Intel stock extends gains after report of possible U.S. government stake

Introduction & Market Context

Festi hf (ICE:FESTI) presented its Q1 2025 financial results on April 30, showcasing strong performance across most of its business segments despite mixed economic conditions in Iceland. The company reported significant growth in revenue and profitability as consumer spending remained resilient, with the salary index rising 6.9% over the last twelve months while the consumer price index increased by 3.8%.

The presentation, delivered by CEO Ásta S. Fjeldsted and CFO Magnús Kr. Ingason, highlighted how Festi’s diversified portfolio of retail, pharmacy, fuel, and real estate businesses has continued to expand market share while improving operational efficiency. The company’s stock closed at ISK 301 on April 29, 2025, down 0.33% ahead of the earnings announcement, trading within its 52-week range of ISK 185-318.

Quarterly Performance Highlights

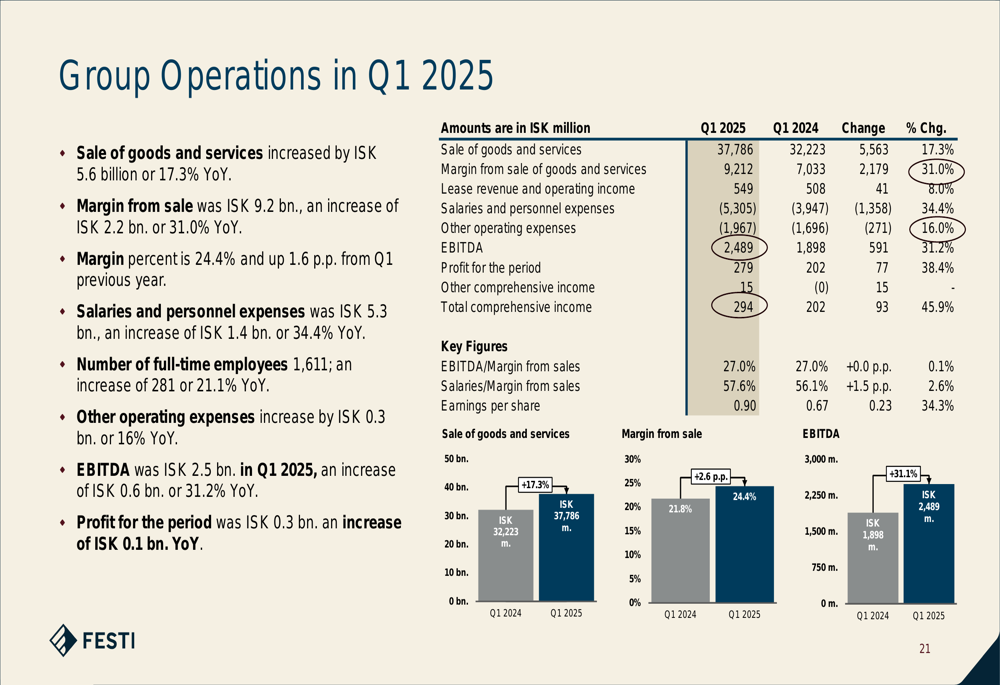

Festi reported impressive financial results for Q1 2025, with sale of goods and services reaching ISK 37.8 billion, representing a 17.3% year-over-year increase. The company’s EBITDA grew by 31.2% to ISK 2,489 million, while profit for the period increased by 38.4% to ISK 279 million.

As shown in the following consolidated highlights chart, Festi has demonstrated consistent growth across key metrics over the past four years:

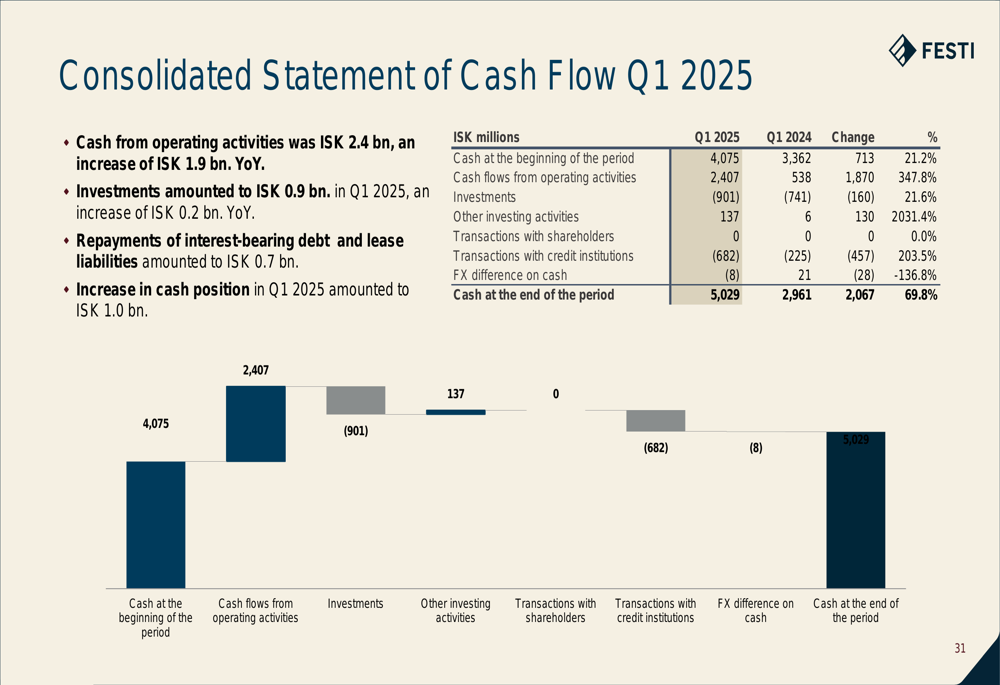

The company’s gross margin improved to 24.4%, up 2.6 percentage points from the previous year. This margin expansion, coupled with a 347.8% increase in cash from operating activities to ISK 2,407 million, reflects Festi’s enhanced operational efficiency and stronger cash generation capabilities.

Customer engagement metrics were equally impressive, with the number of customer transactions increasing by 10.2% and items sold rising by 6.9% compared to Q1 2024. Domestic card turnover grew by 14.4%, while foreign card turnover saw a modest 0.5% increase.

Detailed Financial Analysis

The financial overview for Q1 2025 reveals strong performance across most income statement categories. The 17.3% increase in sales was accompanied by a 31.0% rise in gross margin to ISK 9,212 million. While salaries and personnel expenses increased by 34.4% to ISK 5,305 million, the company still managed to improve its overall profitability.

The following chart provides a comprehensive breakdown of the group’s financial performance:

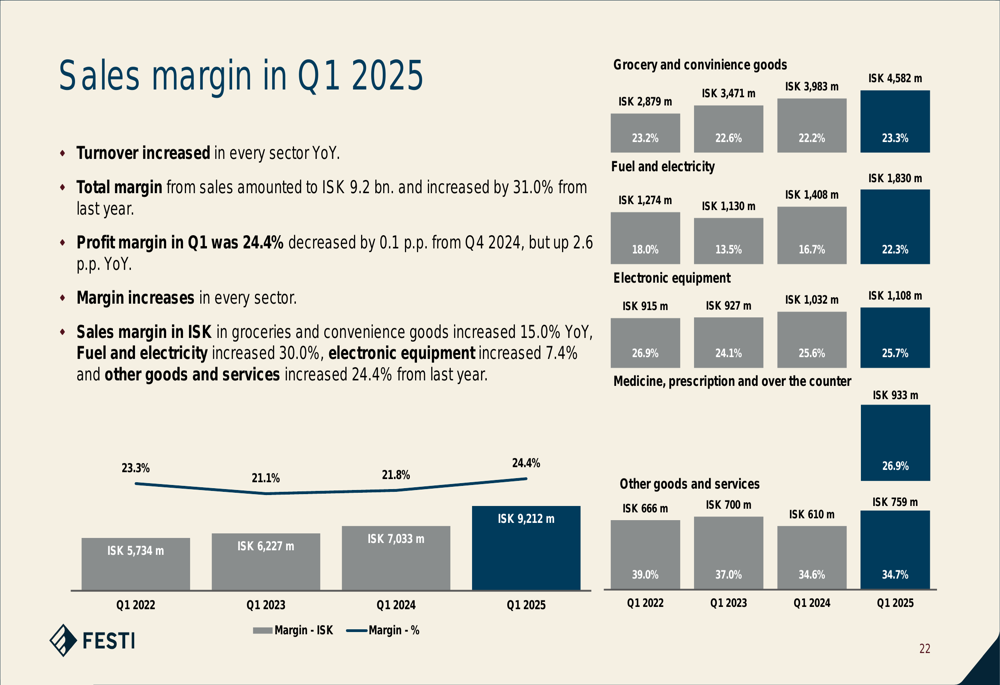

Sales margin analysis by product category shows varying levels of profitability across Festi’s diverse business lines. Medicine (26.9%) and electronic equipment (25.7%) delivered the highest margins, followed by grocery and convenience goods (23.3%), fuel and electricity (22.3%), and other goods and services (34.7%).

The margin trends by category are illustrated in the following chart:

The company’s balance sheet remains solid, with total assets increasing by ISK 0.4 billion from year-end 2024. Cash flow from operations showed remarkable improvement, as illustrated in the consolidated statement of cash flow:

Subsidiary Performance

Festi’s subsidiaries delivered mixed results, with most showing revenue growth but varying EBITDA performance:

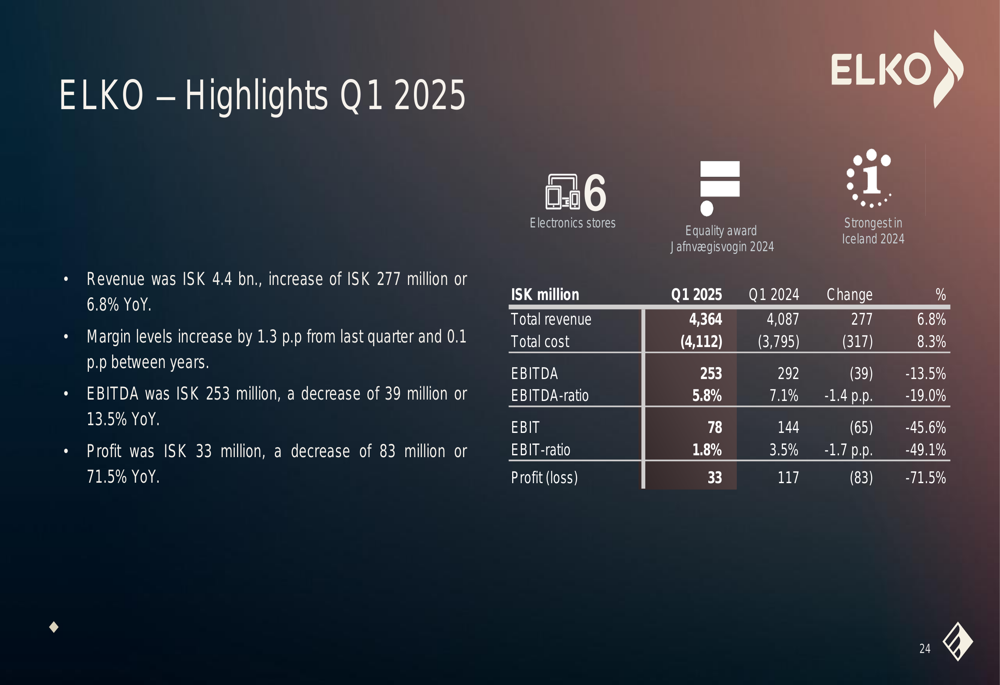

ELKO, Iceland’s largest electronics retailer, reported revenue of ISK 4,364 million, up 6.8% year-over-year, though EBITDA declined by 13.5% to ISK 253 million. The company strengthened its market position with turnover growing at triple the market rate, while e-commerce share rose to 27.1%.

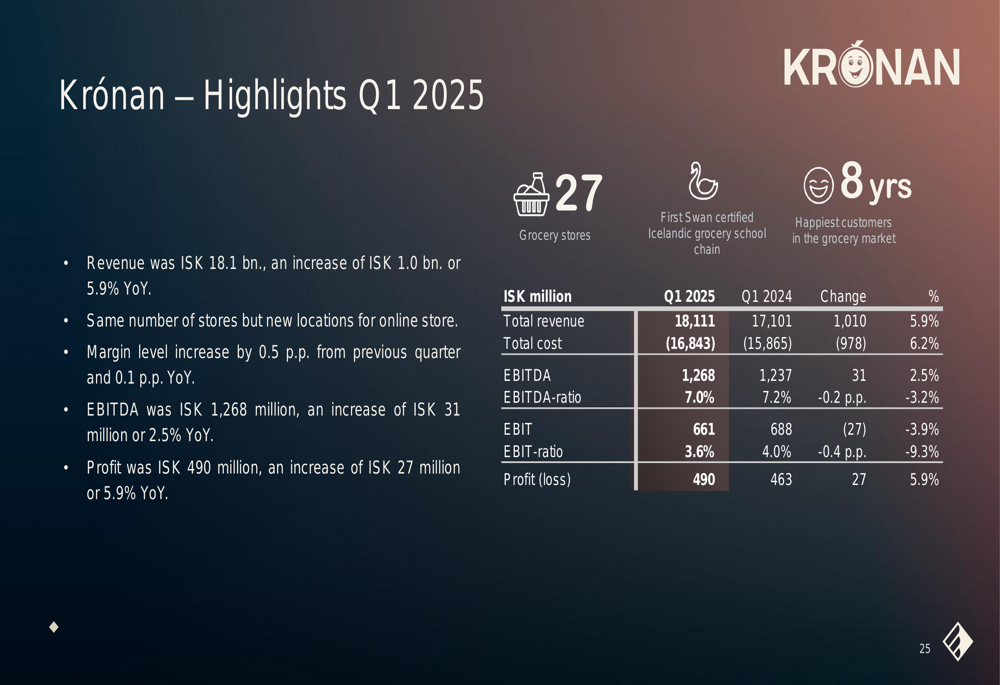

Krónan, Festi’s low-cost grocery chain, delivered solid results with revenue increasing by 5.9% to ISK 18,111 million and EBITDA growing by 2.5% to ISK 1,268 million. The chain saw nearly 5% more transactions and over 3% more units sold compared to Q1 2024.

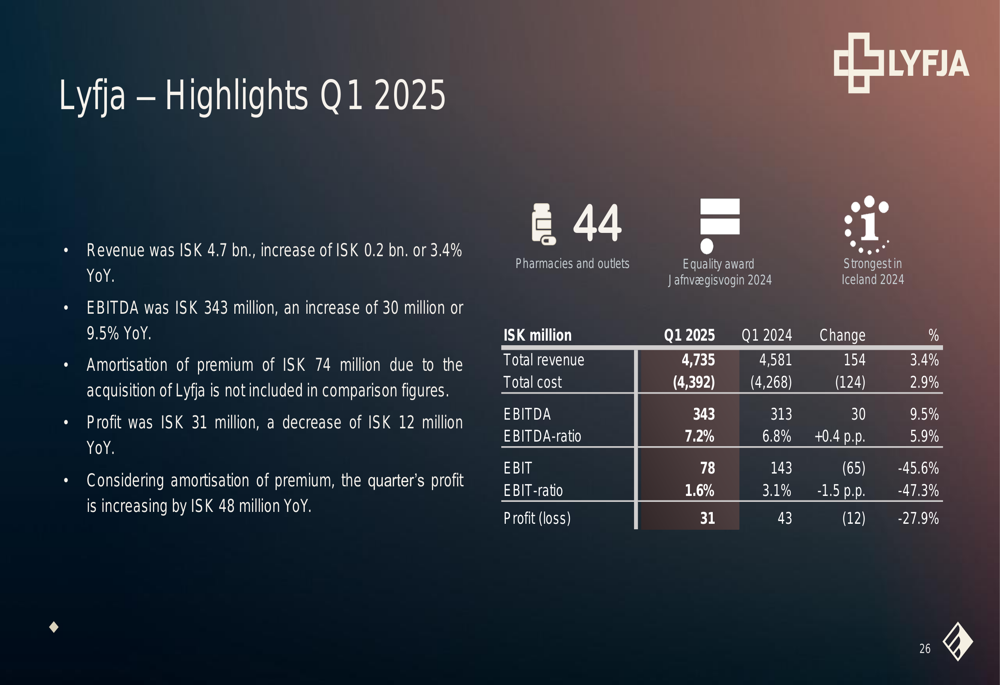

Lyfja, the pharmacy chain, achieved revenue growth of 3.4% to ISK 4,735 million and EBITDA growth of 9.5% to ISK 343 million. The Lyfja app was named App of the Year and recorded its highest monthly turnover ever in March.

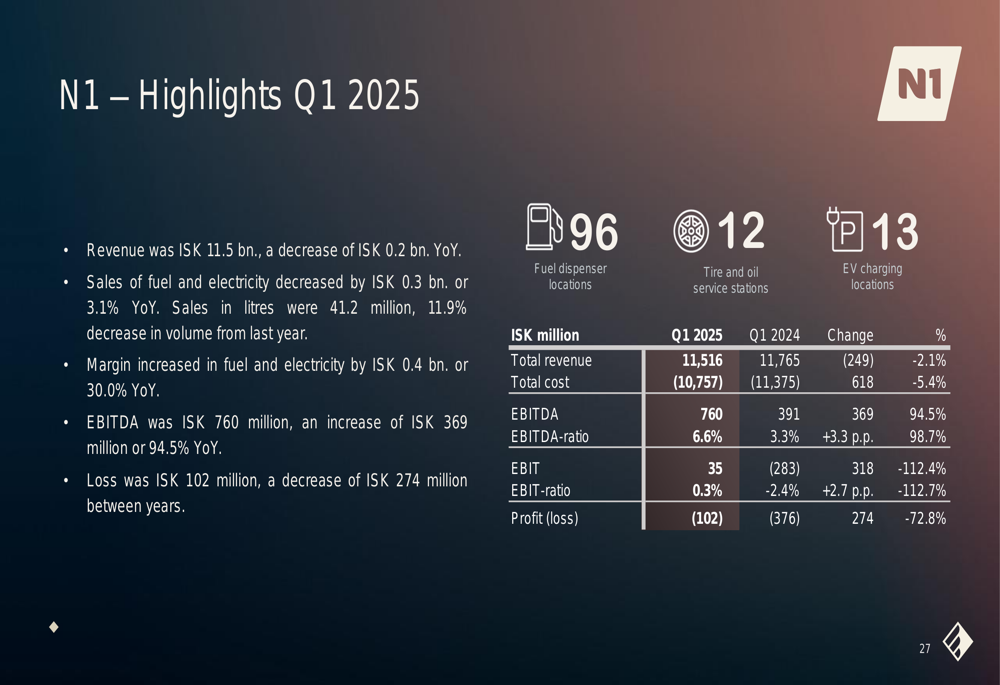

N1, Festi’s fuel and service station network, experienced a 2.1% revenue decline to ISK 11,516 million but saw EBITDA surge by 94.5% to ISK 760 million. The company strengthened its position in the car wash market and expanded its EV charging infrastructure.

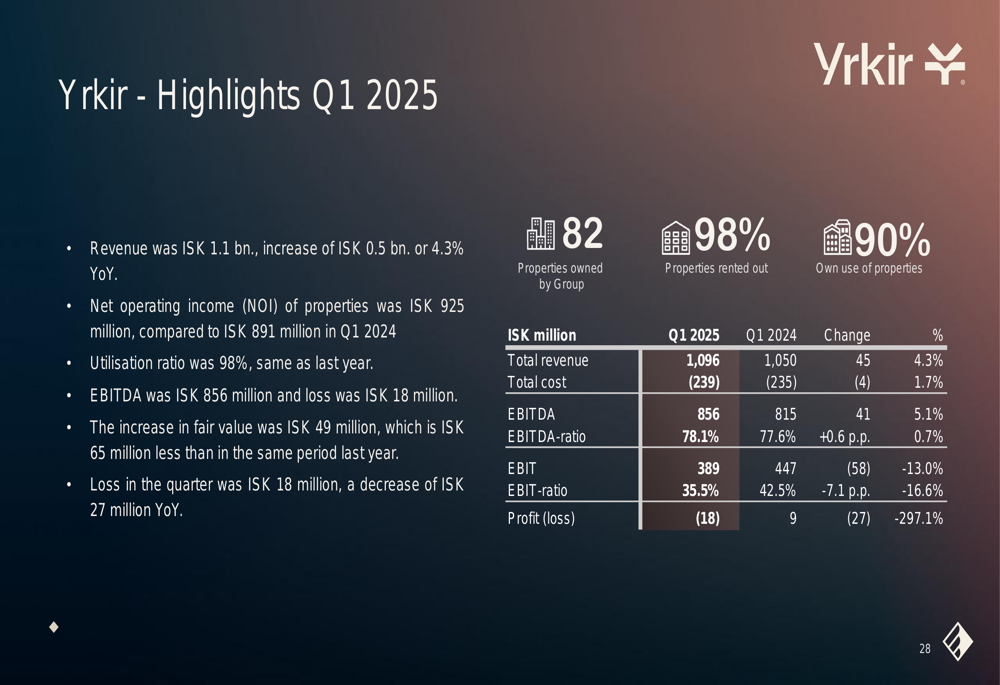

Yrkir, responsible for managing the Group’s real estate, reported revenue growth of 4.3% to ISK 1,096 million and EBITDA growth of 5.1% to ISK 856 million.

Strategic Initiatives

Festi highlighted several strategic initiatives across its subsidiaries aimed at enhancing market position and driving future growth:

Yrkir acquired a strategic location in Hafnarfjörður for ISK 475 million and is preparing a new multi-energy N1 station at Fiskislóð, with fuel pumps operational from May 1.

ELKO continues to strengthen its e-commerce presence, with online sales reaching 27.1% of total revenue, up from 24.7% year-over-year. The company is also focusing on private label products, which increased from 3.1% to 4.3% of sales.

Krónan is expanding its coverage in rural areas and developing B2B services. The chain is also upgrading existing stores, with a full refurbishment of the Vallakór location underway. Online sales grew by over 24% year-over-year in Q1.

Lyfja is diversifying beyond traditional pharmacy services, introducing AI-powered eye screening and expanding its hearing services, with appointments for hearing tests increasing by 58% month-on-month.

N1 is strengthening its position in the car wash market and enhancing its EV charging infrastructure, with 12 new Tesla (NASDAQ:TSLA) Superchargers installed during the quarter. The company plans to establish a centralized tire hotel and workshop in 2026.

Forward-Looking Statements

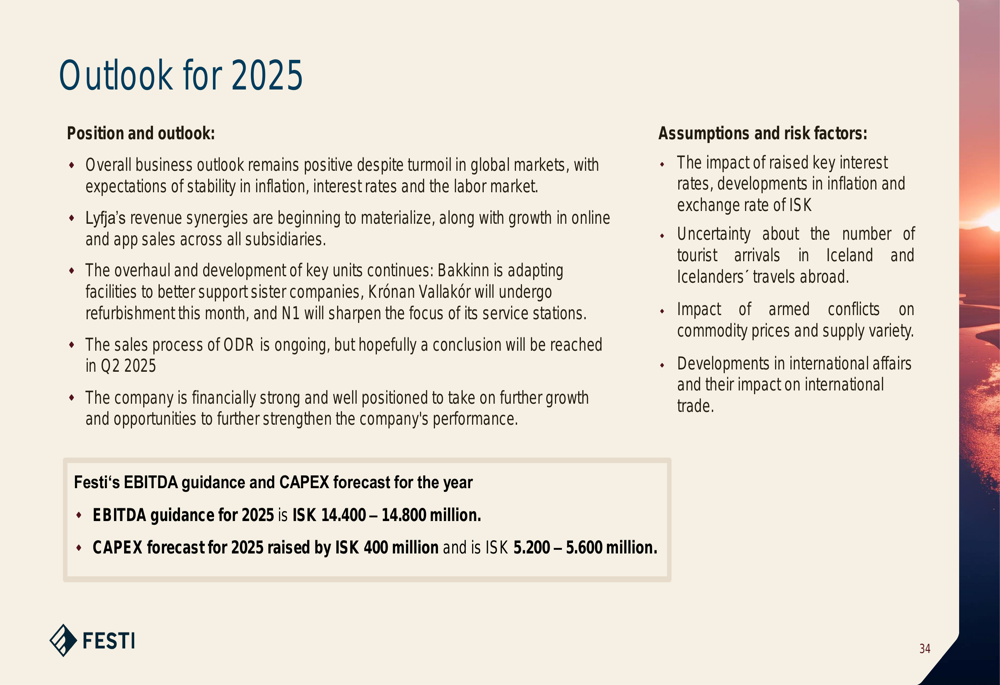

Looking ahead to the remainder of 2025, Festi provided guidance for full-year EBITDA between ISK 14,400-14,800 million and CAPEX between ISK 5,200-5,600 million. The outlook is based on assumptions of continued economic stability and consumer spending growth.

The company’s forward-looking guidance is summarized in the following chart:

Management highlighted that while the overall economic environment remains favorable, potential risks include fluctuations in fuel prices, currency exchange rates, and interest rates. The company’s diversified business model and strategic initiatives are expected to mitigate these risks and support continued growth across its various subsidiaries.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.