Can anything shut down the Gold rally?

Introduction & Market Context

The Ensign Group , Inc. (NASDAQ:ENSG) presented its Q2 2025 investor presentation on July 25, 2025, highlighting strong financial performance and continued growth in the post-acute healthcare sector. The company’s stock jumped 8.92% during regular trading hours and continued to rise by an additional 7.43% in after-hours trading following the presentation, reflecting positive investor sentiment.

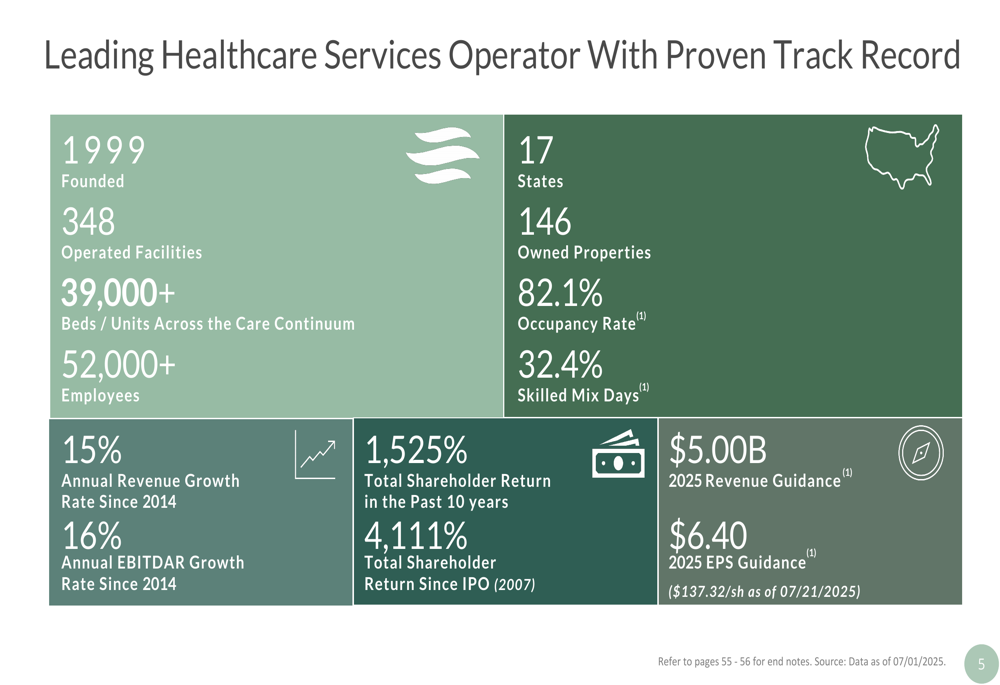

Founded in 1999, Ensign has grown into a leading healthcare services provider with 348 facilities across 17 states, employing over 52,000 people and serving patients through more than 39,000 beds and units. The company continues to outperform the broader post-acute care sector through its unique local leadership model and focus on clinical excellence.

As shown in the following overview of Ensign’s key metrics and achievements:

Quarterly Performance Highlights

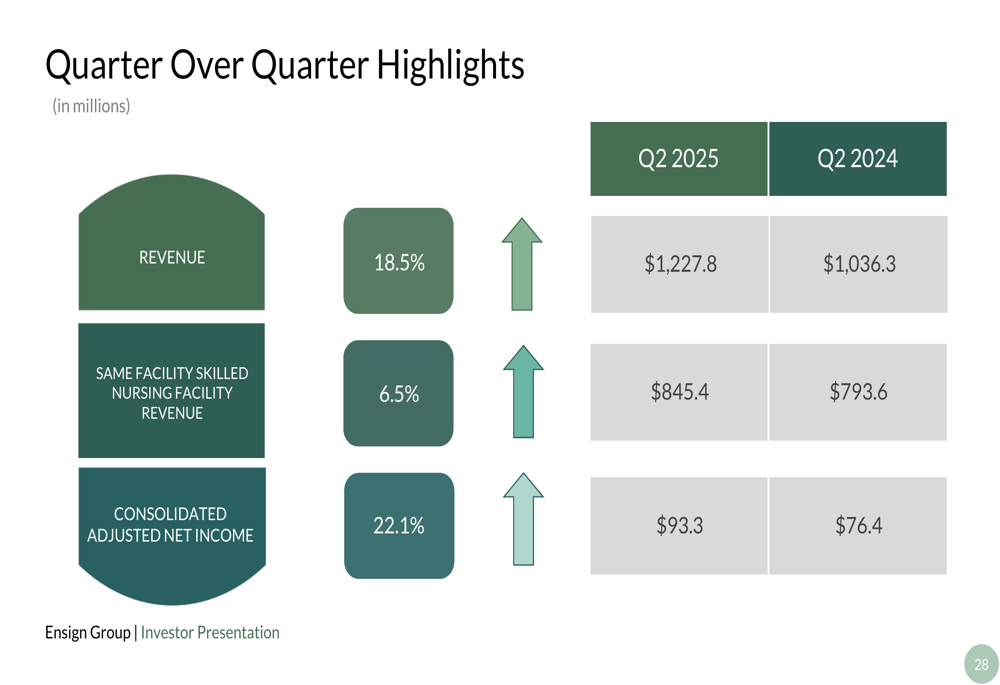

Ensign Group reported impressive financial results for Q2 2025, with revenue increasing by 18.5% to $1,227.8 million compared to $1,036.3 million in Q2 2024. Same facility skilled nursing revenue grew by 6.5% to $845.4 million, while consolidated adjusted net income rose by 22.1% to $93.3 million.

The quarter’s strong performance builds on momentum from Q1 2025, when the company reported adjusted EPS of $1.52 and revenue of $1.2 billion. The consistent growth trajectory demonstrates Ensign’s ability to execute its operational strategy effectively.

The following chart illustrates Ensign’s Q2 2025 financial highlights compared to the same period last year:

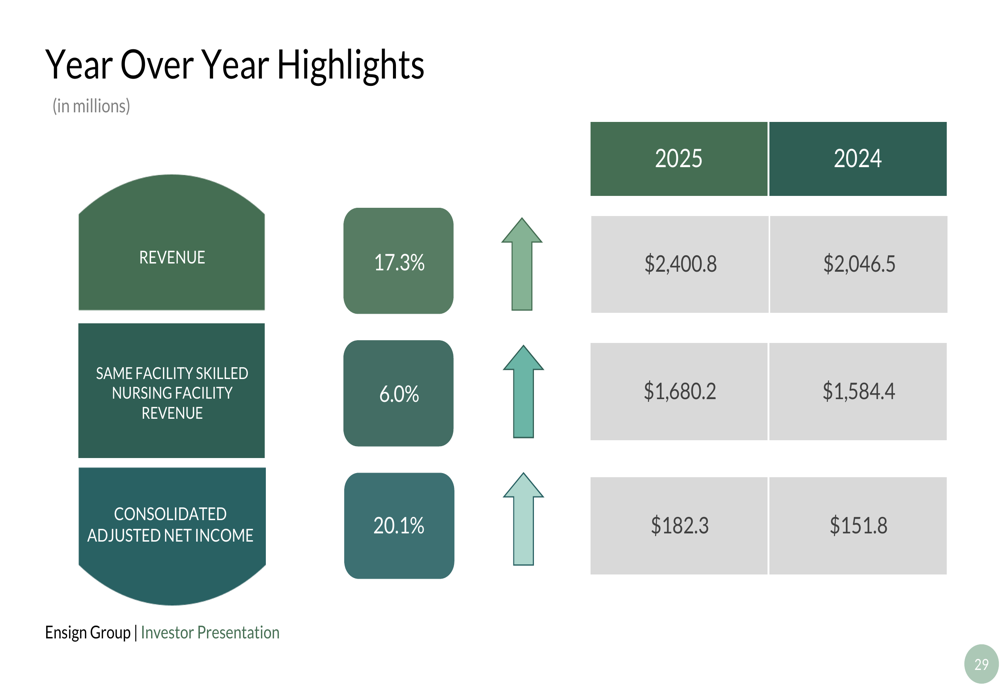

For the first half of 2025, Ensign reported equally strong results with revenue up 17.3% to $2,400.8 million and consolidated adjusted net income increasing by 20.1% to $182.3 million compared to the same period in 2024:

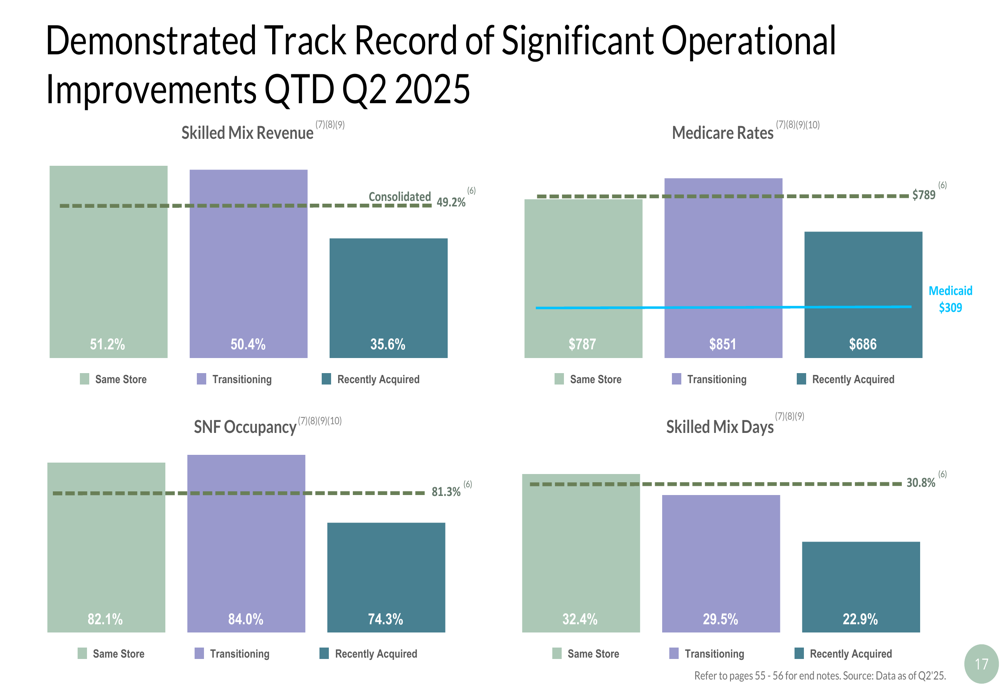

Ensign’s operational improvements across its portfolio are particularly noteworthy. The company categorizes its facilities as Same Store (operated for more than one year), Transitioning (operated between one and three years), and Recently Acquired (operated less than one year). All three categories showed improvements in key metrics including skilled mix revenue, occupancy rates, and skilled mix days:

Growth Strategy and Operational Excellence

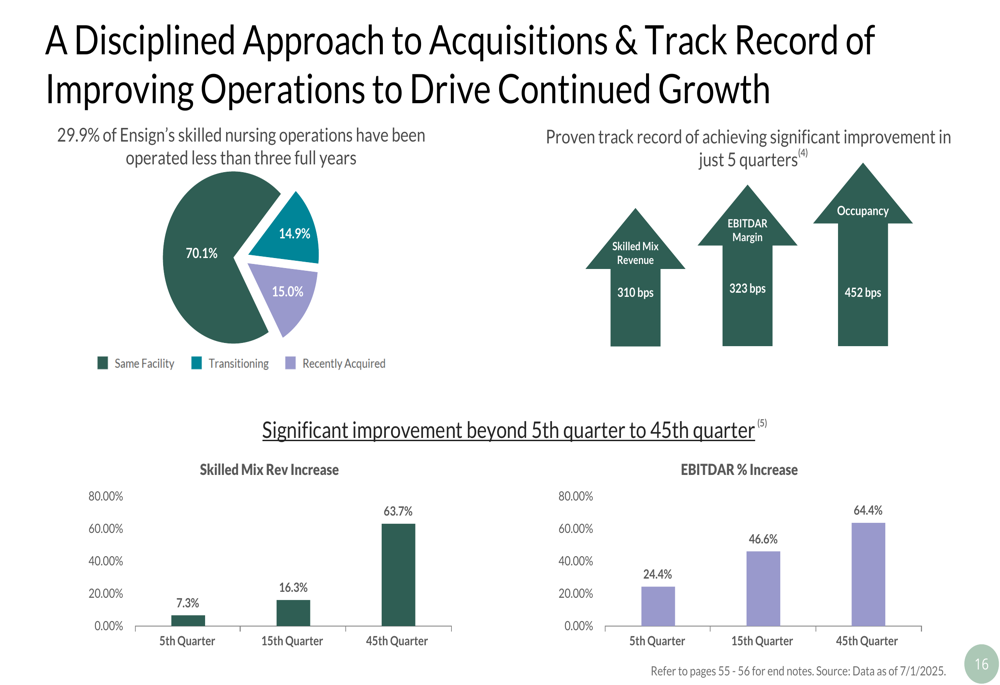

Ensign’s growth strategy combines organic growth, disciplined acquisitions, and development of new ventures. The company has demonstrated a consistent ability to improve operations at acquired facilities, with significant enhancements in skilled mix revenue, EBITDAR margin, and occupancy within just five quarters of acquisition.

As illustrated in the following chart, Ensign has a proven track record of achieving substantial operational improvements in acquired facilities:

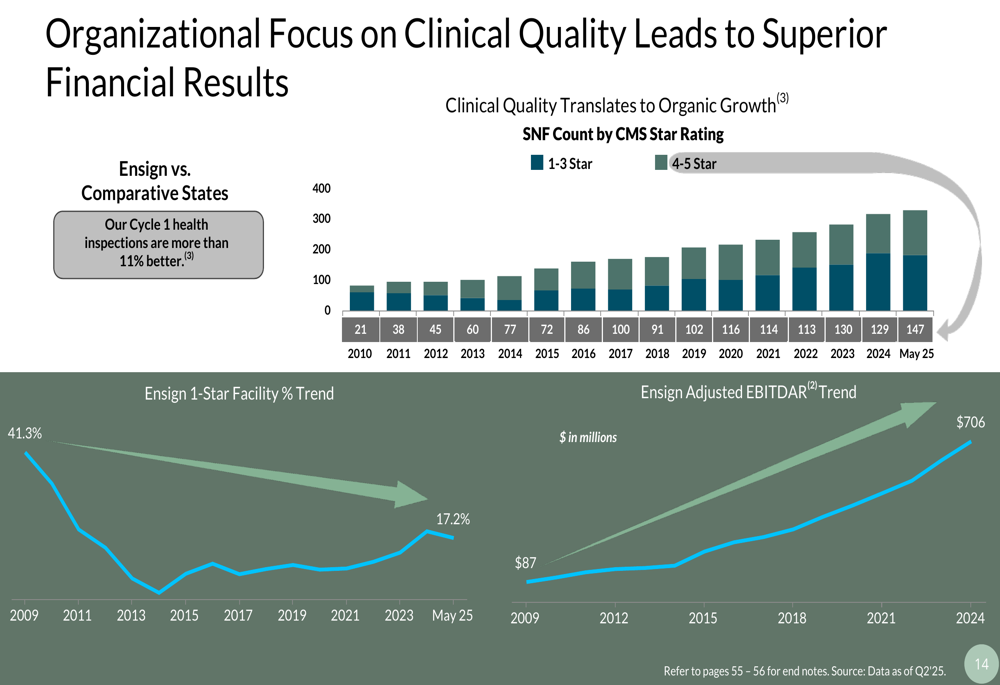

A key differentiator for Ensign is its focus on clinical quality, which translates directly to financial performance. The company’s facilities have consistently improved their CMS star ratings over time, contributing to higher EBITDAR:

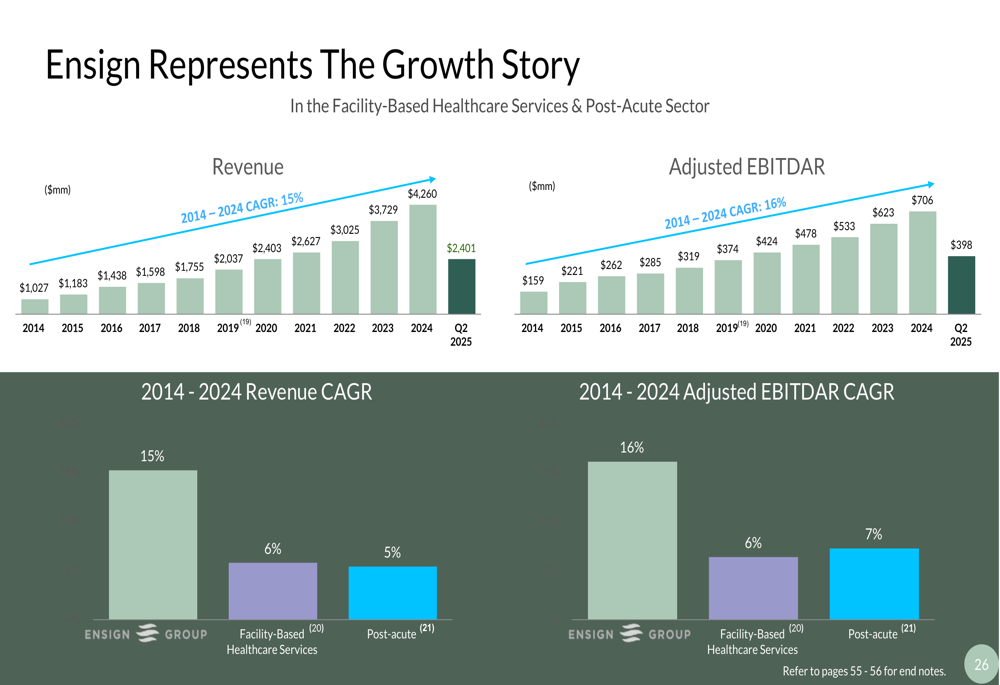

Ensign’s growth has significantly outpaced industry peers over the past decade. From 2014 to 2024, the company achieved a revenue CAGR of 15% and an adjusted EBITDAR CAGR of 16%, compared to 5-6% for the broader post-acute care sector:

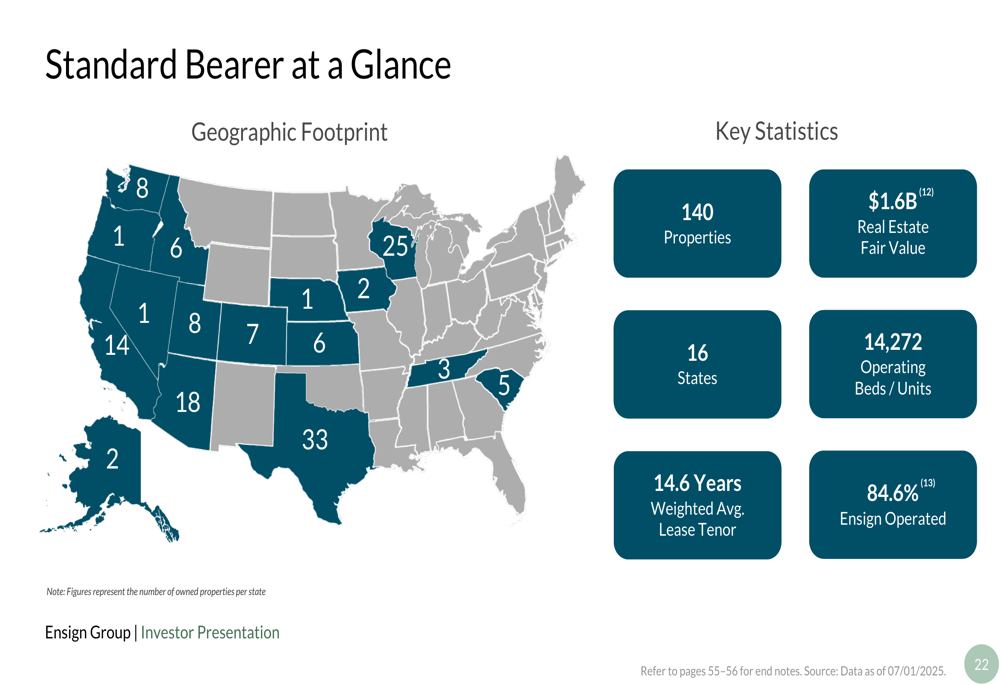

Real Estate Portfolio and Standard Bearer REIT

A significant component of Ensign’s strategy is its real estate portfolio, managed through Standard Bearer, the company’s captive REIT. Standard Bearer owns 146 properties valued at approximately $1.6 billion across 16 states, providing both operational flexibility and value creation opportunities.

The following map and statistics provide an overview of Standard Bearer’s portfolio:

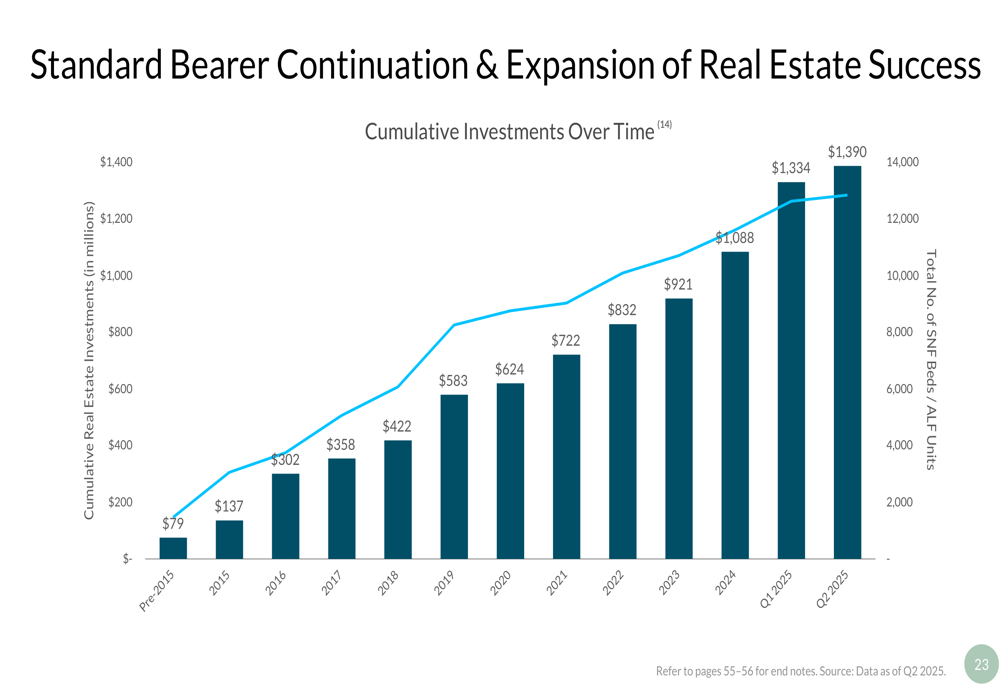

Standard Bearer has demonstrated consistent growth in its real estate investments over time, increasing from pre-2015 levels of $79 million to $1,390 million by Q2 2025:

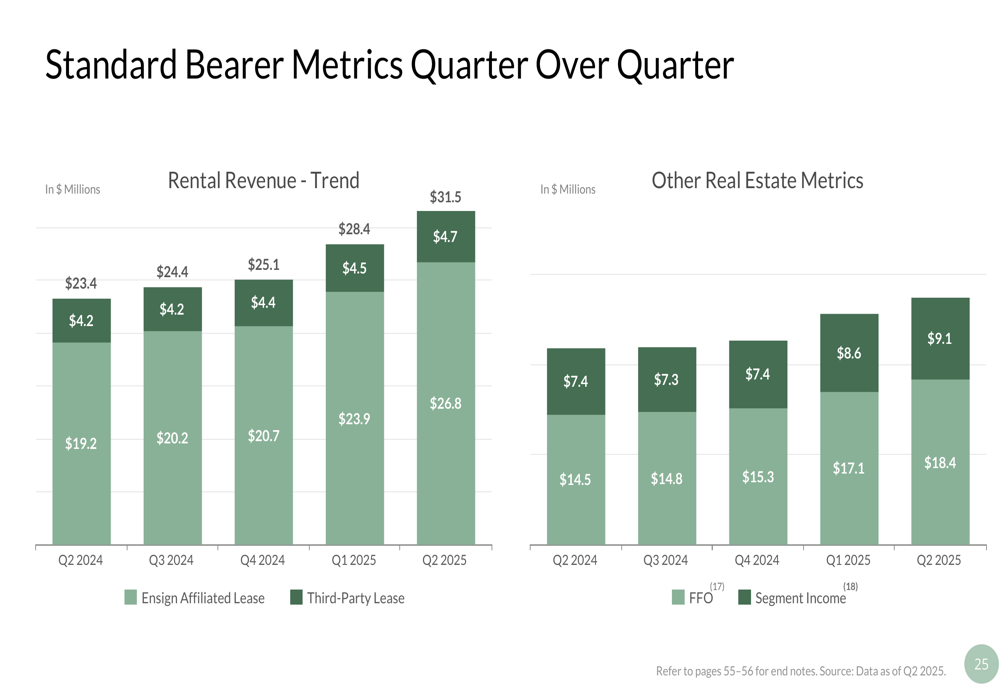

The REIT structure provides several benefits, including increased visibility into embedded real estate value, expanded acquisition opportunities, and capital flexibility. Standard Bearer’s performance metrics have shown steady improvement quarter over quarter:

Forward-Looking Statements and Guidance

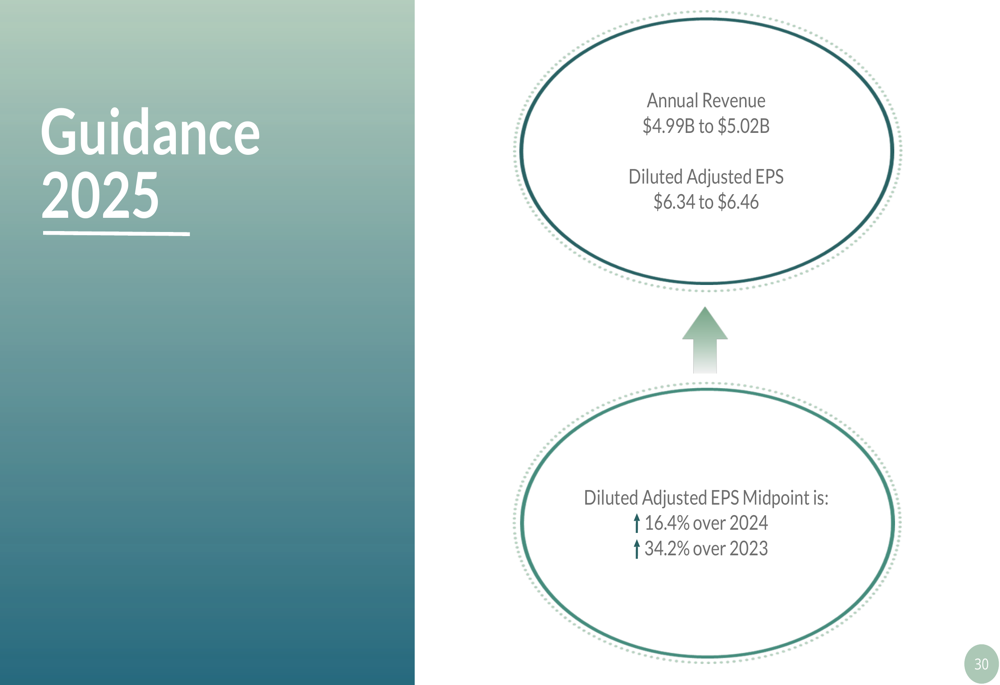

Based on its strong first-half performance, Ensign has raised its full-year 2025 guidance. The company now expects annual revenue between $4.99 billion and $5.02 billion, with diluted adjusted EPS between $6.34 and $6.46. This represents a 16.4% increase over 2024 and a 34.2% increase over 2023 at the midpoint.

The updated guidance is slightly higher than what was provided after Q1 2025 ($6.22-$6.38 EPS), reflecting continued operational improvements and successful integration of recent acquisitions.

Ensign’s long-term value creation is evident in its shareholder returns, which have significantly outperformed the broader market. Since its IPO in 2007, the company has delivered a total shareholder return of 4,111%, with 1,525% over the past decade:

Ensign maintains a strong balance sheet with $364.0 million in cash and cash equivalents as of Q2 2025 and a net debt to adjusted EBITDAR ratio of 1.97x, providing ample capacity for continued acquisitions and investments. The company’s disciplined approach to growth, focus on operational excellence, and strategic real estate investments position it well for continued success in the fragmented post-acute healthcare market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.