Uxin shares drop 45% as predicted by InvestingPro’s Fair Value model

Introduction & Market Context

Ferroglobe PLC (NASDAQ:GSM) released its third quarter 2025 results on November 6, revealing a challenging period marked by soft demand and continued pressure from low-priced imports, particularly from China. The specialty metals producer reported a 19% sequential decline in revenue to $311.7 million, though the company maintained positive adjusted EBITDA and generated free cash flow despite the headwinds.

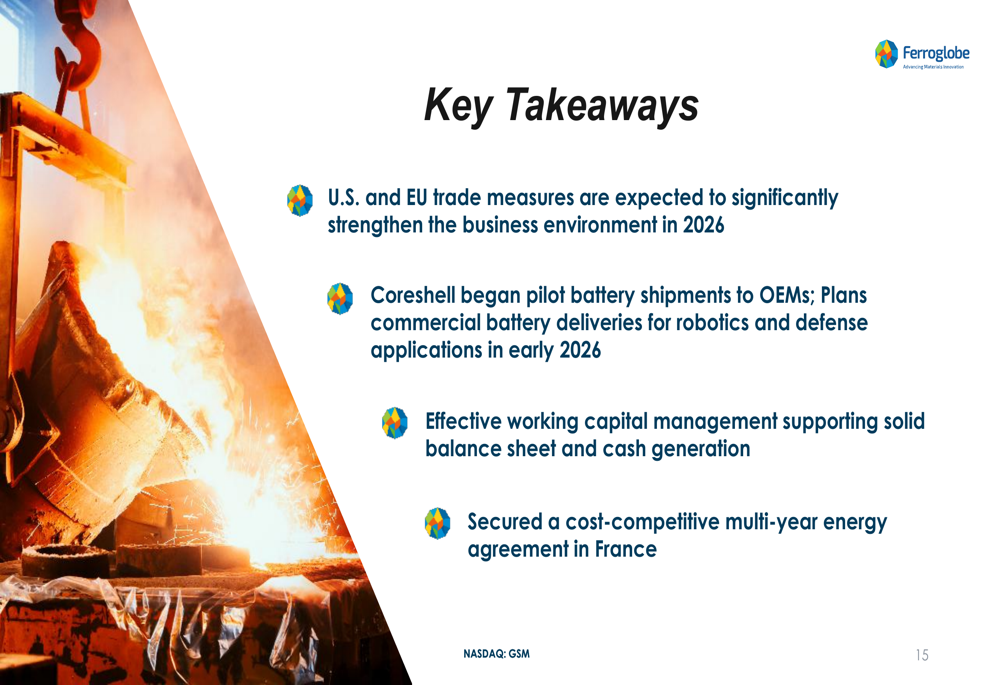

Management expressed optimism about future market conditions, highlighting favorable preliminary trade case decisions in the U.S. and anticipated measures in the European Union that are expected to significantly strengthen the business environment in 2026.

Quarterly Performance Highlights

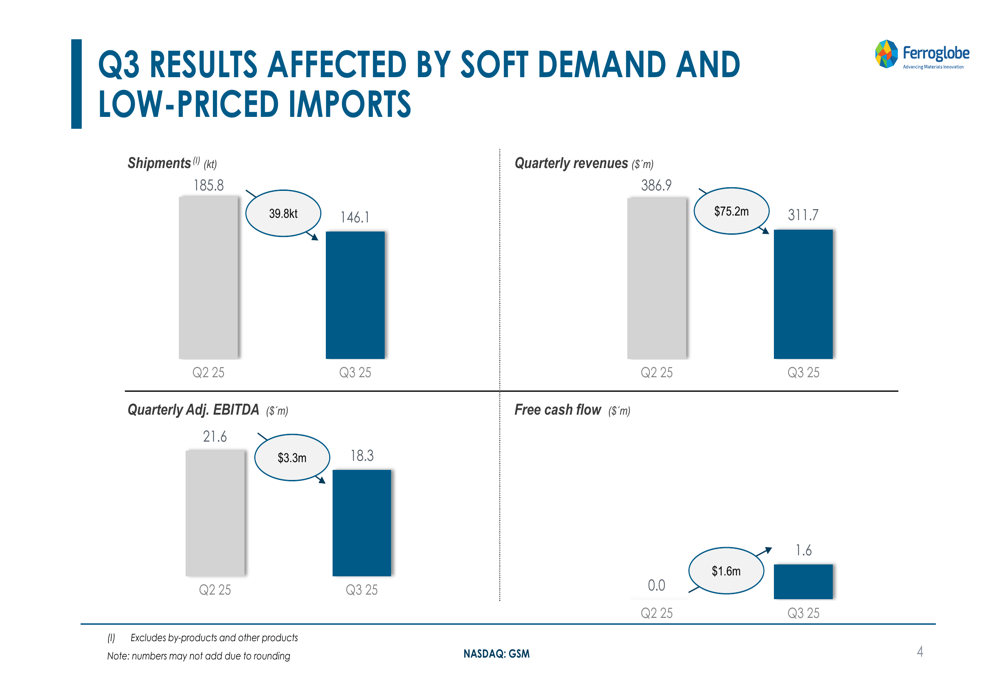

Ferroglobe's Q3 2025 results reflected the impact of challenging market conditions, with shipments declining to 146.1kt from 185.8kt in the previous quarter. Revenue fell to $311.7 million from $386.9 million in Q2, while adjusted EBITDA decreased to $18.3 million from $21.6 million. Despite these declines, the company's adjusted EBITDA margin improved slightly to 5.9% from 5.6% in the previous quarter.

As shown in the following chart of Ferroglobe's Q3 2025 financial performance:

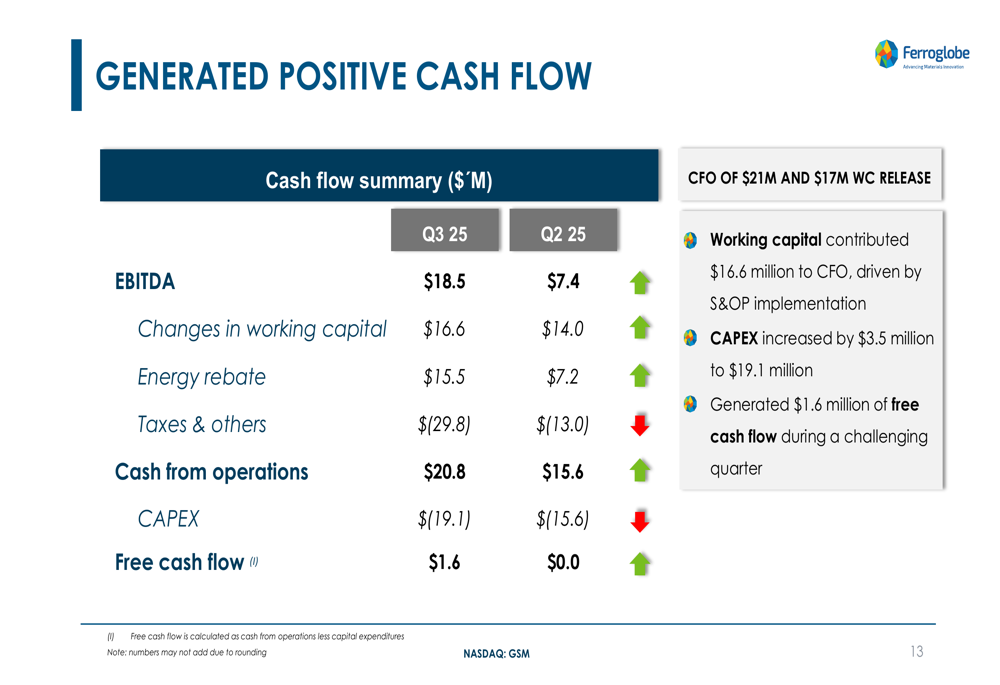

The company managed to generate positive free cash flow of $1.6 million, an improvement from breakeven in Q2 2025. This was achieved through effective working capital management, which contributed $16.6 million to operating cash flow.

Segment Performance

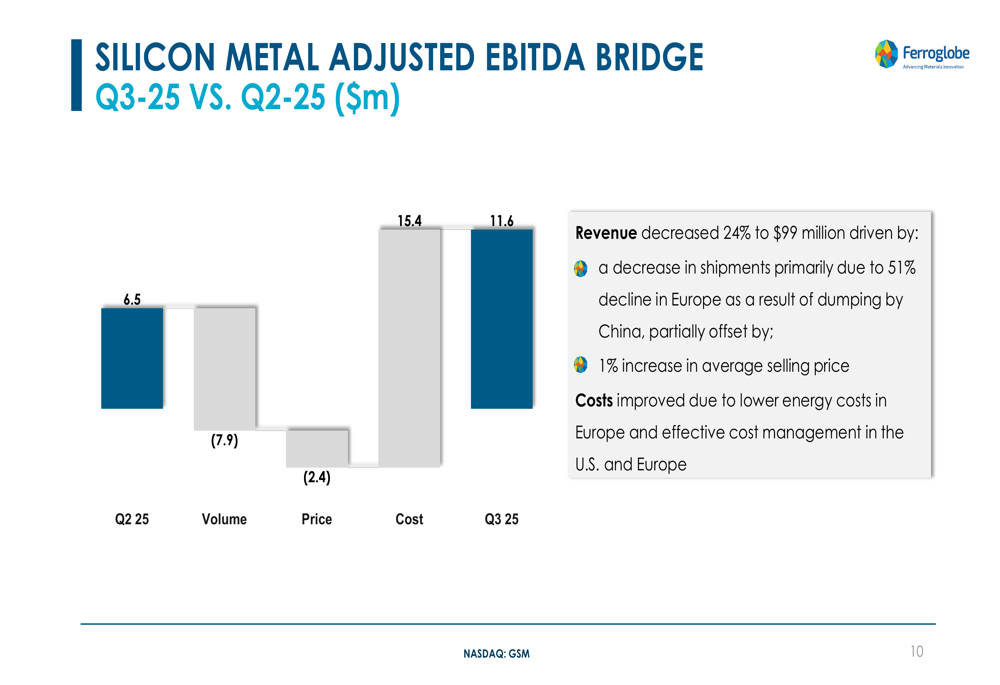

Silicon Metal, the company's largest segment by revenue, saw volumes decline by 25% quarter-over-quarter, primarily due to a 51% decrease in European shipments attributed to Chinese dumping. Despite this, the segment's adjusted EBITDA improved to $11.6 million from $6.5 million in Q2, benefiting from lower energy costs in Europe and effective cost management.

The following chart illustrates the Silicon Metal segment's adjusted EBITDA bridge:

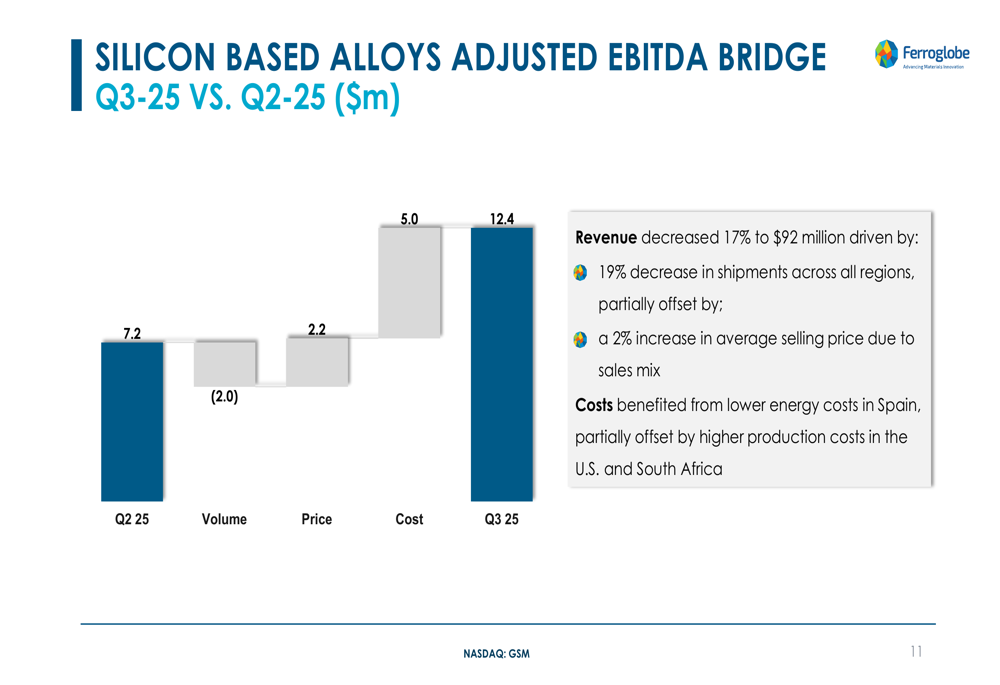

Silicon-based alloys experienced a 19% decrease in shipments across all regions, with revenue declining 17% to $92 million. However, adjusted EBITDA for this segment increased to $12.4 million from $7.2 million in Q2, supported by a 2% increase in average selling price and lower energy costs in Spain.

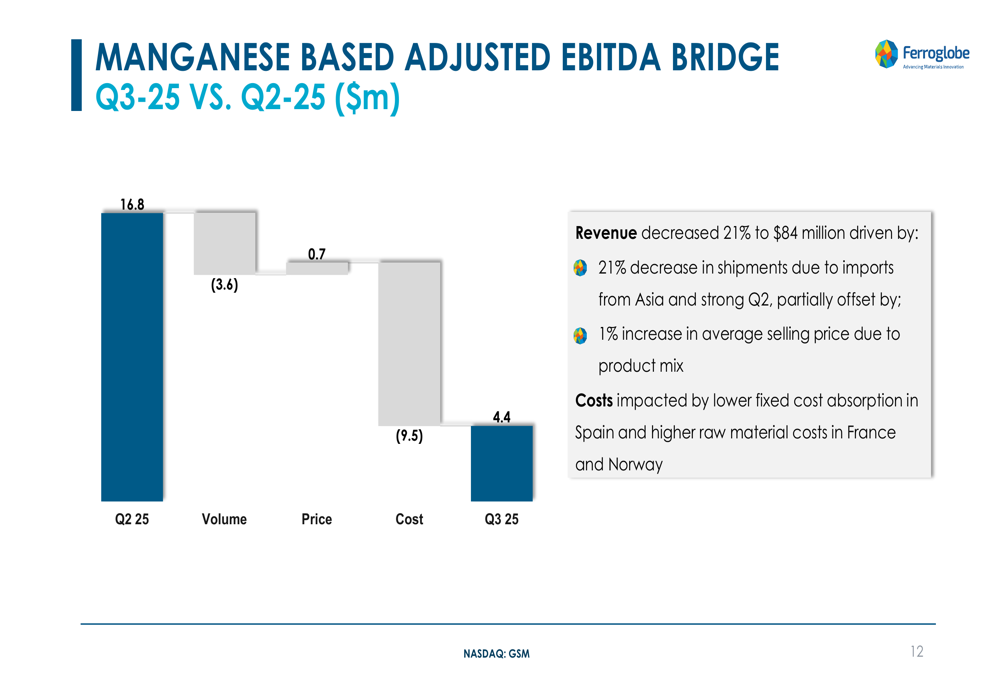

Manganese-based alloys faced the most significant challenges, with adjusted EBITDA declining to $4.4 million from $16.8 million in the previous quarter. This segment was impacted by a 21% decrease in shipments due to increased imports from Asia and higher raw material costs in France and Norway.

Cash Flow and Balance Sheet

Despite the challenging market environment, Ferroglobe generated positive operating cash flow of $20.8 million in Q3 2025, supported by effective working capital management and energy rebates. Capital expenditures increased to $19.1 million, resulting in free cash flow of $1.6 million for the quarter.

The following chart details the company's cash flow performance:

Ferroglobe maintained a solid balance sheet with a net debt position of approximately $16 million. The company continued its dividend program, distributing $2.6 million to shareholders in Q3.

Market Challenges and Trade Developments

A key focus of Ferroglobe's presentation was the impact of low-priced imports on market conditions, particularly in Europe, and the potential relief expected from trade measures.

The company highlighted positive developments in U.S. trade cases, including preliminary countervailing duties ranging from 17% to 240% on silicon metal imports and anti-dumping duties on imports from Angola (68%) and Laos (94%). Additional decisions regarding Australia and Norway are expected before year-end.

As shown in the following slide detailing these trade developments:

European Union trade measures are anticipated by November 18, which management expects will help stabilize the market. The company projects these trade actions will significantly improve the business environment in 2026.

Strategic Initiatives

Ferroglobe reported progress on key strategic initiatives that position the company for future growth. The partnership with Coreshell for silicon anode technology is advancing, with pilot batteries being delivered to OEMs and plans for commercial battery deliveries for robotics and defense applications in early 2026.

The company also secured a competitive multi-year energy agreement for its French operations, providing flexibility to produce 12 months a year, which is expected to enhance operational efficiency and cost competitiveness.

Forward-Looking Statements

Management expressed optimism about market conditions improving in 2026, driven by anticipated trade measures in both the U.S. and EU. The company's key takeaways emphasized these expected benefits along with the strategic positioning of its Coreshell partnership and energy agreements.

As illustrated in the following summary slide:

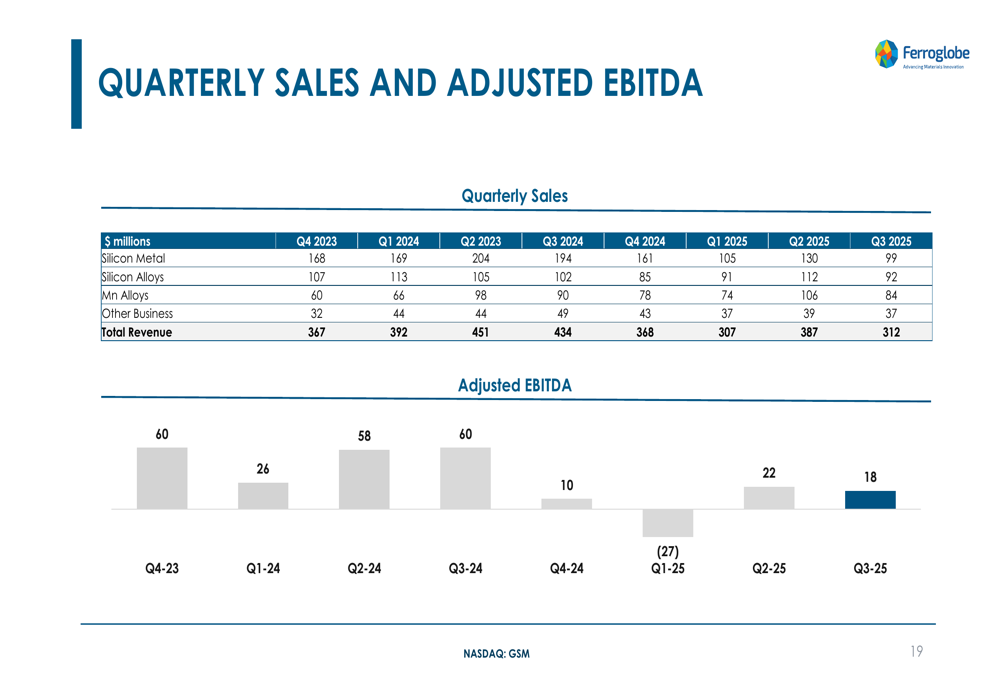

The historical context of Ferroglobe's quarterly performance shows the volatility the company has experienced over the past two years, with adjusted EBITDA fluctuating significantly:

Executive Commentary

While specific executive quotes were not provided in the presentation materials, the company's messaging emphasized resilience in a challenging environment and strategic positioning for future improvement. The presentation highlighted effective cost management and working capital optimization as key factors in maintaining profitability despite market headwinds.

According to the earnings call transcript, CEO Marco Levi expressed optimism about future trade measures, stating, "We expect trade measures in the U.S. and the EU to improve the business environment significantly in 2026." CFO Beatriz García-Cos noted the company's belief that its share price remains undervalued.

Conclusion

Ferroglobe's Q3 2025 presentation revealed a company navigating significant market challenges while maintaining profitability and generating positive cash flow. While revenue and volumes declined across all segments, effective cost management and working capital optimization helped sustain adjusted EBITDA margins.

The company's outlook hinges significantly on anticipated trade measures expected to improve market conditions in 2026, along with strategic initiatives including the Coreshell partnership and energy agreements. Investors will be watching closely to see if these factors deliver the improved business environment that management anticipates.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.