Street Calls of the Week

EVgo Inc. (NASDAQ:EVGO) delivered a record first quarter in 2025, reporting substantial growth across key operational and financial metrics while making progress toward EBITDA breakeven. The company’s Q1 earnings presentation, delivered on May 6, 2025, highlighted accelerating throughput, expanding network capacity, and improving utilization rates amid favorable market dynamics for non-Tesla electric vehicles.

Quarterly Performance Highlights

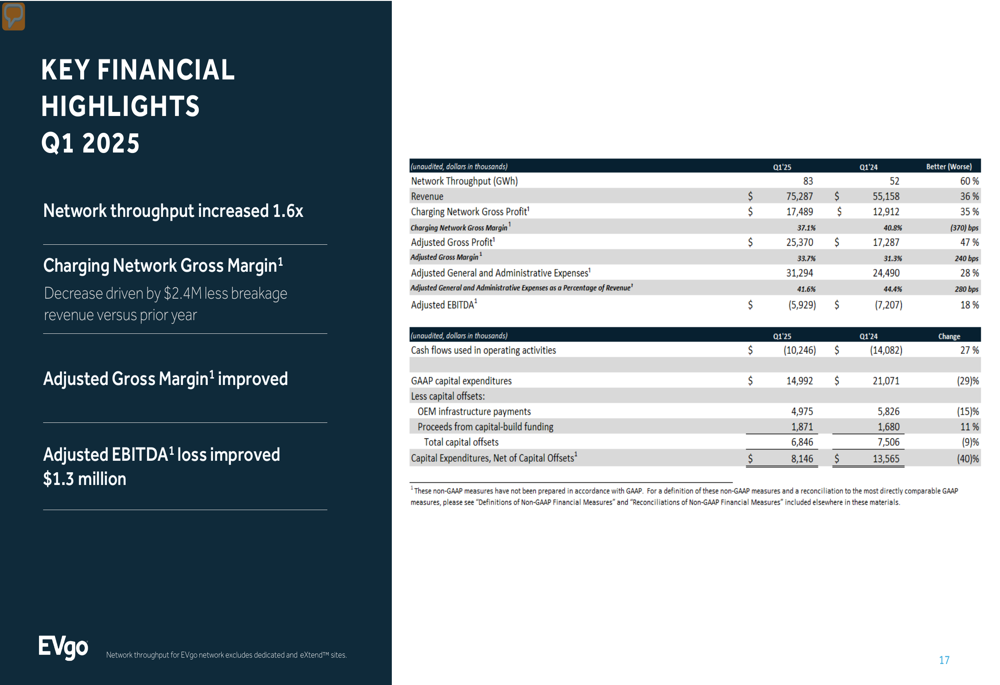

EVgo reported Q1 2025 revenue of $75.3 million, representing 36% year-over-year growth, while network throughput surged 60% to 83 GWh compared to the same period last year. The company’s operational stall count reached 4,240, a 32% increase year-over-year, with 180 new stalls added during the quarter.

"Q1 2025 was a record quarter for EVgo across multiple metrics," said Badar Khan, CEO of EVgo, emphasizing the company’s thirteenth consecutive quarter of double-digit year-over-year charging revenue growth.

The company’s financial performance showed significant improvement, with adjusted EBITDA loss narrowing to $5.9 million, an 18% improvement from the $7.2 million loss in Q1 2024. Cash flow used in operating activities improved by 27% to $10.2 million, while the company maintained a strong cash position of $171 million.

As shown in the following summary of key financial highlights:

Strategic Initiatives & Customer Experience

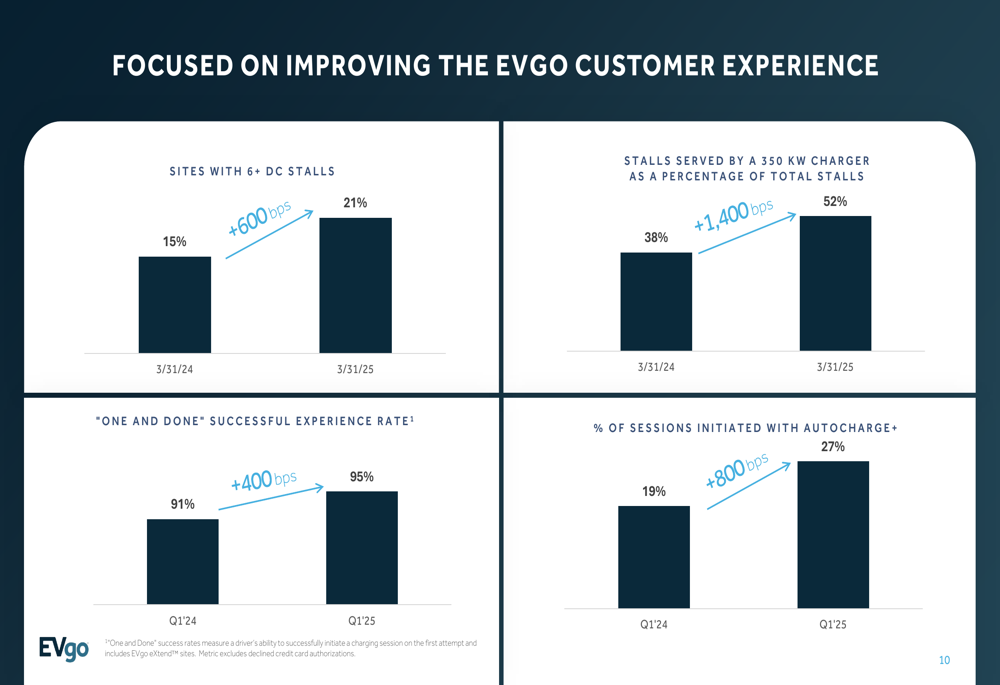

EVgo highlighted several strategic initiatives aimed at enhancing customer experience and operational efficiency. The company increased the percentage of sites with six or more DC stalls by 600 basis points year-over-year to 21%, while expanding the proportion of stalls served by 350kW chargers from 38% to 52%.

The "One and Done" successful experience rate improved to 95%, up from 91% in Q1 2024, indicating higher reliability. Additionally, sessions initiated with Autocharge+ increased from 19% to 27%, streamlining the charging process for returning customers.

The following chart illustrates these customer experience improvements:

On the operational efficiency front, EVgo signed a joint development agreement with Delta Electronics for next-generation charging architecture and reduced call center costs per call by 37% compared to the prior year. The company is also developing dynamic pricing algorithms and beginning to deploy J3400 (NACS) connectors to serve Tesla (NASDAQ:TSLA) vehicles.

"Rideshare, OEM charging credit, and subscription plans accounted for 55% of Q1 2025 throughput," noted Khan, highlighting the company’s success in capturing high-value customers.

Financial Analysis & 2025 Outlook

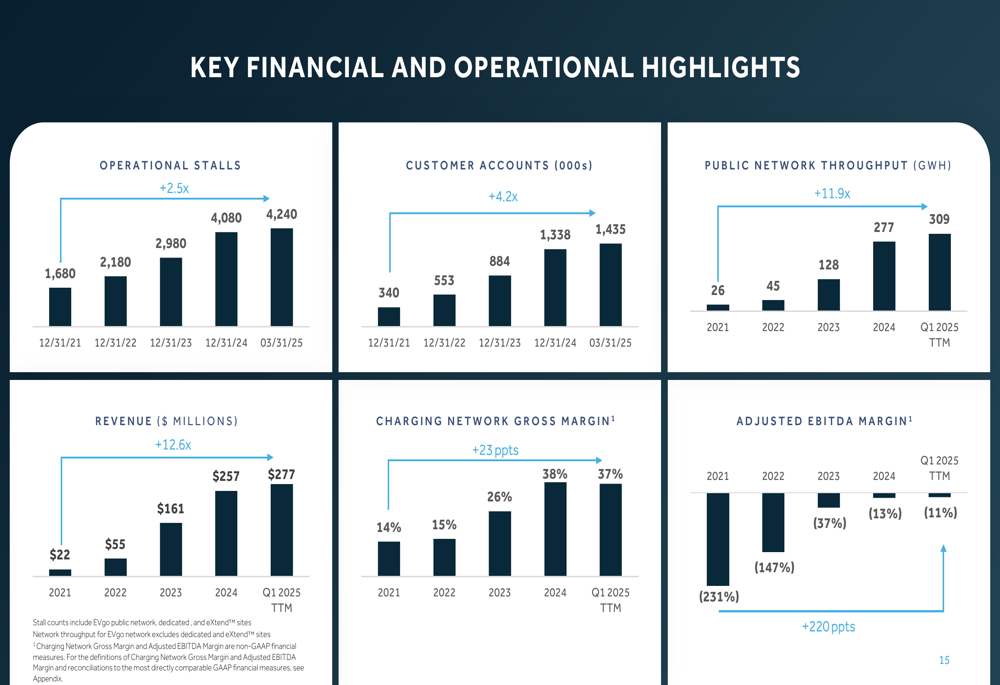

EVgo’s long-term financial trajectory shows remarkable improvement across key metrics. Since December 2021, the company has increased its operational stalls by 2.5x, customer accounts by 4.2x, and public network throughput by 11.9x. Revenue has grown 12.6x over the same period, while charging network gross margin has improved by 23 percentage points.

The following chart demonstrates this multi-year growth trajectory:

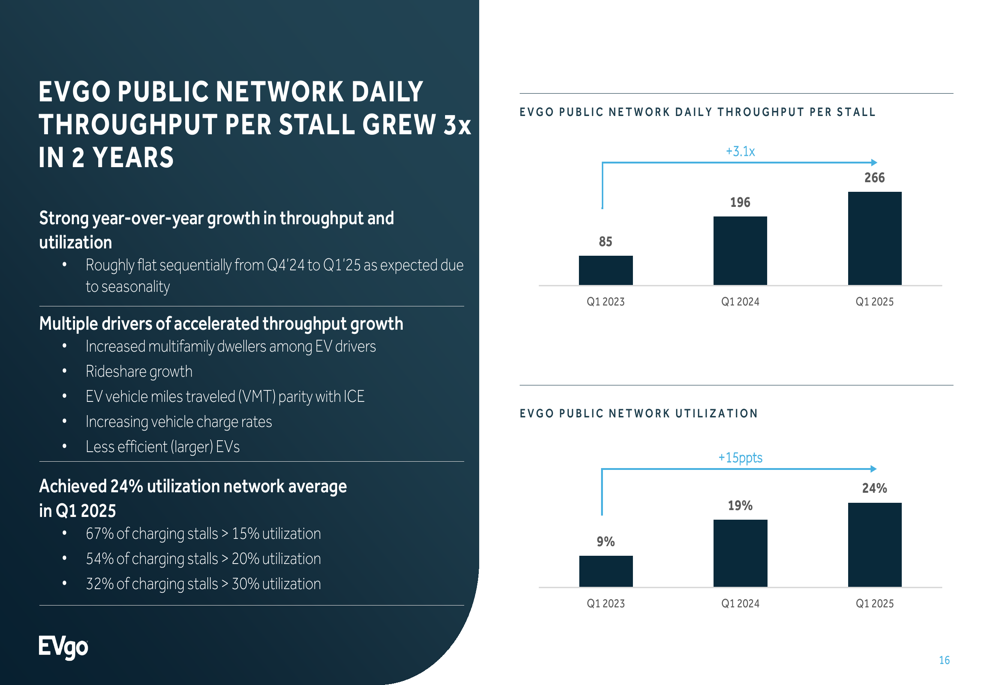

Daily throughput per stall has grown threefold in just two years, reaching 266 kWh in Q1 2025 compared to 85 kWh in Q1 2023. This has driven network utilization from 9% to 24% over the same period, significantly improving the economics of EVgo’s charging infrastructure.

The utilization improvement is illustrated in this chart:

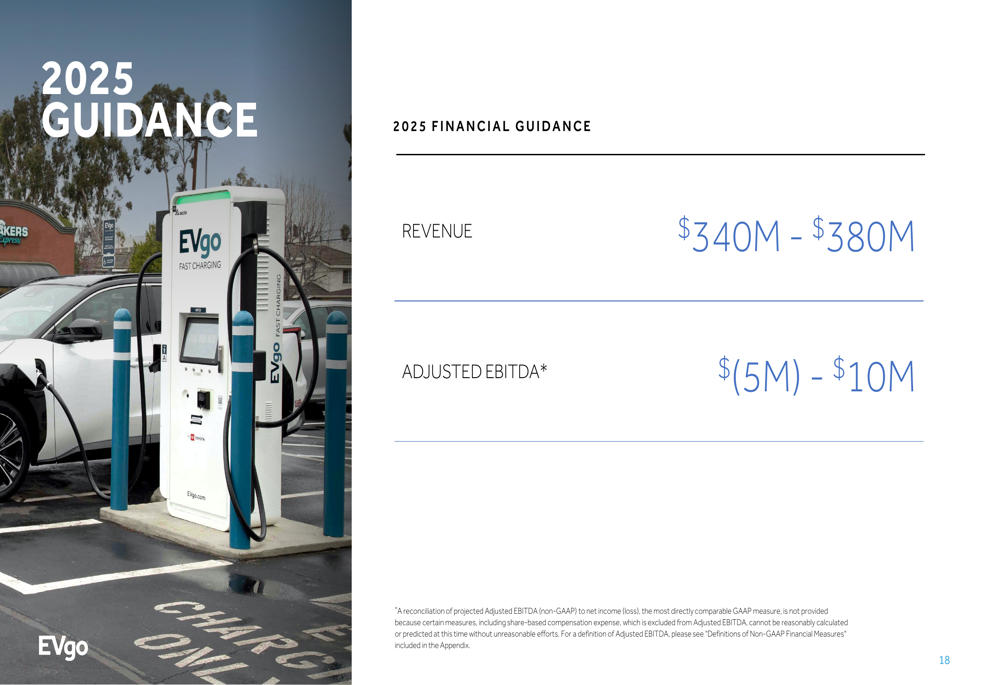

For full-year 2025, EVgo provided guidance of $340-380 million in revenue and adjusted EBITDA between -$5 million and +$10 million, suggesting the company could achieve EBITDA breakeven this year. This outlook represents significant growth from the $257 million in revenue reported for 2024.

Competitive Positioning & Industry Trends

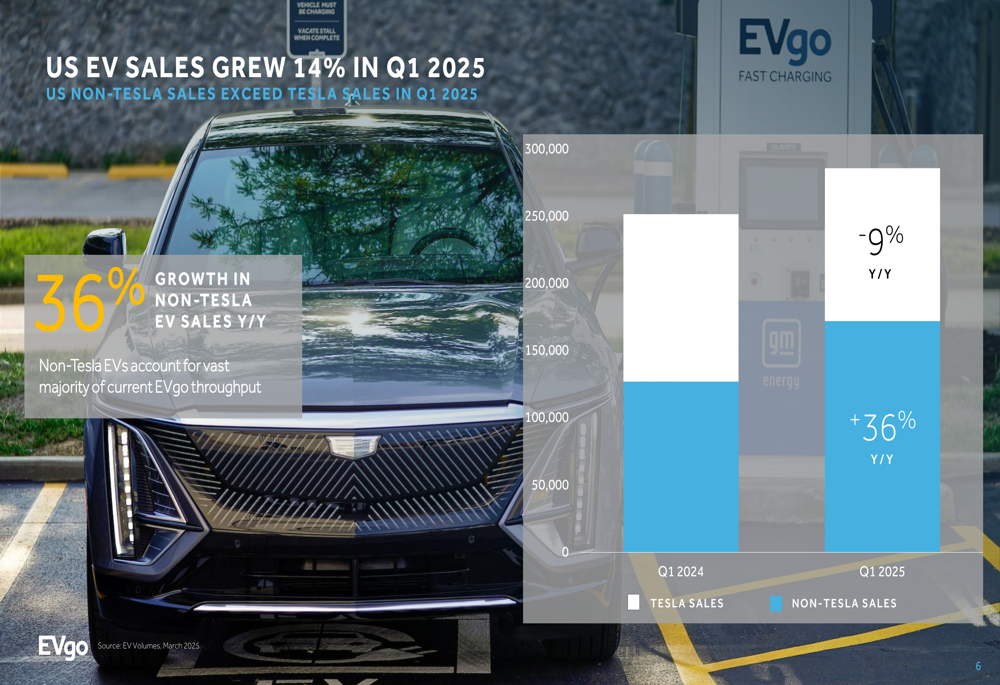

EVgo’s presentation highlighted favorable market dynamics, particularly the growth of non-Tesla electric vehicles, which account for the majority of EVgo’s throughput. US EV sales grew 14% in Q1 2025, with non-Tesla EV sales exceeding Tesla sales for the first time and growing 36% year-over-year.

The following chart illustrates this shift in the US EV market:

The company noted that DCFC (Direct Current Fast Charging) supply growth has been flat for the last seven quarters, while EVgo captured 10% of net stall growth in Q1 2025. This suggests EVgo is gaining market share in a constrained supply environment.

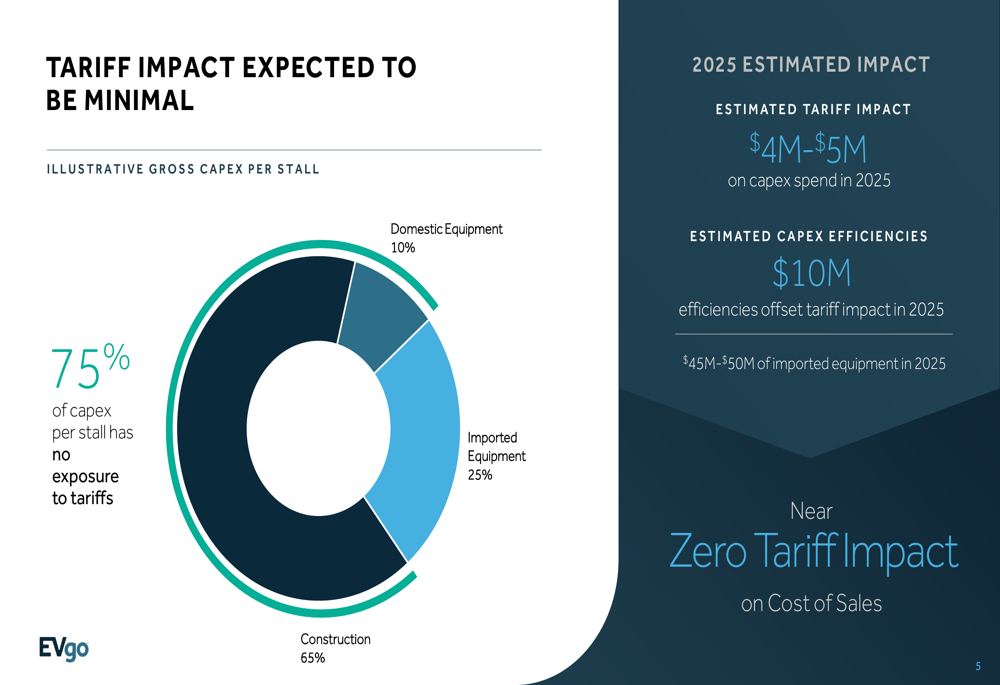

EVgo also addressed concerns about tariffs on imported equipment, stating that 75% of capex per stall has no exposure to tariffs. The company estimates a $4-5 million tariff impact on capex spending in 2025, which is expected to be fully offset by $10 million in capex efficiencies, resulting in minimal impact on cost of sales.

The tariff impact breakdown is shown here:

Looking ahead, EVgo expects demand for DCFC to continue outpacing supply, with the ratio of electric vehicles in operation to DCFC stalls projected to grow 1.8-2.1x by 2030. This favorable supply-demand dynamic positions EVgo well for continued growth as the EV market expands.

The company is also making progress on financing initiatives, having completed the first and second advances for $94 million under its $1.25 billion Department of Energy loan guarantee. EVgo plans to offset 30% of 2025 vintage capital expenditures through capital offsets, including the 30C income tax credit transfer.

With its expanding network, improving operational efficiency, and strong position in a growing market, EVgo appears well-positioned to capitalize on the continued adoption of electric vehicles while progressing toward sustainable profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.