Bitcoin price today: slips below $113k, near 6-wk low despite Fed cut bets

Energy Vault Holdings Inc (NYSE:NRGV) reported its first quarter 2025 financial results on May 12, revealing substantial margin improvement despite modest revenue growth as the company continues its strategic transition toward a build-own-operate business model.

Quarterly Performance Highlights

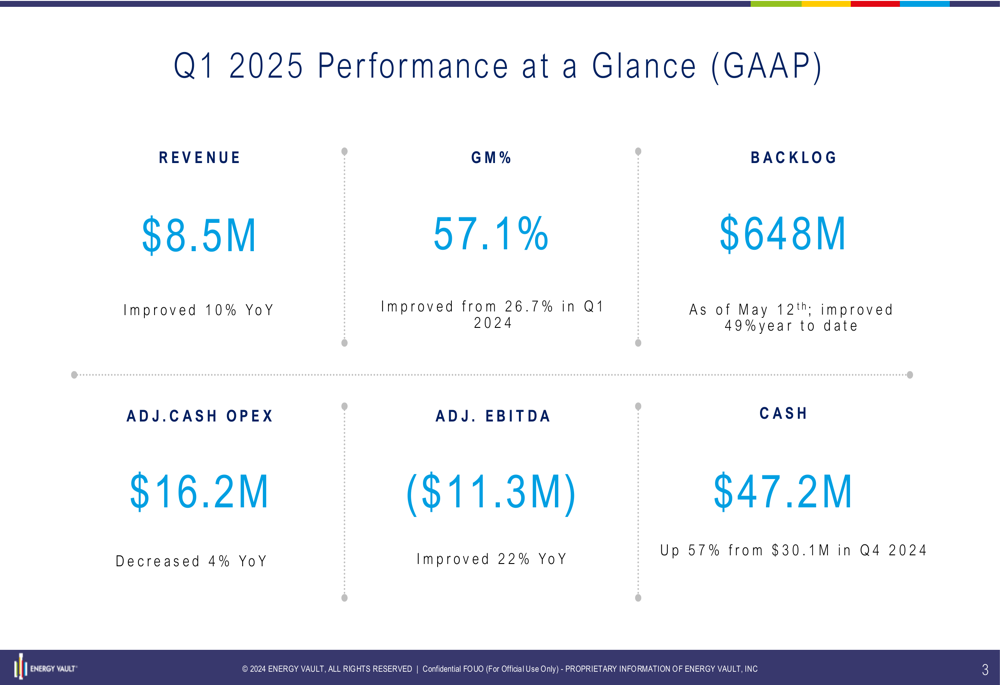

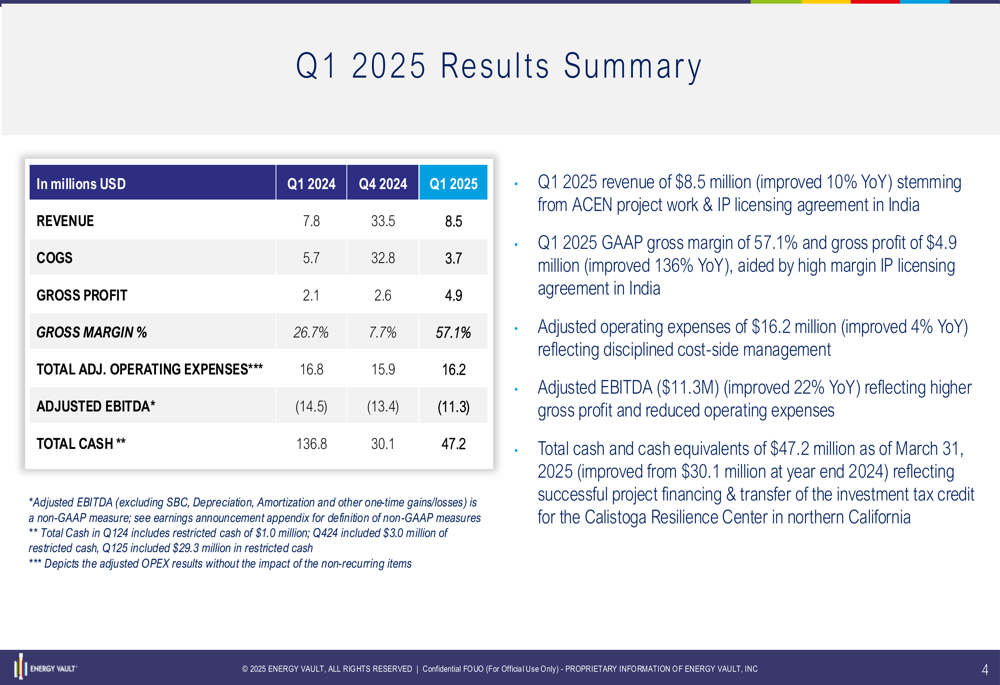

Energy Vault reported Q1 2025 revenue of $8.5 million, representing a 10% year-over-year increase from $7.8 million in Q1 2024. While this figure marks a significant sequential decline from the $33.5 million reported in Q4 2024, the company achieved remarkable improvement in profitability metrics.

The most notable performance highlight was the dramatic expansion in gross margin, which reached 57.1% in Q1 2025, more than doubling from 26.7% in the same period last year. This margin improvement was primarily driven by high-margin IP licensing agreements in India, according to the company’s presentation.

As shown in the following financial overview:

The company also reported an improved adjusted EBITDA loss of $11.3 million, representing a 22% year-over-year improvement. Energy Vault’s cash position strengthened significantly to $47.2 million as of March 31, 2025, up 57% from $30.1 million at the end of Q4 2024, reflecting successful project financing and transfer of investment tax credits for the Calistoga Resilience Center in northern California.

A more detailed breakdown of the quarterly results shows the company’s financial trajectory:

The stock reacted negatively to the earnings release, falling 11.22% in aftermarket trading to $0.95 per share, despite the improved margins and cash position. This reaction follows a strong regular session where the stock gained 39.87% to close at $1.07.

Commercial Pipeline and Backlog

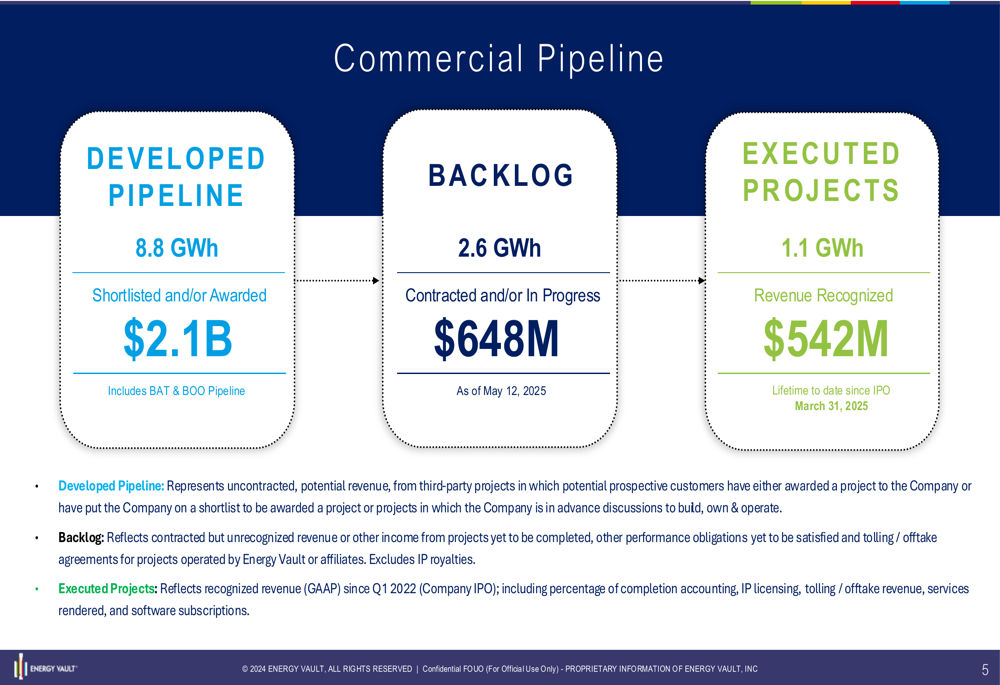

Energy Vault reported a substantial commercial pipeline, with $648 million in backlog as of May 12, 2025, representing a 49% increase year-to-date. The company’s total developed pipeline stands at 8.8 GWh with a potential value of $2.1 billion.

The following visualization illustrates the company’s commercial pipeline progression:

The company has recognized $542 million in revenue from executed projects since its IPO, representing 1.1 GWh of energy storage capacity. This demonstrates Energy Vault’s ability to convert pipeline opportunities into revenue, though the pace of conversion remains a key focus for investors.

Strategic Initiatives & Project Updates

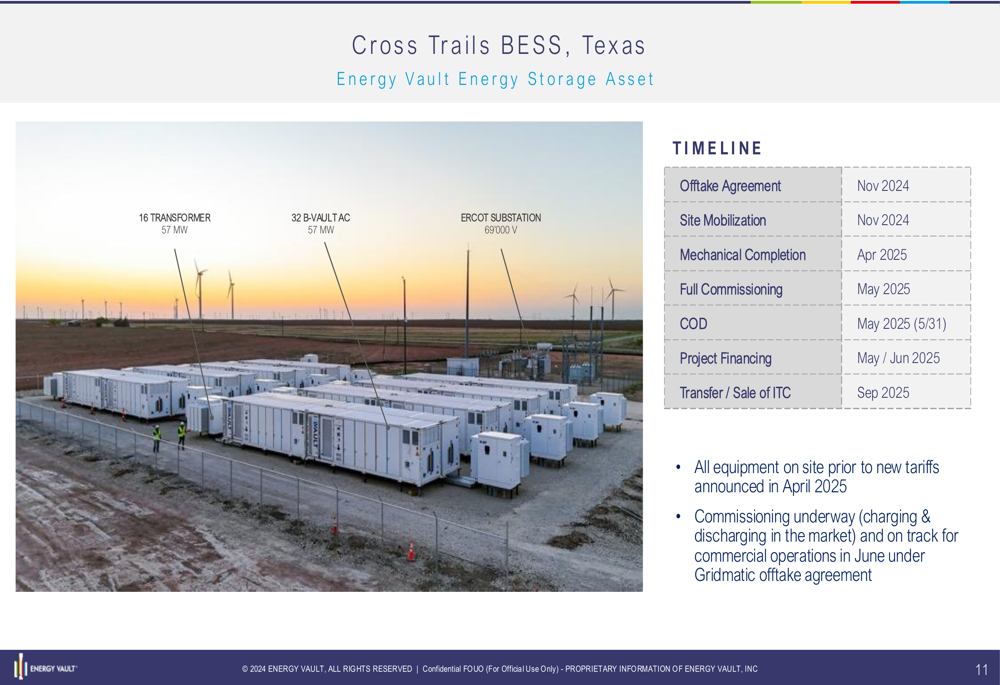

Energy Vault continues to advance its strategic transition toward a build-own-operate business model, which aims to generate recurring revenue and more stable cash flows. The Cross Trails Battery Energy Storage System (BESS) project in Texas represents a significant milestone in this strategy, with commissioning currently underway and commercial operation targeted for June 2025.

The project timeline and key milestones are illustrated below:

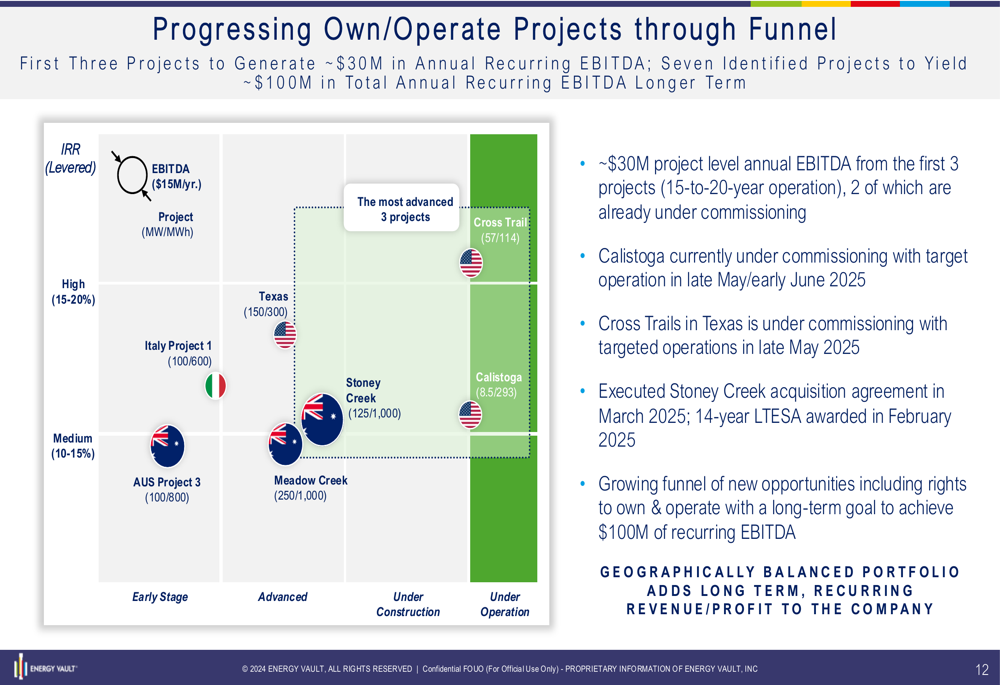

The company is progressing multiple owned and operated projects through its development funnel, with a target of approximately $30 million in project-level annual EBITDA from the first three projects. This geographically balanced portfolio is expected to add long-term recurring revenue and profit to the company.

As shown in the following project progression visualization:

Financial Outlook & Risk Mitigation

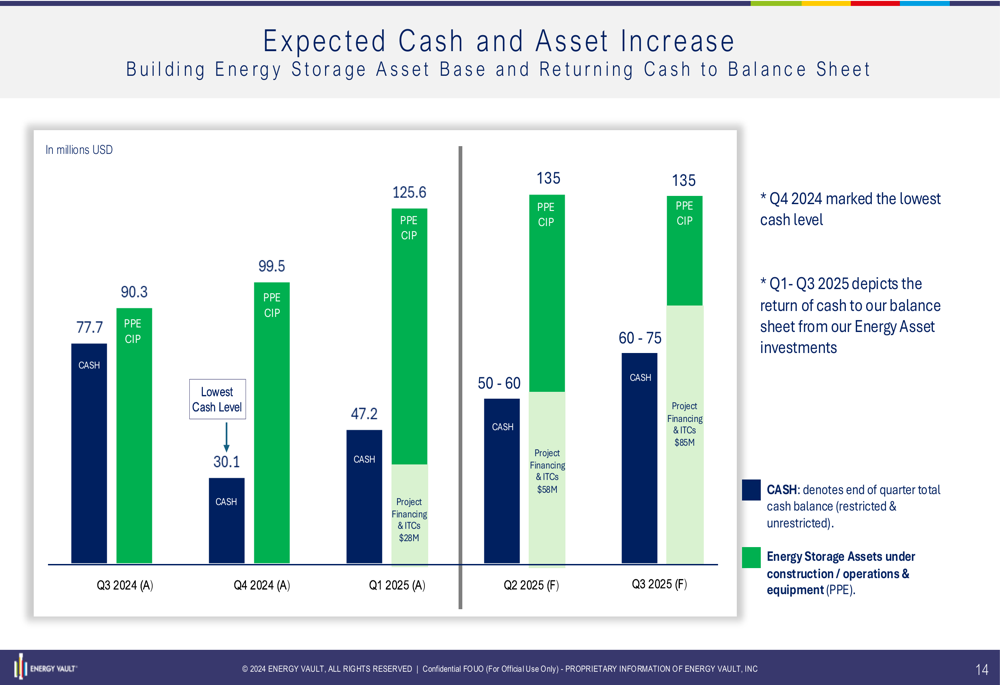

Energy Vault expects its cash position and asset base to continue improving throughout 2025, driven by project financing and investment tax credits. The company projects a significant increase in both cash and property, plant, and equipment (PPE) assets in the coming quarters.

The projected financial improvement is illustrated in this chart:

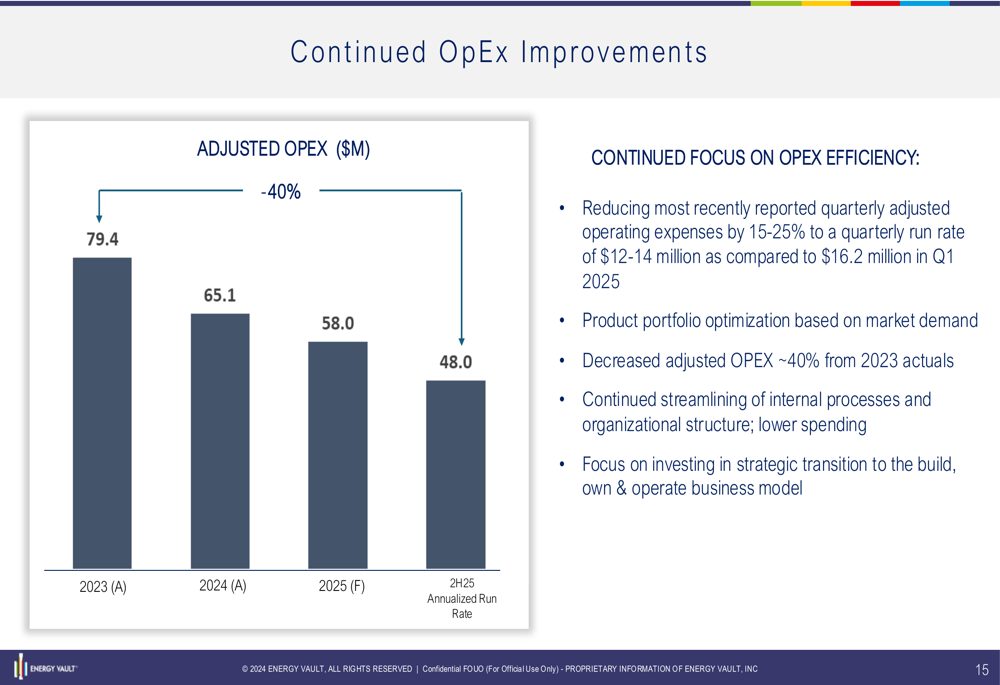

The company is also making substantial progress in reducing operating expenses, with plans to decrease quarterly adjusted operating expenses by 15-25% to a run rate of $12-14 million. This represents approximately a 40% reduction from 2023 levels, as shown below:

Addressing potential headwinds, Energy Vault highlighted that approximately 90% of its contracted revenue backlog is not impacted by China/US tariffs due to its non-US regional and business mix. The company has secured non-Chinese battery manufacturing capabilities and noted that the current China-US tariff pause is an encouraging sign.

Market Context & Conclusion

Energy Vault’s Q1 2025 results come after a challenging Q4 2024, where the company missed revenue expectations and reported a larger-than-expected loss per share. The improvement in gross margin and cash position suggests the company may be turning a corner, though revenue growth remains modest.

The strategic pivot toward owned and operated projects represents a significant shift in business model, potentially providing more stable and predictable revenue streams. However, this transition requires substantial upfront capital investment, which explains the company’s focus on project financing and investment tax credits.

With a stock price that has experienced significant volatility, trading near its 52-week low before the recent earnings-day surge, Energy Vault faces continued pressure to demonstrate that its strategic transition can deliver sustainable growth and a path to profitability. The substantial improvement in gross margin provides a positive signal, but investors will be watching closely to see if revenue growth can accelerate in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.