Fannie Mae, Freddie Mac shares tumble after conservatorship comments

Introduction & Market Context

FibroGen Inc . (NASDAQ:FGEN) presented its first quarter 2025 financial results on May 12, highlighting a strategic transformation focused on pipeline development and operational streamlining despite significant revenue challenges. The company’s stock, currently trading at $0.302 per share, remains near its 52-week low of $0.18 and far from its high of $1.53, reflecting ongoing investor concerns about its financial position.

The presentation emphasized FibroGen’s strategic pivot, centered on the divestment of its China operations and advancement of key pipeline assets in oncology and anemia treatment. This comes as the company reported a steep 89% year-over-year revenue decline, though management pointed to reduced losses and extended cash runway as positive developments.

Quarterly Performance Highlights

FibroGen reported Q1 2025 revenue of $2.7 million, down dramatically from $25.4 million in the same period last year. Despite this revenue contraction, the company managed to reduce its net loss to $16.8 million ($0.16 per share), a significant improvement from the $49 million ($0.49 per share) loss recorded in Q1 2024.

This financial improvement was largely driven by aggressive cost-cutting measures, with operating expenses decreasing by 76% year-over-year to $17.7 million. Research and development expenses saw a similar reduction, falling 75% to $9.2 million. The company reported a cash position of $128.4 million total, with $33.8 million held in the United States.

For the full year 2025, management projects revenue between $4 million and $8 million, reflecting the challenging near-term revenue environment as the company transitions its business model.

Strategic Initiatives

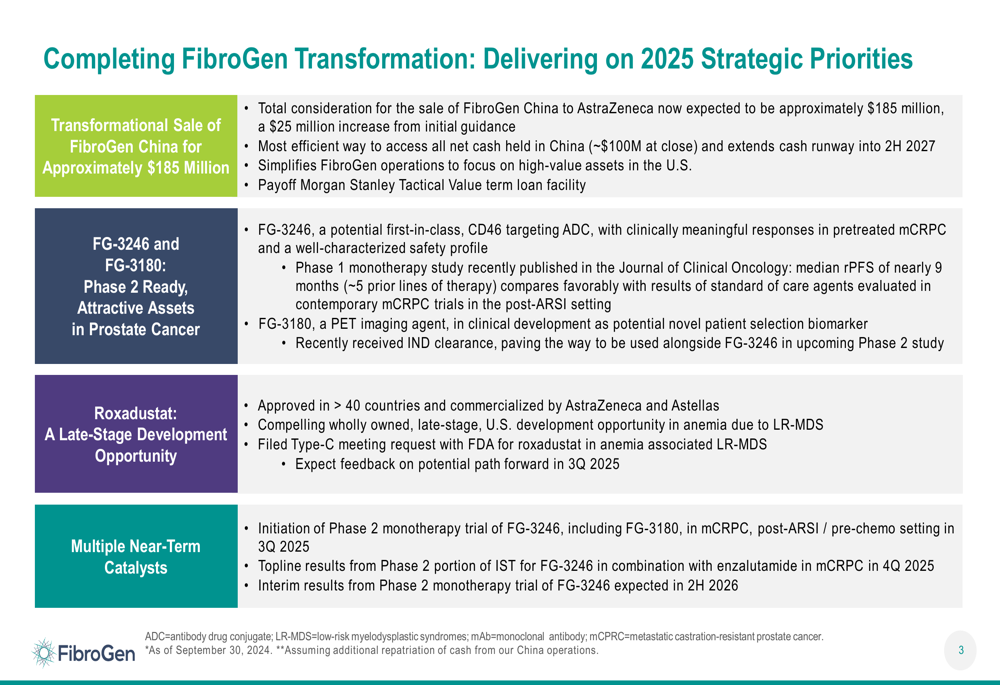

The cornerstone of FibroGen’s transformation strategy is the sale of its China operations, which the company presented as a transformational move to extend its cash runway and simplify operations.

As shown in the following slide detailing the transaction terms:

The deal, valued at $85 million in enterprise value plus approximately $100 million in FibroGen net cash held in China, is expected to close in Q3 2025. Management emphasized that proceeds will be used to pay off the Morgan Stanley (NYSE:MS) Tactical Value term loan facility and extend the company’s cash runway into the second half of 2027.

This strategic divestment aligns with FibroGen’s broader transformation, as outlined in its 2025 priorities:

Pipeline Development & Clinical Progress

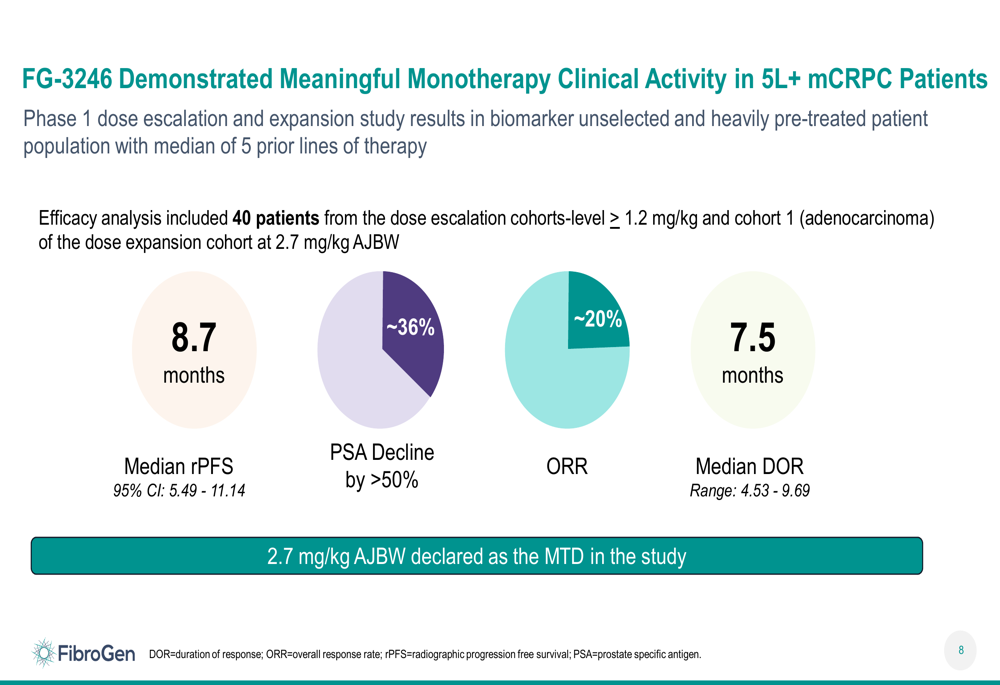

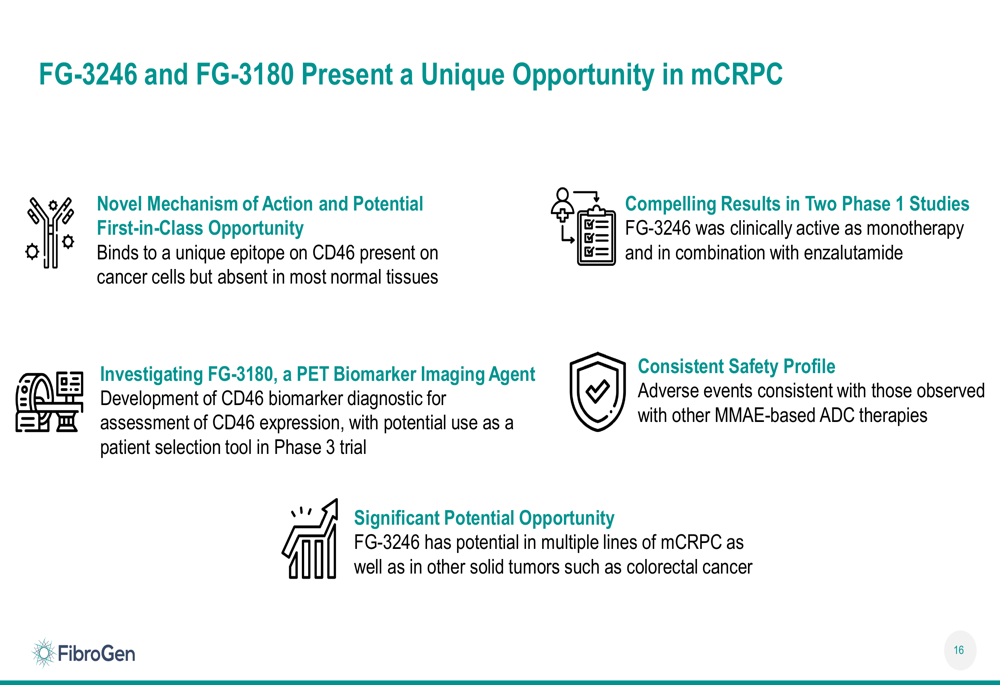

FibroGen’s presentation heavily emphasized its pipeline assets, particularly FG-3246, a potential first-in-class CD46-targeting antibody-drug conjugate (ADC) for metastatic castration-resistant prostate cancer (mCRPC).

The company highlighted promising clinical data from a Phase 1 study of FG-3246, demonstrating meaningful monotherapy activity in heavily pre-treated patients:

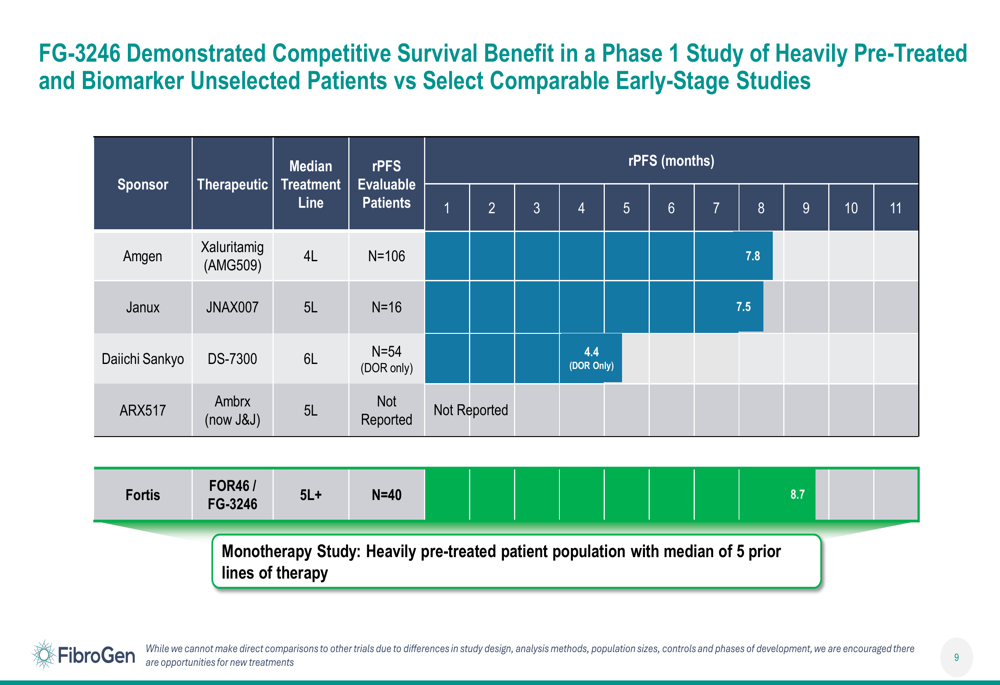

FibroGen positioned these results as competitive when compared to other therapies in development, emphasizing the 8.7-month median radiographic progression-free survival (rPFS) achieved in patients who had received five or more prior lines of therapy:

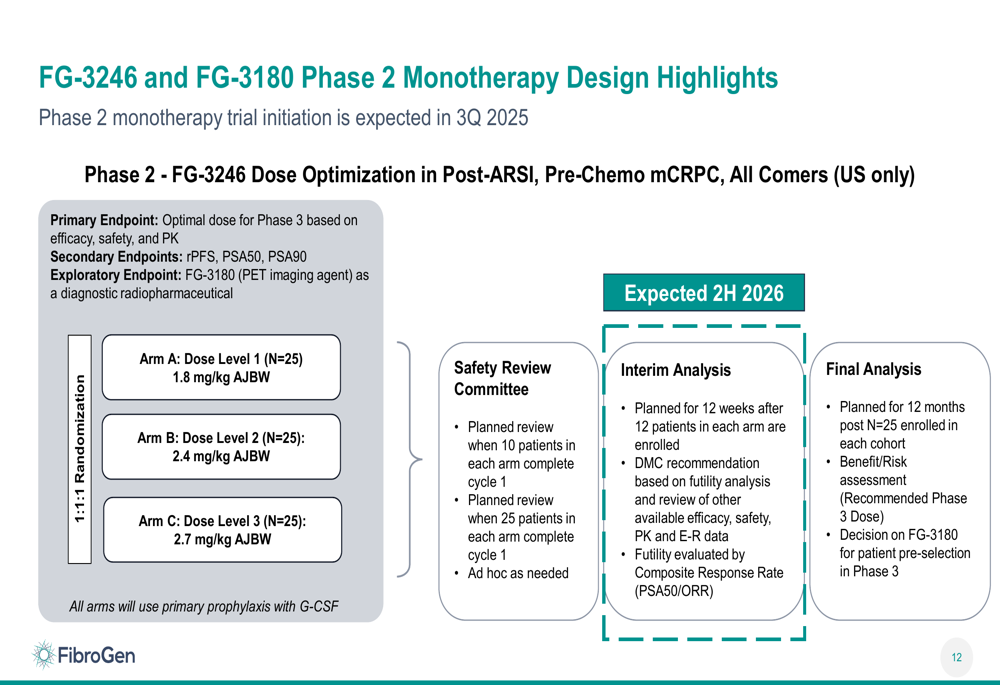

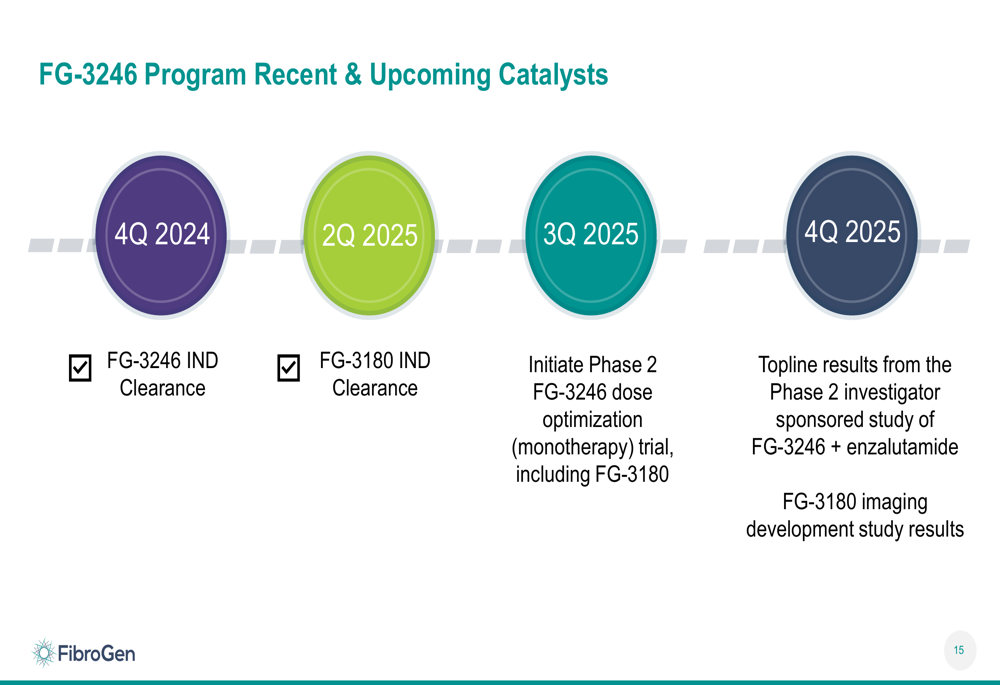

The company also outlined its Phase 2 monotherapy trial design, which is expected to begin in Q3 2025:

Beyond FG-3246, FibroGen discussed FG-3180, a PET imaging agent designed to identify patients most likely to benefit from FG-3246 therapy, and Roxadustat, an oral treatment for anemia that has been approved in over 40 countries outside the United States.

The company presented a timeline of upcoming catalysts that could potentially drive value:

Financial Analysis & Outlook

While FibroGen’s presentation emphasized pipeline potential and strategic transformation, the company’s current financial reality remains challenging. The 89% year-over-year revenue decline underscores the difficulties FibroGen faces in generating near-term revenue, though cost-cutting measures have helped reduce losses.

The China divestment represents a critical financial lifeline, potentially extending the company’s cash runway into the second half of 2027. This extended runway is essential as FibroGen works to advance its clinical programs, particularly FG-3246 and Roxadustat, toward potential commercialization.

Investors appear cautiously optimistic about the company’s strategic direction, with the stock rising 2.13% in aftermarket trading following the earnings release, though it remains near 52-week lows. The company’s market capitalization of approximately $30.72 million reflects significant investor skepticism about its near-term prospects.

FibroGen’s transformation strategy hinges on successfully executing its clinical development plans while managing its limited cash resources. The company’s presentation highlighted the unique opportunity it sees in the prostate cancer market:

For investors, FibroGen represents a high-risk, potentially high-reward opportunity, with success largely dependent on clinical trial outcomes and regulatory decisions expected over the next 12-24 months.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.