Street Calls of the Week

Introduction & Market Context

EQT Corporation (NYSE:EQT), the largest natural gas producer in the United States, presented its second quarter 2025 results on July 22, 2025, highlighting strong operational performance and continued progress on its strategic initiatives. The company reported robust free cash flow generation despite a securities class action settlement expense, while making significant strides in debt reduction and efficiency improvements.

EQT (ST:EQTAB) shares closed at $53.54 on the day of the presentation, up 1.59% for the session, reflecting positive investor sentiment. The company’s stock has traded between $30.02 and $61.02 over the past 52 weeks, indicating some volatility in line with natural gas price fluctuations.

Quarterly Performance Highlights

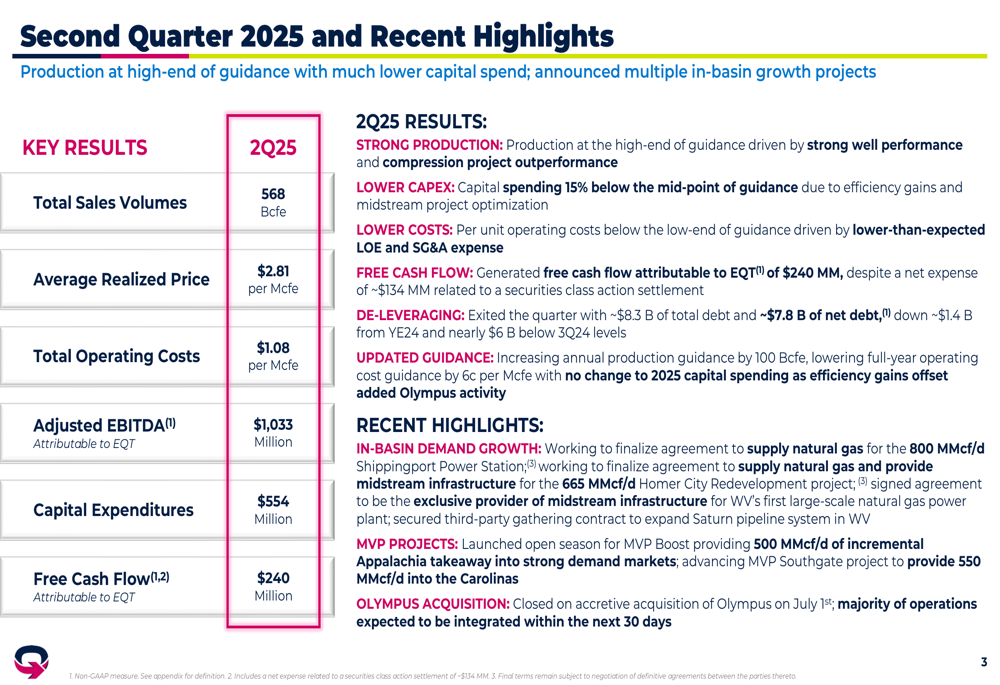

EQT delivered strong second quarter results, with production volumes reaching 568 Bcfe, at the high end of guidance. The company generated $240 million in free cash flow attributable to EQT despite absorbing a net expense of approximately $134 million related to a securities class action settlement. Average realized price for the quarter was $2.81 per Mcfe, while total operating costs came in at $1.08 per Mcfe, below the low end of guidance.

As shown in the following comprehensive overview of Q2 2025 results:

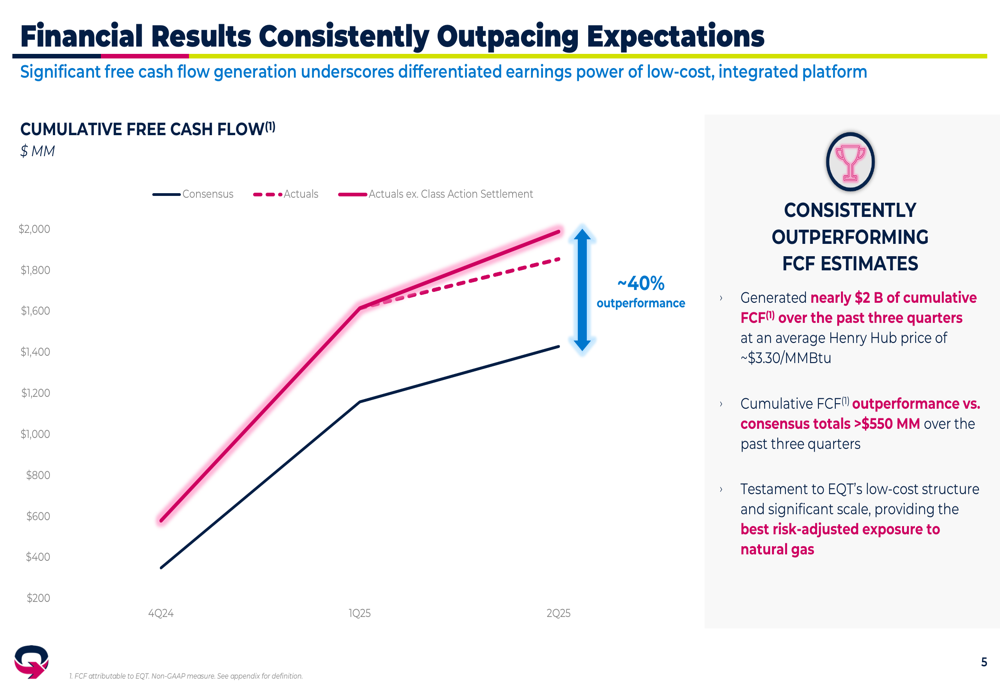

The company’s financial performance has consistently exceeded expectations over recent quarters. EQT has generated nearly $2 billion in cumulative free cash flow over the past three quarters at an average Henry Hub price of approximately $3.30/MMBtu, outperforming consensus estimates by more than $550 million during this period.

The following chart illustrates how EQT’s actual free cash flow generation has consistently outpaced consensus expectations:

Capital expenditures for the quarter totaled $554 million, approximately 15% below the mid-point of guidance, driven by efficiency gains and midstream project optimization. This capital discipline, combined with strong production and lower operating costs, contributed to the company’s robust free cash flow generation.

Operational Efficiency Improvements

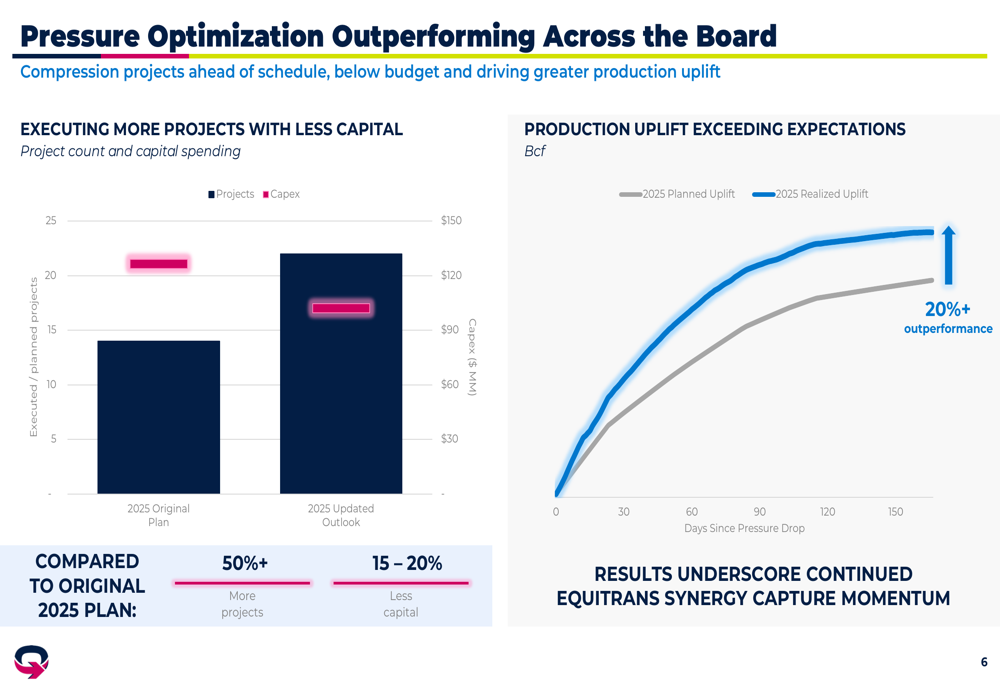

EQT continues to make significant strides in operational efficiency, which has been a key driver of its financial outperformance. The company’s pressure optimization initiatives have exceeded expectations, with 50% more projects being executed with 15-20% less capital compared to the original 2025 plan.

The following chart demonstrates how EQT is executing more pressure optimization projects with less capital while achieving greater production uplift:

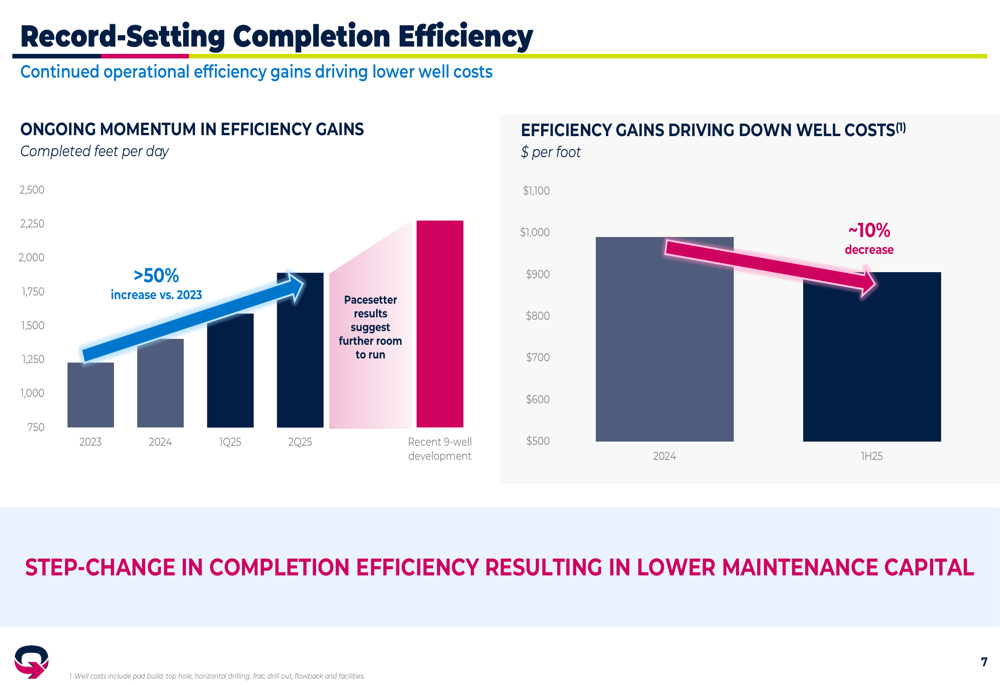

Completion efficiency has also shown remarkable improvement, increasing by more than 50% compared to 2023 levels. This efficiency gain has translated into approximately 10% lower well costs compared to 2024, contributing to EQT’s lower capital spending and improved free cash flow generation.

As illustrated in this chart showing record-setting completion efficiency:

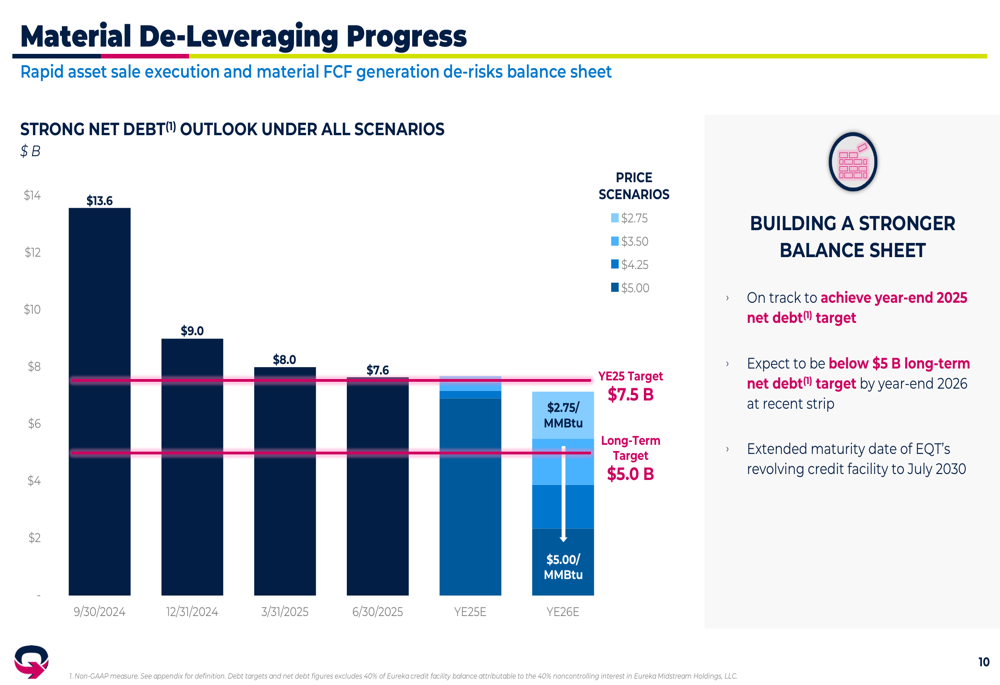

Balance Sheet Improvements

EQT has made substantial progress in strengthening its balance sheet through debt reduction. The company exited the second quarter with approximately $8.3 billion of total debt and $7.8 billion of net debt, representing a reduction of about $1.4 billion from year-end 2024 and nearly $6 billion below third quarter 2024 levels.

The following chart shows EQT’s material de-leveraging progress and future targets:

The company is on track to achieve its year-end 2025 net debt target of $7.5 billion and expects to be below its long-term net debt target of $5 billion by year-end 2026 at recent strip pricing. This rapid de-leveraging enhances EQT’s financial flexibility and supports its investment grade credit profile.

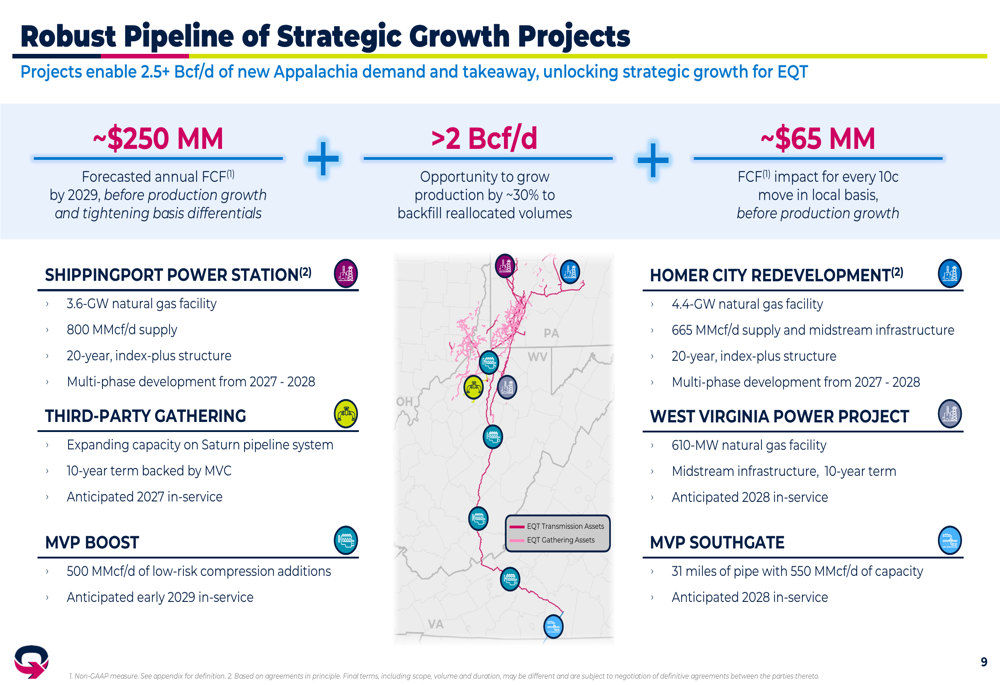

Strategic Growth Initiatives

EQT is pursuing several strategic growth initiatives to capitalize on increasing natural gas demand, particularly from power generation and data centers. The company is working to finalize agreements to supply natural gas for the 800 MMcf/d Shippingport Power Station and the 665 MMcf/d Homer City Redevelopment project, both scheduled for multi-phase development from 2027-2028.

Additionally, EQT has launched an open season for MVP Boost, which will provide 500 MMcf/d of incremental Appalachia takeaway capacity into strong demand markets. The company is also advancing the MVP Southgate project to provide 550 MMcf/d into the Carolinas.

The following slide illustrates EQT’s robust pipeline of strategic growth projects:

These projects are expected to enable 2.5+ Bcf/d of new Appalachia demand and takeaway, unlocking strategic growth opportunities for EQT. The company forecasts these initiatives will generate approximately $250 million in annual free cash flow by 2029, before accounting for production growth and tightening basis differentials.

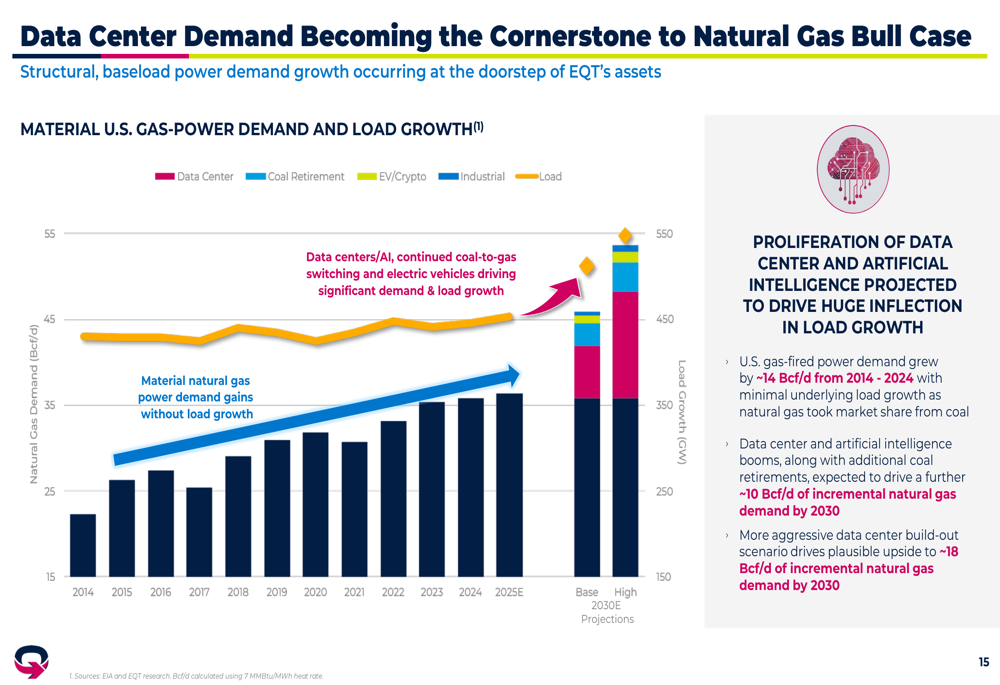

Natural Gas Market Outlook

EQT’s presentation highlighted several factors that support a positive outlook for natural gas demand and pricing. Data center growth is emerging as a significant driver of natural gas demand, with approximately 55 gigawatts of data centers under development in EQT’s core operating area. The company estimates that 1 gigawatt of data center capacity translates to approximately 0.15 Bcf/d of natural gas demand.

As shown in this chart illustrating how data center demand is becoming fundamental to the natural gas bull case:

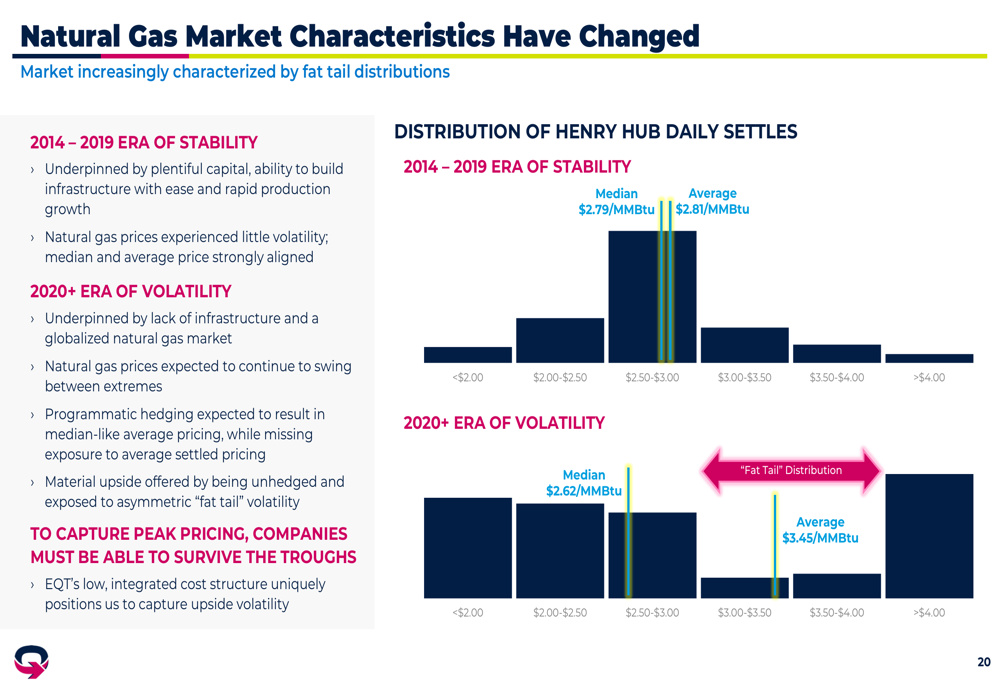

The natural gas market is also evolving toward greater price volatility, characterized by "fat tail" distributions that create both challenges and opportunities. EQT’s low breakeven costs and unhedged upside exposure position the company to navigate market troughs while capturing peak pricing opportunities.

The following chart illustrates how natural gas market characteristics have changed from an era of stability (2014-2019) to an era of volatility (2020+):

ESG Leadership

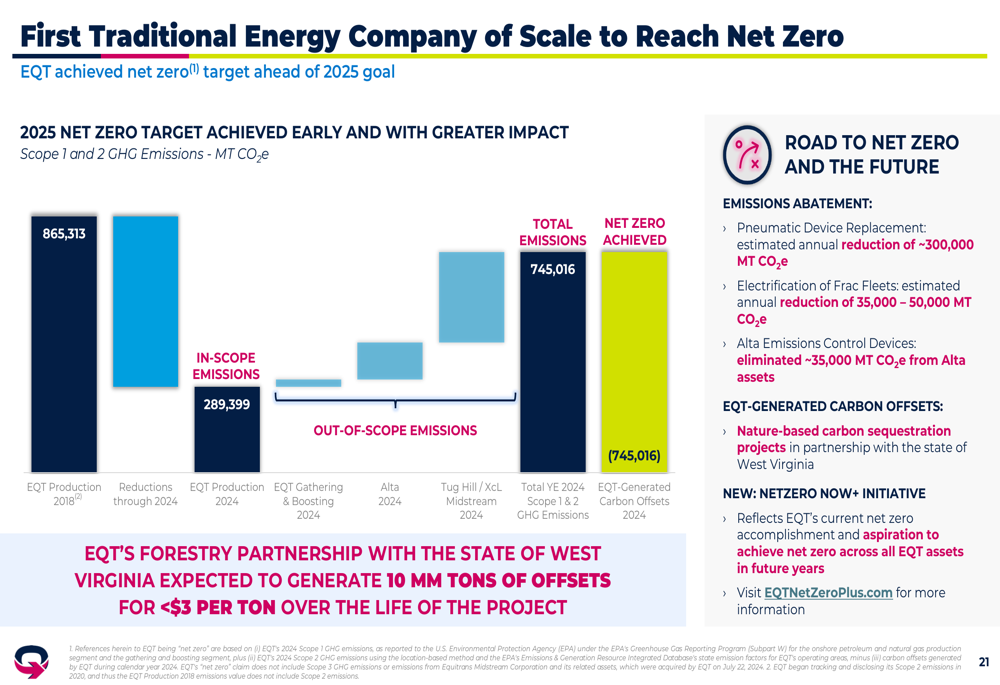

EQT has achieved its net zero target for Scope 1 and Scope 2 greenhouse gas emissions ahead of its 2025 goal, becoming the first traditional energy company of scale to reach this milestone. The company’s emissions reduction initiatives include pneumatic device replacement, electrification of frac fleets, and the implementation of emissions control devices.

The following slide details EQT’s sustainability achievements:

Additionally, EQT has established a forestry partnership with the state of West Virginia that is expected to generate 10 million tons of carbon offsets for less than $3 per ton over the life of the project, further enhancing the company’s environmental credentials.

Forward-Looking Statements

EQT has updated its guidance for 2025, increasing annual production guidance by 100 Bcfe and lowering full-year operating cost guidance by 6 cents per Mcfe, while maintaining its 2025 capital spending forecast as efficiency gains offset added activity from the Olympus acquisition, which closed on July 1, 2025.

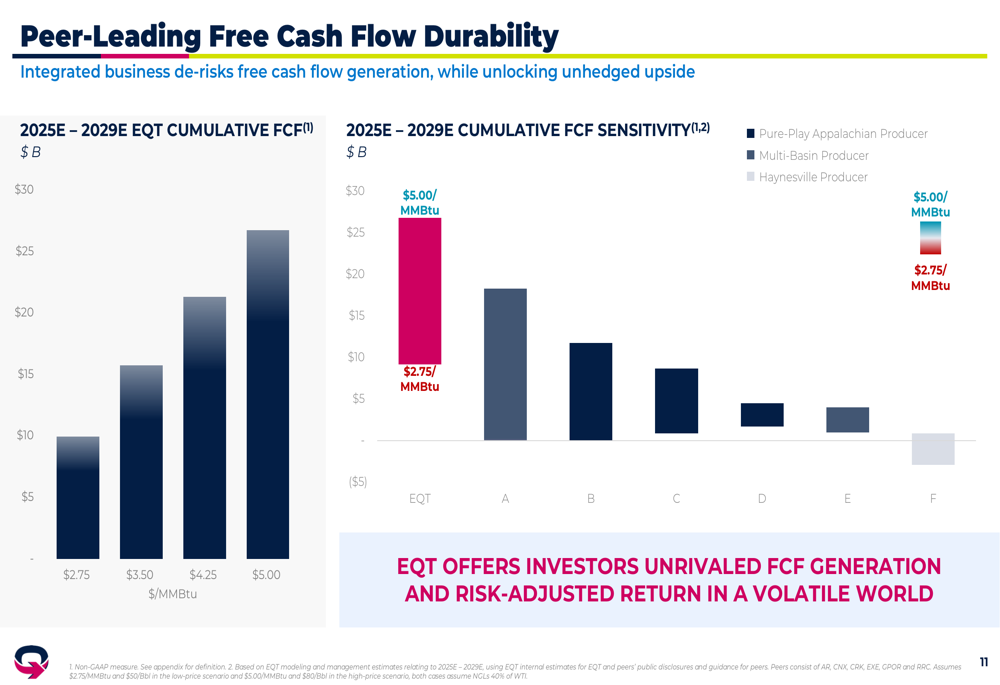

The company projects peer-leading free cash flow durability, with its integrated business model de-risking free cash flow generation while preserving unhedged upside potential. EQT’s low breakeven costs of approximately $2.00/MMBtu for unlevered free cash flow provide resilience across commodity cycles.

As illustrated in this chart showing EQT’s peer-leading free cash flow durability:

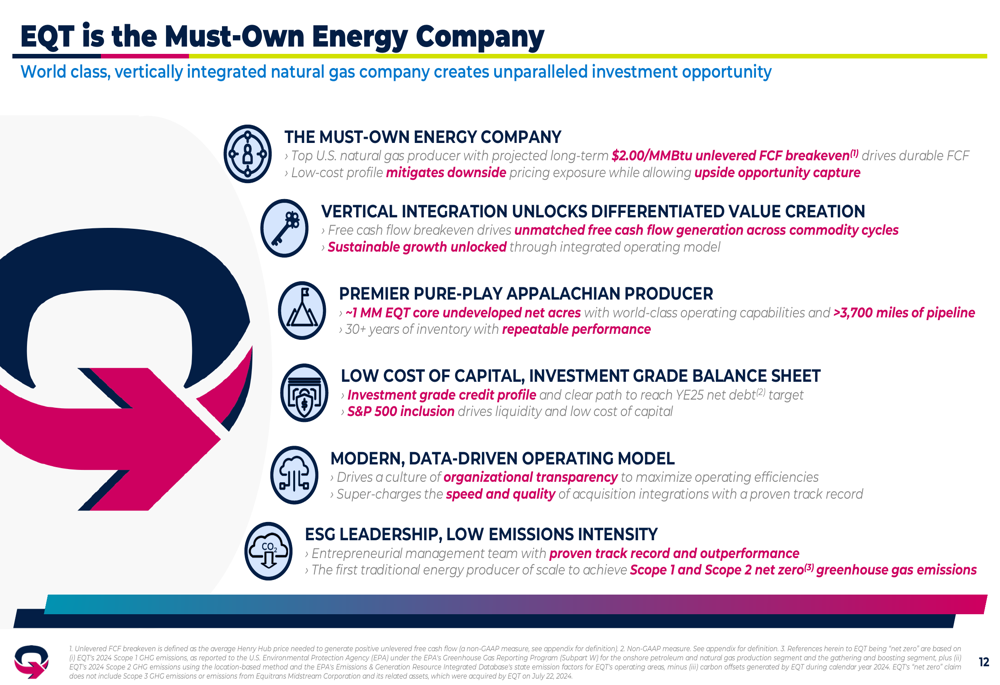

EQT positions itself as "the must-own energy company" based on its status as the top U.S. natural gas producer, vertical integration, premier Appalachian acreage position, investment grade balance sheet, data-driven operating model, and ESG leadership.

The following slide summarizes EQT’s investment case:

With approximately 1 million core undeveloped net acres, over 30 years of inventory, and a clear path to reaching its year-end 2025 net debt target, EQT appears well-positioned to deliver sustainable value to shareholders while capitalizing on growing natural gas demand from power generation, data centers, and LNG exports.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.