US LNG exports surge but will buyers in China turn up?

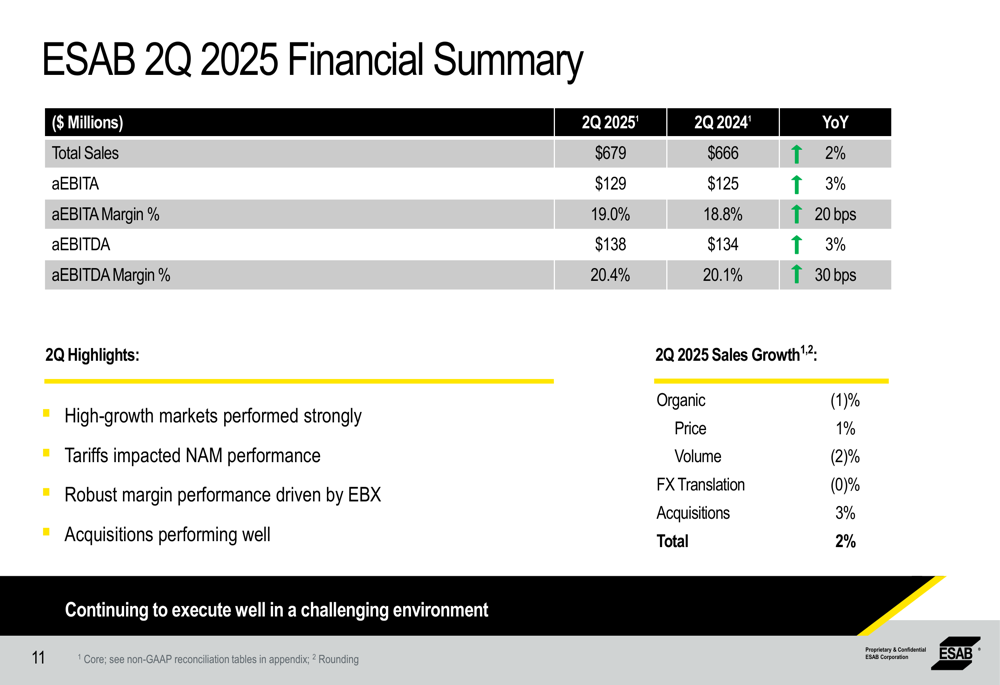

ESAB Corporation (NYSE:ESAB) presented its second quarter 2025 earnings results on August 6, revealing mixed regional performance but overall growth that prompted the company to raise its full-year guidance. The welding and cutting equipment manufacturer reported total sales of $679 million, representing a 2% increase in core sales growth year-over-year, while achieving a record core adjusted EBITDA margin of 20.4%.

Quarterly Performance Highlights

ESAB’s second quarter results showed divergent regional performance, with strong growth in EMEA & APAC markets offsetting challenges in the Americas. The company reported adjusted EBITDA of $138 million, a 3% increase compared to the same period last year, with margins expanding by 30 basis points.

"We delivered stellar performance in high-growth markets, though we experienced tariff-related softness in Mexico and Automation," noted the company in its presentation. Overall organic sales decreased by 1%, while acquisitions contributed 3% to sales growth.

As shown in the following financial summary:

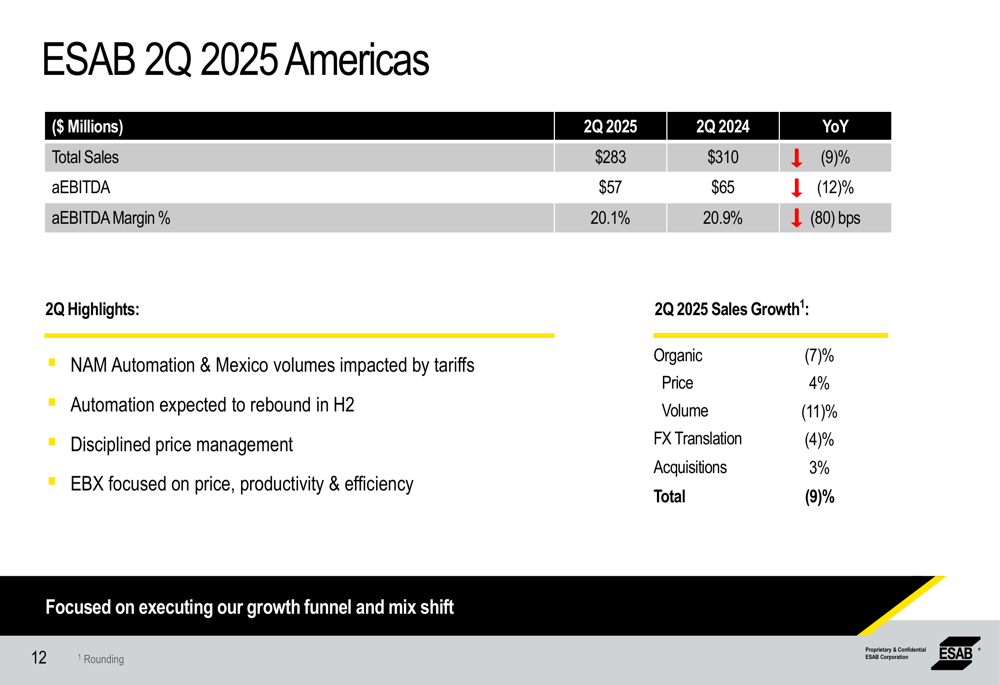

The Americas segment faced significant headwinds, with sales declining 9% year-over-year to $283 million. Adjusted EBITA for the region fell 12% to $57 million, though the segment maintained a healthy 20.1% margin. The company attributed this decline primarily to tariff impacts on North American Automation and Mexico volumes.

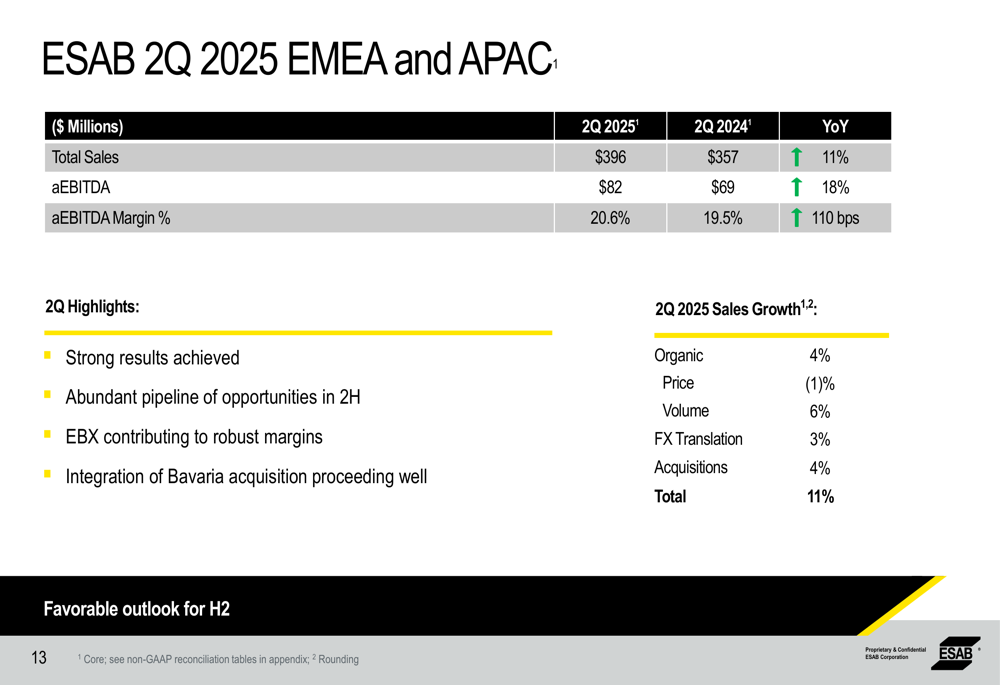

In contrast, ESAB’s EMEA & APAC segment delivered robust performance with sales of $396 million, representing an 11% increase year-over-year. Adjusted EBITA in these regions grew by 18% to $82 million, with margins reaching 20.6%. The company cited strong results across Europe, Middle East, Africa, and Asia, with particularly strong growth in India and double-digit growth in the Middle East and Africa region.

Strategic Acquisitions and Growth Initiatives

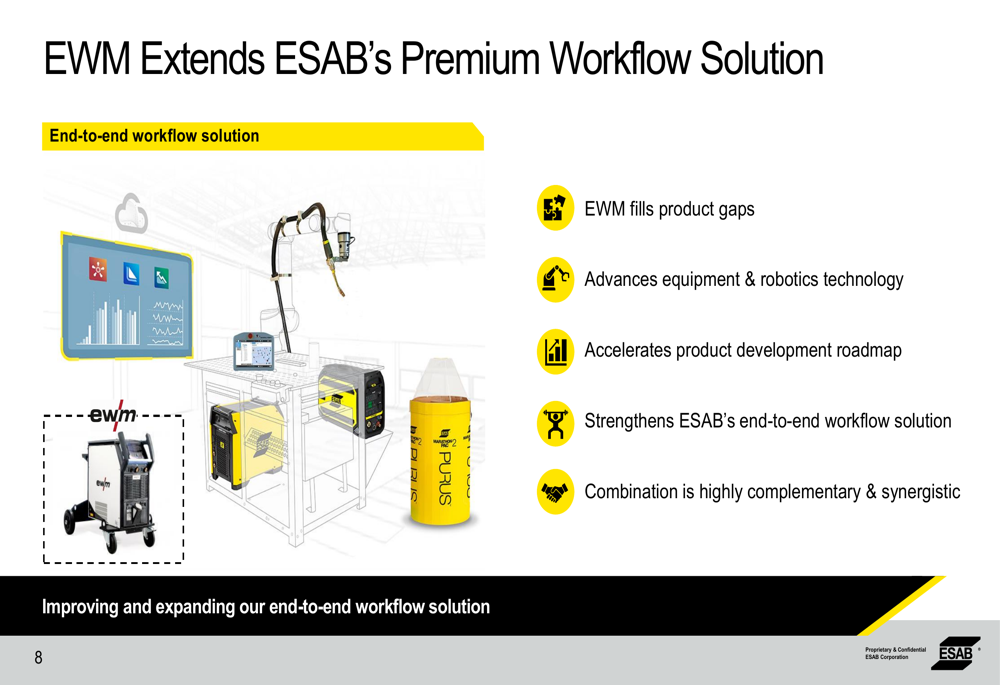

A significant highlight of ESAB’s presentation was the announcement of multiple strategic acquisitions aimed at expanding the company’s capabilities in equipment, robotics, and medical gas control systems.

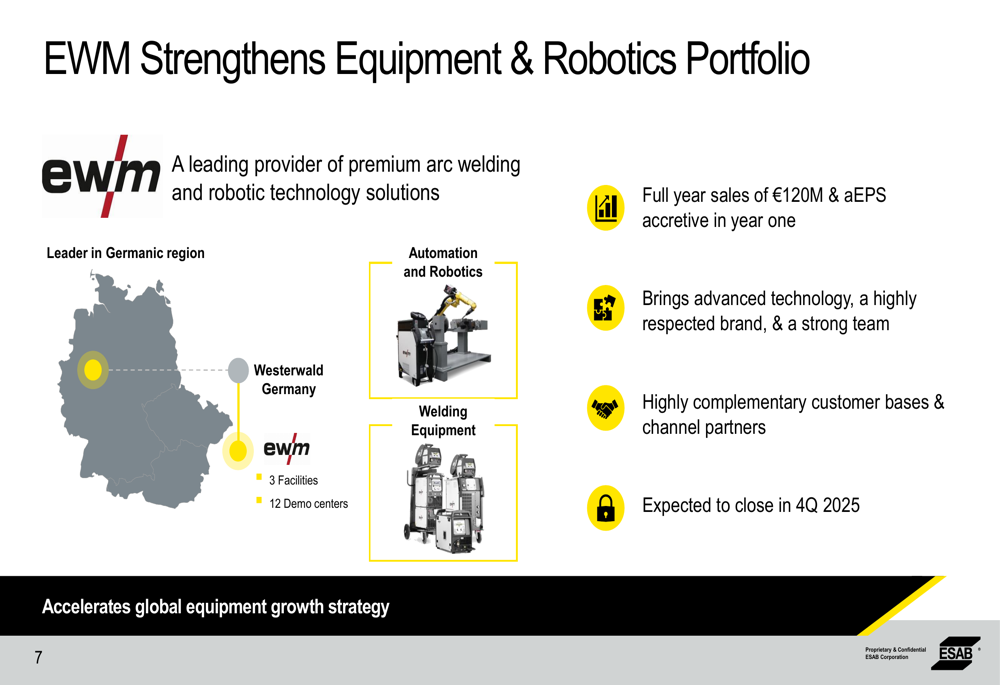

The most notable acquisition is EWM, a leading provider of premium arc welding and robotic technology solutions based in Westerwald, Germany. With annual sales of approximately €120 million, EWM is expected to be accretive to earnings per share in its first year following the anticipated closing in Q4 2025.

The EWM acquisition strategically extends ESAB’s premium workflow solutions by filling product gaps and advancing the company’s equipment and robotics technology. According to the presentation, the combination is "highly complementary and synergistic," strengthening ESAB’s end-to-end workflow solutions.

In addition to EWM, ESAB completed two acquisitions in the medical gas control space: DeltaP, a European-based manufacturer of medical central gas systems with approximately $10 million in sales, and Aktiv, an India-based medical gas system manufacturer with approximately $5 million in sales. Both acquisitions feature attractive gross margins exceeding 40%.

These acquisitions align with ESAB’s strategy to expand its medical gas control portfolio, which now extends across the entire hospital gas system from oxygen generation to point-of-use applications.

Operational Excellence and Innovation

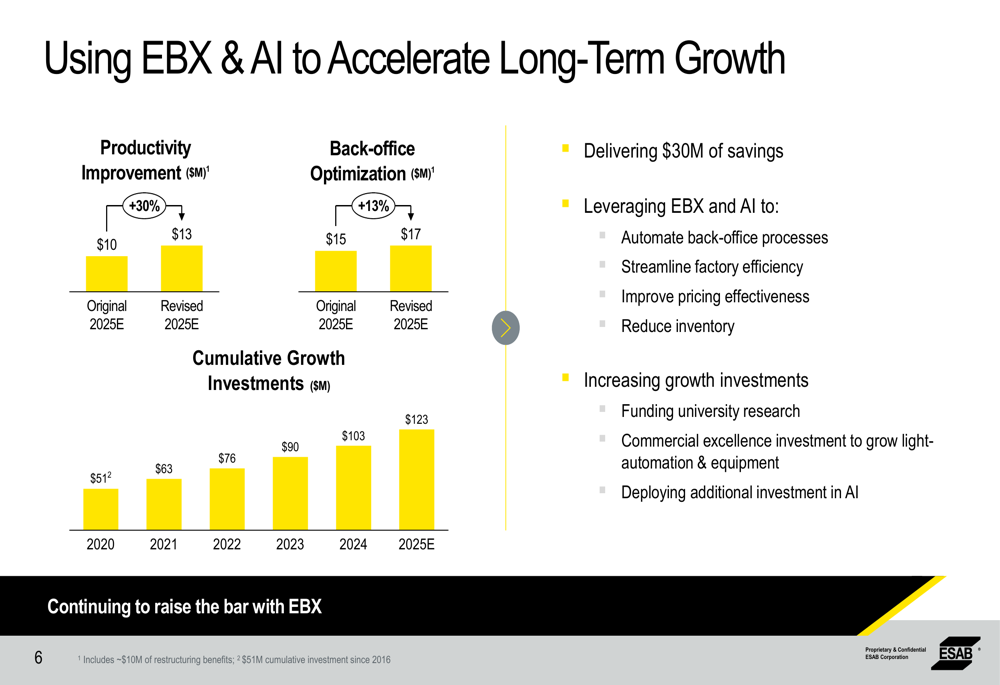

ESAB highlighted its use of EBX (ESAB Business Excellence) and AI initiatives to drive operational improvements and long-term growth. The company reported delivering $30 million in savings through these initiatives, which include automating back-office processes, streamlining factory efficiency, improving pricing effectiveness, and reducing inventory.

The company is also investing in talent development through its "Flame Trainee Internship Program," which has trained over 100 leaders in fabrication technology and is expanding globally. This initiative aims to accelerate professional growth and develop the next generation of fabrication technology leaders.

Forward-Looking Statements and Guidance

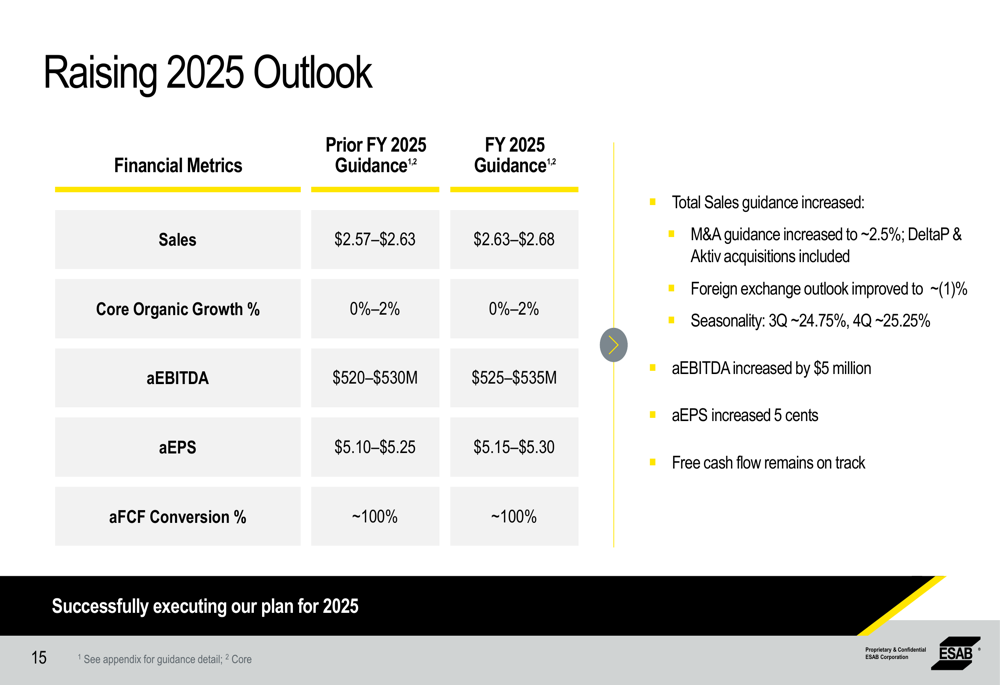

Based on its strong performance and strategic acquisitions, ESAB raised its full-year 2025 guidance across multiple metrics. The company now projects total sales of $2.63-2.68 billion, up from its previous guidance of $2.55-2.60 billion. Adjusted EBITDA is expected to reach $525-535 million, an increase from the prior guidance of $510-525 million.

For the remainder of 2025, ESAB expects core organic growth of 0-2%, with M&A contributing approximately 2.5% to overall growth. The company anticipates adjusted EPS of $5.15-5.30, up from its previous guidance of $5.00-5.20.

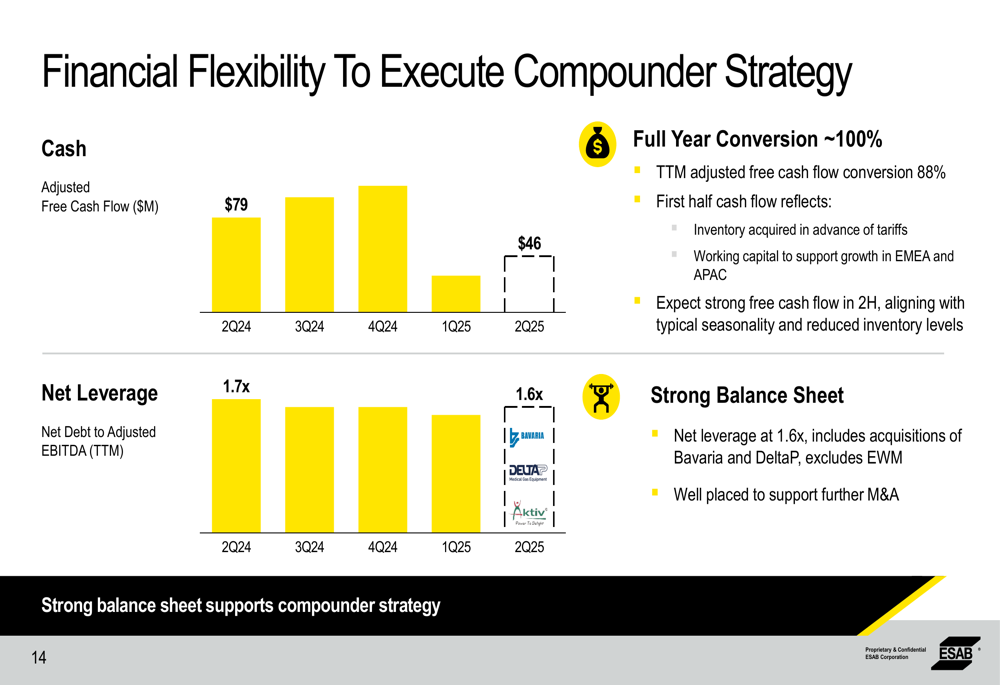

The company’s financial position remains strong, with net leverage at 1.6x and strong free cash flow expected in the second half of the year. This financial flexibility supports ESAB’s "compounder strategy" of combining organic growth with strategic acquisitions.

Market Context and Outlook

Looking ahead to the second half of 2025, ESAB expects improvement in North American Automation and noted that the third quarter is "off to a good start." The company anticipates that EBX initiatives will continue driving margin expansion, while its strong balance sheet will support further strategic acquisitions.

This positive outlook comes despite ongoing challenges from tariffs in North America, which have impacted volumes by approximately 500 basis points according to the company’s presentation. ESAB’s global footprint has proven valuable in offsetting these regional challenges, with Europe remaining steady and well-positioned to capture EU stimulus, while emerging markets continue to deliver strong growth.

ESAB’s stock closed at $132.03 on August 5, 2025, representing a 0.76% increase. The stock has traded between $92.86 and $135.97 over the past 52 weeks, suggesting investors have responded positively to the company’s strategic direction and financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.