Trump meets Zelenskiy, says Putin wants war to end, mulls trilateral talks

Introduction & Market Context

Exelixis (NASDAQ:EXEL) presented its second quarter 2025 financial results on July 28, 2025, highlighting the continued growth of its cabozantinib franchise and progress across its development pipeline. The company reported non-GAAP earnings per share of $0.75, exceeding analyst expectations of $0.64, despite revenue of $568.3 million falling slightly below forecasts of $578.46 million. Following the earnings release, Exelixis shares rose 0.86% in aftermarket trading, reflecting positive investor sentiment toward the company’s performance and strategic direction.

As shown in the following comprehensive overview of the company’s quarterly achievements, Exelixis demonstrated strong momentum in its core business while advancing key pipeline candidates:

Quarterly Performance Highlights

The second quarter of 2025 was marked by robust performance in Exelixis’ cabozantinib franchise, which grew 19% year-over-year to $520 million compared to $438 million in Q2 2024. This growth was driven by the company’s continued leadership in renal cell carcinoma (RCC) and the successful launch of CABOMETYX in neuroendocrine tumors (NET), which now represents approximately 4% of quarterly net product revenue.

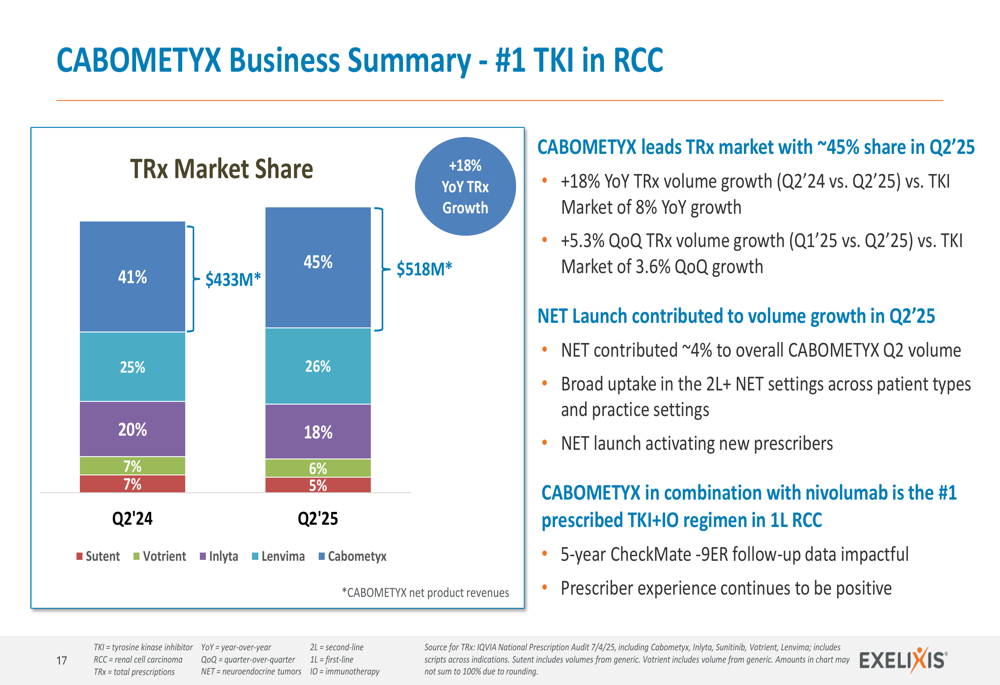

The company’s flagship product, CABOMETYX, maintained its dominant position in the RCC market while rapidly establishing leadership in the NET space. As illustrated in the following chart, CABOMETYX has achieved the #1 position in the RCC tyrosine kinase inhibitor (TKI) market:

CABOMETYX in combination with nivolumab remained the most prescribed TKI+IO regimen in first-line RCC for the eleventh consecutive quarter, demonstrating the product’s sustained competitive advantage. The company has also successfully executed its NET launch plan, with early uptake exceeding expectations.

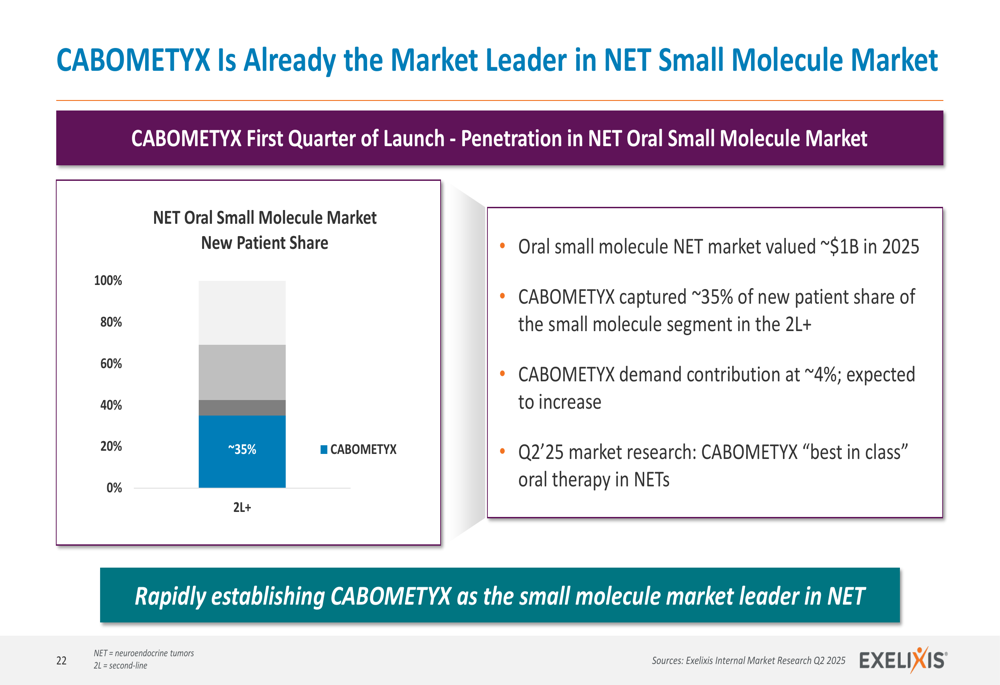

As shown in the following slide, CABOMETYX has quickly established itself as the market leader in the NET small molecule market:

Detailed Financial Analysis

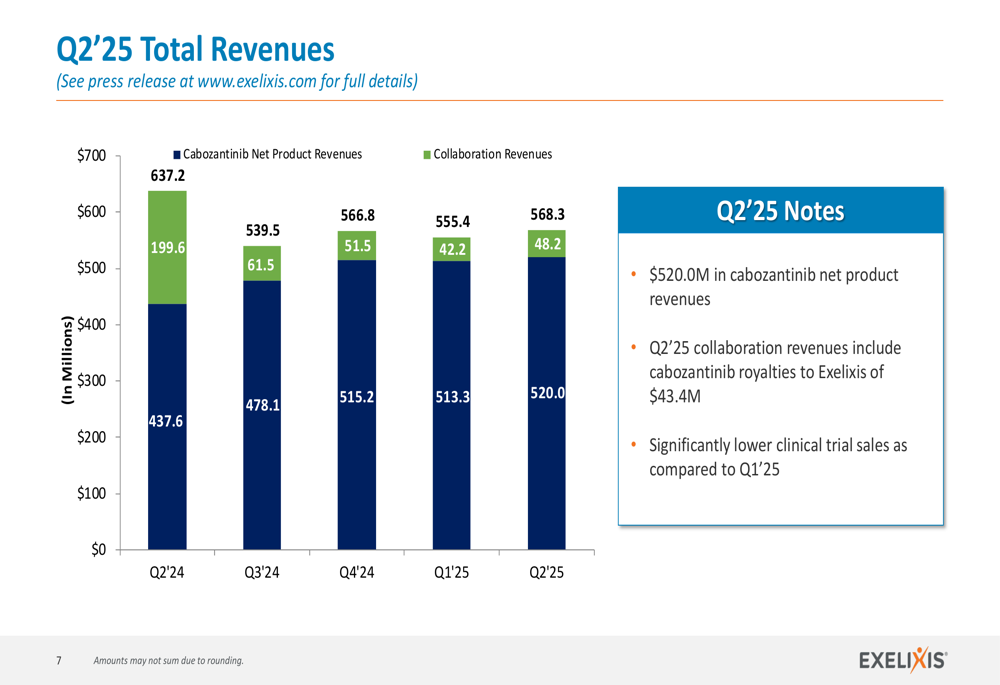

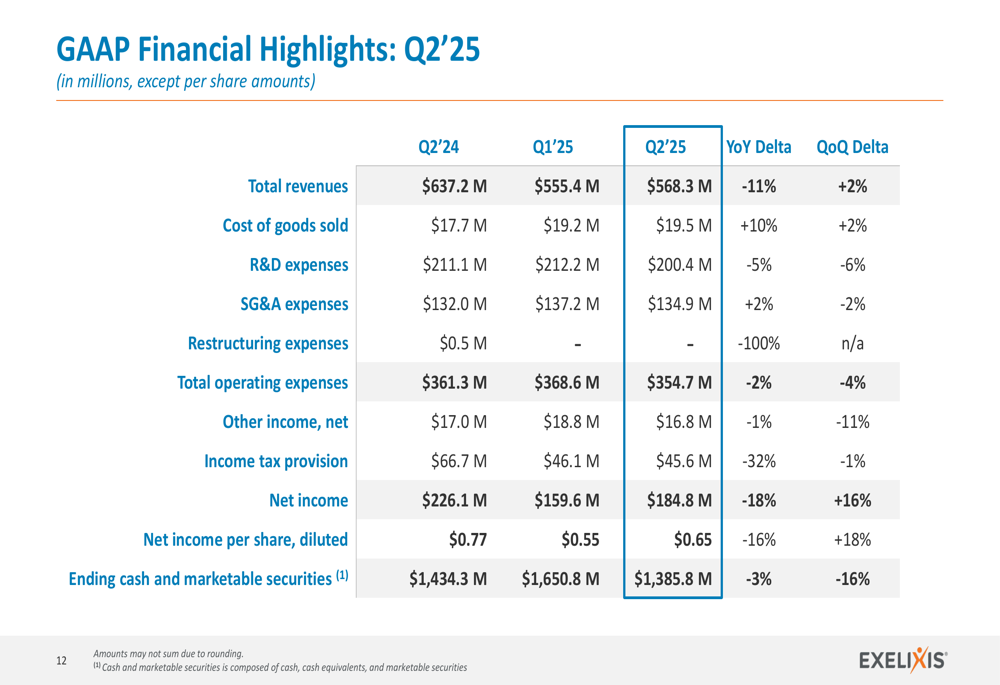

Exelixis reported total revenues of $568.3 million for Q2 2025, representing an 11% decrease year-over-year but a 2% increase quarter-over-quarter. The following chart illustrates the company’s revenue performance over the past five quarters:

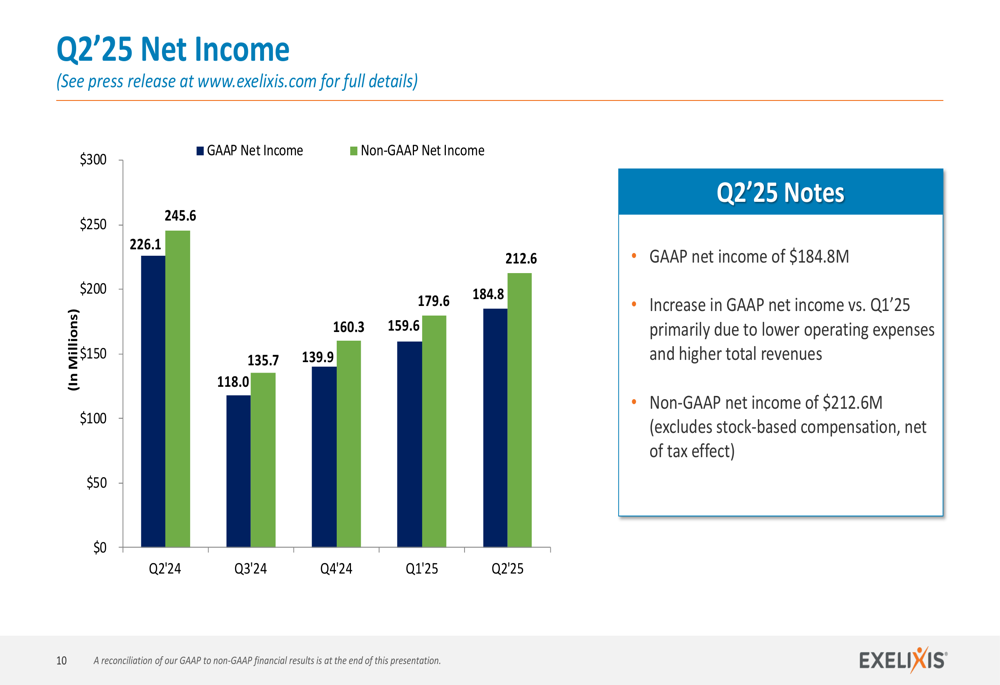

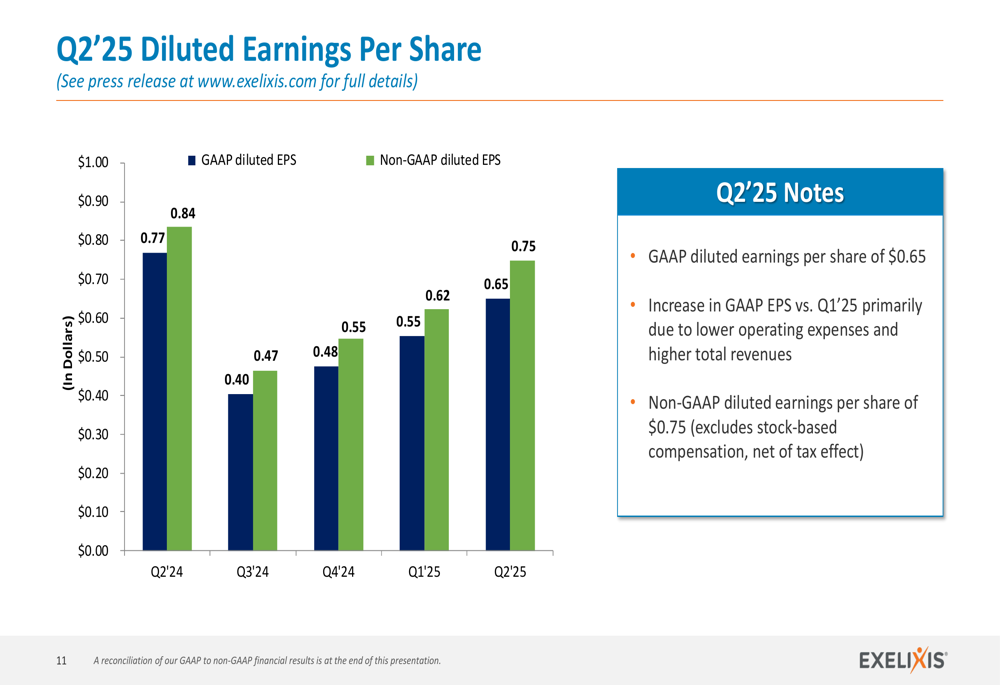

On the profitability front, Exelixis reported GAAP net income of $184.8 million ($0.65 per diluted share) and non-GAAP net income of $212.6 million ($0.75 per diluted share). While these figures represent an 18% and 13% decrease year-over-year respectively, they show a 16% and 18% improvement compared to the previous quarter.

The following chart details the company’s net income performance over the past five quarters:

Similarly, the company’s earnings per share trajectory is illustrated below:

Operating expenses showed improvement, with R&D expenses decreasing 5% year-over-year to $200.4 million and SG&A expenses increasing modestly by 2% to $134.9 million. The company maintained a strong cash position with $1.39 billion in cash and marketable securities as of June 30, 2025, despite an aggressive stock repurchase program that saw $301.8 million deployed in Q2 2025 alone.

The following comprehensive financial summary provides additional context for the company’s quarterly performance:

Strategic Initiatives

Beyond its commercial success with CABOMETYX, Exelixis continues to advance its pipeline, with particular focus on zanzalintinib, its next-generation TKI. The company reported positive topline results from the STELLAR-303 trial evaluating zanzalintinib in combination with atezolizumab in metastatic colorectal cancer (mCRC), with plans to discuss these results with regulators and potentially file a New Drug Application.

As shown in the following slide, the STELLAR-303 trial demonstrated statistically significant improvement in overall survival:

Additionally, Exelixis completed enrollment in the STELLAR-304 trial investigating zanzalintinib plus nivolumab in first-line non-clear cell RCC, with topline results expected in the first half of 2026. The company also made the strategic decision not to advance the STELLAR-305 trial in head and neck squamous cell carcinoma to phase 3 based on an evaluation of phase 2 data, emerging competition, and assessment of other potentially larger commercial opportunities.

In Q2 2025, Exelixis initiated the phase 3 STELLAR-311 pivotal study evaluating zanzalintinib versus everolimus in advanced NET patients, aiming to establish zanzalintinib as the preferred first oral therapy in NET.

The company continues to diversify its pipeline with multiple potentially best-in-class molecules, as illustrated in the following overview:

Forward-Looking Statements

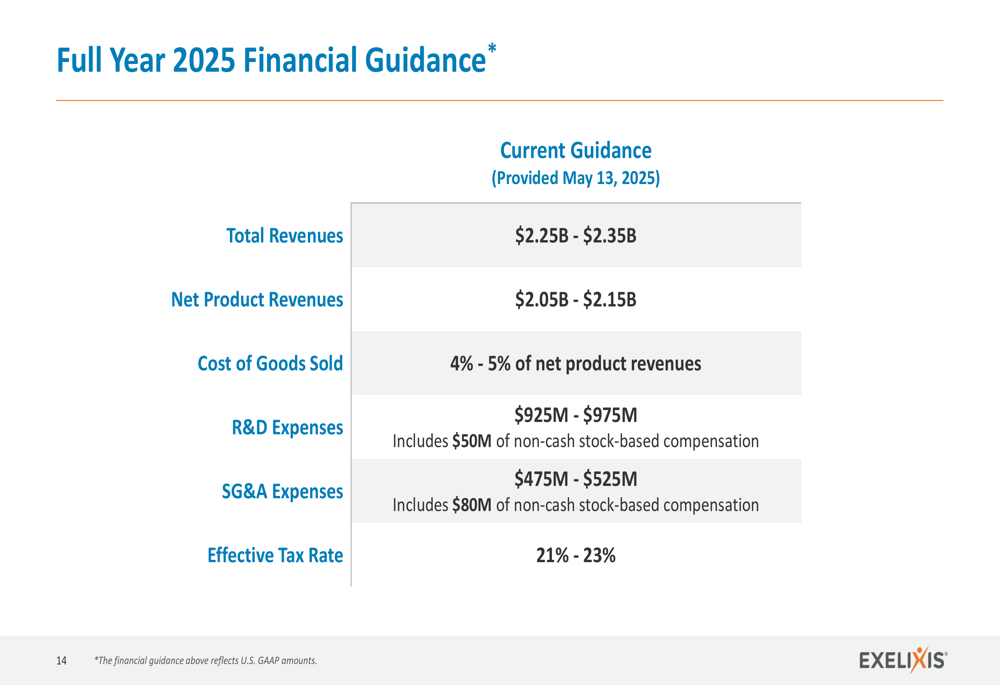

Exelixis maintained its full-year 2025 financial guidance, projecting total revenues between $2.25 billion and $2.35 billion, with net product revenues expected to range from $2.05 billion to $2.15 billion. The company anticipates R&D expenses between $925 million and $975 million and SG&A expenses between $475 million and $525 million.

The following slide details the company’s full-year 2025 financial guidance:

Looking ahead, Exelixis has outlined several key corporate objectives for 2025, including executing on business goals and maintaining strong financial performance, pursuing label expansion opportunities for CABOMETYX, advancing and expanding the zanzalintinib development program, and accelerating the development of phase 1 clinical-stage assets toward full development.

CEO Michael M. Morrissey expressed satisfaction with the company’s resilience and strategic focus during the earnings call, stating, "We work in a tough business, and I’m pleased to see our resilience and drive." He also emphasized the importance of careful pipeline development, noting, "We’re not looking to just build a big pipeline, but carefully and quickly identify the winners."

While Exelixis continues to demonstrate strong execution in its core business, investors should be mindful of potential challenges, including market saturation in key oncology segments, dependence on the success of new product launches, regulatory hurdles in expanding indications, competitive pressures from other cancer therapies, and economic factors that could impact healthcare spending.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.