CCH Holdings prices IPO at $4 per share on NASDAQ

Introduction & Market Context

EQB Inc. (TSX:EQB) released its third-quarter 2025 results on August 28, revealing significant challenges despite continued growth in key business segments. The company’s stock dropped nearly 13% following the announcement, as investors reacted to an earnings miss and deteriorating credit metrics.

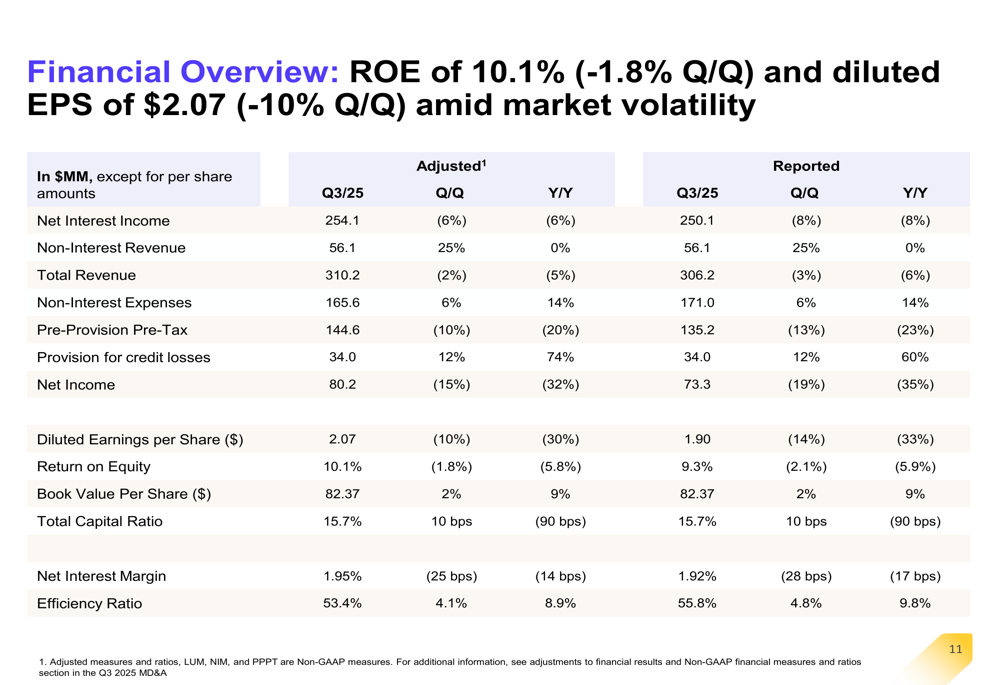

According to the presentation, EQB reported adjusted diluted earnings per share of $2.07, representing a 10% decline quarter-over-quarter and a 30% drop year-over-year. This fell well short of market expectations of $2.63, contributing to the stock’s sharp decline to $88.47, approaching its 52-week low of $85.14.

Quarterly Performance Highlights

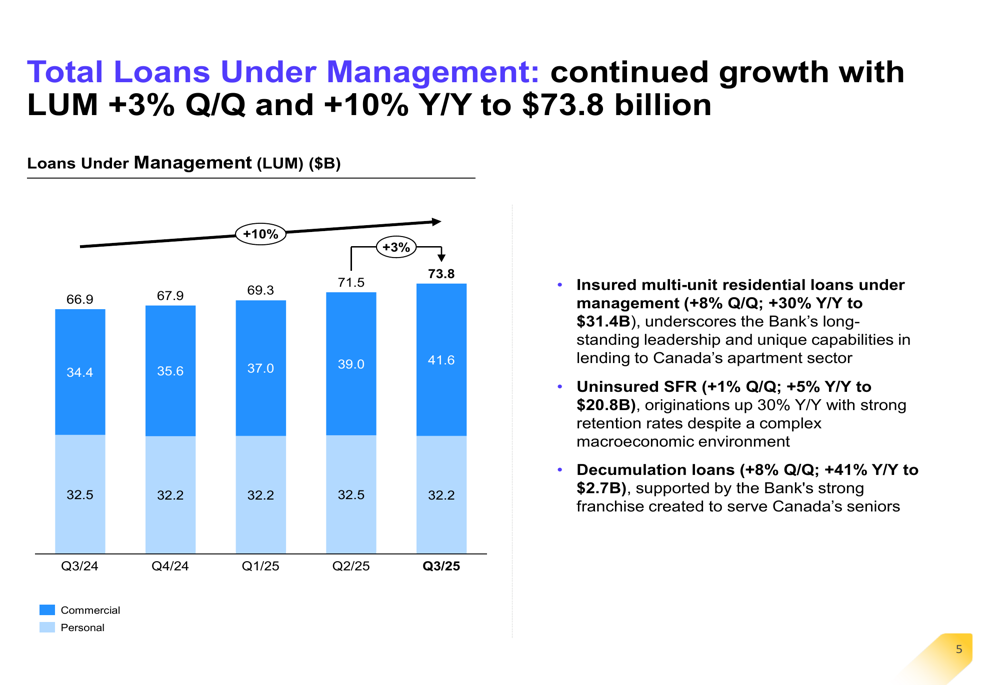

EQB’s financial performance showed mixed results, with growth in loans and deposits offset by margin compression and higher credit provisions. The company’s total loans under management reached $73.8 billion, increasing 3% quarter-over-quarter and 10% year-over-year, driven primarily by personal banking growth.

As shown in the following comprehensive financial overview, EQB’s adjusted net income fell to $80.2 million, down 15% quarter-over-quarter and 32% year-over-year:

The company’s return on equity declined to 10.1%, a decrease of 1.8 percentage points from the previous quarter and 5.8 percentage points year-over-year. This performance falls short of the company’s adjusted full-year ROE guidance of 11.5%.

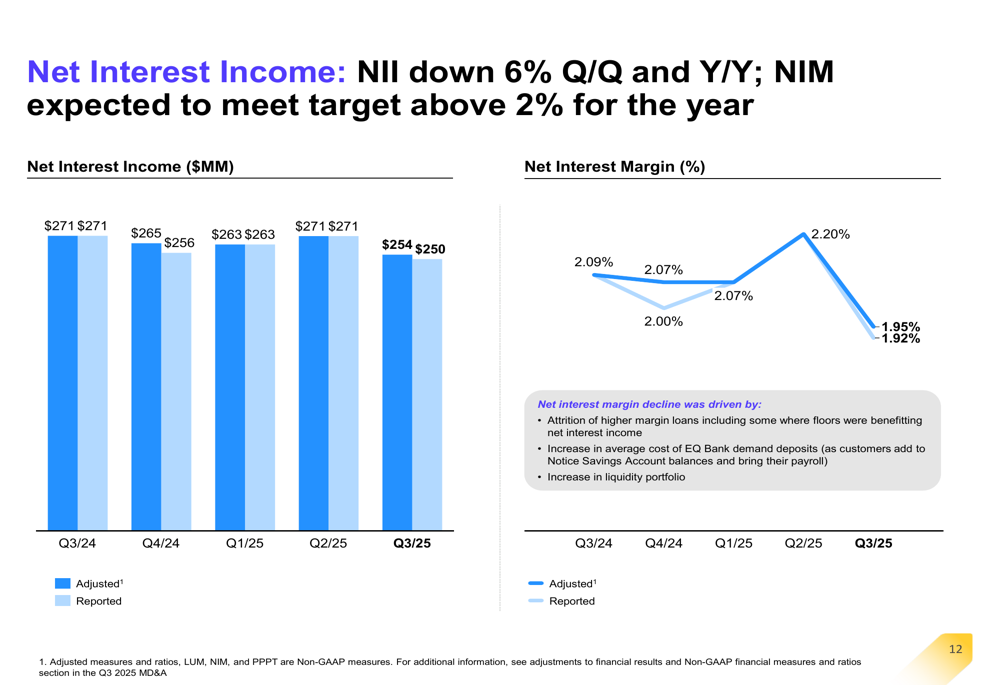

A key factor in the earnings decline was pressure on net interest income, which fell 6% both quarter-over-quarter and year-over-year to $254.1 million. More concerning was the sharp drop in net interest margin to 1.95%, down 25 basis points sequentially:

Management attributed the margin decline to attrition of higher-margin loans, increased cost of EQ Bank demand deposits, and growth in the lower-yielding liquidity portfolio.

Loan Portfolio and Credit Quality

EQB’s loan portfolio continued to grow, with personal banking showing stronger momentum than commercial banking. The following chart illustrates the consistent growth in total loans under management:

Personal loans grew to $41.6 billion, up from $39.0 billion in the previous quarter, while commercial loans remained relatively flat at $32.2 billion. Within personal banking, decumulation loans showed particularly strong growth, increasing 41% year-over-year to $2.7 billion.

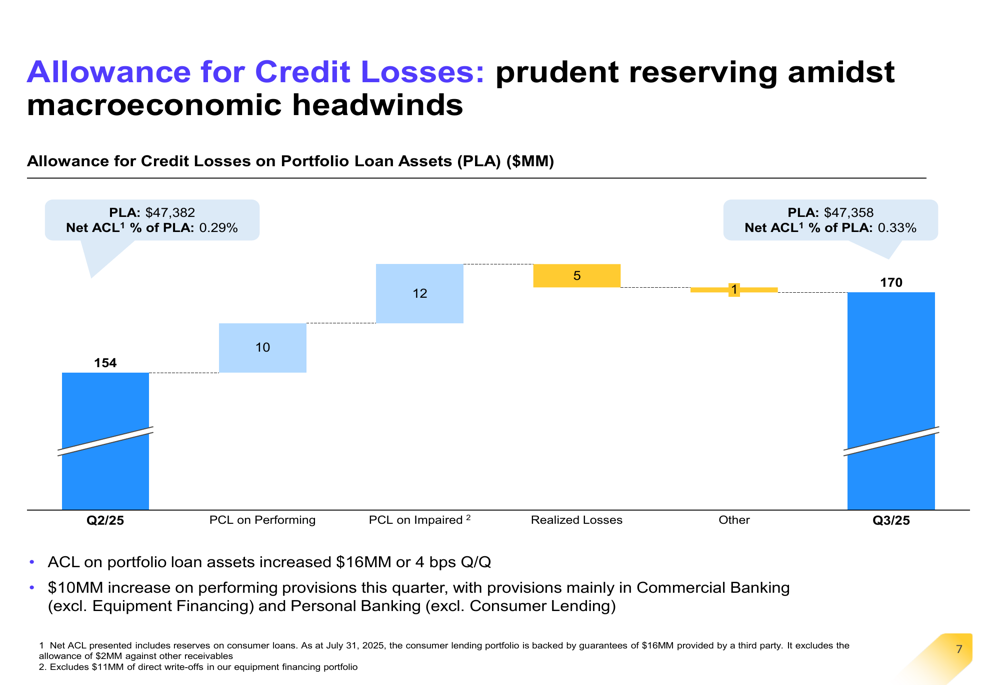

However, credit quality metrics showed signs of deterioration. The allowance for credit losses increased by $16 million quarter-over-quarter:

Provisions for credit losses rose 12% quarter-over-quarter and 74% year-over-year to $34.0 million, with increases in both performing and impaired loan provisions. This trend suggests growing caution about the loan portfolio’s future performance amid challenging economic conditions.

Digital Banking Growth

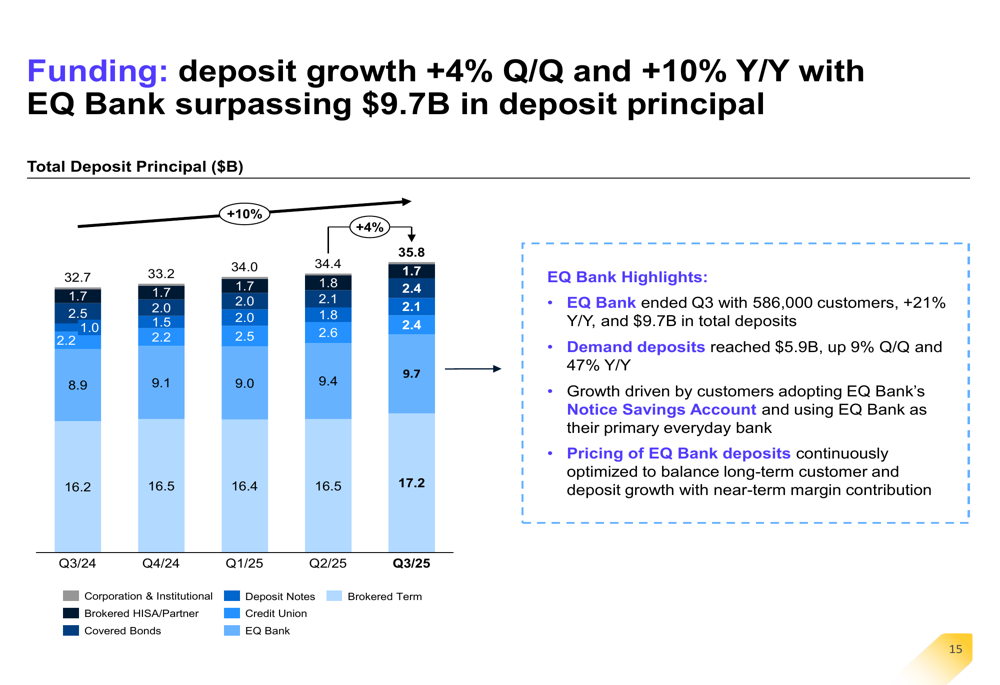

Despite profitability challenges, EQB’s digital banking platform continued to show strong growth. EQ Bank ended the quarter with 586,000 customers, representing 21% year-over-year growth, and total deposits of $9.7 billion.

The following chart shows the company’s overall deposit growth, which increased 4% quarter-over-quarter and 10% year-over-year to $35.8 billion:

Particularly noteworthy was the 47% year-over-year growth in demand deposits, which reached $5.9 billion. Management attributed this growth to customers adopting EQ Bank’s Notice Savings Account and increasingly using EQ Bank as their primary everyday bank.

Capital Position and Shareholder Returns

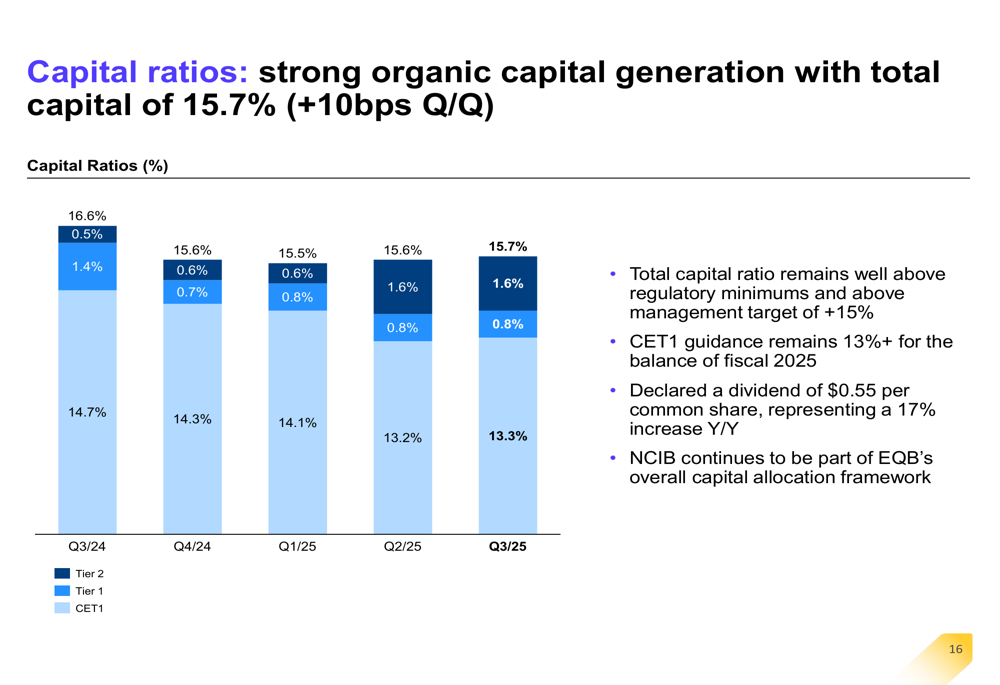

EQB maintained strong capital ratios despite the challenging quarter. The company’s total capital ratio stood at 15.7%, up 10 basis points from the previous quarter but down 90 basis points year-over-year:

The Common Equity Tier 1 (CET1) ratio was 13.3%, slightly up from 13.2% in the previous quarter but down from 14.7% a year ago. Management reaffirmed its guidance to maintain CET1 above 13% for the remainder of fiscal 2025.

EQB declared a quarterly dividend of $0.55 per common share, maintaining its 22-year streak of consistent dividend payments despite current challenges. The company also indicated that its Normal Course Issuer Bid (NCIB) remains part of its capital allocation framework.

Forward-Looking Statements

Looking ahead, EQB faces continued challenges in the near term. Management expects fourth-quarter performance to mirror the third quarter, suggesting ongoing pressure on profitability metrics.

The company’s strategic priorities focus on three key areas: achieving scale as a challenger bank, reaching full growth potential, and enhancing capabilities and purpose. Under the leadership of new President and CEO Chadwick Westlake, EQB is emphasizing innovation and digital banking while maintaining its focus on the Canadian market.

During the earnings call, Westlake emphasized the company’s commitment to innovation, stating, "We are dedicated to helping build a better country, bringing real change to banking." He also reiterated EQB’s focus on the Canadian market, saying, "Our focus is and will remain here in Canada, where there is still so much to do."

However, the company faces significant headwinds, including macroeconomic uncertainty, potential interest rate changes, housing market weakness, and elevated unemployment, all of which could impact future performance. The decline in net interest margin highlights ongoing challenges in managing loan and deposit dynamics in the current environment.

Despite these challenges, EQB’s continued growth in customers and deposits, particularly in its digital banking platform, provides a foundation for potential recovery as economic conditions improve and credit concerns stabilize.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.