Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Introduction & Market Context

FinWise Bancorp (NASDAQ:FINW) released its Q1 2025 investor presentation on April 30, 2025, highlighting its differentiated business model as a banking and payments solutions provider to fintechs. Despite beating earnings expectations with EPS of $0.23 versus a forecasted $0.18, the company’s stock declined 2.64% in after-hours trading, closing at $15.12.

The presentation emphasized FinWise’s strategic expansion into payments and BIN sponsorship services while maintaining its focus on risk management and compliance. The company reported total assets of $804.1 million, representing a 31.6% year-over-year increase, though its net interest margin declined to 8.27% from 10.12% a year earlier.

Strategic Initiatives

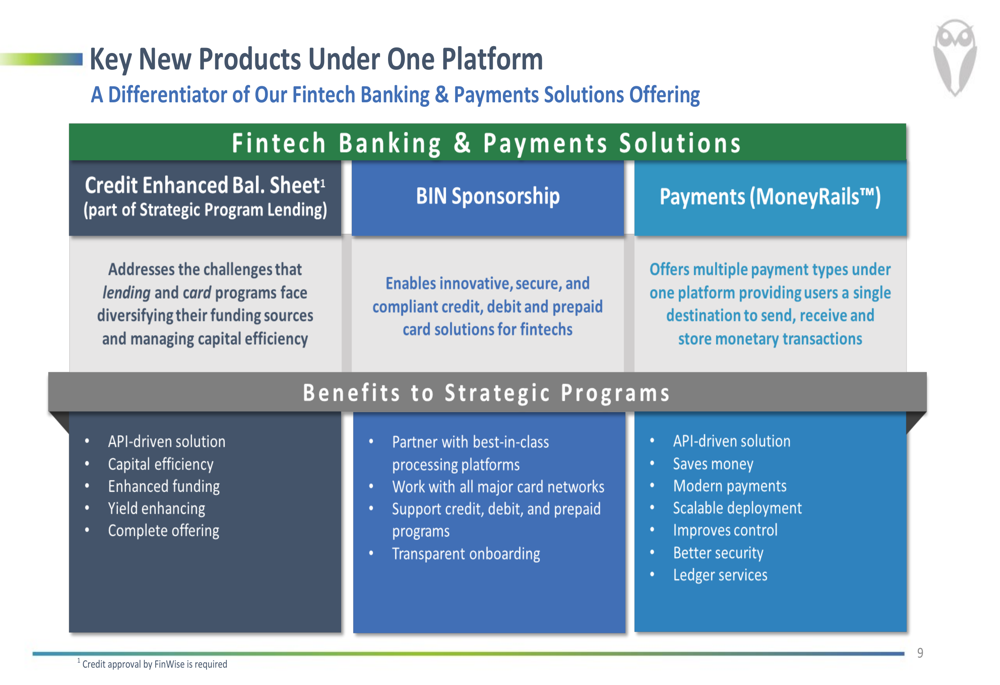

FinWise’s presentation highlighted three key strategic initiatives under its expanded fintech banking and payments solutions platform: Credit Enhanced Balance Sheet, BIN Sponsorship, and Payments (MoneyRails™). These initiatives aim to diversify revenue streams and reduce the company’s reliance on traditional lending.

As shown in the following comprehensive overview of these new product offerings:

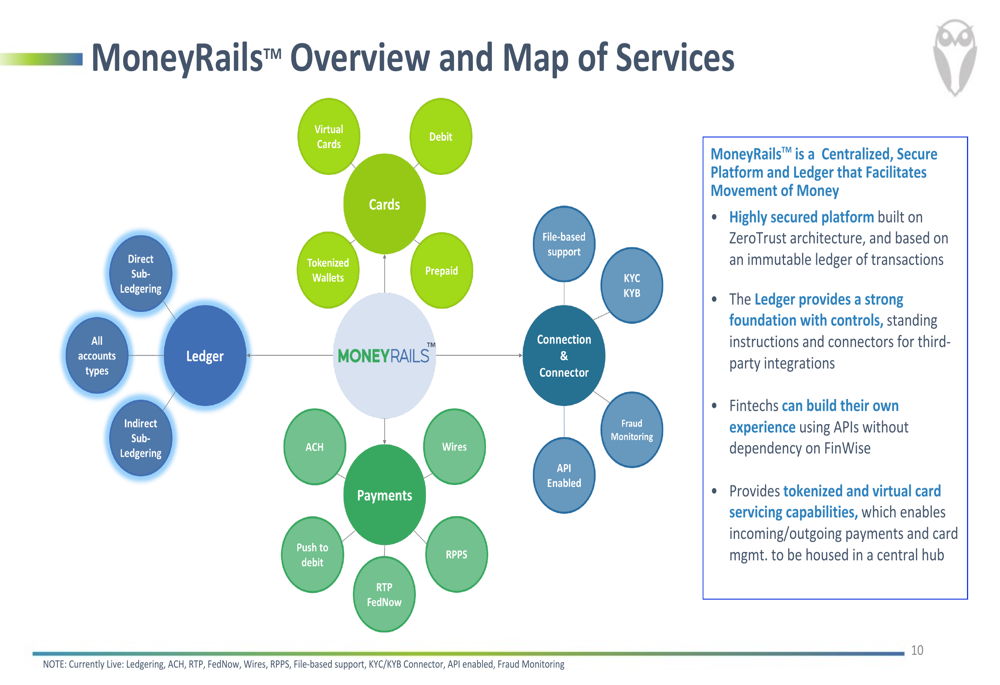

The MoneyRails™ platform represents a significant component of FinWise’s strategic expansion, offering a centralized payment hub that facilitates various payment methods including ACH, wires, real-time payments, and card services. The platform is built on a ZeroTrust architecture with an immutable ledger of transactions, providing security and flexibility for fintech partners.

The following diagram illustrates the comprehensive payment services offered through the MoneyRails™ platform:

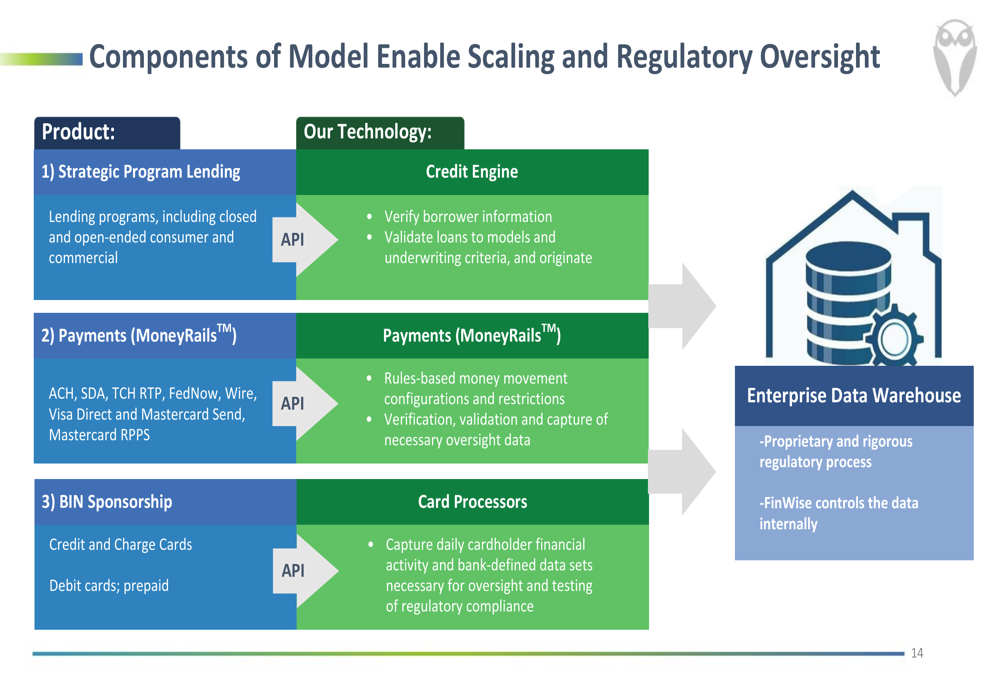

FinWise’s technology infrastructure plays a crucial role in enabling these strategic initiatives while maintaining regulatory compliance. The company has developed proprietary systems for credit origination, payment processing, and data management that support scaling while ensuring proper oversight.

As demonstrated in this overview of the company’s technological infrastructure:

Quarterly Performance Highlights

For Q1 2025, FinWise reported net income of $3.2 million, up from $2.8 million in Q4 2024 but slightly down from $3.3 million in Q1 2024. The company maintained solid loan originations of $1,264.6 million during the quarter, while total loans outstanding held for investment increased to $492.2 million.

The company’s deposit base grew significantly to $605.8 million, up from $545.0 million in the previous quarter and $424.1 million a year earlier. However, the deposit composition remains heavily weighted toward certificates of deposit (61%), presenting what management described as a "significant opportunity to reduce cost of funds by gradually diversifying deposit composition."

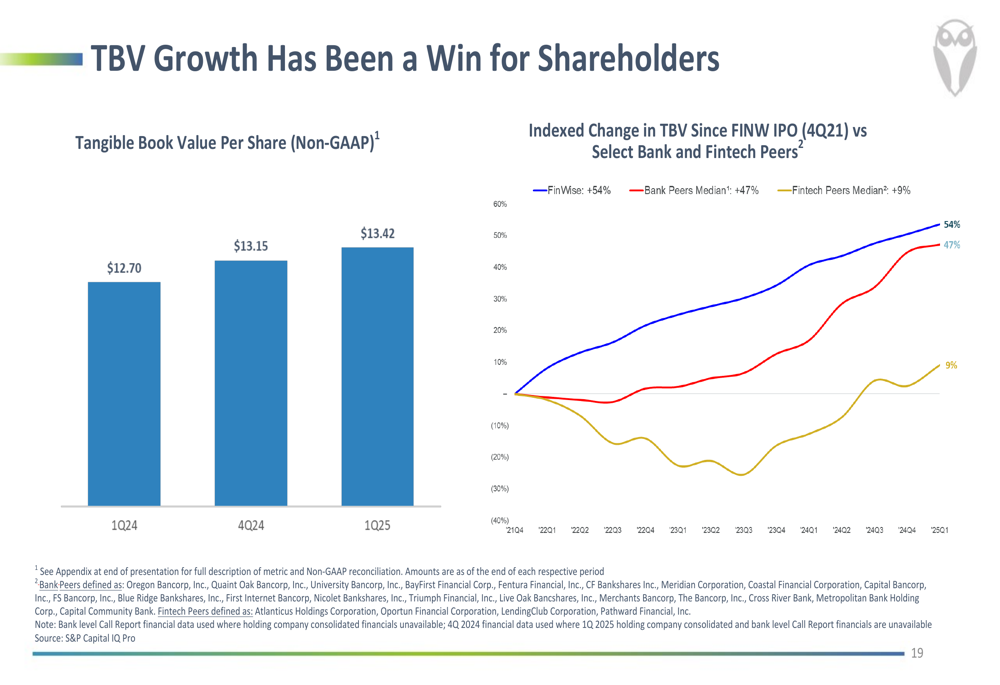

FinWise’s tangible book value per share continued its upward trajectory, reaching $13.42 in Q1 2025 compared to $13.15 in Q4 2024 and $12.70 in Q1 2024. This represents a 54% increase since the company’s IPO, outperforming both bank and fintech peers.

The following chart illustrates this impressive tangible book value growth compared to peers:

Detailed Financial Analysis

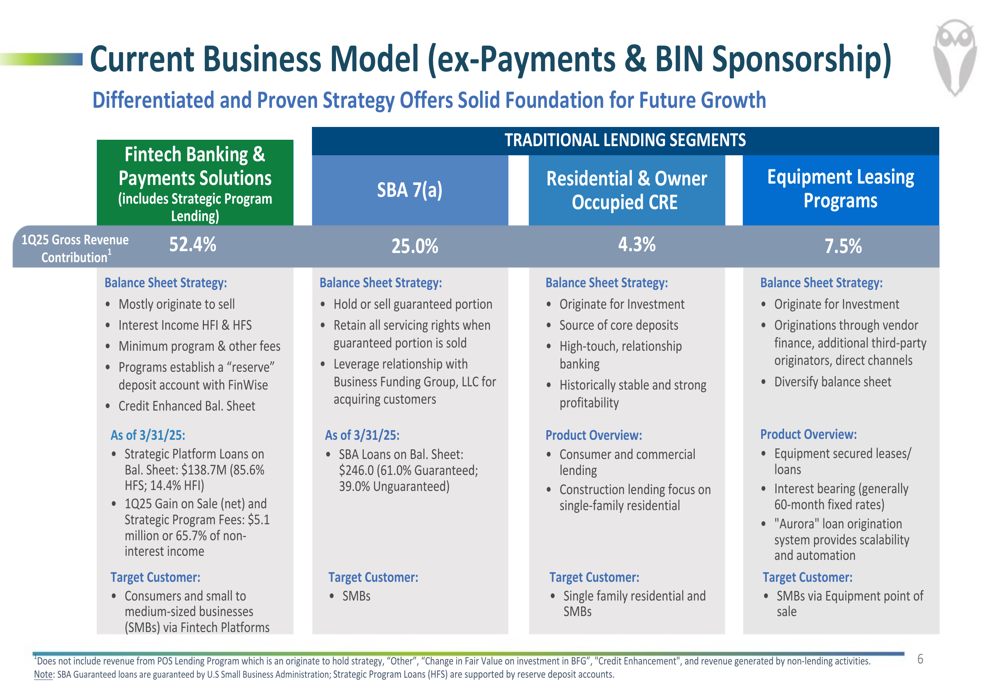

FinWise’s business model continues to generate diversified revenue streams, with Strategic Program Lending contributing 52.4% of Q1 2025 gross revenue, followed by SBA (LON:SBA) 7(a) lending at 25.0%, Equipment Leasing Programs at 7.5%, and Residential & Owner Occupied CRE at 4.3%.

The following breakdown illustrates the company’s current business model:

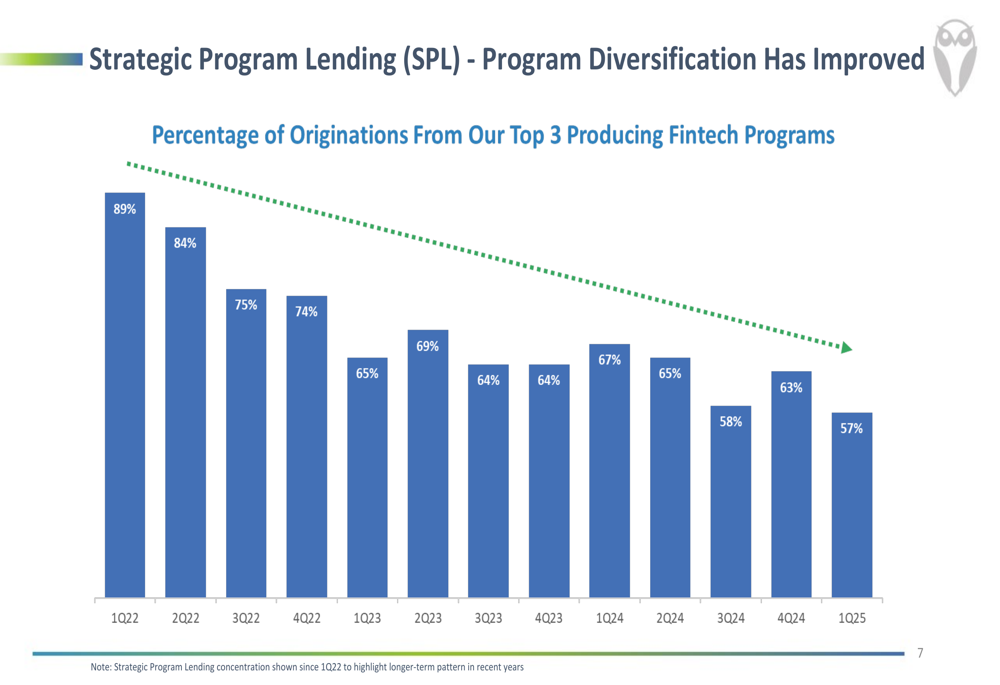

The company has successfully diversified its Strategic Program Lending portfolio over time, reducing concentration risk. The percentage of originations from the top three producing fintech programs has decreased from 89% in Q1 2022 to 57% in Q1 2025, as shown in this trend analysis:

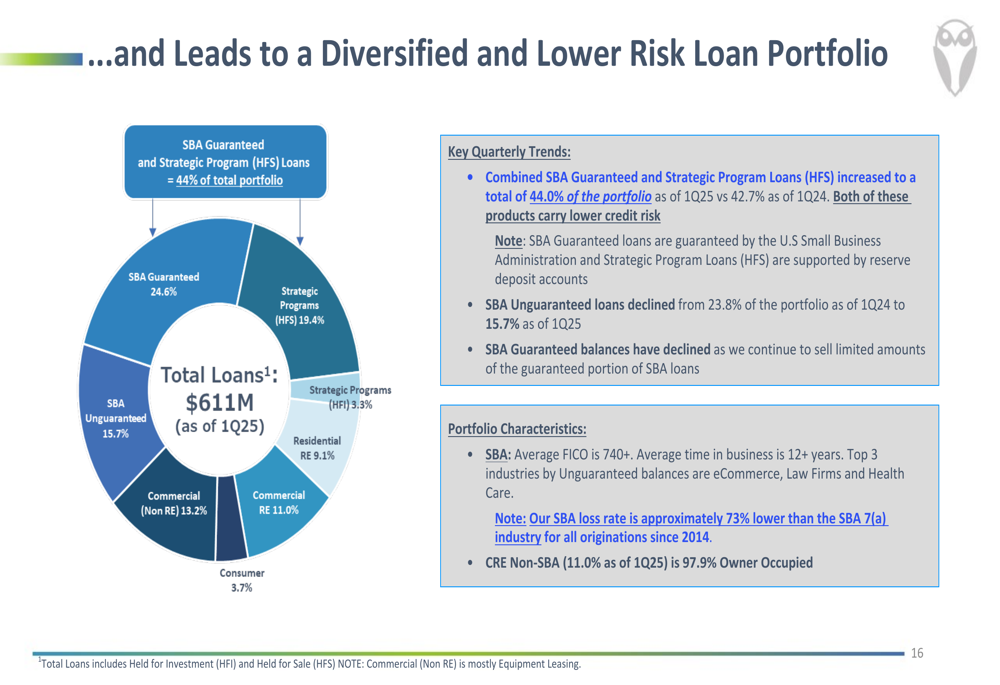

FinWise maintains a lower-risk loan portfolio with 44% consisting of SBA Guaranteed loans and Strategic Program loans held for sale (which are typically cash-collateralized). This conservative approach has helped mitigate net charge-offs even as credit quality normalized due to the higher rate environment.

The following chart shows the company’s diversified loan portfolio composition:

Despite the positive trends in asset growth and portfolio diversification, FinWise faces challenges with margin compression. Net interest margin declined to 8.27% in Q1 2025 from 10.00% in Q4 2024 and 10.12% in Q1 2024. Additionally, non-interest expenses increased to $14.3 million in Q1 2025 from $13.6 million in Q4 2024, resulting in an efficiency ratio of 64.8%, up from 64.2% in the previous quarter.

Competitive Industry Position

FinWise highlighted its industry recognition as a top-performing bank, including ranking #1 in Independent (LON:IOG) Banker’s Best Performing Banks for the third consecutive year (based on 3-year average pre-tax ROA) and placing in the top three on American Banker’s annual list of Top-Performing Publicly Traded Banks with under $2 billion of assets.

The company’s differentiated business model focuses on providing banking and payments solutions to fintechs while maintaining a strong compliance and risk management culture. As of Q1 2025, 72 employees (37% of total staff) worked in IT, compliance, risk management, and BSA functions, underscoring the company’s commitment to regulatory compliance.

FinWise currently supports several prominent fintech brands, including Upstart (NASDAQ:UPST), Elevate, Reach Financial, Empower, LendingPoint, OppLoans, and others, providing various combinations of strategic program lending, payments processing, credit-enhanced balance sheet services, and BIN sponsorship.

Forward-Looking Statements

Looking ahead, FinWise anticipates credit-enhanced loan balances to increase by $50 million to $100 million by the end of 2025, according to CFO Bob Wohlman. The company expects net interest income growth driven by seasonal returns of high-yielding programs and continued loan portfolio expansion, though net interest margin is projected to continue its decline.

The presentation outlined several potential long-term benefits from the company’s fintech banking and payments solutions strategy, including expanded and diversified revenue sources, more diversified deposit composition with reduced cost of funds, increased percentage of prime loans, and enhanced operating leverage through outsourced solutions.

However, investors should note that while FinWise beat earnings expectations for Q1 2025, revenue slightly missed forecasts at $22.09 million versus an anticipated $22.37 million. The stock’s negative reaction despite the earnings beat suggests some investor concerns about revenue growth and margin compression going forward.

Chairman and CEO Kent Landwatter remarked, "The FinWise business model remained resilient in its first quarter, even amidst a more uncertain macro environment," highlighting the company’s ability to navigate challenging conditions while continuing to execute its strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.