US stock futures inch lower after Wall St marks fresh records on tech gains

Eversource Energy (NYSE:ES) reported a slight increase in first-quarter earnings as the company continues its strategic shift toward becoming a pure-play regulated utility. According to the company’s May 2, 2025 earnings presentation, Eversource achieved GAAP earnings per share of $1.50 for Q1 2025, up marginally from $1.49 in the same period last year.

Quarterly Performance Highlights

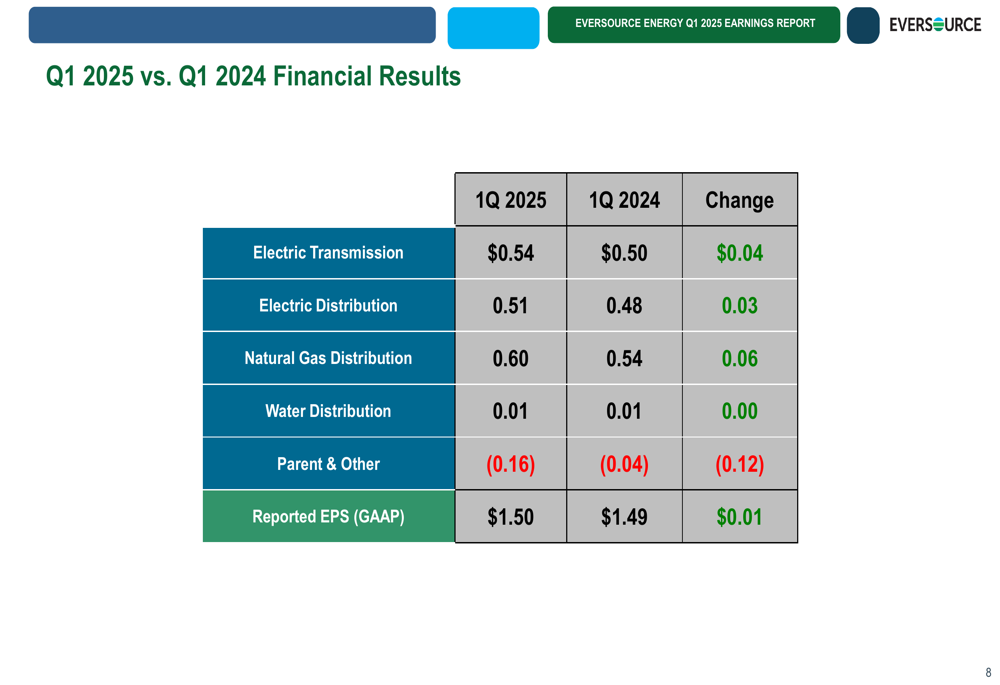

Eversource’s Q1 results showed mixed performance across business segments. The natural gas distribution business delivered the strongest year-over-year improvement, while the parent company segment experienced a significant decline.

As shown in the following quarterly results breakdown:

The electric transmission segment contributed $0.54 per share, up $0.04 from Q1 2024, while electric distribution added $0.51 per share, a $0.03 increase. Natural gas distribution showed the strongest growth, contributing $0.60 per share, up $0.06 year-over-year. The water distribution segment remained flat at $0.01 per share, while the parent and other segment declined significantly to ($0.16) from ($0.04) in the prior year.

This modest overall growth comes as Eversource’s stock has faced pressure, with shares closing at $59.08 on May 1, down 0.67% for the day, and falling an additional 2.76% in after-hours trading.

Strategic Initiatives

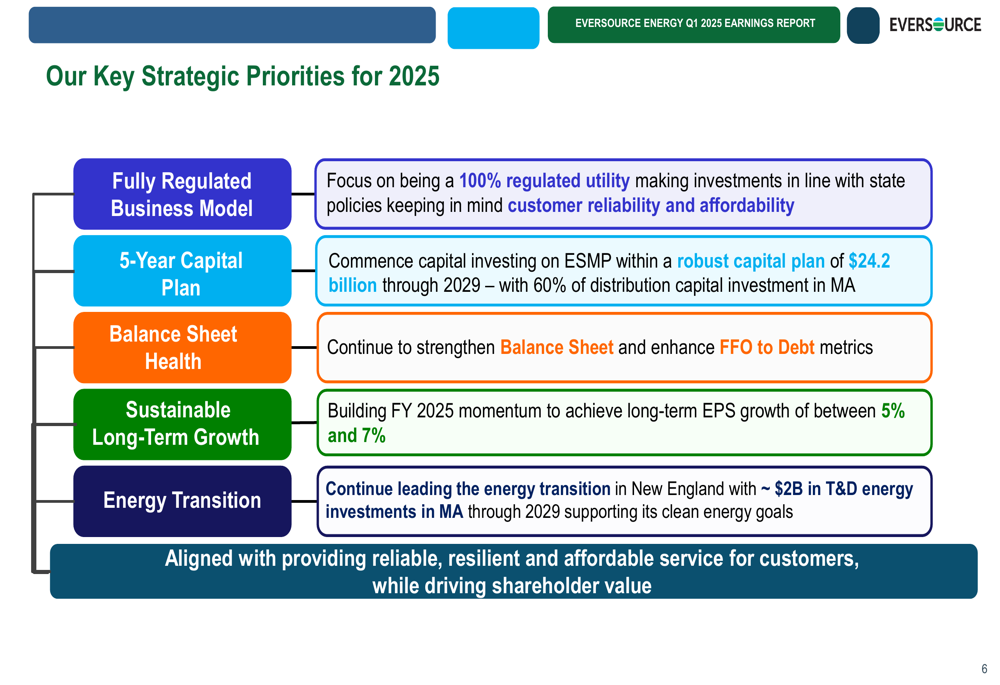

Eversource outlined five key strategic priorities for 2025, emphasizing its transition to a fully regulated business model and sustainable long-term growth:

The company is positioning itself as a "pure play pipes and wires regulated utility" following its exit from offshore wind investments. This strategic shift includes the pending sale of its Aquarion water business, which is expected to generate $1.6 billion in proceeds.

Eversource plans significant capital investments of $24.2 billion through 2029, with approximately 60% of distribution capital investment targeted for Massachusetts. The company is also focusing on energy transition initiatives, with approximately $2 billion in transmission and distribution energy investments in Massachusetts through 2029 to support the state’s clean energy goals.

The utility is also investing in customer experience improvements, including Advanced Metering Infrastructure (AMI) in Massachusetts. Network equipment installation is scheduled for the second half of 2025, with smart meter deployment beginning in July 2025 in Western Massachusetts.

Capital Expenditure and Rate Base Growth

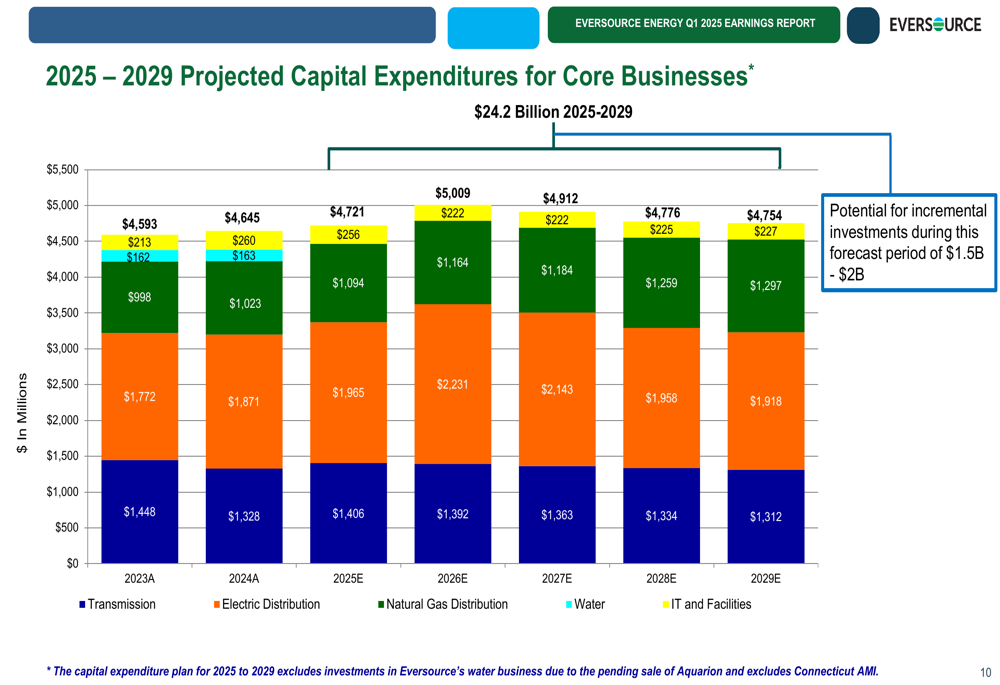

Eversource’s five-year capital expenditure plan shows increasing investments across its core regulated businesses:

The $24.2 billion capital plan excludes investments in the water business due to the pending sale of Aquarion and excludes Connecticut AMI. The company noted potential for an additional $1.5-$2 billion in incremental investments during this forecast period.

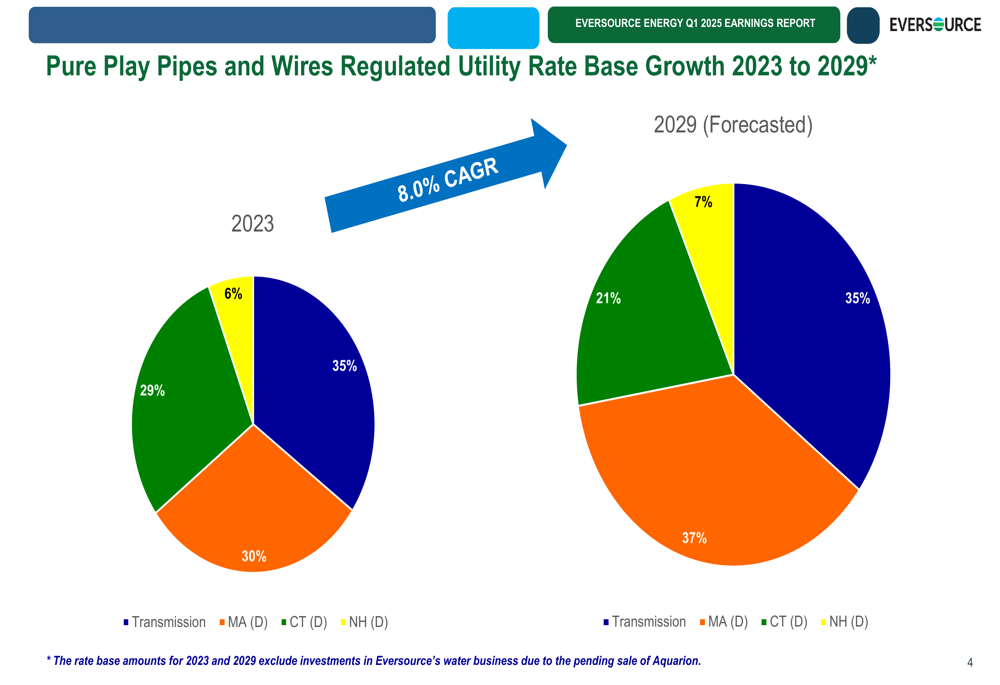

These investments are expected to drive significant rate base growth from $26.4 billion in 2023 to a projected $41.9 billion by 2029, representing an 8.0% compound annual growth rate:

The composition of the rate base is also shifting, with Massachusetts increasing from 30% to 37% of the total, while the transmission portion decreases from 29% to 21%. This reflects the company’s strategic emphasis on state-level distribution infrastructure investments.

Balance Sheet Strengthening Initiatives

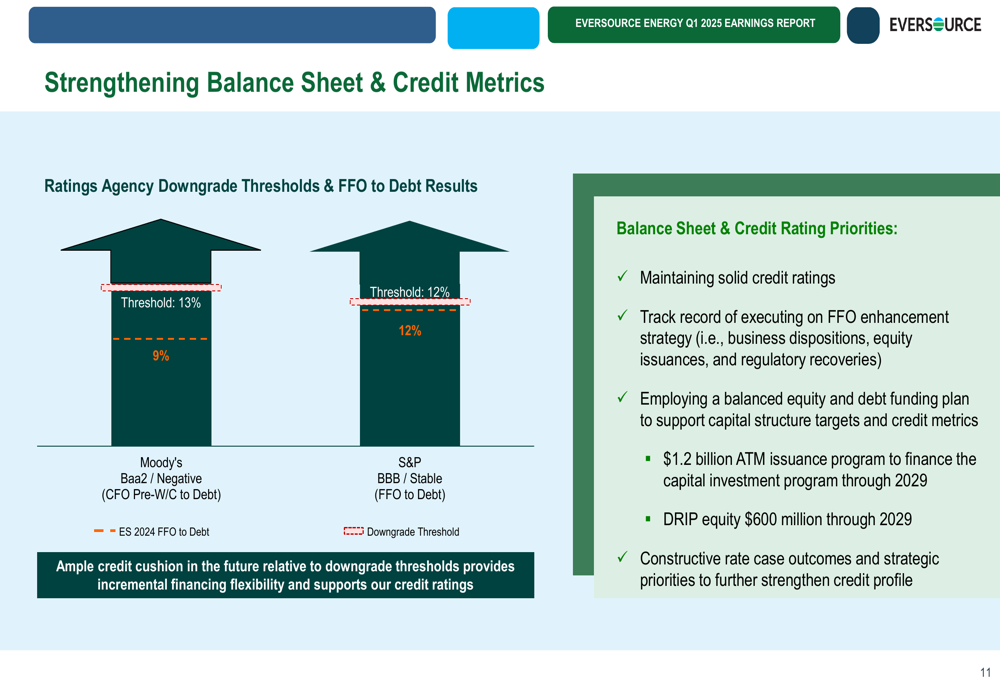

A key focus of the presentation was Eversource’s efforts to strengthen its balance sheet and credit metrics, which currently sit at or below rating agency thresholds:

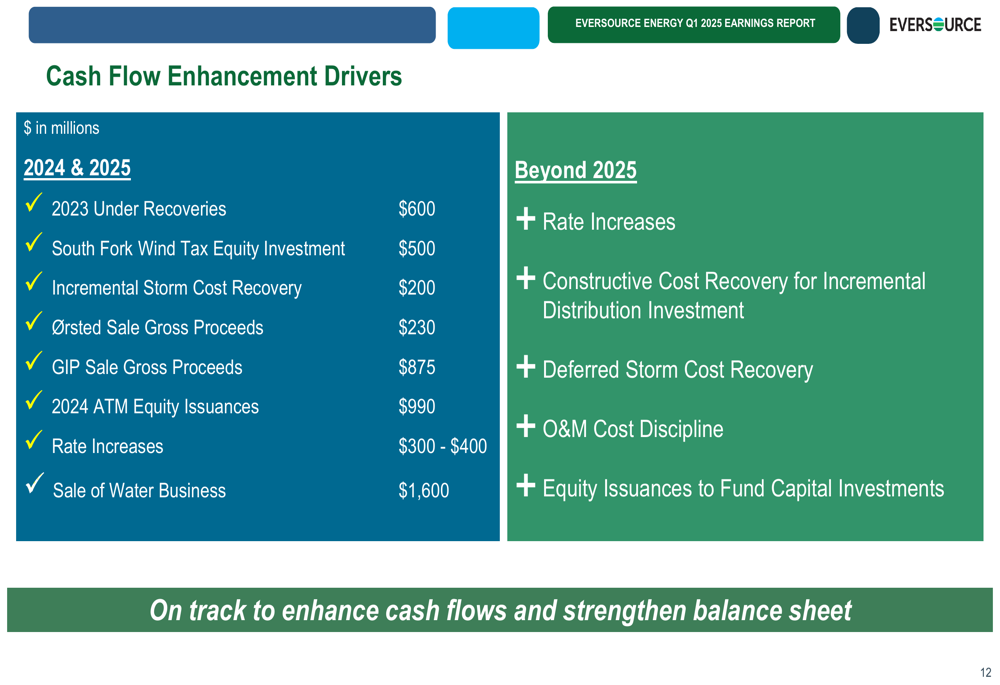

The company’s FFO to Debt ratio stands at 9% against Moody’s downgrade threshold of 13%, while meeting S&P’s threshold of 12%. To address this, Eversource outlined several cash flow enhancement initiatives:

These initiatives include recovering $600 million in 2023 under-recoveries, proceeds from asset sales (including $230 million from Ørsted sale, $875 million from GIP sale, and $1.6 billion from the water business sale), and $990 million from ATM equity issuances completed in October 2024.

The company has also implemented a $1.2 billion ATM issuance program and expects to generate approximately $600 million through its dividend reinvestment plan (DRIP) through 2029.

Regulatory Progress and Outlook

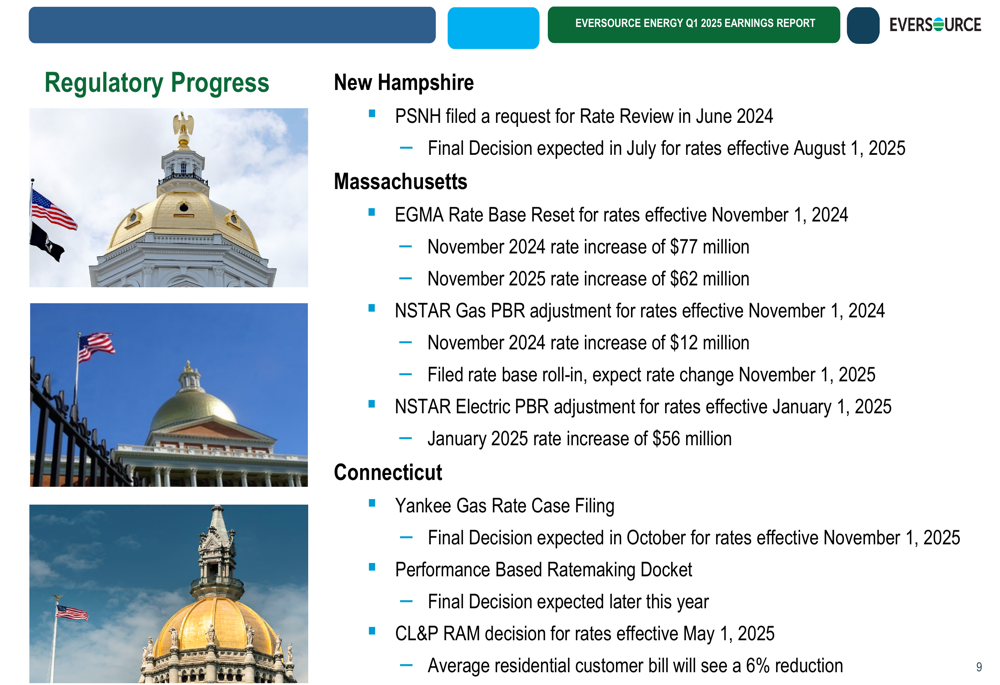

Eversource highlighted several key regulatory developments across its service territories:

In New Hampshire, PSNH filed for a rate review in June 2024, with a final decision expected in July for rates effective August 1, 2025. Massachusetts developments include EGMA rate base reset for rates effective November 1, 2024, including a $77 million rate increase, and NSTAR Electric PBR adjustment with a January 2025 rate increase of $56 million. In Connecticut, Yankee Gas has a rate case filing with a final decision expected in October for rates effective November 1, 2025.

Forward-Looking Statements

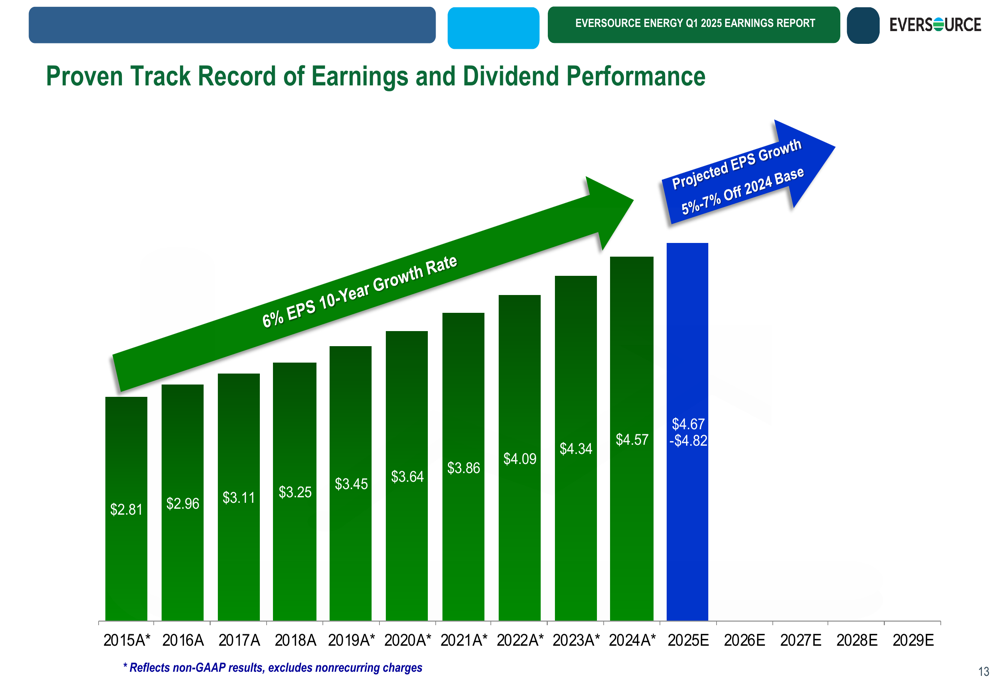

Eversource reaffirmed its long-term EPS growth target of 5-7%, building on its historical performance:

The company has maintained consistent earnings growth since 2015 and projects continued performance within its targeted range. This growth is expected to be driven by its regulated business investments and constructive regulatory outcomes.

As Eversource continues its transition to a pure-play regulated utility model, management emphasized the company’s position as the largest utility in New England, serving 4.6 million customers across three states with $60 billion in total assets. The strategic focus on transmission and distribution infrastructure, coupled with balance sheet strengthening initiatives, reflects the company’s efforts to deliver reliable service while maintaining financial stability in a challenging utility environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.