Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

Four Corners Property Trust (NYSE:FCPT) released its Q1 2025 investor presentation on May 1, showcasing the company’s evolution from a Darden Restaurants (NYSE:DRI) spin-off to a diversified net lease REIT. The presentation emphasizes FCPT’s decade-long growth journey, conservative financial management, and strategic focus on recession-resistant sectors.

Despite reporting Q1 2025 earnings per share of $0.27 (missing forecasts of $0.29) and revenue of $60.7 million (below the expected $61.5 million), FCPT’s stock has shown resilience. The company’s shares closed at $27.95 on April 30, 2025, with a 0.36% gain on the day, and continued to rise 0.86% in pre-market trading on May 1.

10-Year Growth and Diversification

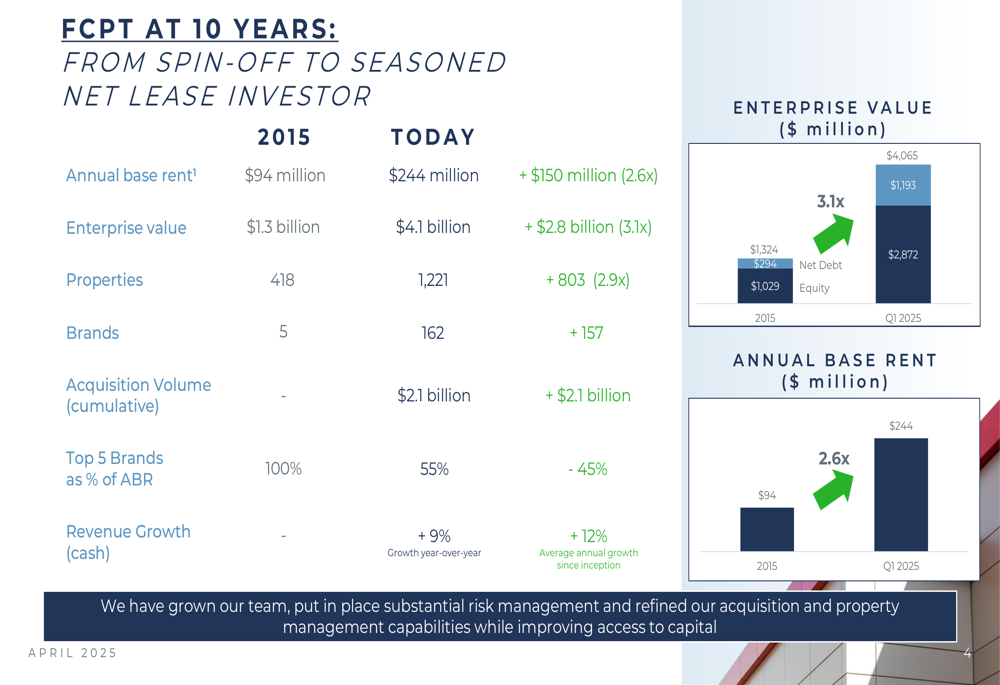

FCPT’s presentation highlights its remarkable transformation since its 2015 spin-off from Darden Restaurants. Over the past decade, the company has significantly expanded its portfolio and diversified its tenant base while maintaining strong financial metrics.

As shown in the following comprehensive growth comparison between 2015 and today:

The company has grown its annual base rent from $94 million to $244 million (a 2.6x increase) and expanded its enterprise value from $1.3 billion to $4.1 billion (a 3.1x increase). Perhaps most notably, FCPT has diversified from just 5 brands in 2015 to 162 brands today, while reducing its top 5 brand concentration from 100% to 55% of annual base rent.

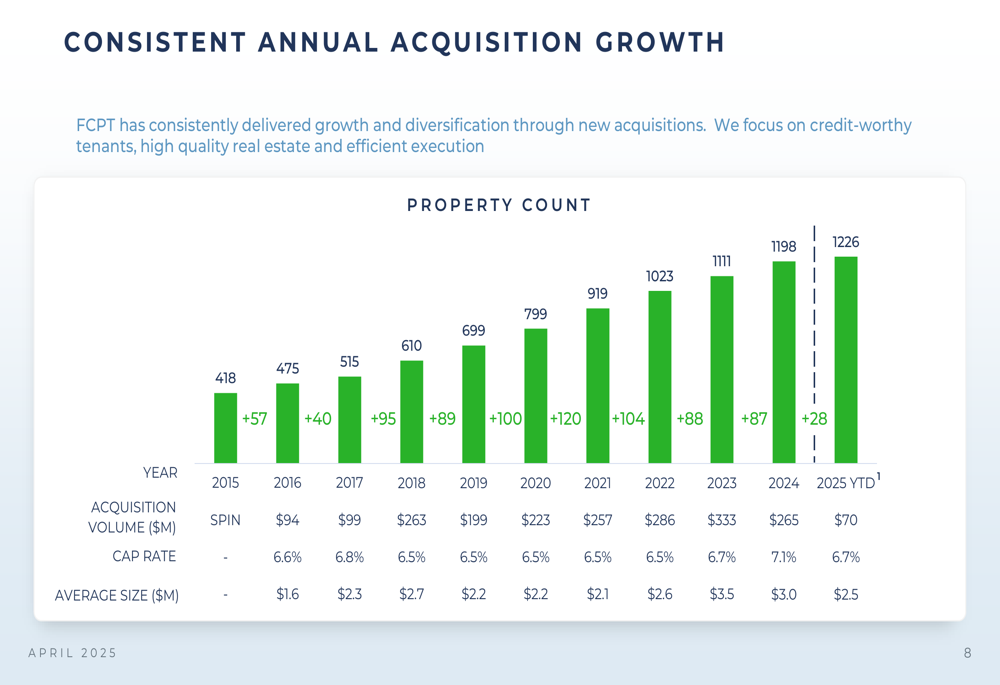

This growth has been fueled by consistent acquisition activity, with the company highlighting record acquisition volume in Q4 2024 and Q1 2025. FCPT’s presentation shows it has acquired 87 properties for $255 million at a 7.0% cap rate over the past eight months.

The following chart illustrates FCPT’s consistent acquisition growth over time:

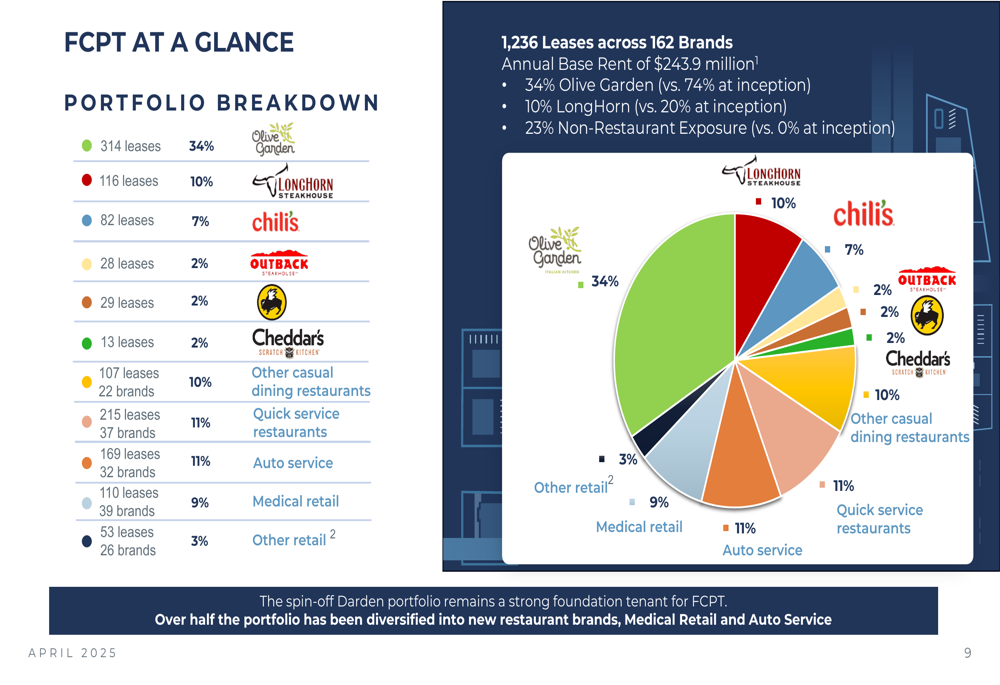

Portfolio Quality and Tenant Mix

FCPT’s portfolio now comprises 1,236 leases across 162 brands with a weighted average lease term of 7.3 years. The company maintains high occupancy (99.4%) and strong tenant EBITDAR coverage (4.9x), with 55% of tenants being investment grade.

The presentation provides a detailed breakdown of the company’s portfolio diversification:

While Olive Garden remains FCPT’s largest tenant at 34% of annual base rent (down from its initial concentration), the company has strategically diversified into other restaurant concepts, auto service centers, and medical retail properties. This diversification strategy has helped FCPT maintain high rent collections (>99% since inception) and avoid problem tenant categories that have affected some peers.

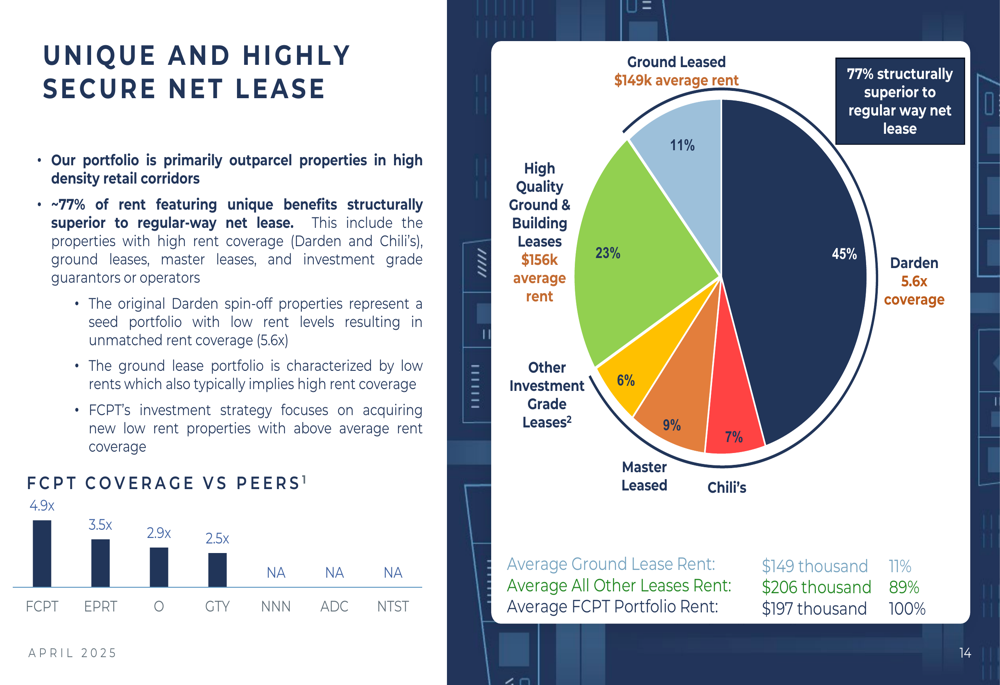

FCPT emphasizes the security of its net lease portfolio, with 77% of rent featuring structural advantages compared to typical net lease arrangements:

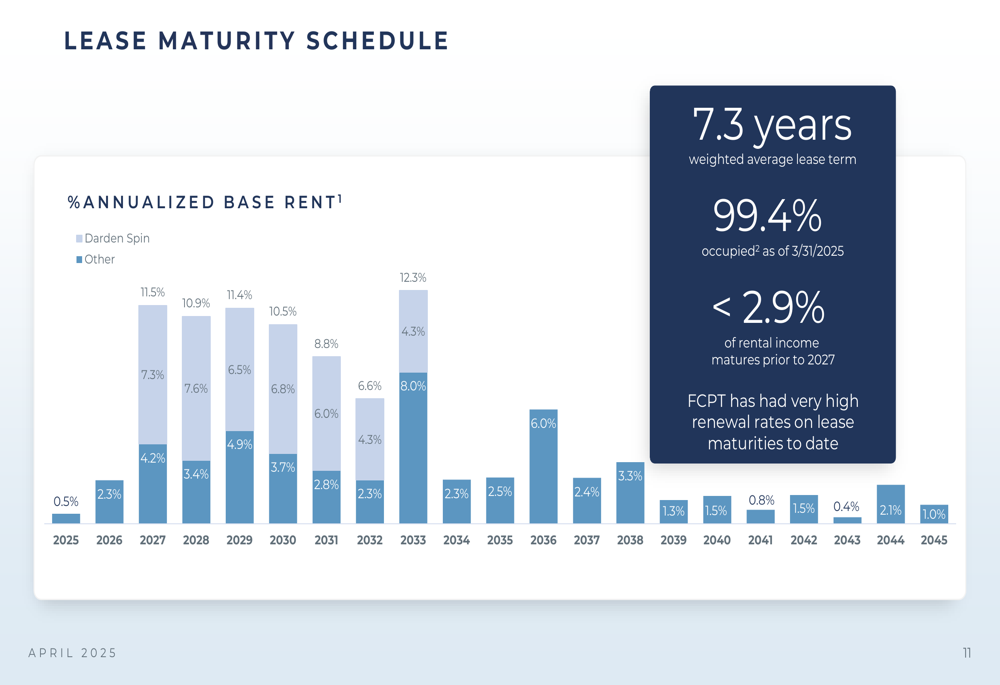

The company’s lease maturity schedule shows minimal near-term expirations, with less than 2.9% of rental income maturing prior to 2027:

Conservative Financial Position

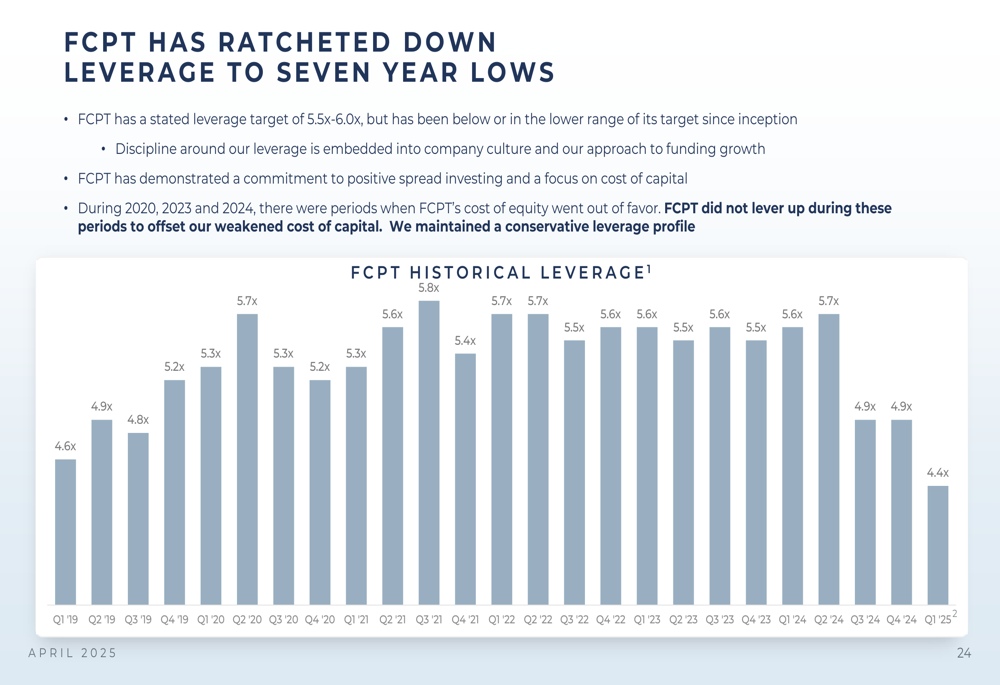

A key theme throughout the presentation is FCPT’s conservative financial management. The company has steadily reduced its leverage ratio to a seven-year low of 4.4x net debt to adjusted EBITDAre, well below its target range of 5.5x-6.0x:

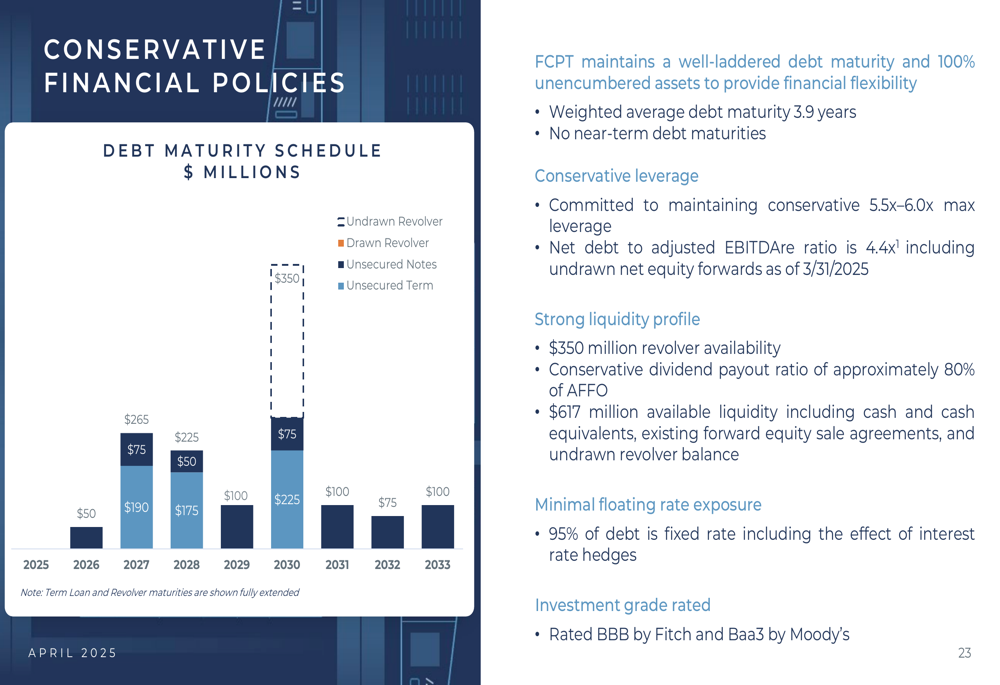

FCPT maintains a strong balance sheet with $254 million in unsettled forward equity, $350 million in undrawn revolver capacity, and a well-laddered debt maturity schedule. The company has fixed rates on 95% of its debt through Q3 2027, providing stability in the current interest rate environment:

This conservative approach has earned FCPT investment grade credit ratings of Baa3 from Moody’s and BBB from Fitch.

Acquisition Strategy and Future Outlook

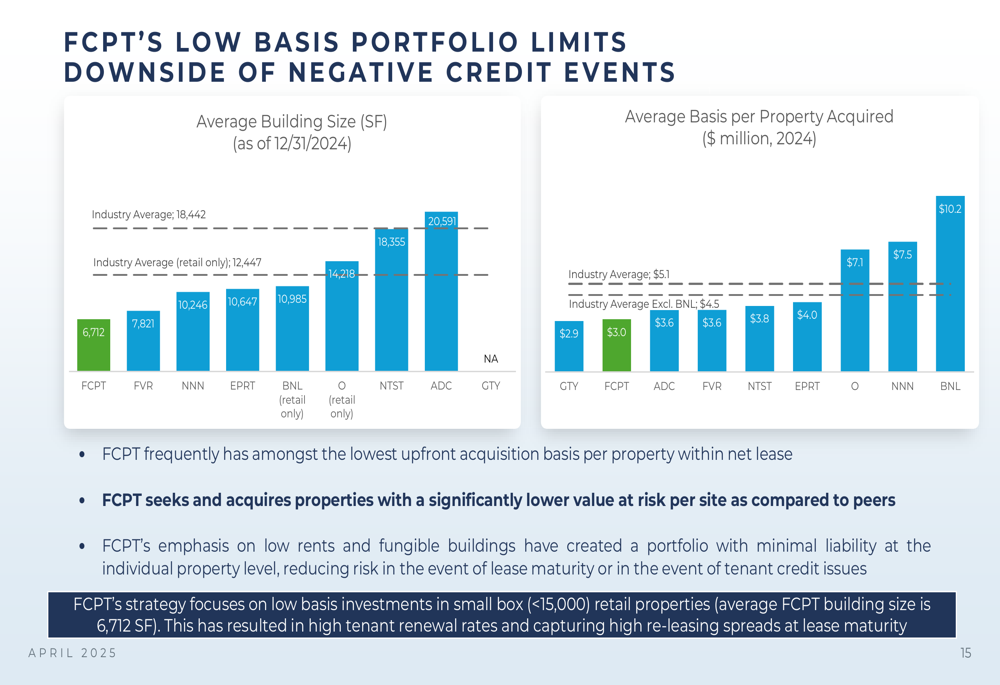

FCPT’s presentation outlines its selective approach to net lease investing, focusing on recession-resistant sectors while avoiding higher-risk categories. The company emphasizes its "low basis" strategy, with an average property acquisition cost of approximately $3 million, which limits downside risk compared to peers:

The company specifically targets restaurants (currently 77% of annual base rent), auto service centers (11%), and medical retail (9%), while avoiding sectors like pharmacies, entertainment venues, gyms, furniture stores, and car washes.

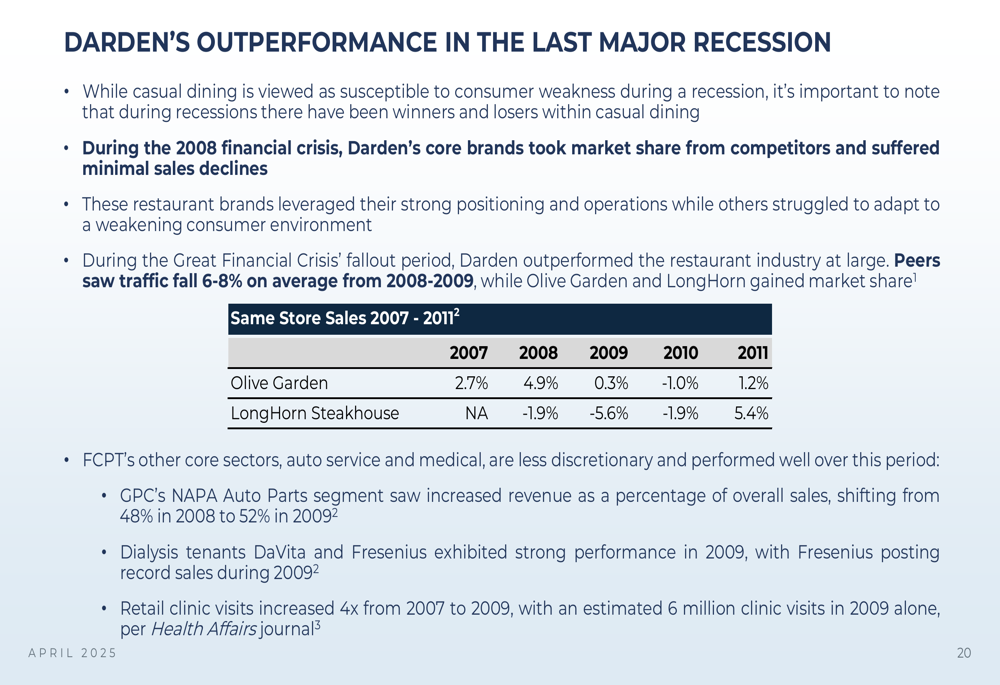

FCPT highlights the recession resistance of its portfolio, particularly its Darden-leased properties, which outperformed during the last major economic downturn:

Looking forward, FCPT appears well-positioned for continued growth with its substantial liquidity ($254 million in unsettled forward equity plus $350 million in revolver capacity) and disciplined acquisition approach. According to the earnings call, the company has $250-$350 million available for acquisitions and plans to maintain a similar sector mix in its investment strategy.

CEO Bill Lenahan emphasized the company’s strong rent coverage in the earnings call, stating, "Our rent coverage in the fourth quarter was 4.9 times for the majority of our portfolio," which aligns with the figure presented in the Q1 2025 slides.

With its decade-long track record of growth, diversified portfolio of recession-resistant tenants, and conservative financial management, FCPT presents itself as a "calm port in the volatility storm" for net lease REIT investors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.