Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Norwegian specialist contractor Endúr ASA (OB:ENDUR) presented its second quarter 2025 financial results on August 21, showcasing record-high EBITA figures amid continued revenue growth. The company’s shares closed at NOK 87.30 on August 20, down 2.68% ahead of the results announcement.

Endúr, which positions itself as a leading full-service provider for aquaculture solutions and infrastructure in Norway and Sweden, continues to benefit from strong sustainability-driven megatrends in its core markets while maintaining a robust project backlog.

Quarterly Performance Highlights

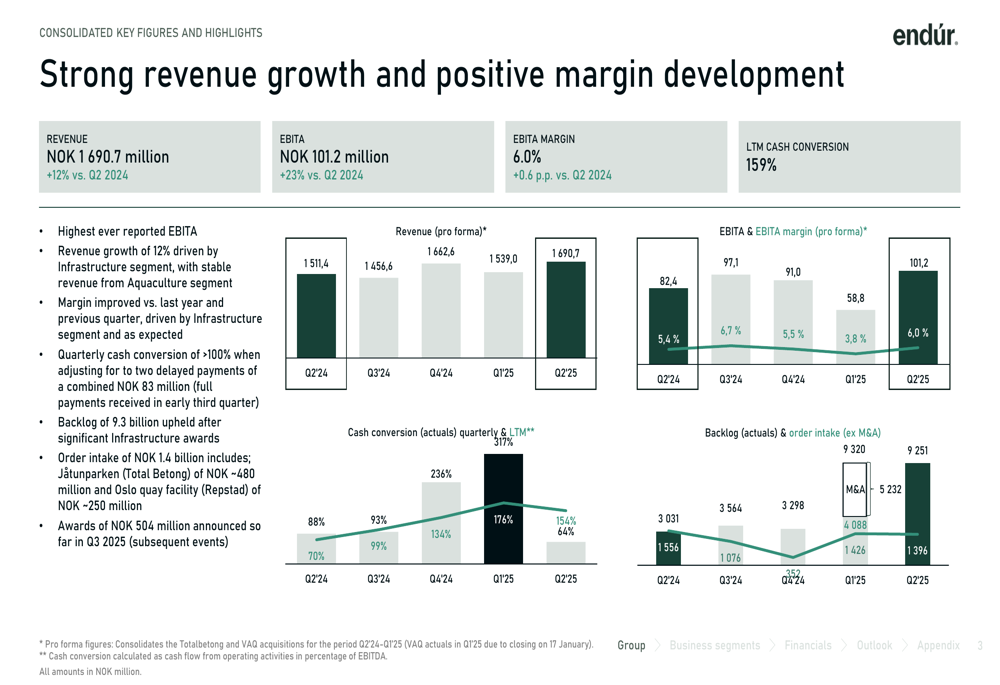

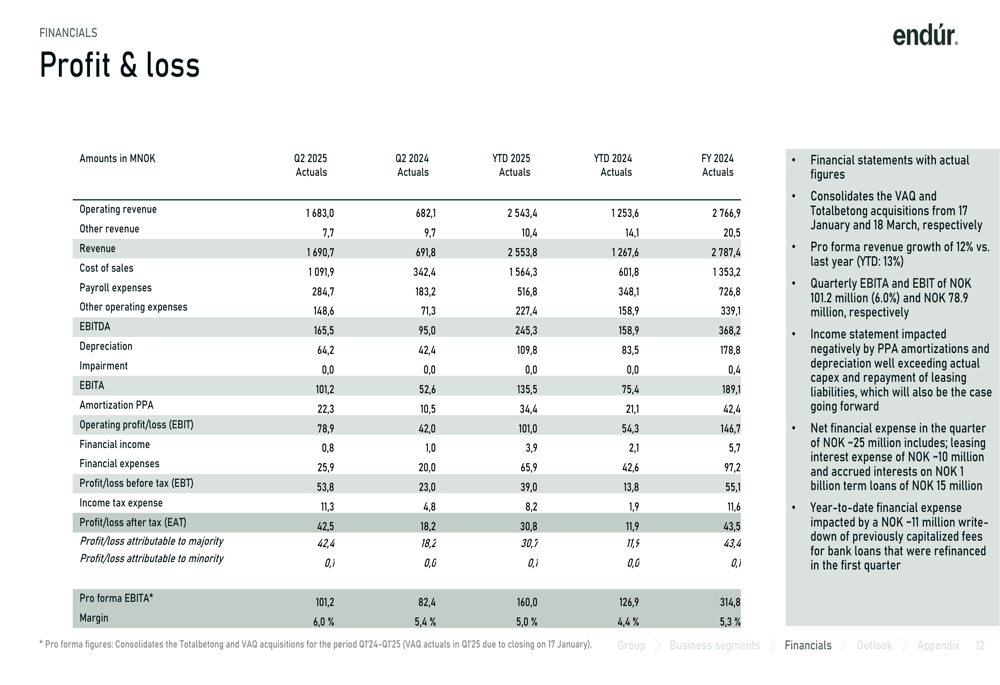

Endúr reported its highest-ever quarterly EBITA of NOK 101.2 million, representing a 23% increase compared to the same period last year. Revenue grew by 12% year-over-year to NOK 1,690.7 million, while the EBITA margin expanded by 0.6 percentage points to reach 6.0%.

As shown in the following chart of quarterly revenue and profitability metrics:

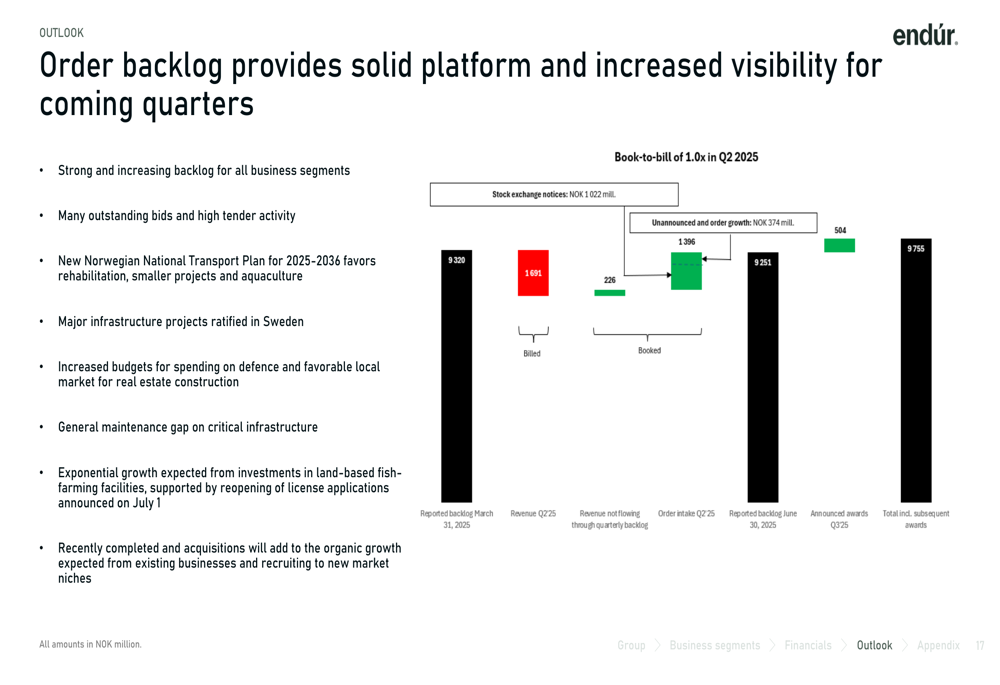

The company maintained strong cash generation with a last twelve months (LTM) cash conversion rate of 159%. Profit after tax reached NOK 42.5 million for the quarter, while the company’s order backlog remained substantial at NOK 9.3 billion, providing solid visibility for future quarters.

CEO Jeppe Raaholt highlighted that the company has already secured new awards worth NOK 504 million in the early part of Q3 2025, further strengthening its position.

Segment Performance Analysis

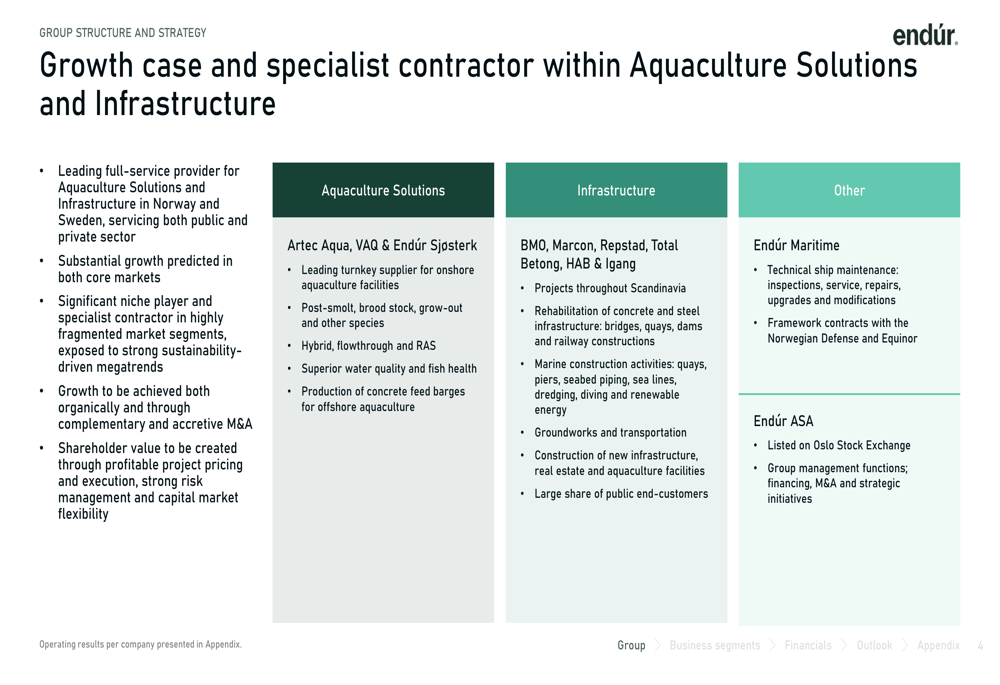

Endúr operates through three main segments: Aquaculture Solutions, Infrastructure, and Other (primarily Endúr Maritime). The company’s structure and strategic positioning are illustrated in this organizational overview:

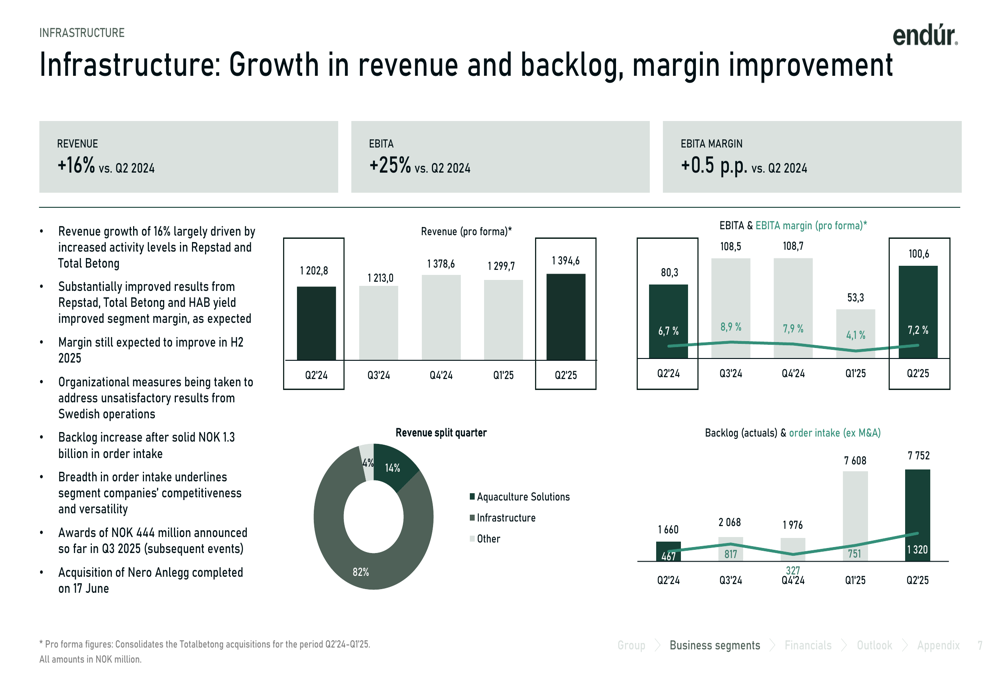

The Infrastructure segment emerged as the primary growth driver during Q2, with revenue increasing 16% year-over-year and EBITA growing by 25%. The segment’s EBITA margin improved by 0.5 percentage points compared to Q2 2024. This performance is visualized in the following segment breakdown:

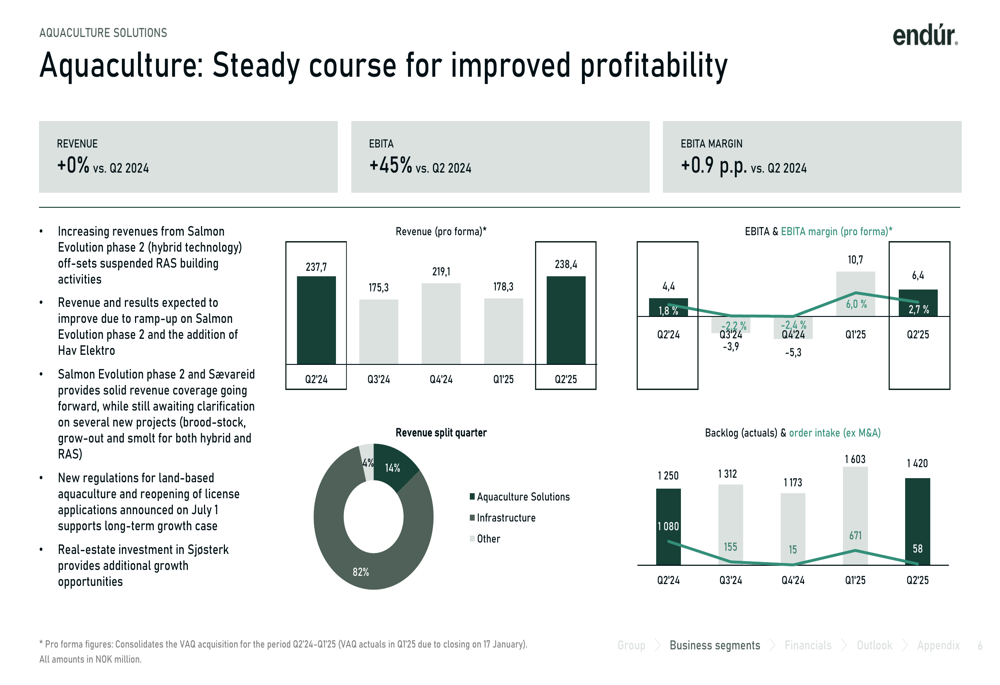

Meanwhile, the Aquaculture Solutions segment maintained steady revenue levels compared to the same period last year, but significantly improved profitability with a 45% increase in EBITA and a 0.9 percentage point expansion in EBITA margin. The company noted that increasing revenues from Salmon Evolution phase 2 (hybrid technology) offset suspended RAS building activities.

The company’s "Other" segment, primarily consisting of Endúr Maritime, saw declining performance with revenue down 17% and EBITA falling 49% compared to Q2 2024. Management indicated this reflects the finalization of an old framework contract, with expectations for improvement in coming quarters.

Financial Position and Outlook

Endúr maintained a strong financial position with cash at bank of NOK 866 million and an additional NOK 250 million in non-utilized overdraft facilities, bringing total available liquidity to NOK 1,116 million. The company’s equity ratio stood at 36.3%.

The detailed profit and loss statement reveals the company’s financial performance across key metrics:

Looking ahead, management expressed confidence in the company’s growth trajectory, supported by a strong and increasing backlog across all business segments. The presentation highlighted high tender activity and noted that major infrastructure projects have been ratified in Sweden, potentially creating additional opportunities.

Strategic Initiatives

Endúr continues to demonstrate versatility through a diverse range of project wins across multiple sectors. Recent contract awards span public buildings, residential properties, harbor infrastructure, railway projects, and recreational facilities, underscoring the company’s broad capabilities.

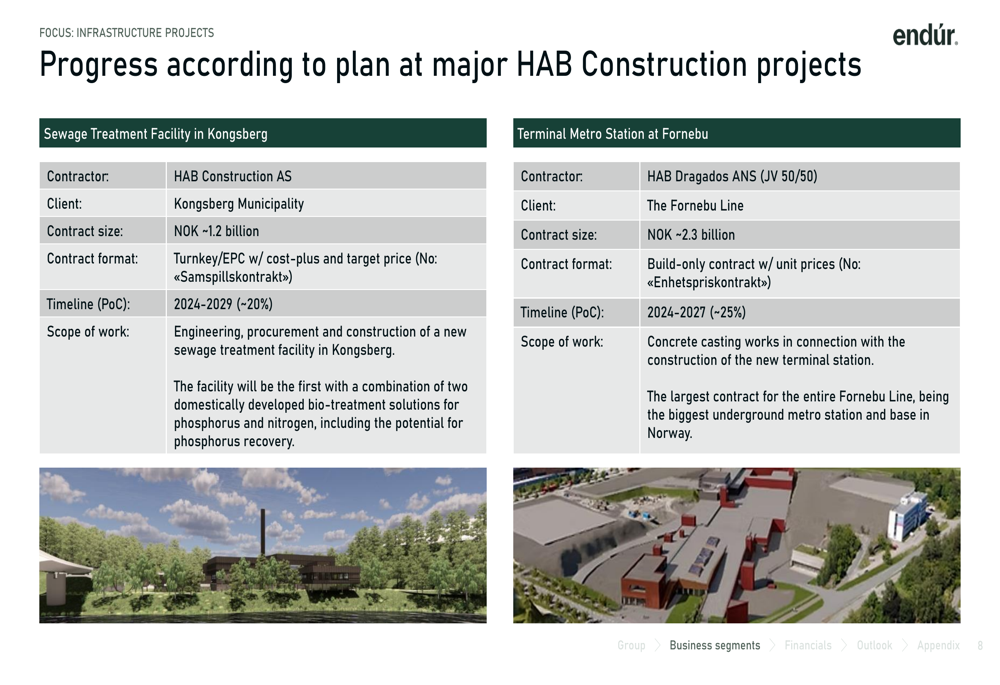

The company highlighted significant progress on major construction projects, including a sewage treatment facility in Kongsberg and the terminal metro station at Fornebu, which represents the largest contract for the entire Fornebu Line.

Management also pointed to positive regulatory developments, noting that new regulations for land-based aquaculture and the reopening of license applications announced on July 1, 2025, support the long-term growth case for its Aquaculture Solutions segment.

In summary, Endúr’s Q2 2025 results demonstrate continued momentum across its core business segments, with particularly strong performance in Infrastructure driving overall growth. The company’s substantial backlog, combined with recent project wins and a robust balance sheet, positions it well for sustained performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.