Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

Envista Holdings Corp (NYSE:NVST) presented its first quarter 2025 results on May 1, showing modest growth in a challenging environment. The dental products company reported performance largely in line with internal expectations, despite facing headwinds from foreign exchange rates and geopolitical uncertainties.

The company described the dental market as "soft but stable," similar to conditions experienced in the second half of 2024. Following the earnings release, Envista’s stock rose by 1.59% in regular trading, closing at $16.34, suggesting investors were satisfied with the results that exceeded analyst expectations.

Quarterly Performance Highlights

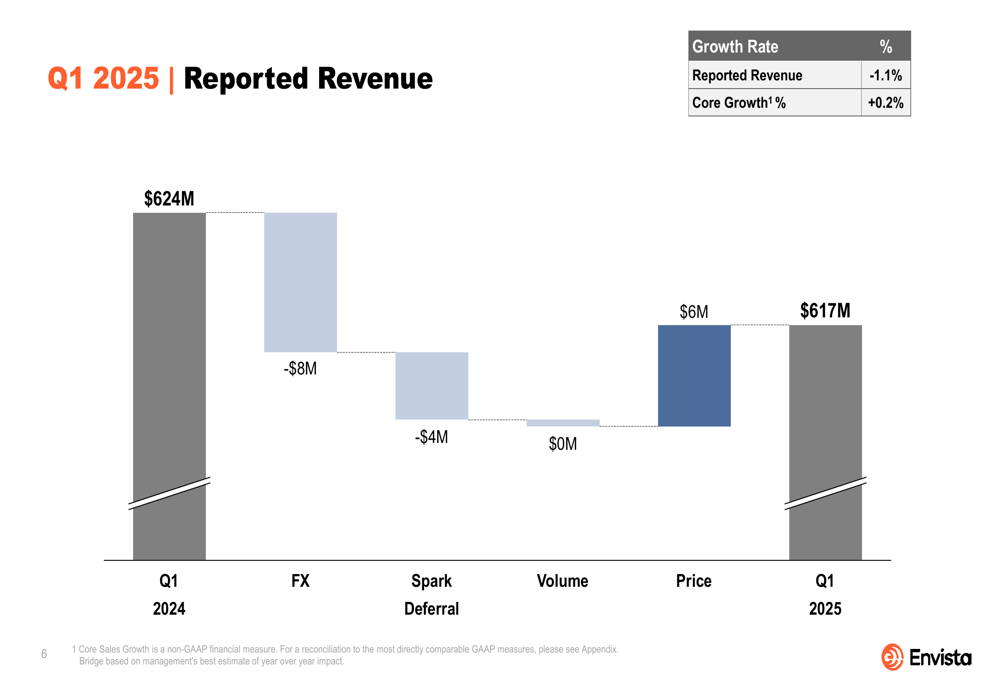

Envista reported Q1 2025 revenue of $616.9 million, representing a 0.2% core growth compared to the same period last year. While reported revenue declined by 1.1%, this was primarily due to negative foreign exchange impacts of $8 million and a $4 million impact from Spark revenue deferrals.

As shown in the following revenue bridge chart:

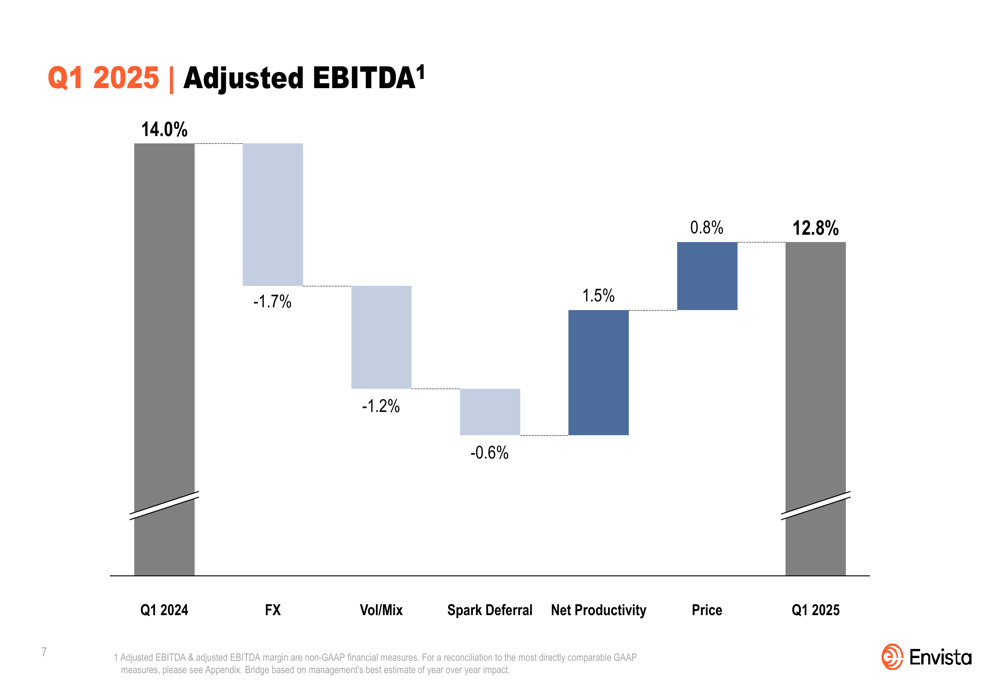

The company’s adjusted EBITDA margin was 12.8%, down from 14.0% in Q1 2024. This decline was attributed to several factors, including a 1.7% negative impact from foreign exchange, 1.2% from volume/mix challenges, and 0.6% from Spark deferrals. These headwinds were partially offset by 1.5% positive impact from productivity improvements and 0.8% from price increases.

The EBITDA margin bridge illustrates these factors:

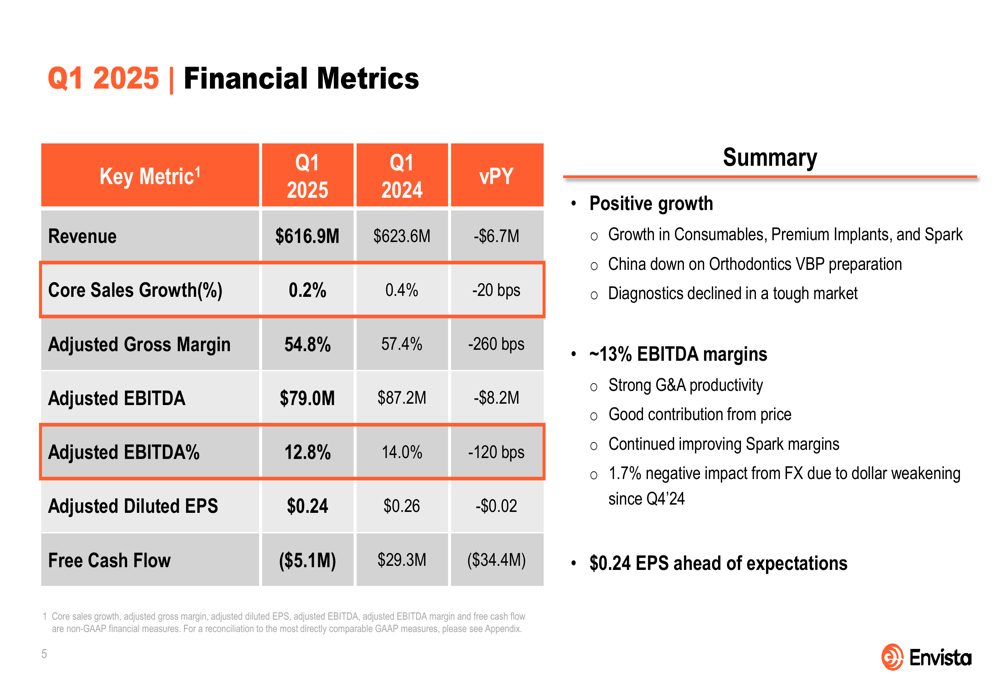

Adjusted earnings per share came in at $0.24, down slightly from $0.26 in the prior year period but exceeding analyst expectations of $0.21. Free cash flow was negative $5.1 million, compared to positive $29.3 million in Q1 2024.

The comprehensive financial metrics summary provides a clear picture of Envista’s performance:

Segment Performance

Envista’s business is divided into two main segments, each showing different performance trends in the quarter.

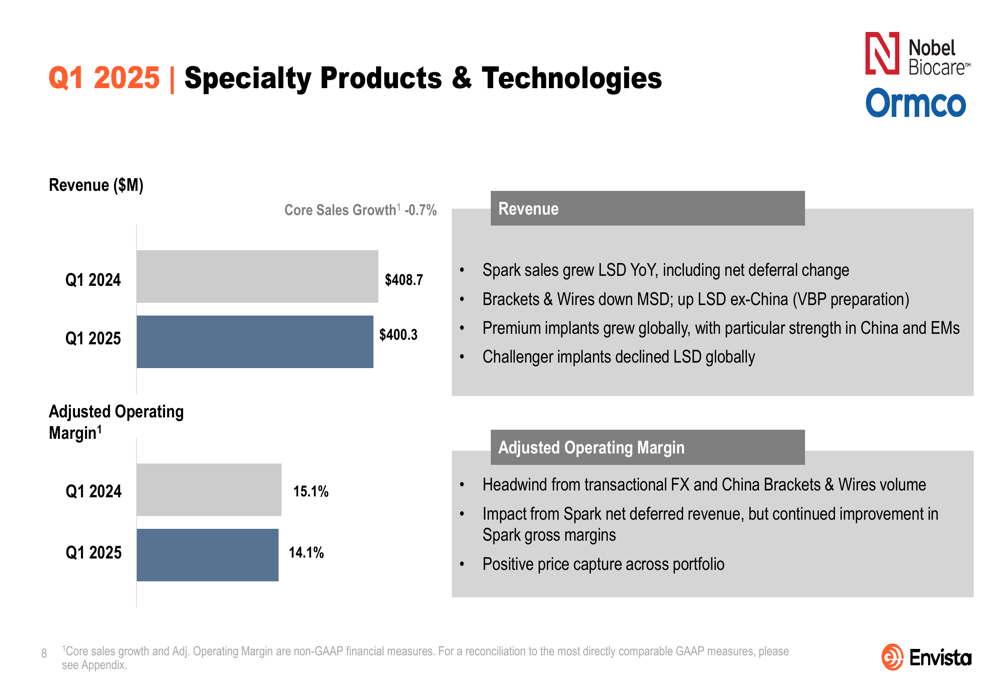

The Specialty Products & Technologies segment, which includes orthodontics and implants, reported revenue of $400.3 million, representing a core sales decline of 0.7%. Adjusted operating margin for this segment was 14.1%, down from 15.1% in the prior year. While Spark clear aligners showed low-single-digit growth and premium implants grew globally, these gains were offset by weakness in brackets and wires, particularly in China.

The segment’s performance metrics are detailed here:

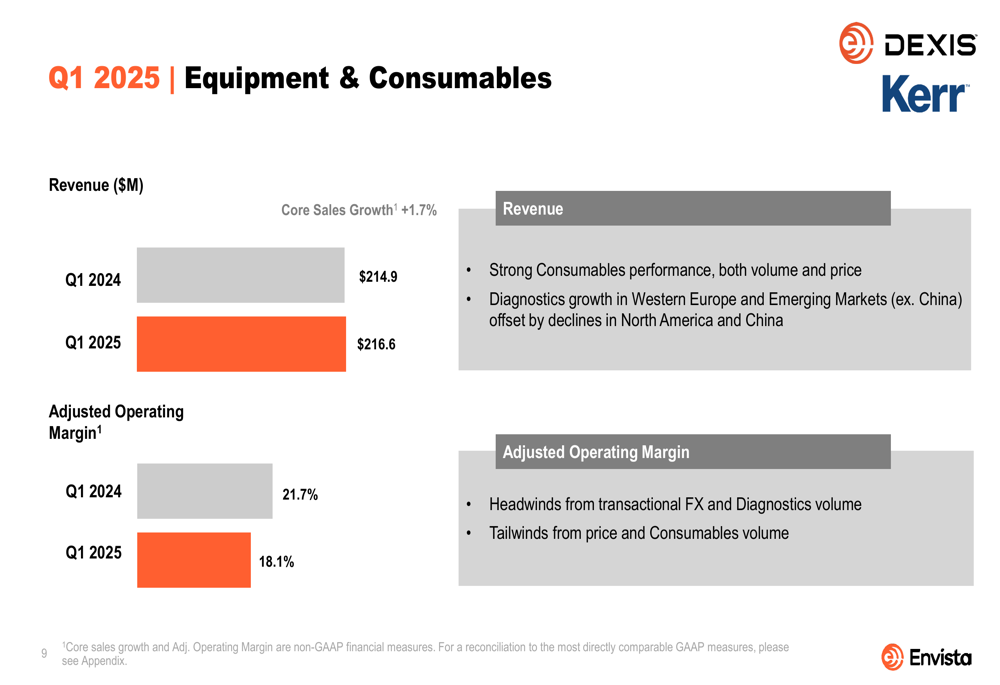

Meanwhile, the Equipment & Consumables segment performed better, with revenue of $216.6 million and core sales growth of 1.7%. However, adjusted operating margin declined from 21.7% to 18.1% year-over-year. Strong consumables performance was partially offset by diagnostics volume challenges.

The Equipment & Consumables segment results are illustrated below:

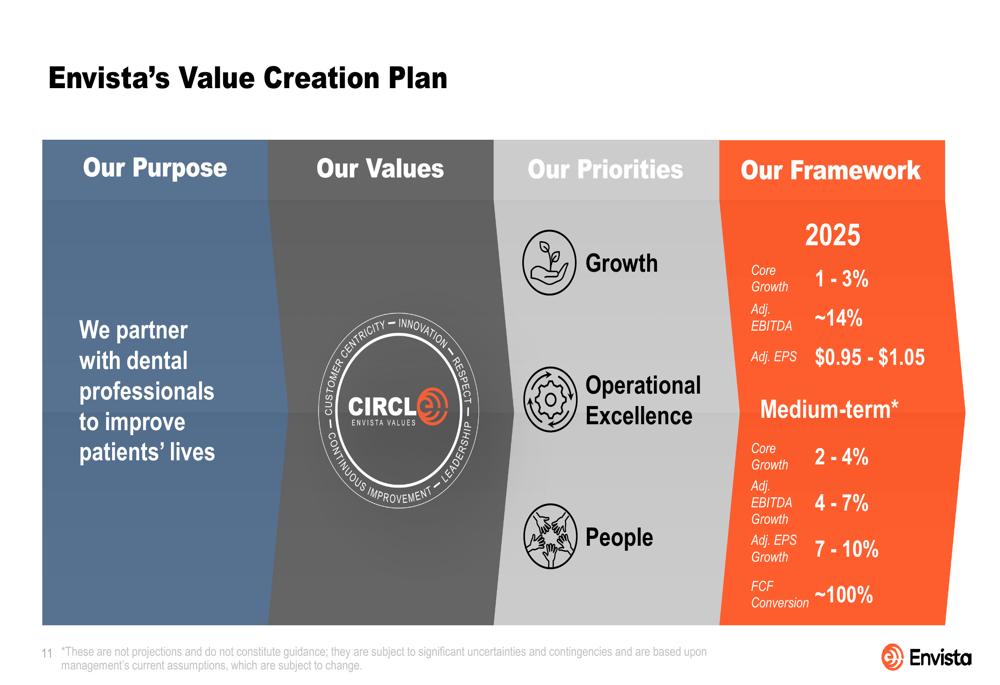

Strategic Initiatives and Value Creation Plan

Envista continues to execute on its value creation plan, which focuses on three key priorities: growth, operational excellence, and people. The company’s framework includes 2025 targets of 1-3% core growth, approximately 14% adjusted EBITDA margin, and $0.95-$1.05 adjusted EPS.

The comprehensive value creation plan is outlined here:

In Q1, the company highlighted several achievements aligned with these priorities, including growth in consumables, premium implants, and orthodontics (excluding China); training of over 15,000 clinicians; maintaining high customer service levels with approximately 95% on-time delivery; and continued sequential improvement in Spark gross margins.

The company also reported executing on its share repurchase plan, buying back over 1 million shares during the quarter. Envista maintains a strong balance sheet with a net debt to adjusted EBITDA ratio of approximately 1x, providing financial flexibility in an uncertain environment.

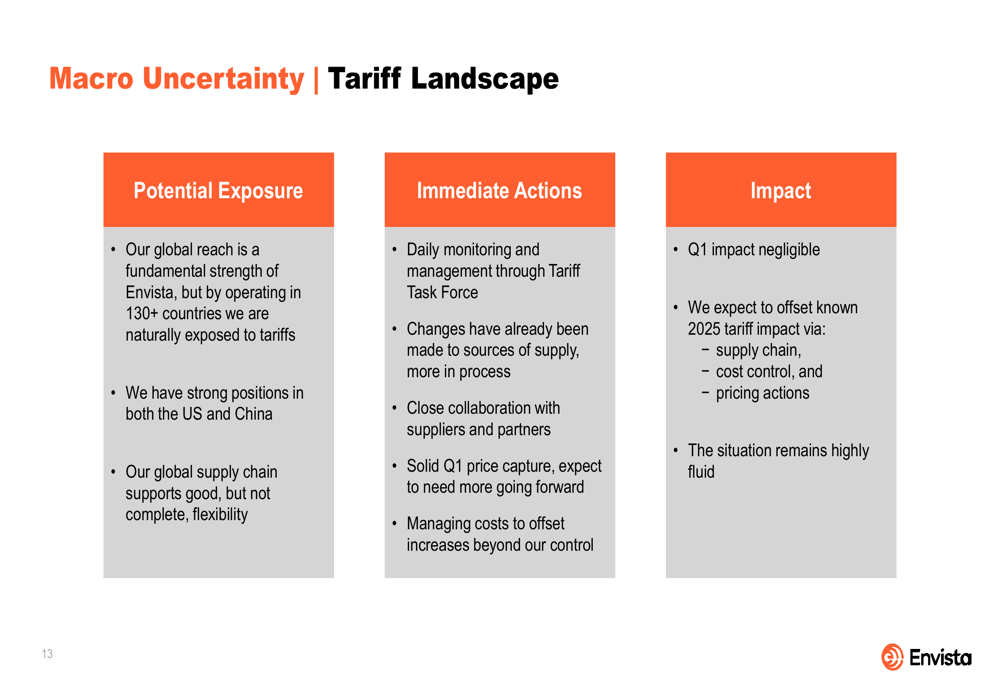

Tariff Concerns and Mitigation Strategies

A significant focus of Envista’s presentation was the increasing macro uncertainty, particularly related to tariffs. As a company with global operations and strong positions in both the US and China, Envista faces potential exposure to tariff impacts.

The company has established a Tariff Task Force to monitor and manage the situation daily. Management noted that while Q1 tariff impact was negligible, they are implementing several mitigation strategies, including changes to supply sources, collaboration with suppliers and partners, and pricing actions.

The tariff landscape and mitigation strategies are detailed here:

CEO Paul Keel emphasized the resilience of the dental market, stating, "While macro uncertainty is certainly elevated, dental has historically been more resilient than the broader economy." He also expressed confidence in the company’s ability to offset tariff impacts through various mitigating actions.

Forward-Looking Statements

Despite the challenging environment, Envista maintained its full-year 2025 guidance, projecting:

- Core growth of 1-3%

- Adjusted EBITDA margin of approximately 14%

- Adjusted EPS of $0.95-$1.05

Management expressed confidence in offsetting known 2025 tariff impacts through supply chain adjustments, cost control measures, and pricing actions. However, they acknowledged that the situation remains highly fluid, with geopolitical tensions potentially impacting consumer confidence and macroeconomic forecasts.

Looking beyond 2025, Envista’s medium-term targets include 2-4% core growth, 4-7% adjusted EBITDA growth, 7-10% adjusted EPS growth, and approximately 100% free cash flow conversion.

The company’s ability to navigate current challenges while maintaining its guidance suggests management confidence in the underlying business fundamentals and the effectiveness of its mitigation strategies. However, investors should continue to monitor the evolving tariff situation and its potential impact on Envista’s global operations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.