Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Endúr ASA (OB:ENDUR) presented its Q1 2025 financial results on May 15, 2025, showcasing strong performance with double-digit growth in key metrics. The Norwegian specialist contractor, which focuses on aquaculture solutions and infrastructure, has positioned itself to capitalize on favorable market conditions in both Norway and Sweden.

The company’s stock closed at NOK 88.30 on May 14, 2025, near its 52-week high of NOK 89.60, reflecting market confidence ahead of the results announcement.

Quarterly Performance Highlights

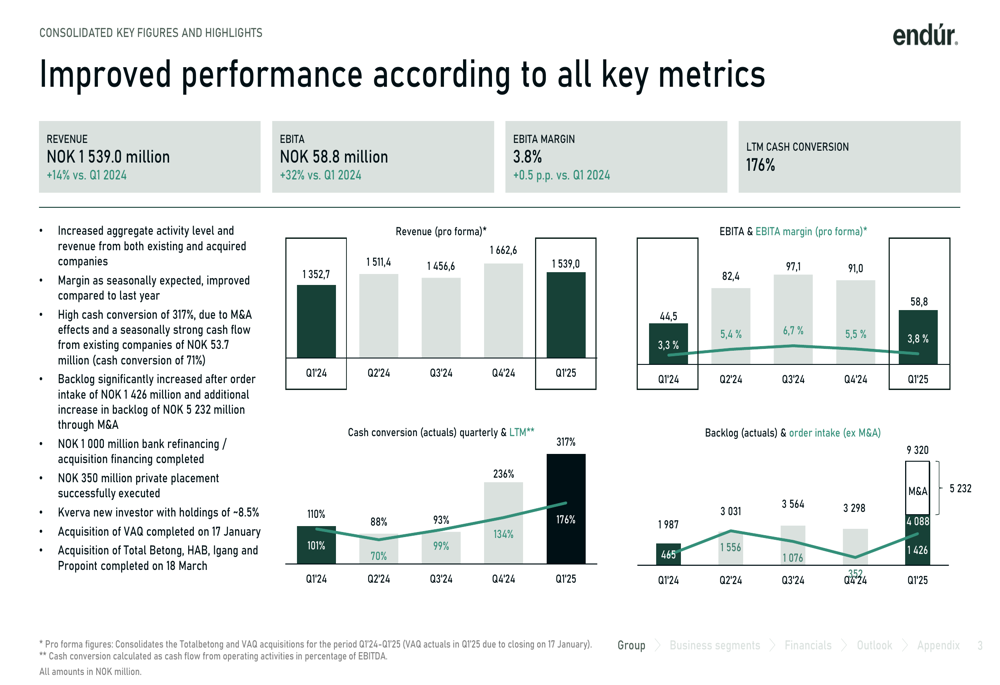

Endúr delivered impressive year-over-year growth in Q1 2025, with revenue reaching NOK 1,539.0 million, up 14% compared to Q1 2024. EBITA showed even stronger improvement, increasing 32% to NOK 58.8 million, while the EBITA margin expanded by 0.5 percentage points to 3.8%.

As shown in the following chart of consolidated key figures, the company has maintained a consistent growth trajectory across its main performance indicators:

Cash conversion was particularly strong at 317% for the quarter and 176% on a last-twelve-months basis, demonstrating the company’s ability to efficiently convert profits into cash flow. The company’s backlog saw significant growth after an order intake of NOK 1,426 million during the quarter.

Despite the positive operational performance, Endúr reported a loss after tax of NOK 11.7 million, compared to a loss of NOK 6.3 million in Q1 2024. This was primarily attributed to PPA amortizations, depreciation, and a NOK 11 million write-down of previously capitalized fees for bank loans.

Segment Performance Analysis

Endúr operates through three main segments: Aquaculture Solutions, Infrastructure, and Other (primarily Endúr Maritime). Each segment showed varied performance in the quarter.

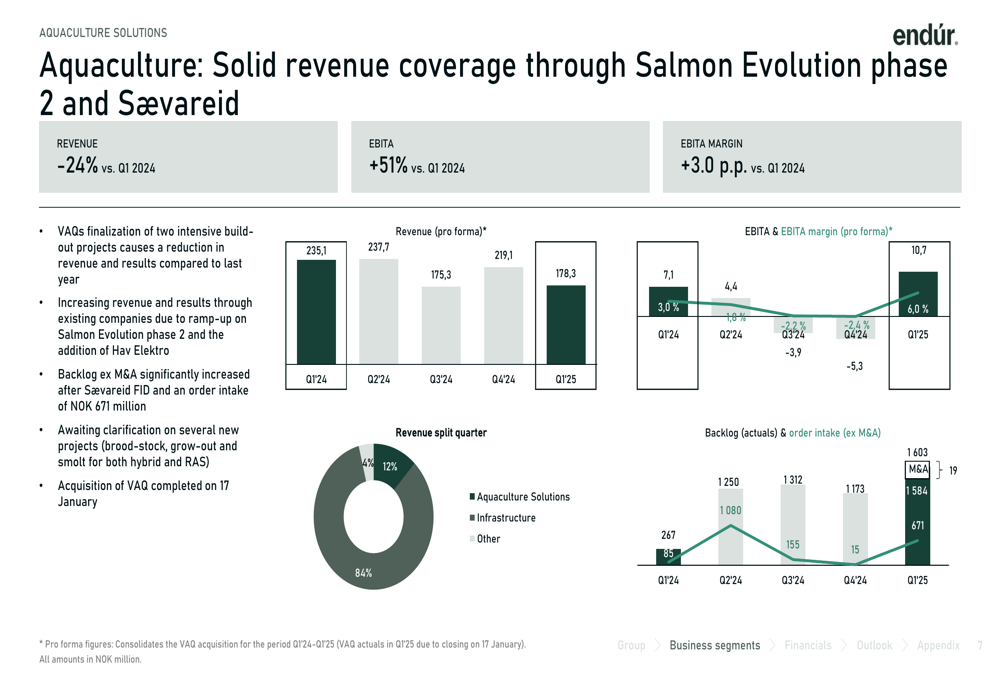

The Aquaculture segment experienced a 24% year-over-year decline in revenue, primarily due to VAQ’s finalization of build-out projects. However, EBITA increased by 51%, and the EBITA margin improved by 3.0 percentage points compared to Q1 2024. The segment’s backlog significantly increased following a NOK 671 million order intake.

As illustrated in the following chart of the Aquaculture segment’s performance:

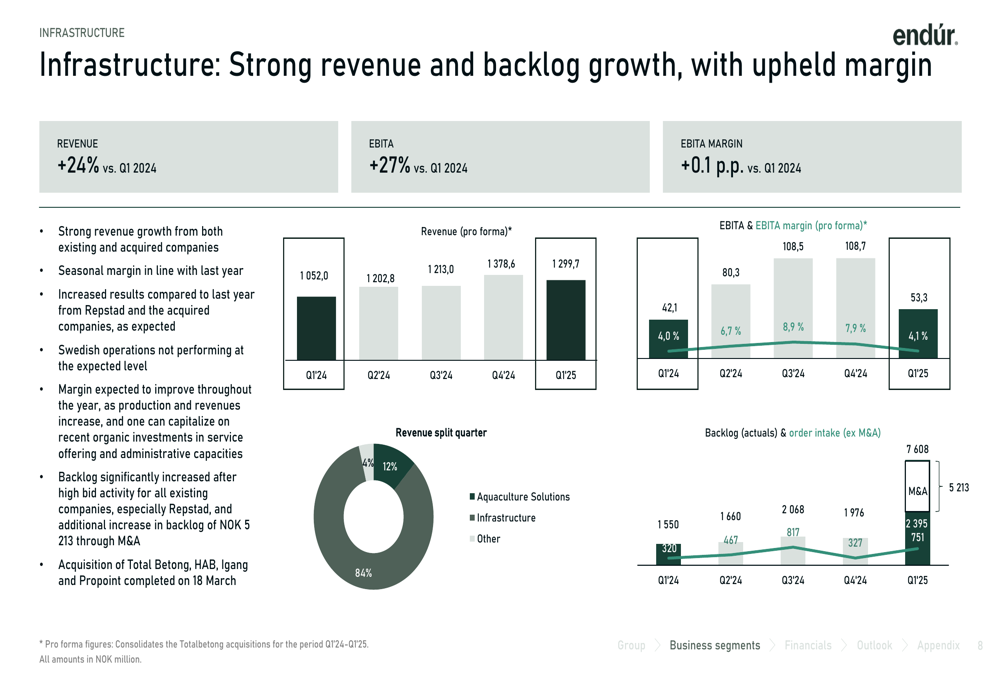

In contrast, the Infrastructure segment delivered strong growth with revenue up 24% and EBITA up 27% compared to Q1 2024. The EBITA margin also improved slightly by 0.1 percentage points.

The segment’s performance is detailed in the following chart:

The "Other" segment, primarily consisting of Endúr Maritime, maintained stable revenue but showed a significant 68% increase in EBITA, with the EBITA margin improving by 2.9 percentage points. The company is preparing to bid on a new framework contract for The Norwegian Defense.

Strategic Initiatives & Acquisitions

During Q1 2025, Endúr completed several strategic initiatives to strengthen its market position and financial foundation. The company successfully refinanced its bank facilities with a NOK 1,000 million package and executed a NOK 350 million private placement, with Kverva becoming a new investor holding approximately 8.5% of the company.

Endúr also completed two strategic acquisitions: VAQ on January 17, 2025, and Total (EPA:TTEF) Betong on March 18, 2025. These acquisitions align with the company’s strategy to become a leading full-service provider in Norway and Sweden.

In a significant development for shareholders, the Board of Directors proposed a dividend policy to distribute 20-40% of the Group’s consolidated net profit after tax as annual dividends, starting in 2026 based on the 2025 financial results. This signals management’s confidence in the company’s future profitability and cash generation capabilities.

Balance Sheet & Cash Flow Strength

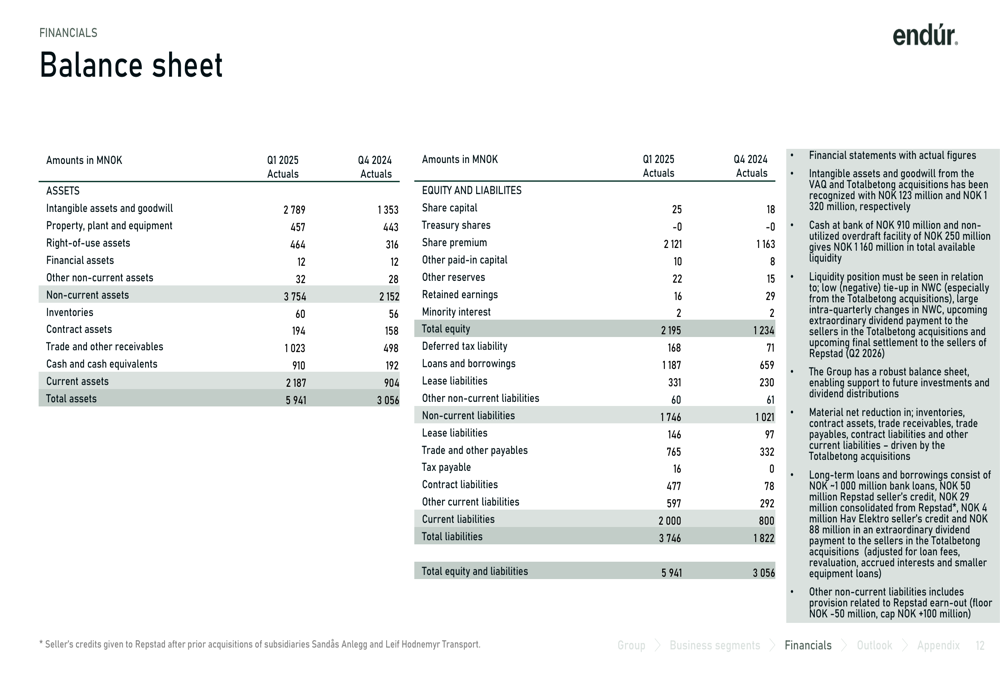

Endúr’s balance sheet as of Q1 2025 showed total assets of NOK 5,941 million, with non-current assets of NOK 3,754 million and current assets of NOK 2,187 million. The company reported a strong cash position of NOK 910 million, complemented by an unused overdraft facility of NOK 250 million.

The detailed balance sheet is presented in the following chart:

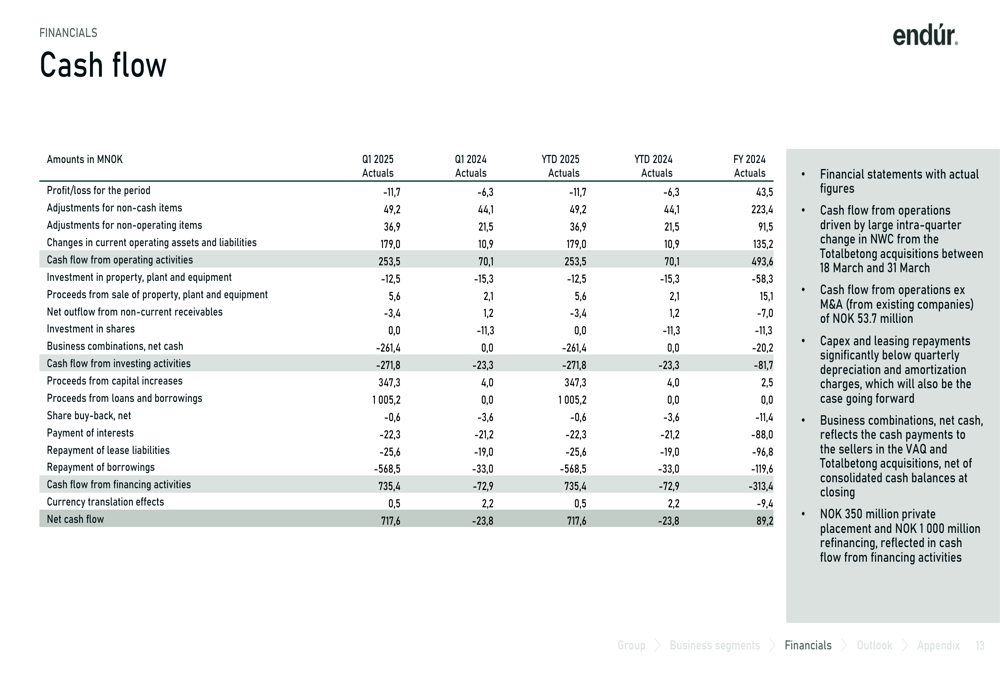

Cash flow from operations was robust at NOK 253.5 million, primarily driven by changes in net working capital. The company’s financing activities generated a cash flow of NOK 735.4 million, reflecting the private placement and refinancing completed during the quarter. Overall, Endúr achieved a net cash flow of NOK 717.6 million for Q1 2025.

The cash flow statement is detailed in the following chart:

Forward-Looking Statements

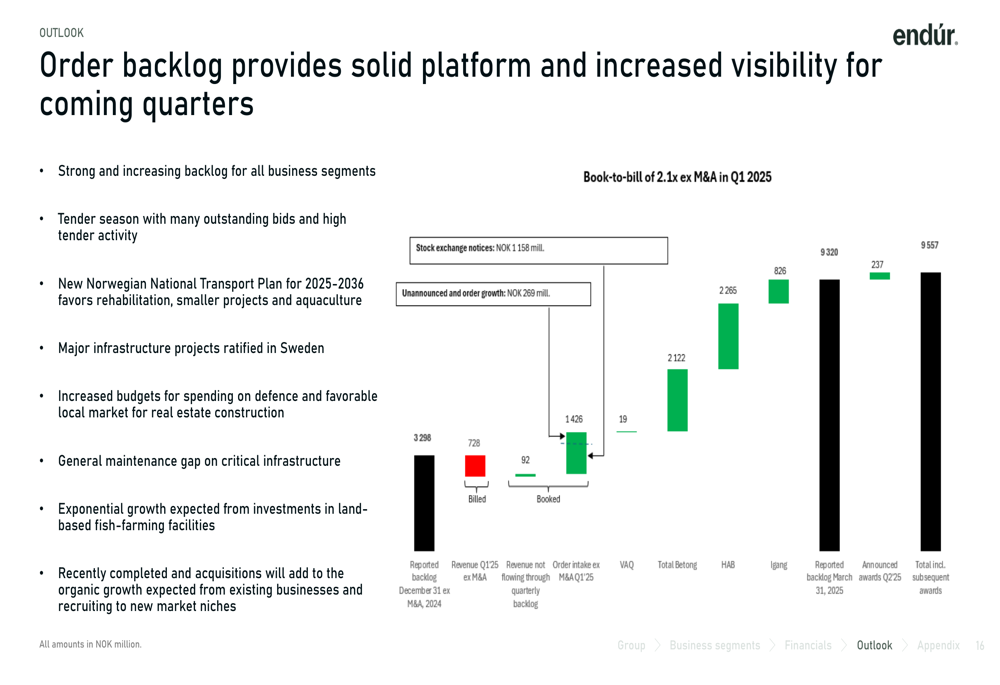

Endúr’s record-high backlog of NOK 9.3 billion provides solid visibility for coming quarters, with a book-to-bill ratio of 2.1x excluding M&A in Q1 2025. The company is actively participating in the tender season with numerous bids submitted.

As illustrated in the following chart of the company’s order backlog:

Management highlighted several favorable market conditions that support their growth outlook, including the Norwegian National Transport Plan’s focus on rehabilitation, major infrastructure projects ratified in Sweden, increased defense spending budgets, and expected exponential growth from investments in land-based fish-farming facilities.

The company summarized its Q1 2025 performance with the following key points:

With its strengthened financial position, strategic acquisitions, and robust backlog, Endúr appears well-positioned to capitalize on growth opportunities in its core markets while delivering improved shareholder returns through its newly proposed dividend policy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.