Oracle stock falls after report reveals thin margins in AI cloud business

First Advantage Corp (NASDAQ:FA) shares climbed 8.27% to $17.55 on August 7, 2025, following the release of the company’s Q2 2025 earnings presentation, which highlighted solid financial performance and accelerated synergy realization from its Sterling acquisition.

Executive Summary

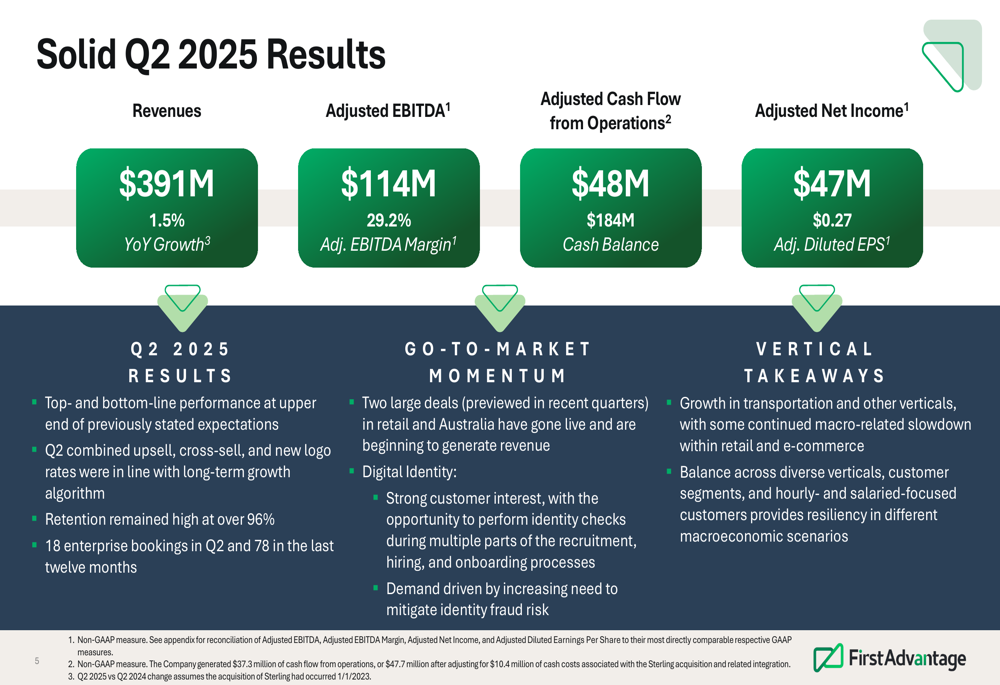

First Advantage reported Q2 2025 revenue of $390.6 million, representing a 1.5% year-over-year increase compared to pro forma Q2 2024. The company achieved adjusted EBITDA of $113.9 million with a 29.2% margin, up from 26.5% in the same period last year. Adjusted diluted earnings per share rose to $0.27 from $0.21 in Q2 2024.

"Q2 performance was at the top end of previously stated expectations, driven by go-to-market execution and accelerated synergy realization," noted CEO Scott Staples in the presentation.

As shown in the following financial results summary:

The company maintained high customer retention at over 96% while securing 18 enterprise bookings in Q2 and 78 in the last twelve months. First Advantage also highlighted the successful launch of several large retail deals and an Australian implementation.

Integration Progress and Synergy Realization

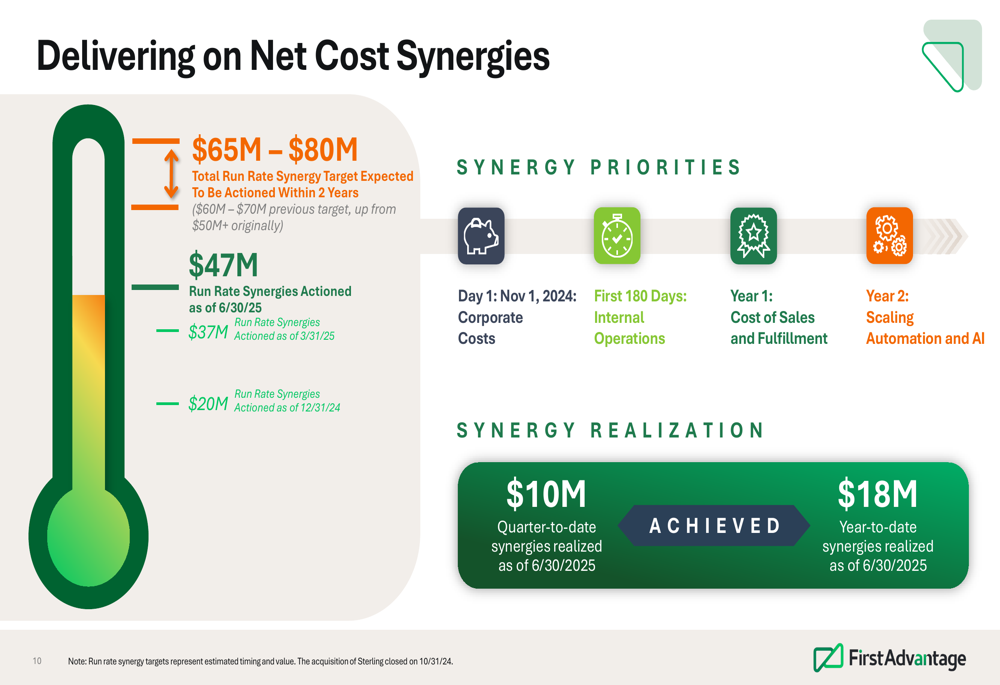

A key focus of the presentation was the company’s progress on integrating Sterling Check Corp, which it acquired in late 2024. First Advantage reported significant advancement in realizing synergies, with $47 million in run-rate synergies actioned as of June 30, 2025, up from $37 million at the end of Q1.

The company has increased its synergy target to $65-80 million expected to be actioned within two years of closing, up from the initial target of $50-70 million. This accelerated synergy realization has contributed significantly to margin expansion.

The following chart illustrates the company’s progress on synergy actioning:

"We’re delivering on post-close priorities and are ahead of schedule on integration while maintaining high levels of customer retention," Staples emphasized. The integration strategy includes leveraging best-of-breed product and platform solutions, launching new offerings like Click.Chat.Call and a higher-margin WOTC product.

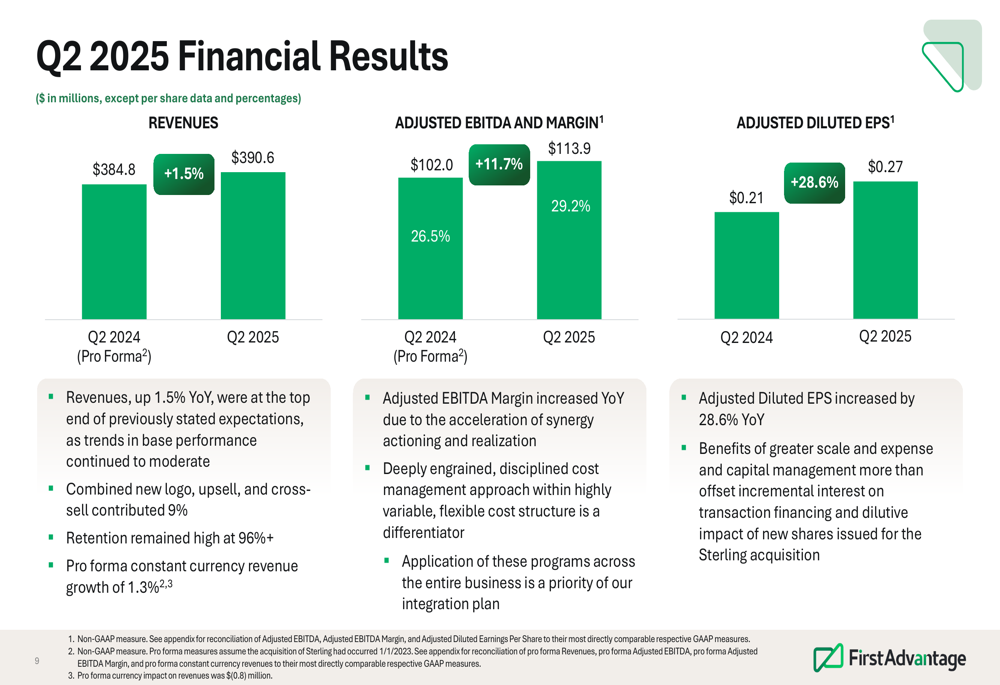

Detailed Financial Analysis

First Advantage provided a comprehensive breakdown of its Q2 2025 financial performance, showing improvements across key metrics. The adjusted EBITDA margin expansion of 270 basis points year-over-year was primarily attributed to accelerated synergy realization.

The detailed financial results are presented in the following chart:

The company’s revenue growth algorithm shows that while base revenue declined by 6%, this was offset by 5% growth from upsell/cross-sell activities and 4% from new logos, resulting in the overall 1.5% revenue growth. The 96% gross retention rate demonstrates the company’s strong customer relationships despite macroeconomic challenges.

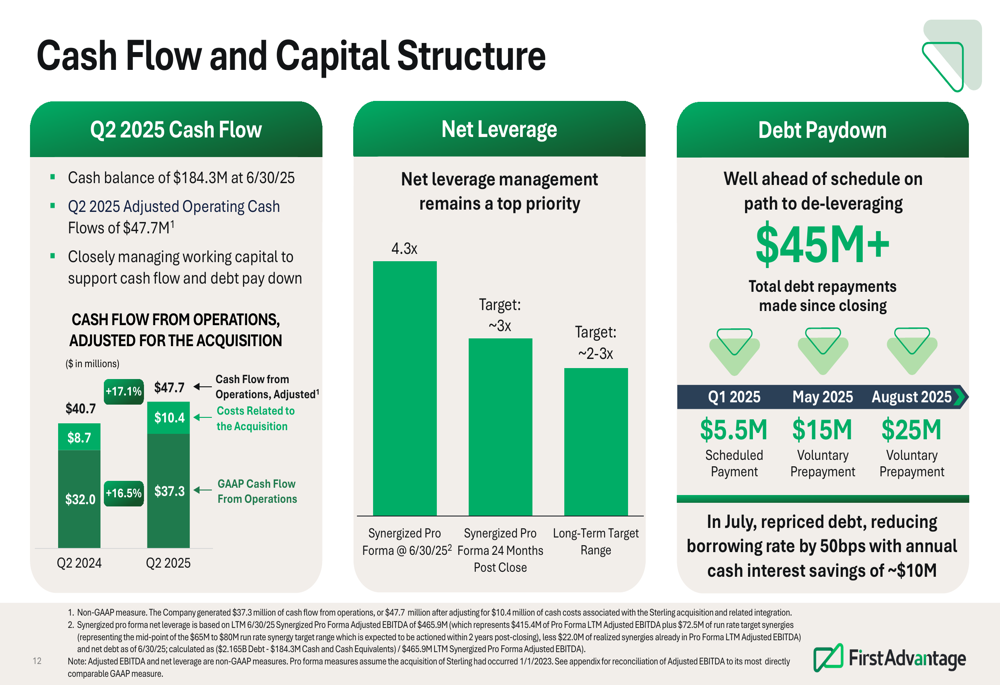

Cash Flow and Capital Structure

First Advantage reported a cash balance of $184.3 million as of June 30, 2025, with Q2 adjusted operating cash flows of $47.7 million. The company has made significant progress on debt reduction, with total debt repayments of over $45 million since closing the Sterling acquisition, including a $25 million payment in August 2025.

In July, the company successfully repriced its debt, reducing its borrowing rate by 50 basis points, which is expected to generate annual cash interest savings of approximately $10 million.

The following slide details the company’s cash flow and capital structure:

Current net leverage stands at 4.3x, with a target to reduce it to approximately 3x in the near term and 2-3x over the longer term. This deleveraging strategy aligns with the company’s focus on strengthening its balance sheet following the Sterling acquisition.

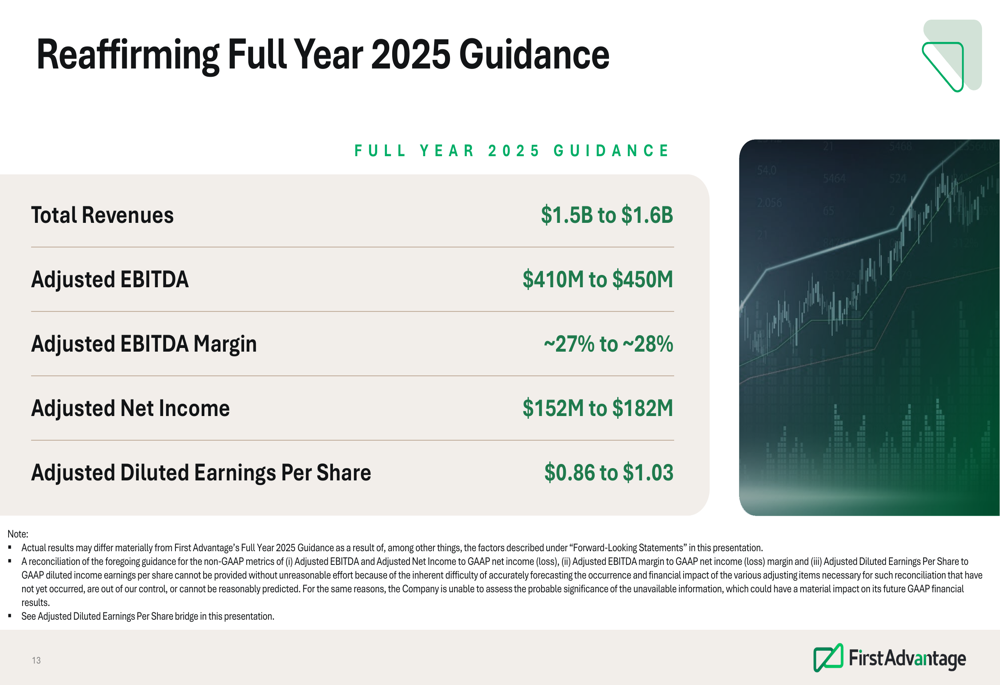

Forward-Looking Statements and Guidance

First Advantage reaffirmed its full-year 2025 guidance, projecting total revenues of $1.5-1.6 billion, adjusted EBITDA of $410-450 million, and adjusted diluted earnings per share of $0.86-1.03.

The guidance details are presented in the following slide:

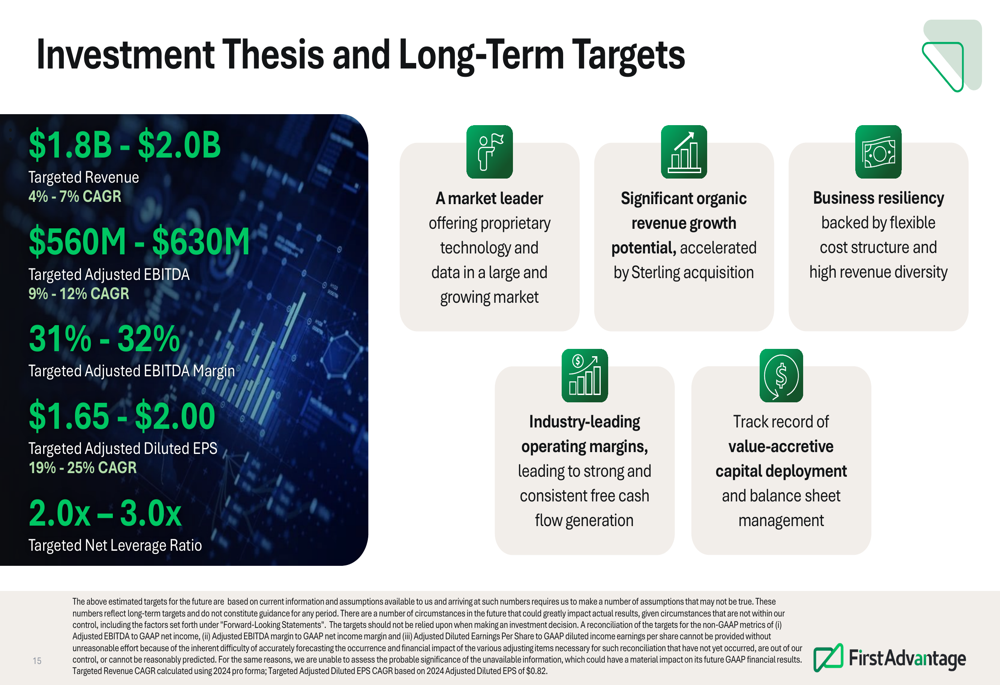

Looking beyond 2025, the company outlined its long-term targets, including revenue of $1.8-2.0 billion (representing a 4-7% CAGR), adjusted EBITDA of $560-630 million (9-12% CAGR), and adjusted EBITDA margin of 31-32%. The company also targets adjusted diluted EPS of $1.65-2.00 (19-25% CAGR) and a net leverage ratio of 2.0-3.0x.

These long-term targets are supported by the company’s investment thesis, as shown below:

Strategic Initiatives

First Advantage is executing on its FA 5.0 strategy, which focuses on increasing market share in target verticals, accelerating international growth, and implementing a best-in-breed product and platform approach. The company highlighted its continued investments in AI and automation to drive innovation and operational efficiency.

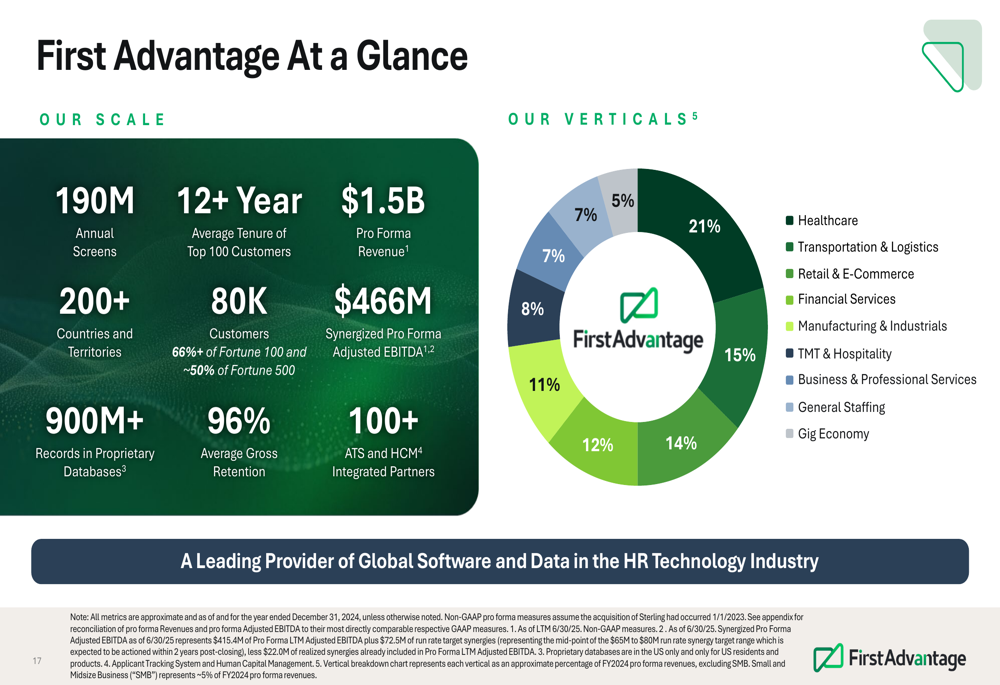

The company’s scale and diversified customer base provide resilience across economic cycles. First Advantage serves approximately 80,000 customers across more than 200 countries and territories, with a balanced distribution across verticals including healthcare (21%), TMT & hospitality (15%), and gig economy (14%).

The following slide provides an overview of First Advantage’s scale and customer distribution:

This diversification strategy has helped the company maintain stability despite varying performance across different sectors of the economy.

The Q2 2025 results represent a continuation of First Advantage’s positive momentum following its strong Q1 performance, when the company exceeded analyst expectations with an adjusted diluted EPS of $0.17 against a forecast of $0.13. The consistent execution on synergy realization and strategic initiatives appears to be resonating with investors, as evidenced by the stock’s positive performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.