Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

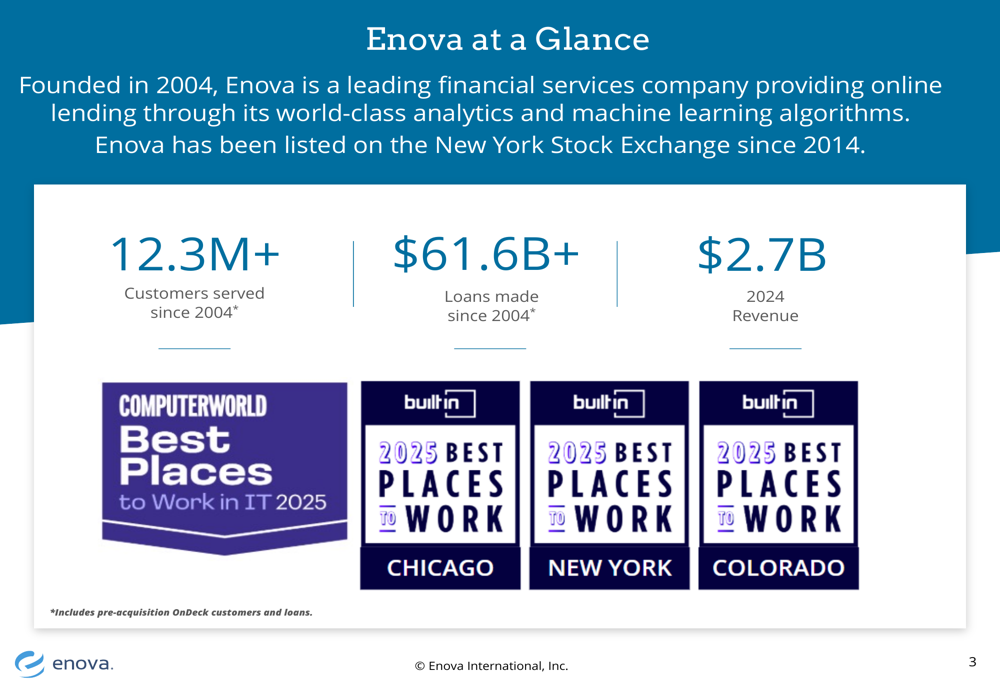

Enova International Inc (NYSE:ENVA) delivered impressive results in its Q1 2025 investor presentation, showcasing substantial growth across key metrics while highlighting the company’s technology-driven approach to serving underserved financial markets. The online financial services provider, which has been operating since 2004 and publicly traded since 2014, continues to demonstrate strong momentum in both its consumer and small business lending segments.

The company’s stock responded positively to the earnings announcement, rising 0.94% in aftermarket trading to $100.49, reflecting investor confidence in Enova’s business model and growth trajectory. The stock has performed exceptionally well over the past year, delivering a 61.27% return according to available data, while trading at an attractive valuation relative to its growth rate.

As shown in the following overview of the company’s scale and reach:

Quarterly Performance Highlights

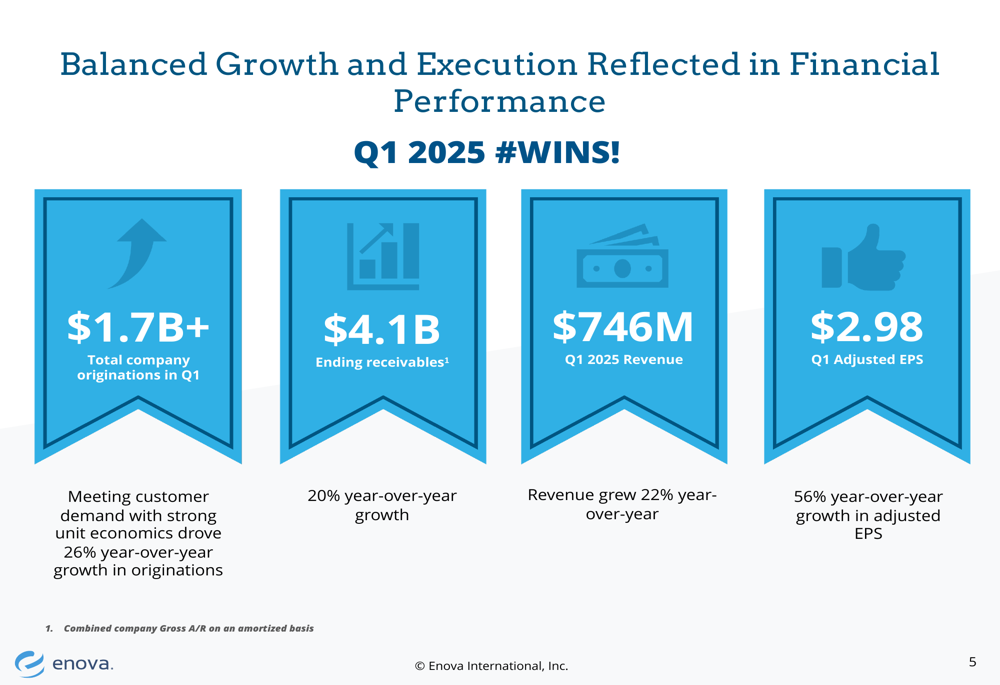

Enova reported robust financial results for Q1 2025, with revenue reaching $746 million, representing a 22% increase year-over-year and exceeding analyst expectations of $734.15 million. The company’s adjusted earnings per share of $2.98 significantly outperformed forecasts of $2.76, marking a substantial 56% increase compared to the same period last year.

This performance was driven by strong origination growth of 26% year-over-year, with total company originations exceeding $1.7 billion for the quarter. The company’s ending receivables grew to $4.1 billion, a 20% increase from Q1 2024, demonstrating continued expansion of Enova’s lending portfolio.

The following slide illustrates these key financial metrics and their year-over-year growth rates:

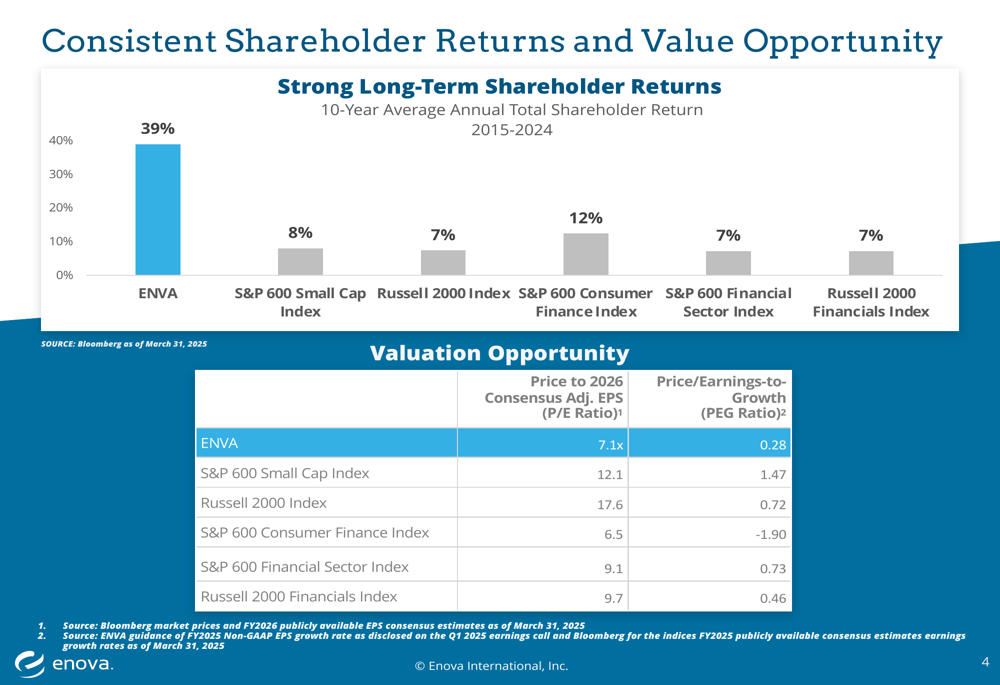

Enova’s financial performance has been consistently strong over an extended period, with the company achieving a 10-year average annual total shareholder return of 39% from 2015 to 2024. This significantly outperforms relevant benchmarks, including the S&P 600 Small Cap Index (8%), Russell 2000 Index (7%), and S&P 600 Consumer Finance Index (12%).

The company also highlighted its attractive valuation metrics, with a Price to 2026 Consensus Adjusted EPS (P/E Ratio) of 7.1x and a Price/Earnings-to-Growth (PEG) Ratio of 0.28, suggesting potential undervaluation relative to its growth profile and peer group.

Strategic Initiatives

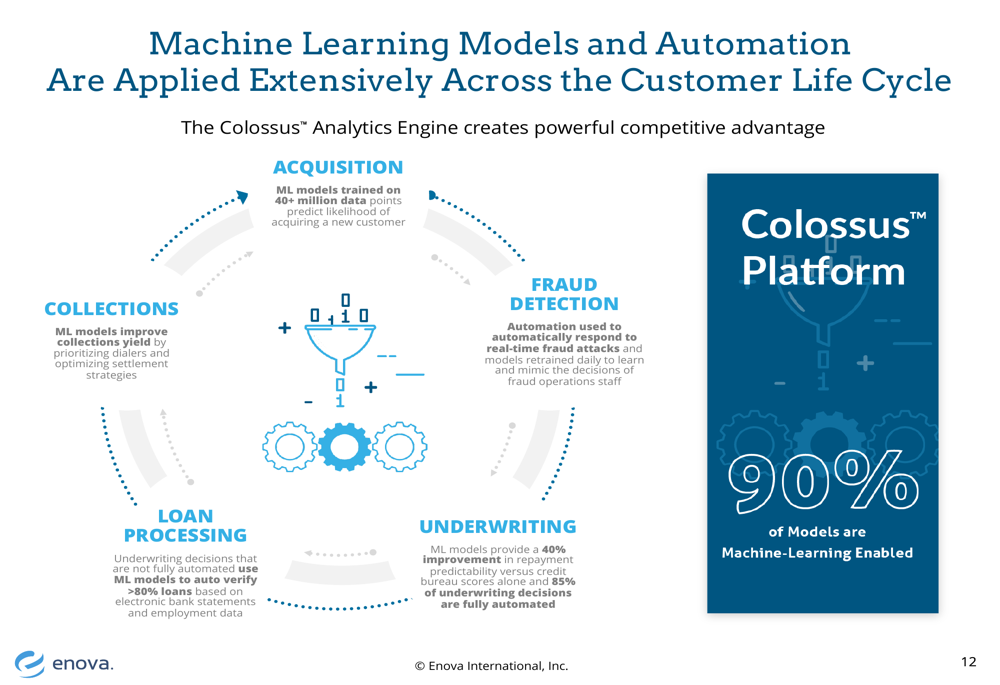

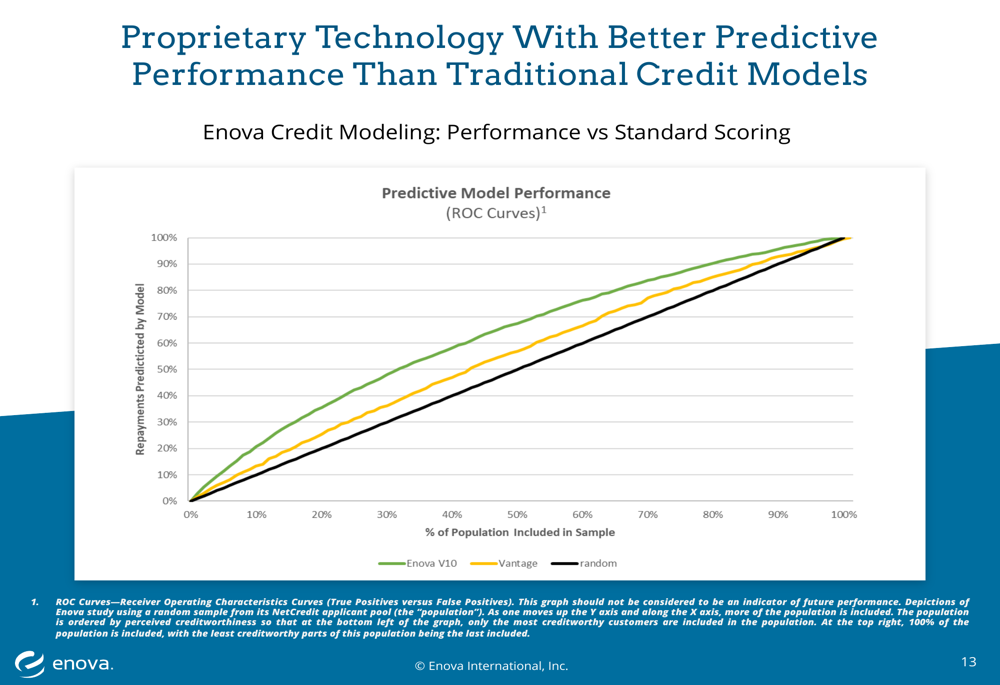

Enova’s success is built on its proprietary technology platform and advanced analytics capabilities. The company emphasized that 90% of its models are machine learning-enabled, resulting in a 40% improvement in repayment predictability compared to traditional methods. This technological advantage allows Enova to more accurately assess risk and serve customer segments that are often overlooked by traditional financial institutions.

The following illustration demonstrates how machine learning and automation are integrated throughout Enova’s business processes:

The company’s proprietary credit models have demonstrated superior predictive performance compared to standard credit scoring methods. This technological edge enables Enova to make more informed lending decisions while maintaining strong credit performance, even during economic downturns.

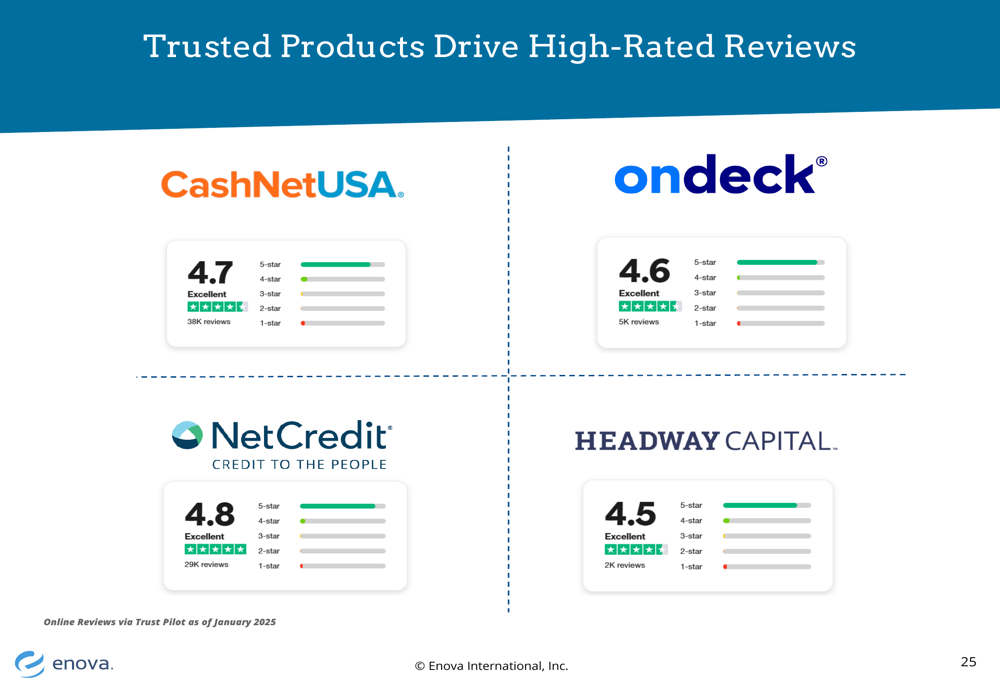

Customer satisfaction remains high across Enova’s product portfolio, with impressive ratings on Trustpilot. CashNetUSA maintains a 4.7-star rating from 38,000 reviews, while NetCredit boasts a 4.8-star rating from 29,000 reviews. The company’s small business lending products also receive strong customer feedback, with OnDeck earning a 4.6-star rating from 5,000 reviews and Headway Capital achieving a 4.5-star rating from 2,000 reviews.

Competitive Industry Position

Enova operates in substantial addressable markets with significant growth potential. The U.S. Consumer Loans market is estimated at $253 billion, while the U.S. Small and Medium-Sized Business (SMB) Loans market represents approximately $271 billion. Notably, Enova currently holds less than 1% market share in both segments, indicating substantial room for expansion.

The company’s focus on underserved populations is supported by market data showing that 37% of Americans cannot cover an emergency expense of $400, and over half of non-prime Americans face three or more unexpected expenses per year. Additionally, 34% of small businesses that apply for loans from large banks are rejected, highlighting the need for alternative lending solutions.

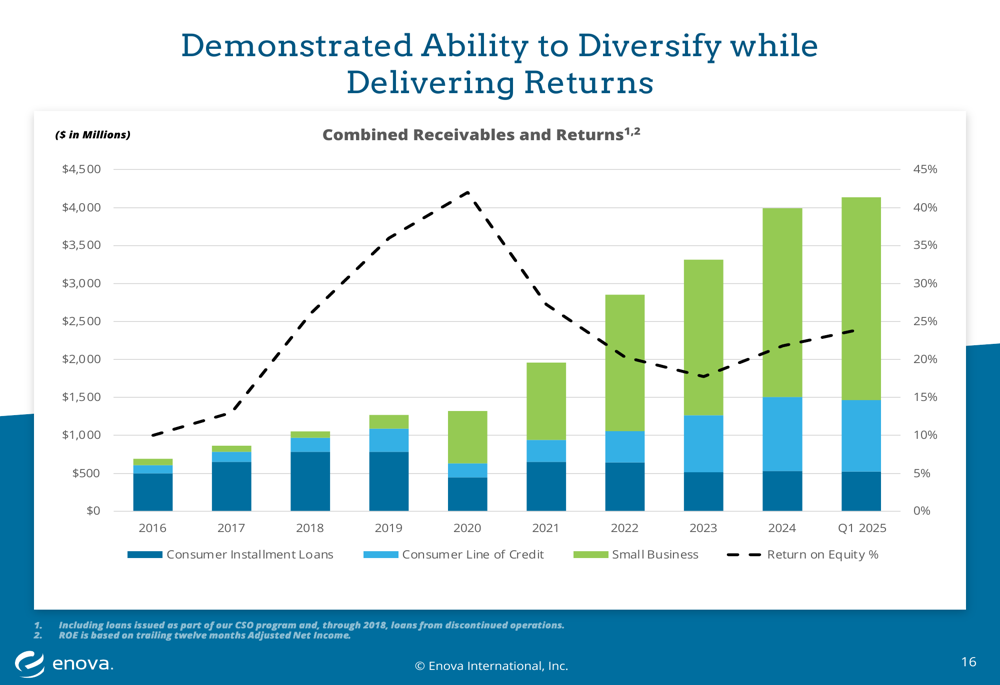

Enova’s diversified portfolio has evolved over time, with a balanced mix of consumer installment loans, consumer lines of credit, and small business loans. This diversification has contributed to improved risk profiles and consistent returns on equity.

Financial Performance Trends

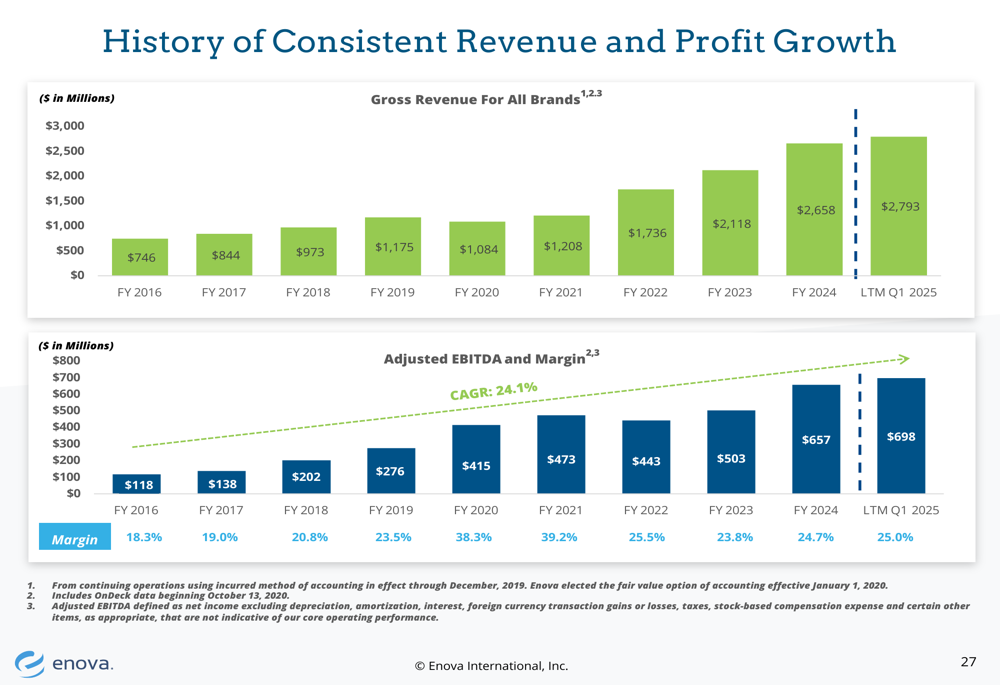

Enova has demonstrated consistent revenue and profit growth over multiple years. From 2016 to Q1 2025, the company achieved a compound annual growth rate (CAGR) of 24.1% for revenue, while maintaining strong adjusted EBITDA margins around 25%.

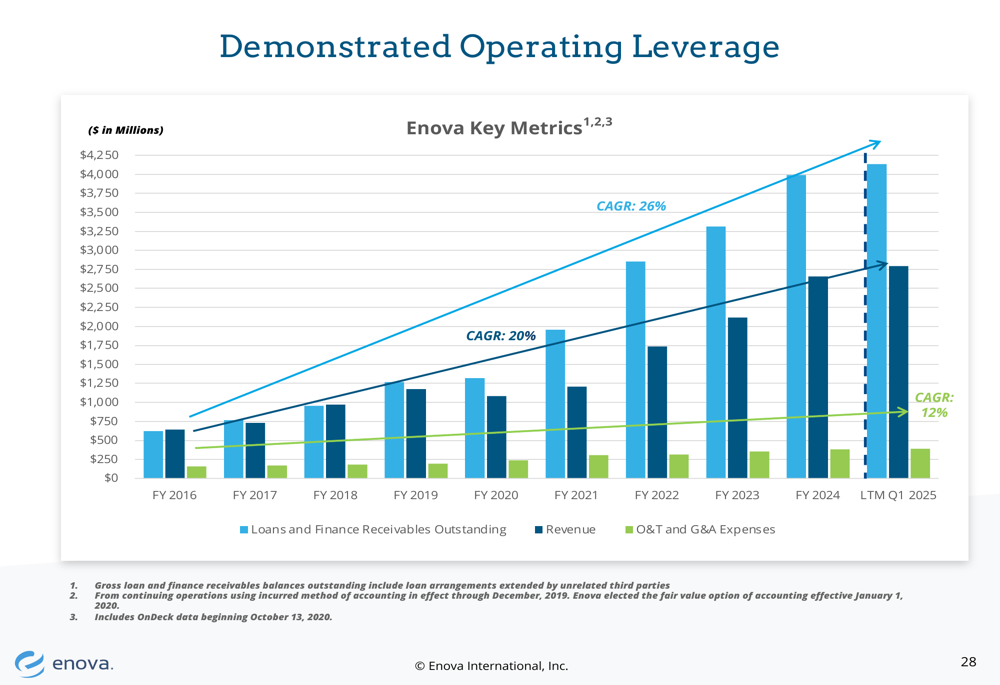

The following chart illustrates this long-term growth trajectory:

A key strength of Enova’s business model is its demonstrated operating leverage. As the company has scaled its loan portfolio and revenue, it has maintained disciplined control over operating expenses, allowing for expanding profit margins. This efficiency is particularly evident in the relationship between revenue growth and operating expense growth.

Credit performance has remained strong despite economic fluctuations, with the company reporting an improved net charge-off ratio of 8.6% in Q1 2025, down from 8.9% in the previous quarter. This stability reflects Enova’s sophisticated risk management capabilities and diversified lending approach.

Forward-Looking Statements

Looking ahead, Enova expects Q2 2025 revenue to be flat to slightly higher sequentially, with full-year originations growth projected at a minimum of 15%. Management anticipates that full-year revenue growth will outpace originations, with adjusted EPS growth expected to be at least 25%.

CEO David Fisher expressed confidence in the company’s outlook, stating, "We continue to demonstrate that our flexible online-only business model, well-diversified portfolio, world-class technology, proprietary analytics, and experienced team can deliver consistent results."

CFO Steve Cunningham added, "Our resilient direct online-only business model, diversified product offerings, nimble machine learning-powered credit risk management capabilities, and solid balance sheet support our ability to continue to drive profitable growth while also effectively managing risk."

While management maintains an optimistic outlook, they acknowledged potential challenges, including the impact of tariffs on small business lending, changes in customer mix affecting credit performance, and macroeconomic factors such as wage growth and consumer spending that require ongoing monitoring.

Overall, Enova’s Q1 2025 presentation portrays a company with strong financial performance, technological advantages, and significant growth potential in large addressable markets, positioning it well for continued success in the non-prime lending space.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.