Fannie Mae, Freddie Mac shares tumble after conservatorship comments

Enterprise Products Partners L.P. (NYSE:EPD) released its first quarter 2025 earnings presentation on April 29, highlighting operational volume growth across key segments despite experiencing a slight decline in gross operating margin (GOM) compared to both the previous quarter and year-ago period.

Quarterly Performance Highlights

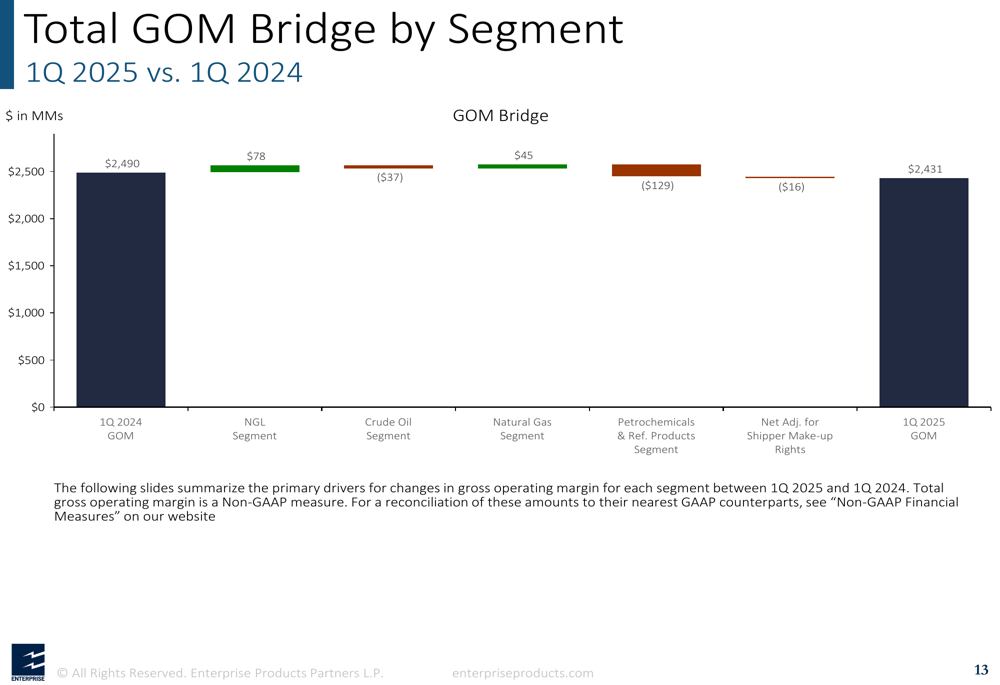

Enterprise reported a total gross operating margin of $2.43 billion for Q1 2025, representing a modest decrease from $2.49 billion in Q1 2024 and a more pronounced decline from $2.63 billion in Q4 2024. Despite this pressure on margins, the company maintained strong operational metrics across its business segments.

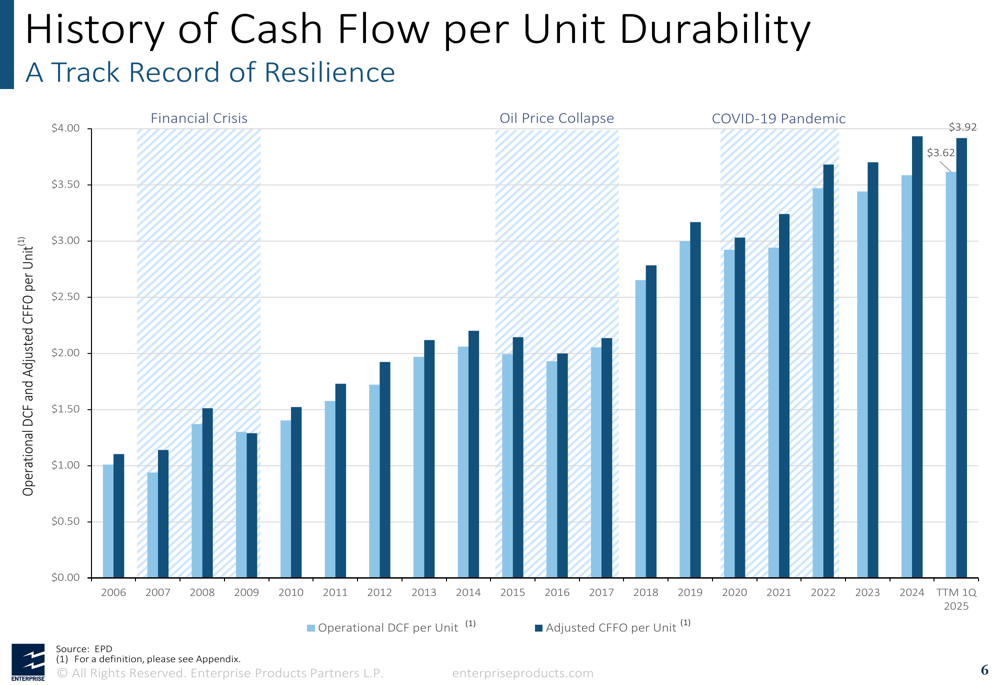

The company’s financial resilience is demonstrated through its consistent cash flow generation. For the trailing twelve months ended Q1 2025, Enterprise reported Operational DCF per unit of $3.62 and Adjusted CFFO per unit of $3.92, continuing its pattern of stable cash flow even during challenging economic periods.

As shown in the following chart of cash flow durability over time:

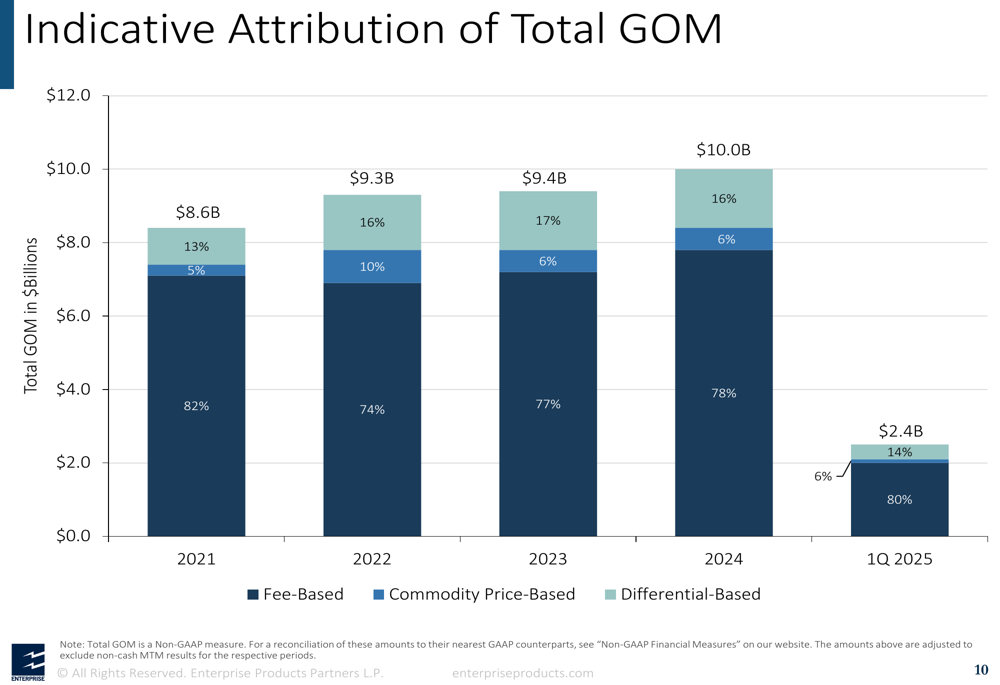

The company’s gross operating margin remains predominantly fee-based, providing stability to its revenue stream. According to the presentation, approximately 80% of Enterprise’s Q1 2025 GOM was fee-based, with 14% differential-based and 6% commodity price-based.

This breakdown of revenue sources is illustrated in the following chart:

Capital Allocation Strategy

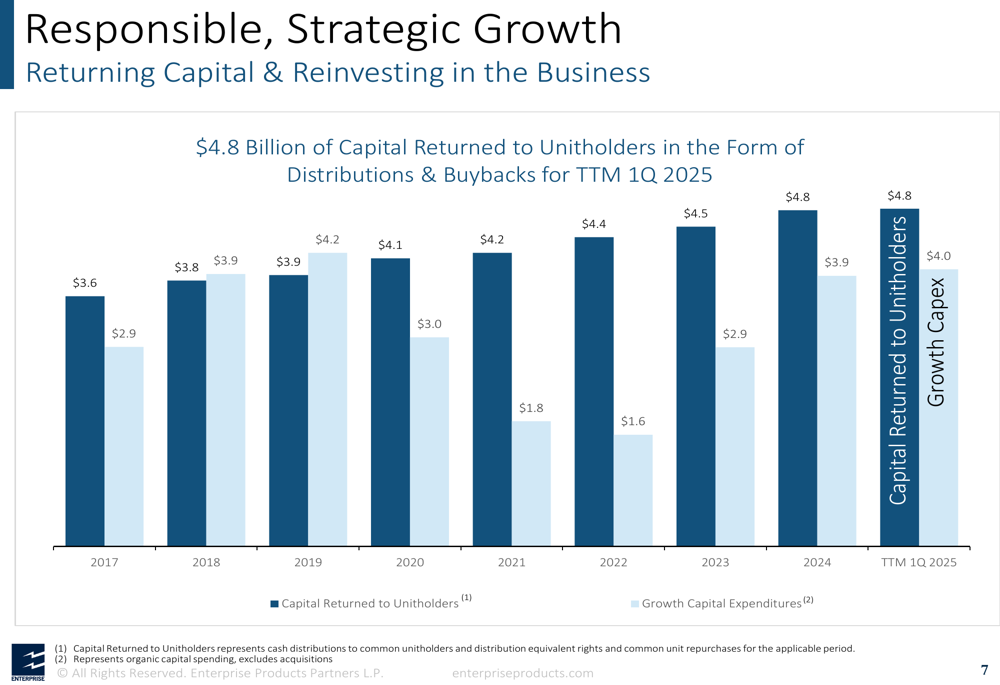

Enterprise continues to emphasize its balanced approach to capital allocation, characterized by the company as an "All of the Above" strategy. The company declared a distribution of $0.535 per unit for Q1 2025, representing a 3.9% increase over Q1 2024, extending its track record to 26 consecutive years of distribution growth.

The company also repurchased $60 million (1.8 million units) during Q1 2025, bringing its trailing twelve-month buyback total to $239 million (8 million units). Enterprise maintained an adjusted CFFO payout ratio of 56% for the trailing twelve months ended Q1 2025.

The following chart illustrates Enterprise’s balanced approach to returning capital to unitholders while funding growth initiatives:

Enterprise continues to maintain a strong balance sheet with a leverage ratio of 3.1x for the trailing twelve months ended Q1 2025, slightly above its target ratio of 3.0x (±0.25x). The company reported $3.6 billion in liquidity as of March 31, 2025, consisting of available credit capacity and unrestricted cash.

This financial strength is supported by the company’s A- credit rating, making it the only midstream energy infrastructure company with this rating. Enterprise’s debt portfolio has an 18-year average maturity, with 96% fixed-rate debt and a weighted-average interest rate of 4.7%.

Operational Growth and Strategic Investments

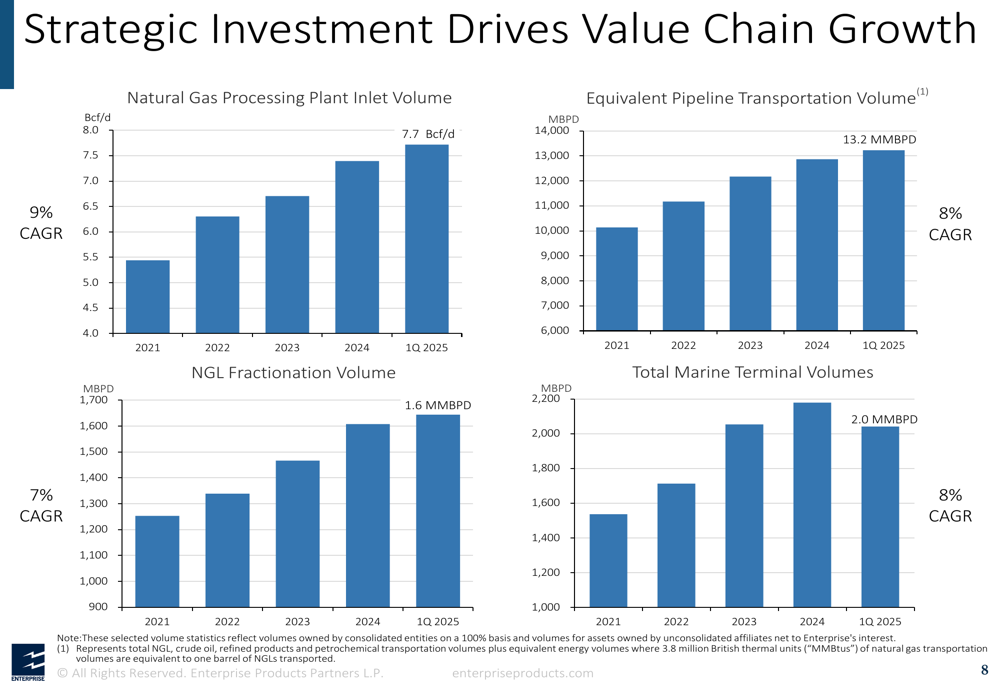

Despite the slight decline in GOM, Enterprise reported impressive volume growth across its operational segments. The company highlighted strong performance metrics including:

- Natural Gas Processing Plant Inlet Volume: 7.7 Bcf/d in Q1 2025 (9% CAGR since 2021)

- Equivalent Pipeline Transportation Volume: 13.2 MMBPD in Q1 2025 (8% CAGR)

- NGL Fractionation Volume: 1.6 MMBPD in Q1 2025 (7% CAGR)

- Total (EPA:TTEF) Marine Terminal Volumes: 2.0 MMBPD in Q1 2025 (8% CAGR)

This consistent operational growth across multiple business lines is illustrated in the following chart:

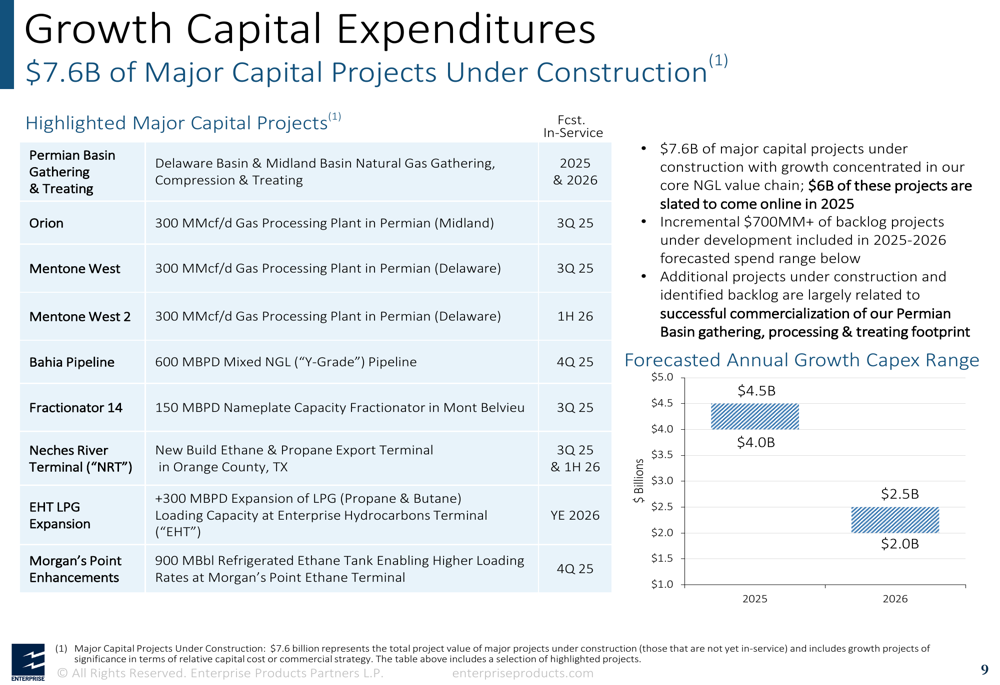

Enterprise continues to invest in growth projects, with $7.6 billion of major capital projects currently under construction. The company’s growth capital expenditure forecast ranges from $4.0 billion to $4.5 billion for 2025, followed by a projected $2.0 billion to $2.5 billion in 2026.

Major projects highlighted in the presentation include Permian Basin Gathering & Treating, Orion, Mentone West, Mentone West 2, Bahia Pipeline, Fractionator 14, Neches River Terminal, EHT LPG Expansion, and Morgan’s Point Enhancements.

The company’s growth capital expenditure forecast is shown in the following chart:

Segment Performance Analysis

The presentation provided detailed breakdowns of segment performance compared to both Q1 2024 and Q4 2024. The NGL segment reported GOM of $1.42 billion in Q1 2025, up from $1.34 billion in Q1 2024 but down from $1.55 billion in Q4 2024. Growth in this segment was driven primarily by Permian Basin Processing Facilities, Permian Basin & Rocky Mountain NGL Pipelines, and the Morgan’s Point Ethane Export Terminal.

The Crude Oil segment saw a decline in GOM to $374 million in Q1 2025 from $411 million in Q1 2024 and $417 million in Q4 2024, primarily due to weaker performance in crude oil assets and marketing activities.

The Natural Gas segment showed improvement with GOM of $357 million in Q1 2025, up from $312 million in Q1 2024 and $323 million in Q4 2024. This growth was driven by strong performance in Permian Basin Gathering Systems, the Texas Intrastate System, and natural gas marketing activities.

The Petrochemical & Refined Products segment experienced the most significant decline, with GOM falling to $315 million in Q1 2025 from $444 million in Q1 2024 and $348 million in Q4 2024. This decrease was primarily attributed to weaker performance in octane enhancement operations, propylene production, and ethylene exports.

The year-over-year changes in segment GOM are illustrated in the following bridge chart:

Forward Outlook

Enterprise positioned itself as a resilient portfolio component, highlighting several key strengths including:

- Recession resistance due to inelastic demand for its infrastructure services

- Inflation protection with approximately 90% of long-term contracts having escalation provisions

- Conservative long-term financing with an A- credit rating

- Stable cash flow yields and consistent distribution growth

The company’s capital expenditure forecast suggests continued investment in growth opportunities, particularly in 2025, with a more moderate pace of investment projected for 2026. This aligns with Enterprise’s previous guidance from Q3 2024, though the current forecast for 2025 capex ($4.0-4.5 billion) is slightly higher than the $3.5-4.0 billion range mentioned in the previous earnings call.

Enterprise’s presentation emphasized its strategic positioning across the energy value chain and its ability to generate stable, fee-based revenues while continuing to invest in growth opportunities and return capital to unitholders. While facing some margin pressure in Q1 2025, the company’s operational volume growth and disciplined capital allocation approach suggest continued resilience in its business model.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.