Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Enovis Corporation (NYSE:ENOV) shares fell nearly 5% in premarket trading following its first quarter 2025 earnings presentation on May 8, despite reporting strong revenue growth, as tariff concerns prompted a reduction in full-year profit guidance.

Introduction & Market Context

The medical technology company reported 8% revenue growth in the first quarter, exceeding analyst expectations, but simultaneously reduced its full-year profit outlook due to anticipated tariff impacts. The stock traded at $32.55 in premarket, down 4.94% from its previous close of $34.24, continuing a challenging trend that has seen shares trade near 52-week lows.

"Strong start to 2025 and underlying fundamentals across key businesses," stated the company in its presentation summary slide, highlighting above-market growth in its Reconstructive segment and momentum from new product launches.

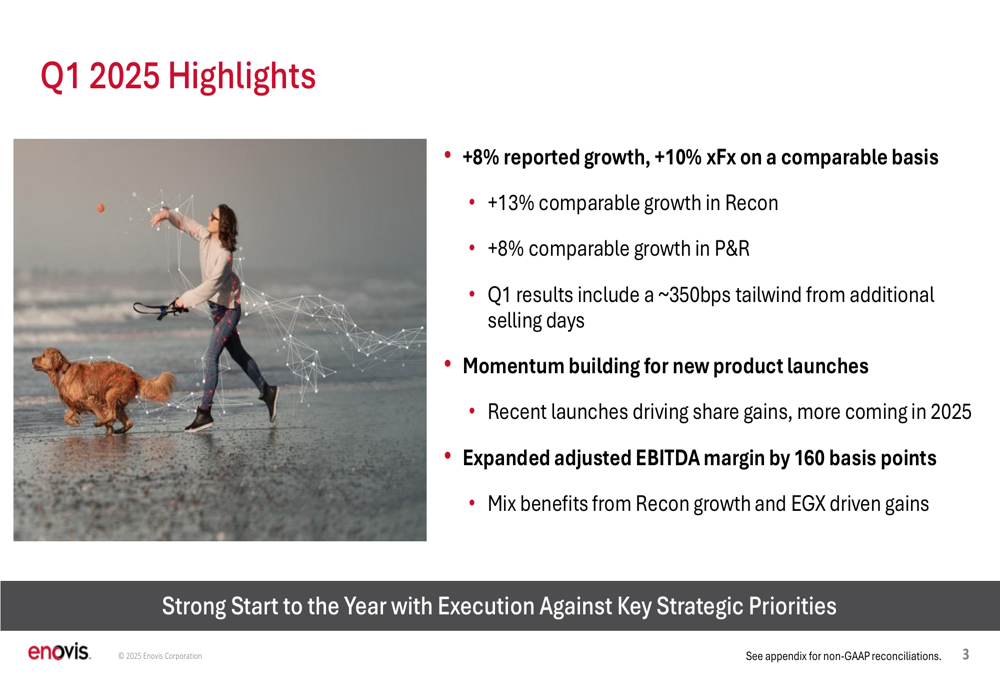

As shown in the following quarterly highlights:

Quarterly Performance Highlights

Enovis reported first quarter revenue of $559 million, up from $516 million in the same period last year, representing 8% reported growth and 10% growth on a comparable constant currency basis. The company noted that Q1 results included approximately 350 basis points of tailwind from additional selling days compared to the prior year.

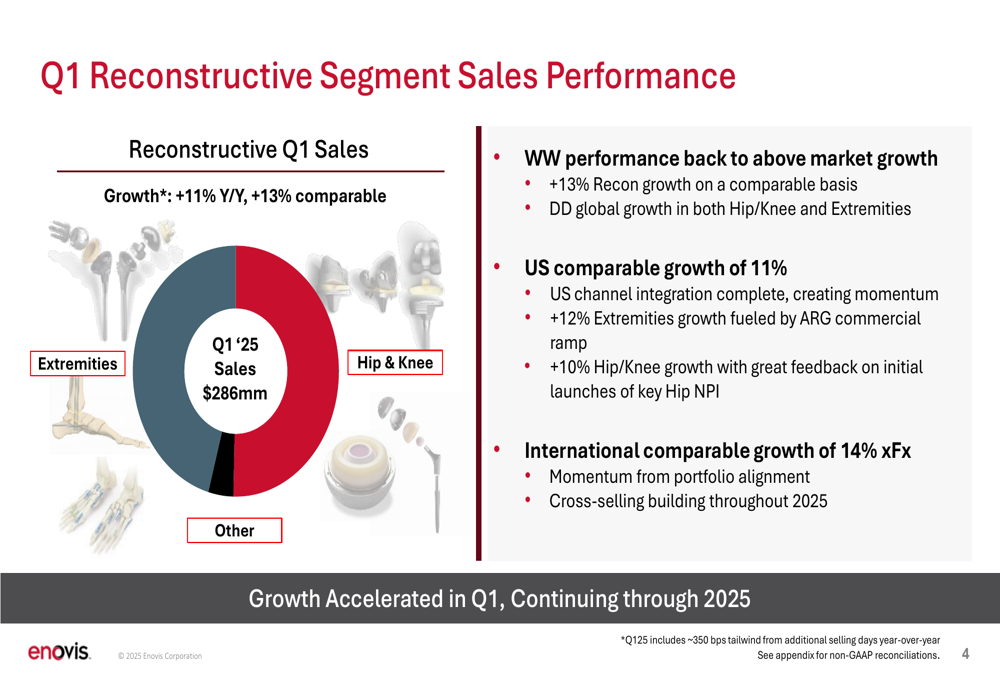

The Reconstructive segment delivered particularly strong results with 13% comparable growth, outpacing market averages. This performance was driven by double-digit global growth in both Hip/Knee and Extremities product lines.

The segment breakdown shows strong performance across both business units:

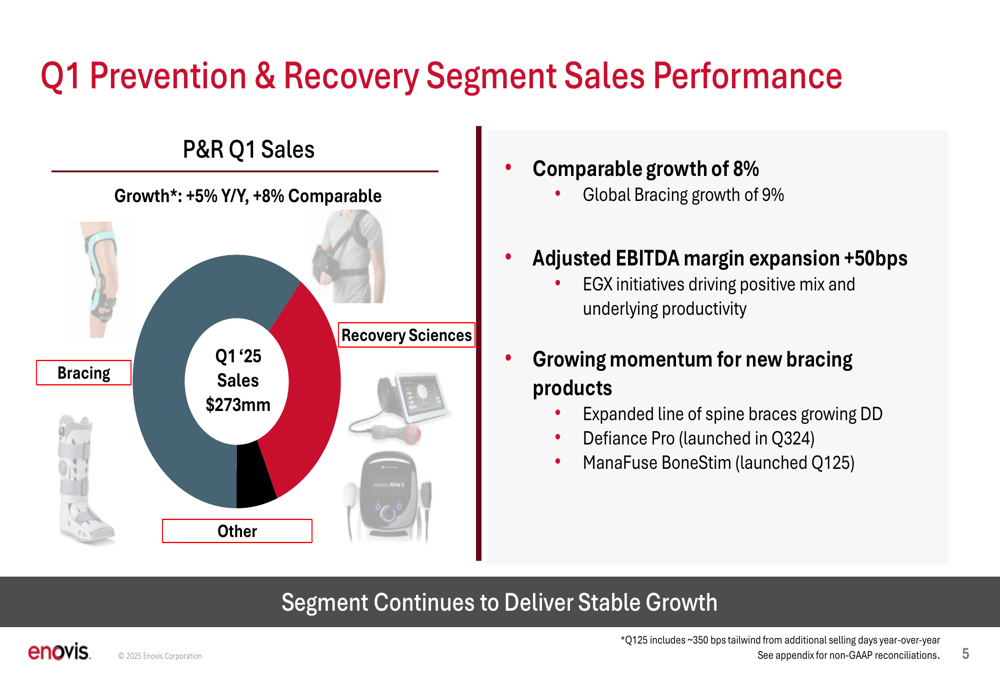

The Prevention & Recovery (P&R) segment also performed well, posting 8% comparable growth with global Bracing growth of 9%. The segment expanded its adjusted EBITDA margin by 50 basis points through efficiency initiatives driving positive mix and underlying productivity.

Detailed Financial Analysis

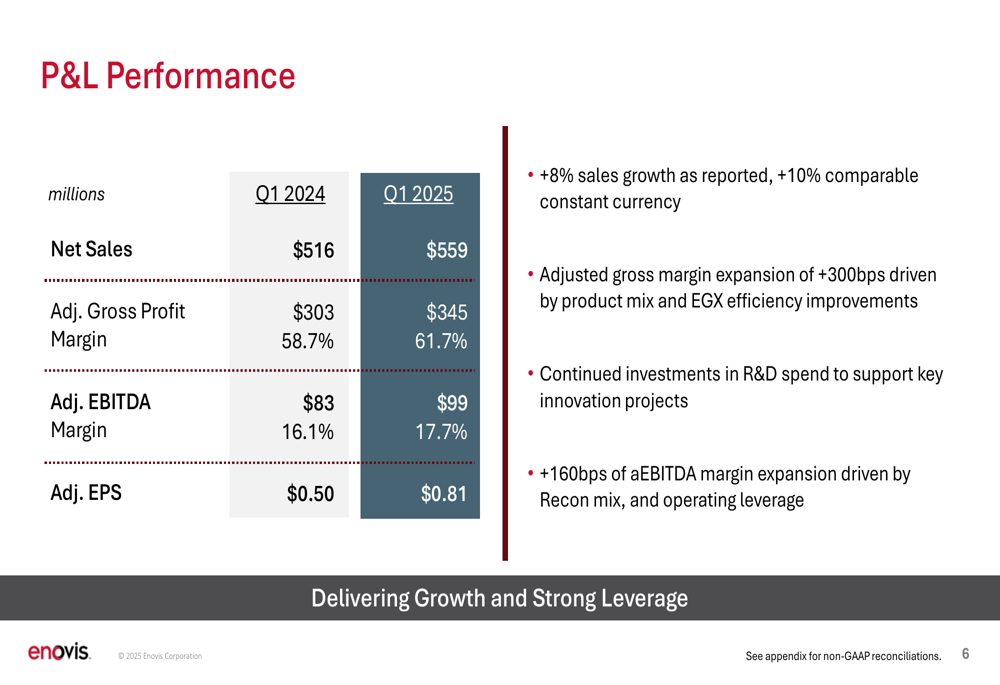

Enovis demonstrated significant margin expansion in the first quarter, with adjusted gross margin improving by 300 basis points to 61.7%, compared to 58.7% in Q1 2024. This improvement was primarily driven by favorable product mix and efficiency improvements from the company’s EGX (Enovis Growth Excellence) initiatives.

Adjusted EBITDA increased to $99 million from $83 million in the prior year, with margins expanding 160 basis points to 17.7%. Adjusted earnings per share grew substantially to $0.81, up from $0.50 in Q1 2024, representing a 62% increase.

The financial performance comparison clearly illustrates these improvements:

Strategic Initiatives

The company highlighted several strategic initiatives driving its growth. In the Reconstructive segment, the U.S. channel integration has been completed, creating momentum for future growth. The segment saw 12% growth in Extremities, fueled by the commercial ramp of ARG products, while Hip/Knee products grew 10% with positive feedback on initial launches of key Hip new product introductions.

In the Prevention & Recovery segment, new bracing products are gaining traction, with an expanded line of spine braces growing double digits. Recently launched products include Defiance Pro (launched in Q3 2024) and ManaFuse BoneStim (launched in Q1 2025).

Forward-Looking Statements

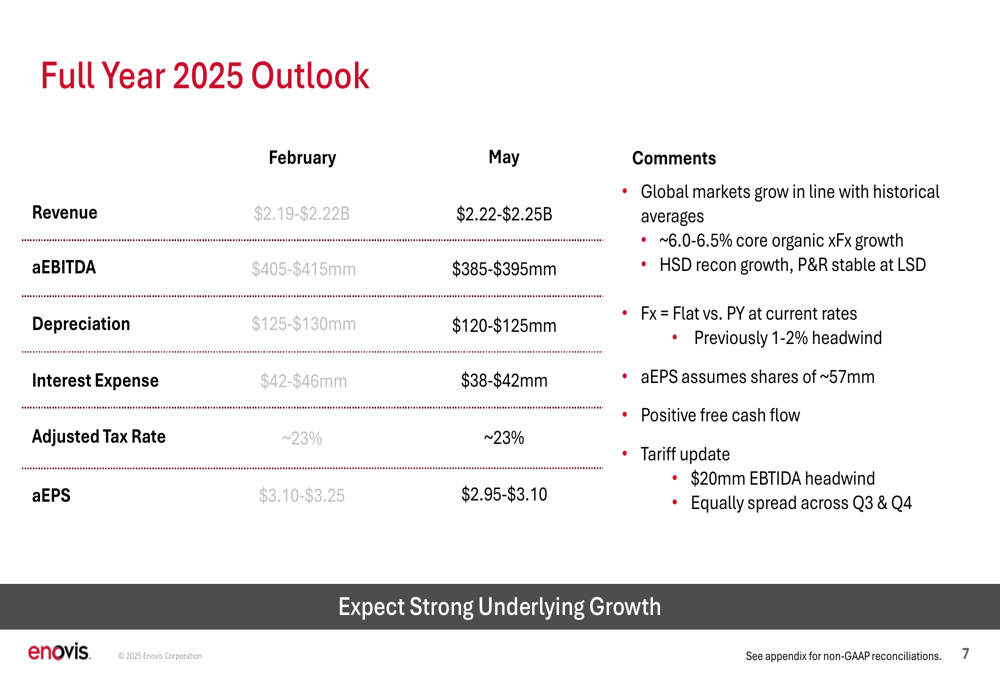

Despite strong Q1 results, Enovis revised its full-year 2025 outlook, raising revenue expectations but lowering profit projections. The company now expects revenue between $2.22-$2.25 billion, up from its February projection of $2.19-$2.22 billion. However, adjusted EBITDA guidance was reduced to $385-$395 million from the previous $405-$415 million, and adjusted EPS guidance was lowered to $2.95-$3.10 from $3.10-$3.25.

The revised outlook reflects the company’s expectation of a $20 million EBITDA headwind from tariffs, equally spread across Q3 and Q4:

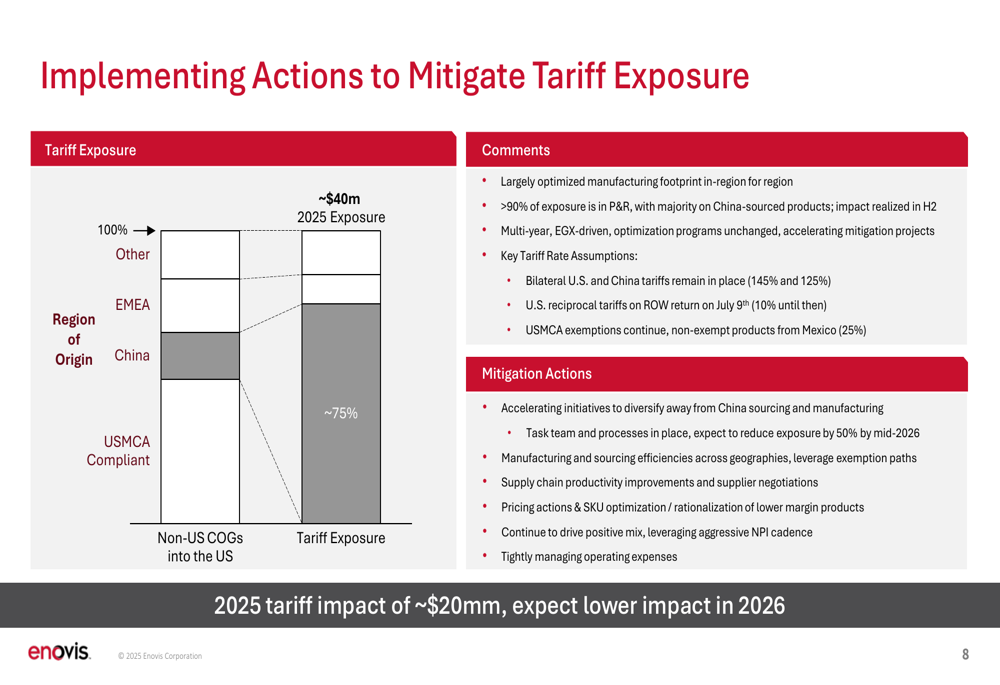

Enovis is implementing comprehensive actions to mitigate tariff exposure, which primarily affects its Prevention & Recovery segment. The company noted that approximately 75% of its $40 million tariff exposure is addressable through various mitigation strategies, including diversifying away from China sourcing and manufacturing, leveraging exemption paths, implementing supply chain productivity improvements, and taking pricing actions.

The company expects to reduce its tariff exposure by 50% by mid-2026 through these initiatives:

Conclusion

Enovis delivered strong first quarter results with above-market growth across its key segments, demonstrating the success of its strategic initiatives and new product launches. However, the revised full-year guidance reflects significant challenges from the changing global trade environment, particularly tariff impacts that are expected to materialize in the second half of 2025.

While the company maintains a positive outlook on its underlying business fundamentals and growth trajectory, investors appear concerned about the profit impact of tariffs, as reflected in the premarket stock decline. Management’s proactive approach to tariff mitigation and continued focus on innovation and commercial execution will be critical factors to watch in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.