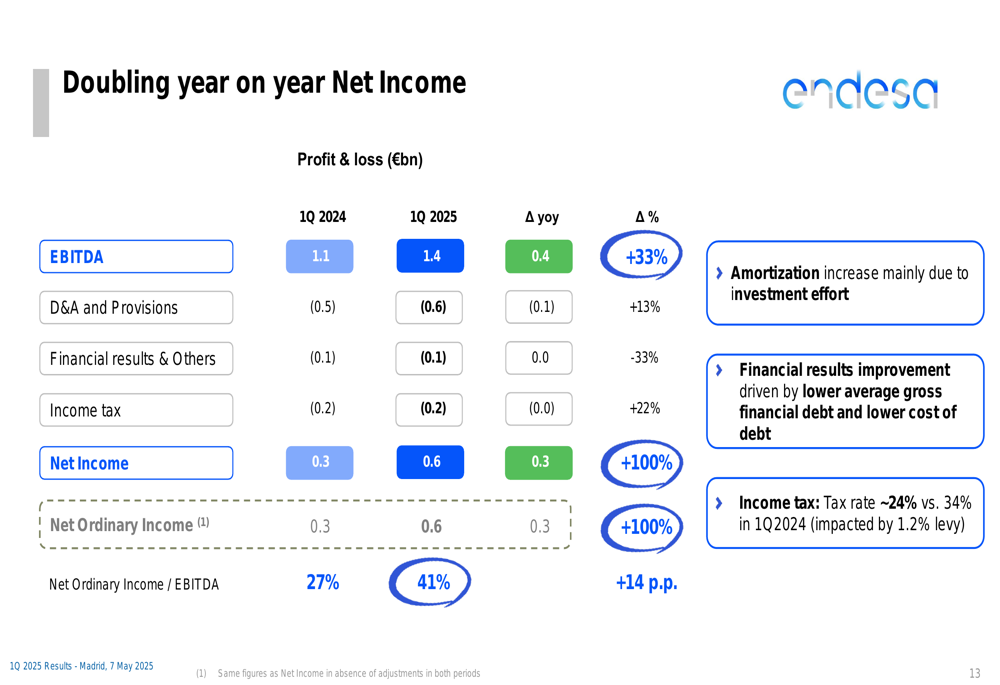

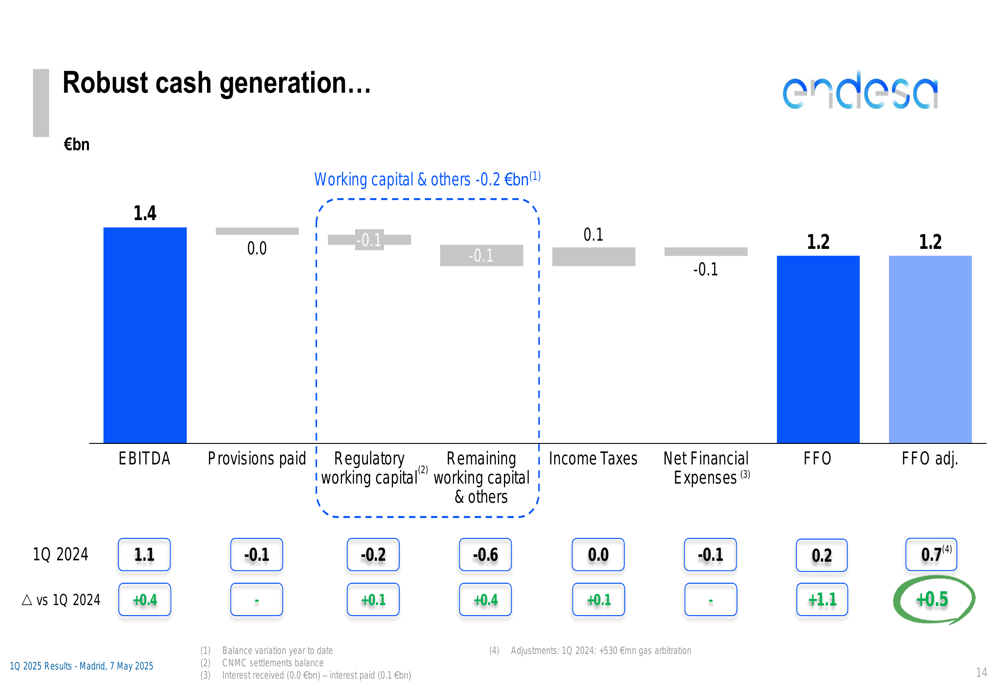

Endesa delivered exceptional financial results for Q1 2025, with EBITDA reaching 1.4 billion euros, representing a 33% increase from 1.1 billion euros in Q1 2024. Net income doubled to 0.6 billion euros, while Funds From Operations (FFO) saw a remarkable sixfold increase to 1.2 billion euros.

The company’s performance metrics are illustrated in this comprehensive comparison:

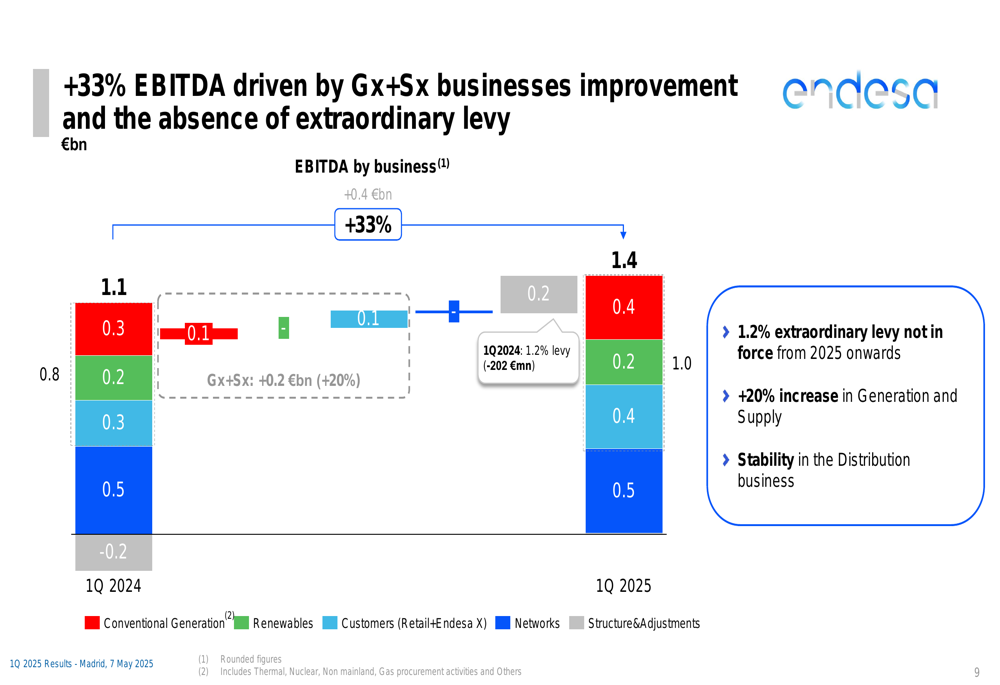

The strong EBITDA growth was primarily driven by the Generation and Supply businesses, which posted a 20% increase, while the Distribution business remained stable. A significant factor in the improved results was the absence of the 1.2% extraordinary levy that was in force during Q1 2024.

This breakdown shows the main contributors to EBITDA growth:

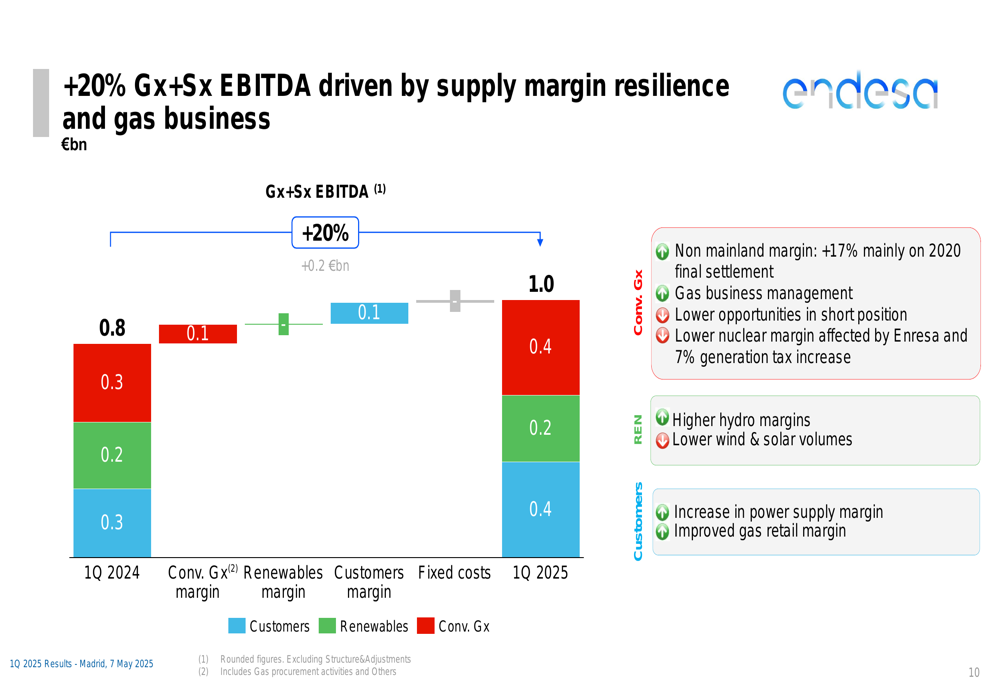

Within the Generation and Supply segment, several factors contributed to the 20% EBITDA growth to 1.0 billion euros. Non-mainland margin improved by 17%, primarily due to the 2020 final settlement. The company also benefited from higher hydro margins, although this was partially offset by lower wind and solar volumes. Both power and gas retail margins showed improvement.

The following chart details these growth drivers:

Detailed Financial Analysis

Endesa’s net ordinary income to EBITDA ratio improved significantly, increasing from 27% in Q1 2024 to 41% in Q1 2025, representing a 14 percentage point improvement. This was achieved through a combination of factors including improved financial results and a decreased tax rate, which fell by 24% to 34%.

The comprehensive profit and loss analysis is illustrated here:

Cash flow generation showed substantial improvement, with adjusted FFO increasing by 0.5 billion euros compared to Q1 2024. This strong cash flow performance occurred despite working capital challenges of -0.2 billion euros, reflecting the company’s operational efficiency and financial discipline.

The cash flow breakdown is presented in this chart:

On the balance sheet side, net financial debt increased by 9%, but financial stability metrics remained solid. The net financial debt to EBITDA ratio held steady at 1.8x, while the FFO to net financial debt ratio improved from 38% to 46%, indicating enhanced debt servicing capability.

Strategic Initiatives

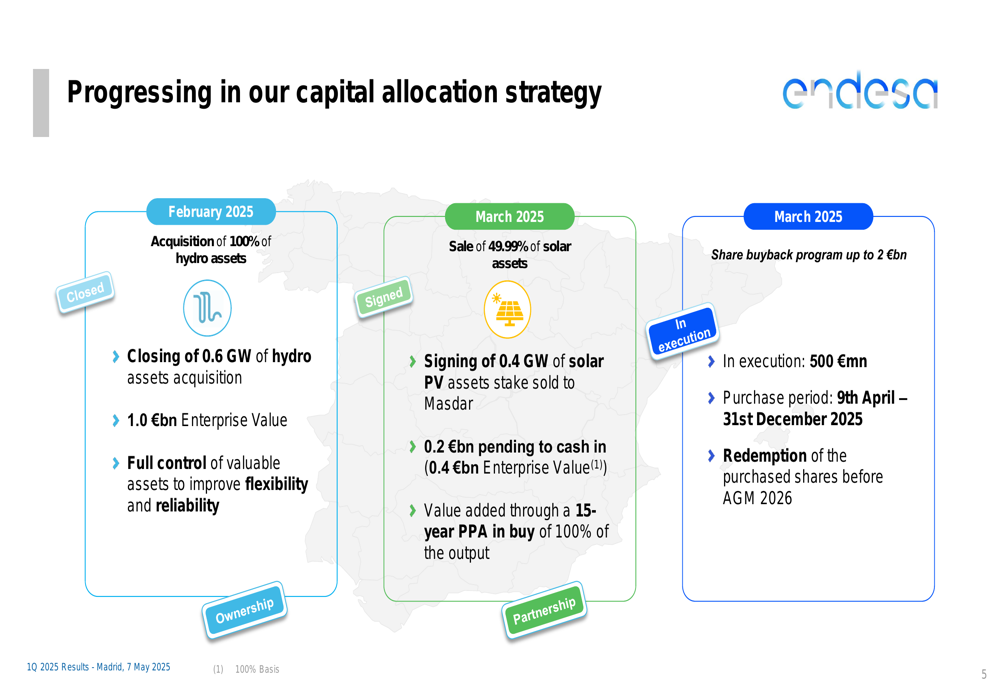

Endesa made significant progress in its capital allocation strategy during the quarter, executing several strategic transactions. In February 2025, the company completed the acquisition of 0.6 GW of hydro assets with an enterprise value of 1.0 billion euros, gaining full control of valuable assets to improve flexibility and reliability.

In March 2025, Endesa sold a 49.99% stake in 0.4 GW of solar PV assets to Masdar, with an enterprise value of 0.4 billion euros (based on 100% valuation). The company retained value through a 15-year power purchase agreement (PPA) for 100% of the output.

Also in March, Endesa announced a significant share buyback program of up to 2 billion euros, with 500 million euros already in execution. The purchase period runs from April 9 to December 31, 2025, with redemption of the purchased shares scheduled before the 2026 Annual General Meeting.

These strategic moves are illustrated in the following map and summary:

In its operational portfolio, Endesa maintained a strong position with 89% CO2-free output/fixed price sales. The company has secured substantial hedging of its inframarginal output, with 98% hedged for 2025, 80% for 2026, and 55% for 2027, providing significant revenue visibility despite market volatility.

The free power unitary margin decreased slightly from 58 €/MWh to 54 €/MWh (-7%), while gas volumes increased by 3% from 19 TWh to 20 TWh. However, the gas unitary margin declined from -2 €/MWh to -11 €/MWh, reflecting challenging market conditions in that segment.

Forward-Looking Statements

Looking ahead, Endesa’s management expressed confidence in achieving its full-year 2025 guidance, supported by the strong Q1 results and solid cash flow generation. The company highlighted its focus on capital structure optimization through the share buyback program.

CEO José Bogas emphasized that "ensuring the security of supply and competitiveness of our electricity system is essential" as the company navigates the evolving energy landscape.

Endesa is also positioning itself to address new demand challenges, noting a 2.9% increase in adjusted system mainland demand. The company highlighted an "unprecedented surge in connection requests" and is already increasing its investment plan for 2025-2027, exceeding the regulatory cap in anticipation of adequate financial remuneration, increased investment caps, and improved remuneration methodology and incentives.

The company’s management stressed that fair remuneration for networks will be crucial to address these demand challenges and support the country’s reindustrialization opportunities.

With strong Q1 performance across all business lines and strategic capital allocation initiatives underway, Endesa appears well-positioned to capitalize on the evolving energy landscape despite ongoing market volatility and regulatory challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.