Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Fifth Third Bancorp (NASDAQ:FITB) released its first quarter 2025 earnings presentation on April 17, showing stable performance with continued net interest margin expansion and accelerating loan growth. The bank reported adjusted earnings per share of $0.73, generating a return on tangible common equity of 15.7% amid a challenging but improving interest rate environment.

The bank’s stock closed at $34.40 on April 16, down 1.91% ahead of the earnings release. However, in extended trading, shares gained 2.03% to $35.10, suggesting positive investor reaction to the results.

Quarterly Performance Highlights

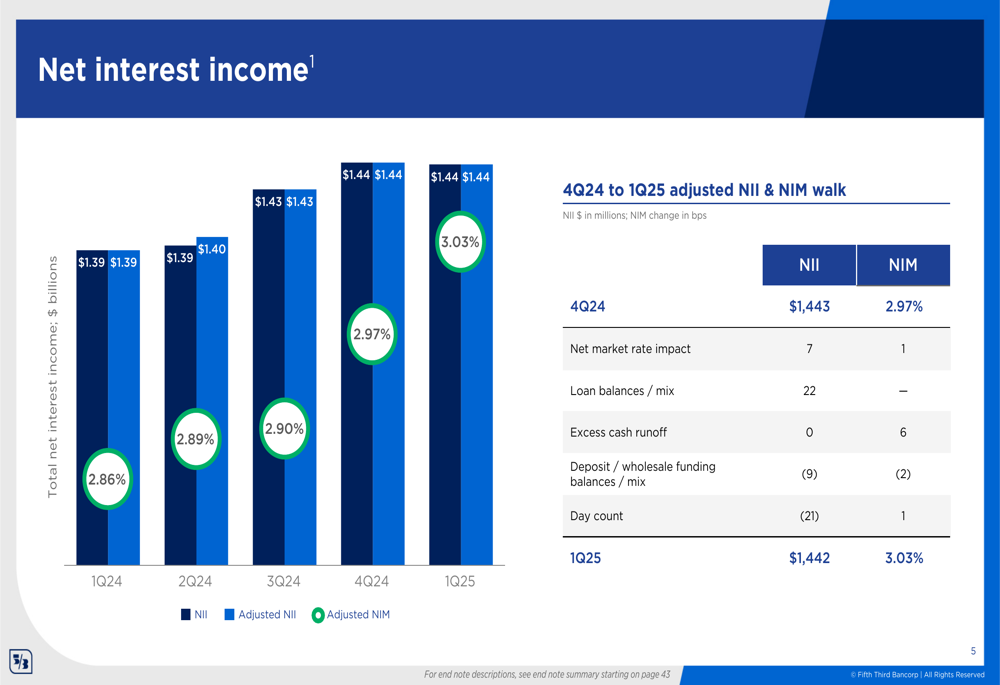

Fifth Third reported stable net interest income of $1.44 billion in Q1 2025, unchanged from the previous quarter, while net interest margin expanded to 3.03%, marking the fifth consecutive quarter of margin improvement. This performance was driven by loan growth, deposit rate management, and fixed-rate asset re-pricing, with interest-bearing liabilities costs declining 20 basis points sequentially.

As shown in the following chart detailing net interest income and margin trends over the past five quarters:

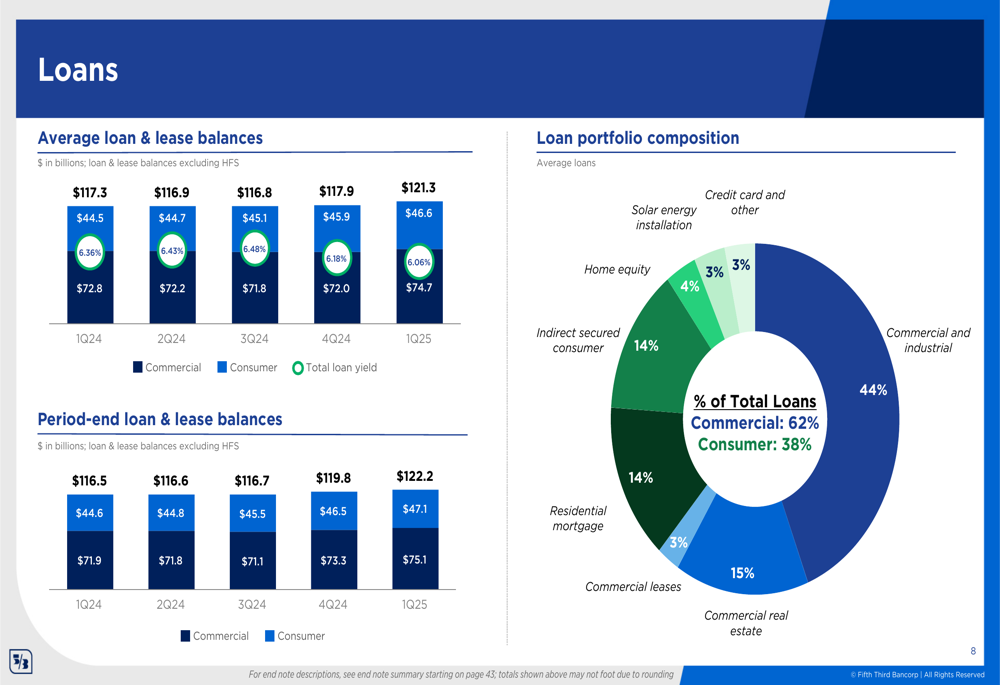

Average loans increased 3% both sequentially and year-over-year, reaching $121.3 billion. Period-end consumer and commercial loans grew 1% and 3% respectively compared to Q4 2024. The bank’s loan portfolio remains well-diversified, with commercial loans representing 62% and consumer loans 38% of the total portfolio.

The following slide illustrates the loan portfolio composition and growth trends:

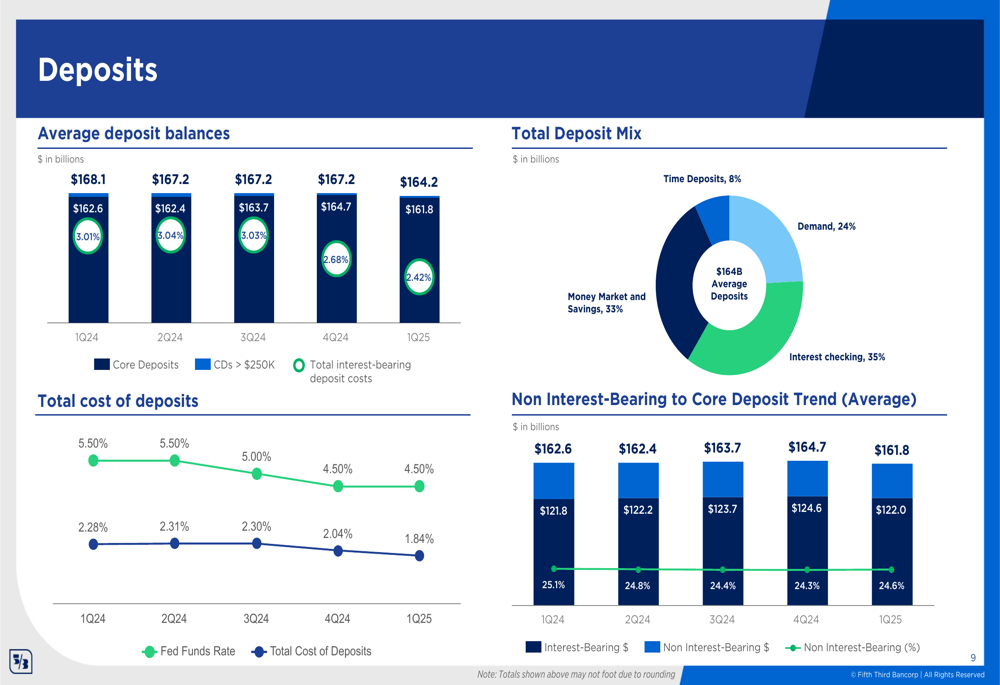

On the deposit front, average core deposits totaled $161.8 billion in Q1 2025, with a cost of 2.42%, down from 2.68% in Q4 2024. The deposit mix remained relatively stable, with non-interest-bearing deposits representing 24.6% of core deposits, a slight increase from 24.3% in the previous quarter.

The following slide shows the deposit trends and mix:

Credit Quality and Risk Management

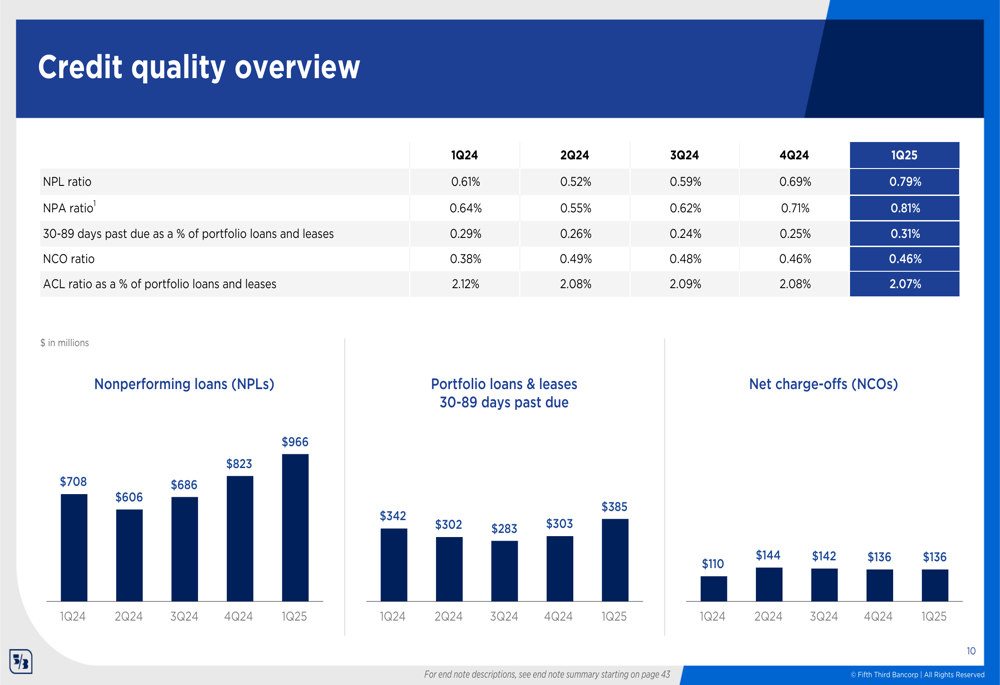

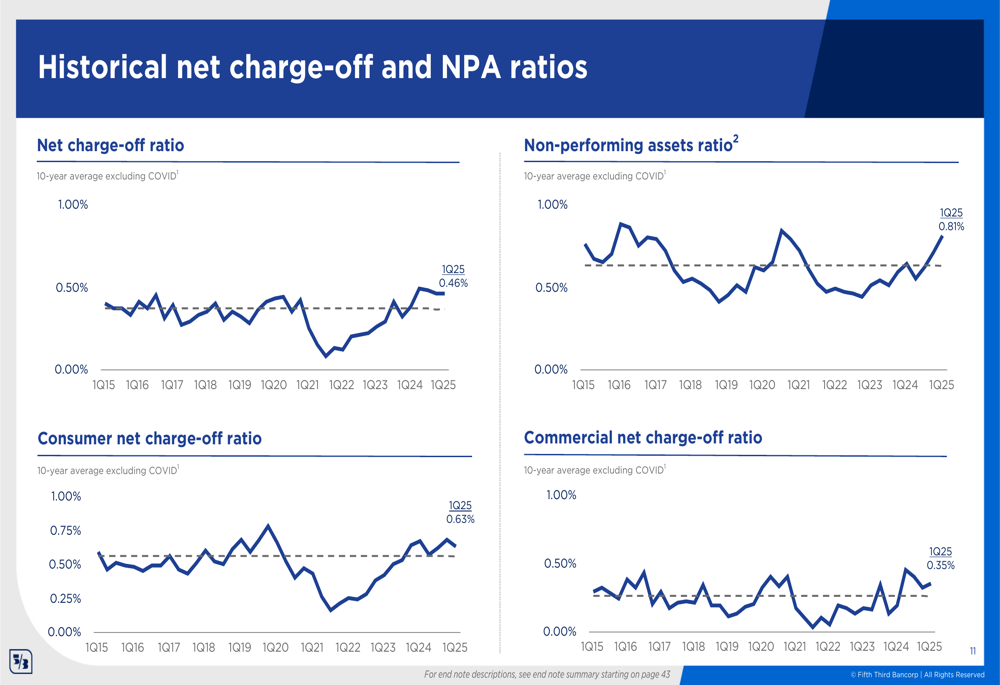

Credit quality metrics showed some mixed signals in Q1 2025. The nonperforming loan ratio increased to 0.79% from 0.69% in Q4 2024, while the net charge-off ratio remained stable at 0.46% for the third consecutive quarter. The allowance for credit losses as a percentage of portfolio loans and leases stood at 2.07%, slightly down from 2.08% in the previous quarter.

The following chart provides a comprehensive overview of credit quality metrics:

Historical credit performance data shows that current credit metrics remain within normalized ranges compared to long-term averages, as illustrated in this slide:

Fee Income and Expense Management

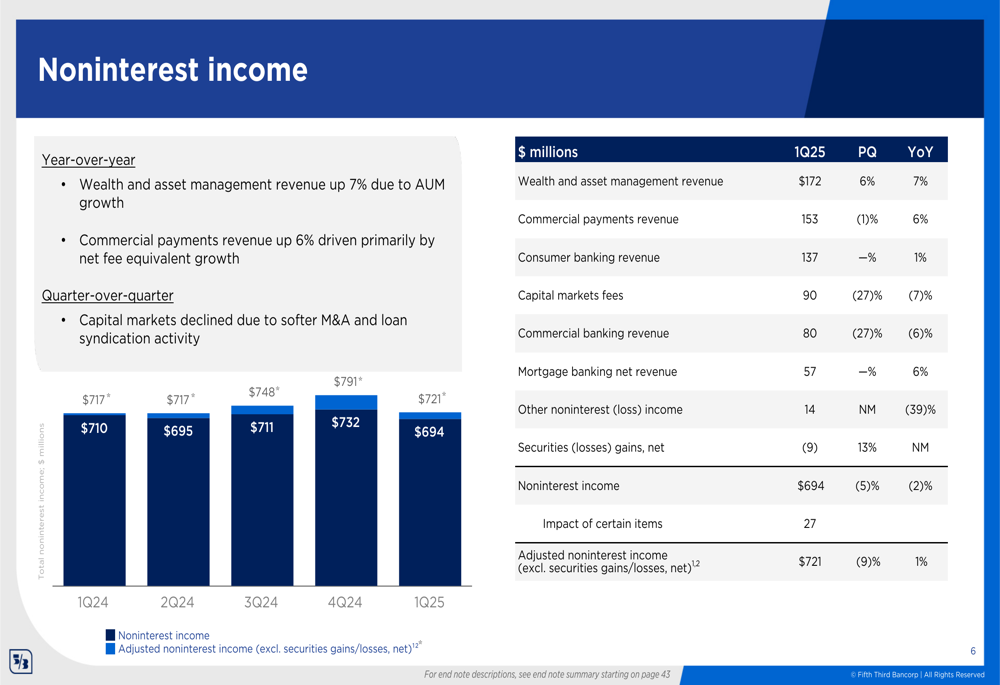

Fifth Third reported adjusted noninterest income of $721 million in Q1 2025, up 1% year-over-year but down 9% sequentially. The bank’s fee revenue demonstrated strength in several areas, with wealth and asset management revenue up 7% year-over-year due to AUM growth, and commercial payments revenue up 6% driven by net fee equivalent growth.

The following slide details the noninterest income breakdown:

Adjusted noninterest expense was $1.304 billion, unchanged from the previous year but up 7% sequentially due to seasonal impact of compensation and benefits. The adjusted efficiency ratio was 60.5%, an improvement of 110 basis points compared to Q1 2024, demonstrating the bank’s focus on expense discipline.

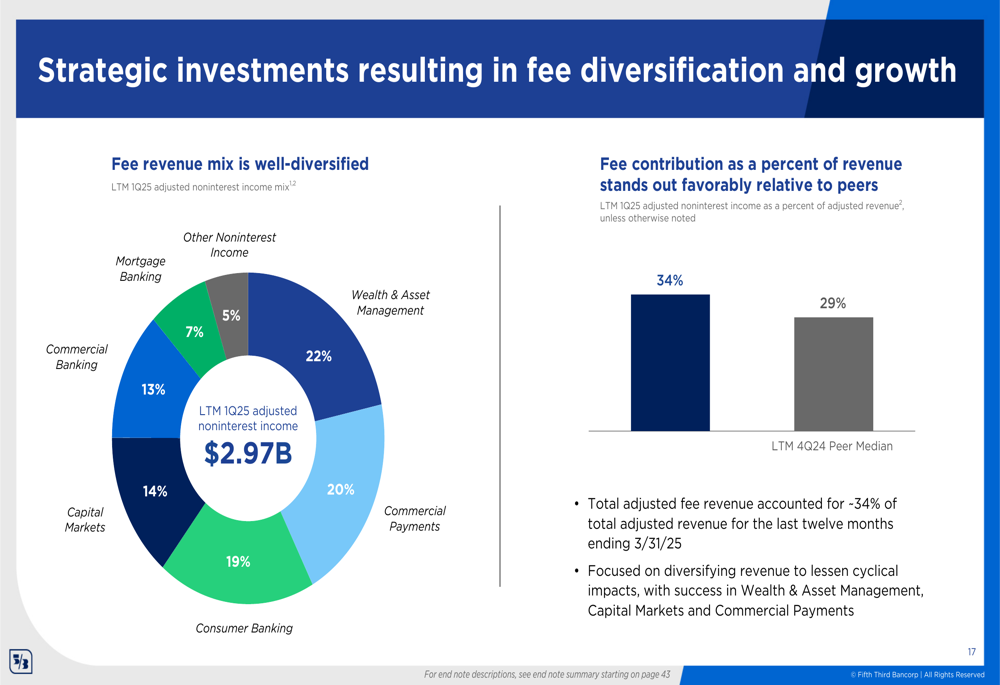

The bank’s strategic investments have resulted in significant fee diversification, with fee revenue accounting for approximately 34% of total adjusted revenue for the last twelve months ending March 31, 2025, compared to a peer median of 29%.

Capital and Liquidity Position

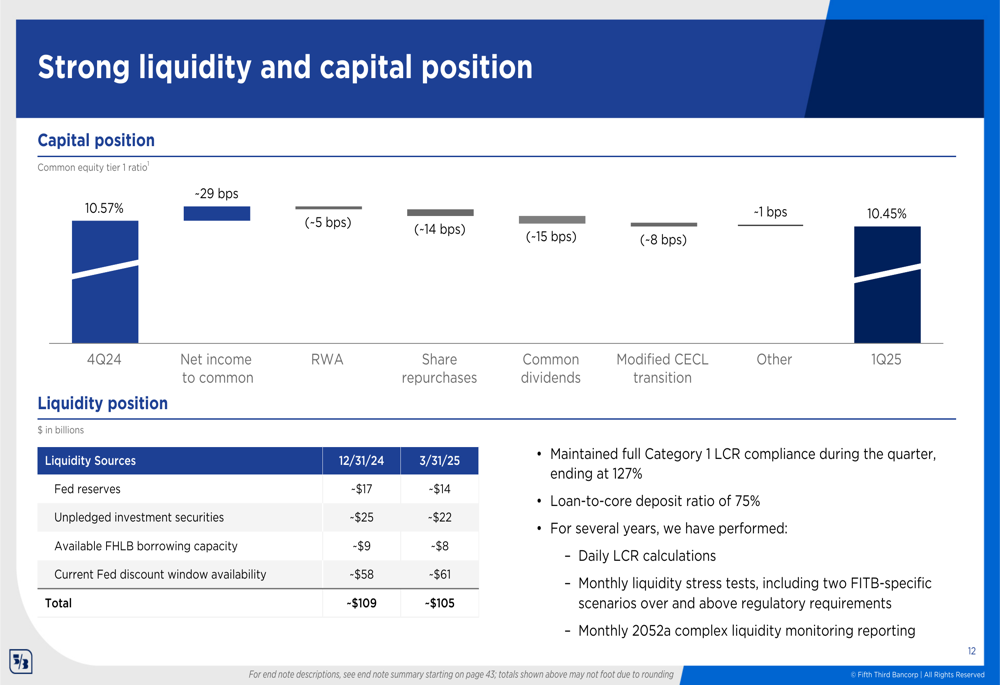

Fifth Third maintained a strong capital position with a Common Equity Tier 1 (CET1) ratio of 10.45% at the end of Q1 2025, down slightly from 10.57% in Q4 2024. The bank reported robust liquidity with approximately $105 billion in liquidity sources as of March 31, 2025, including $14 billion in Fed reserves, $22 billion in unpledged investment securities, and $61 billion in Federal Reserve discount window availability.

The bank maintained full Category 1 LCR compliance during the quarter, ending at 127%, with a loan-to-core deposit ratio of 75%. The following slide details the capital and liquidity position:

Forward-Looking Statements

Fifth Third provided optimistic guidance for both Q2 2025 and the full year. For Q2 2025, the bank expects average loans and leases to increase approximately 1%, net interest income to grow 2-3%, noninterest income to rise 2-6%, and noninterest expense to decrease by about 5%. The net charge-off ratio is projected to be 45-49 basis points.

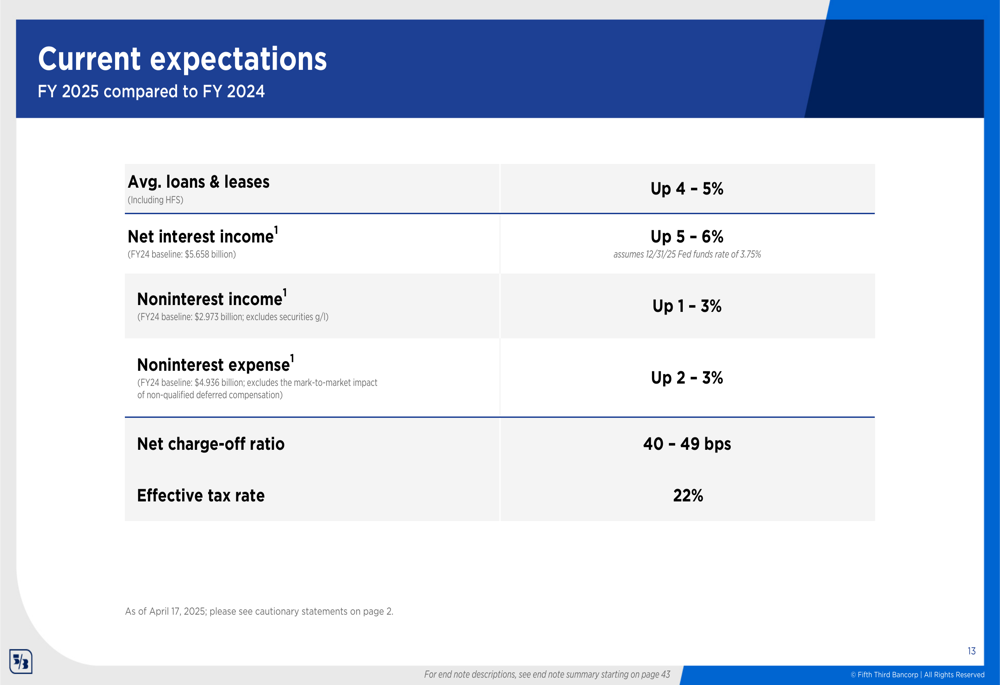

For the full year 2025, Fifth Third forecasts average loans and leases to grow 4-5%, net interest income to increase 5-6%, noninterest income to rise 1-3%, and noninterest expense to grow 2-3%. The net charge-off ratio is expected to be 40-49 basis points for the year.

The following slide outlines the full-year 2025 expectations:

Strategic Initiatives

Fifth Third continues to invest in digital capabilities, with average active digital users reaching 3.14 million in Q1 2025, up from 3.09 million in Q4 2024. Mobile users increased to 2.40 million from 2.37 million in the previous quarter. The bank maintained a high digital mortgage application rate of 98% and reported an average app store rating of 4.8 stars, above the peer average of 4.5 stars.

The bank’s strategic investments have resulted in significant fee diversification, with wealth and asset management (22%), commercial payments (20%), and consumer banking (19%) representing the largest components of the fee revenue mix. This diversification helps reduce cyclical impacts and provides more stable revenue streams.

As illustrated in the following fee revenue mix chart:

Fifth Third generated consumer household growth of 2% compared to Q1 2024, including 5% growth in the Southeast, highlighting the success of its geographic expansion strategy. The bank’s focus on commercial payments and wealth and asset management has driven strong fee performance, positioning it well for future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.