Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

First BanCorp (NYSE:FBP), the bank holding company for FirstBank Puerto Rico, presented its first quarter 2025 financial results on April 24, 2025, highlighting improved profitability metrics despite a slight contraction in its loan portfolio. The bank reported net income of $77.1 million, or $0.47 per diluted share, surpassing analyst expectations in a quarter marked by margin expansion and disciplined expense management.

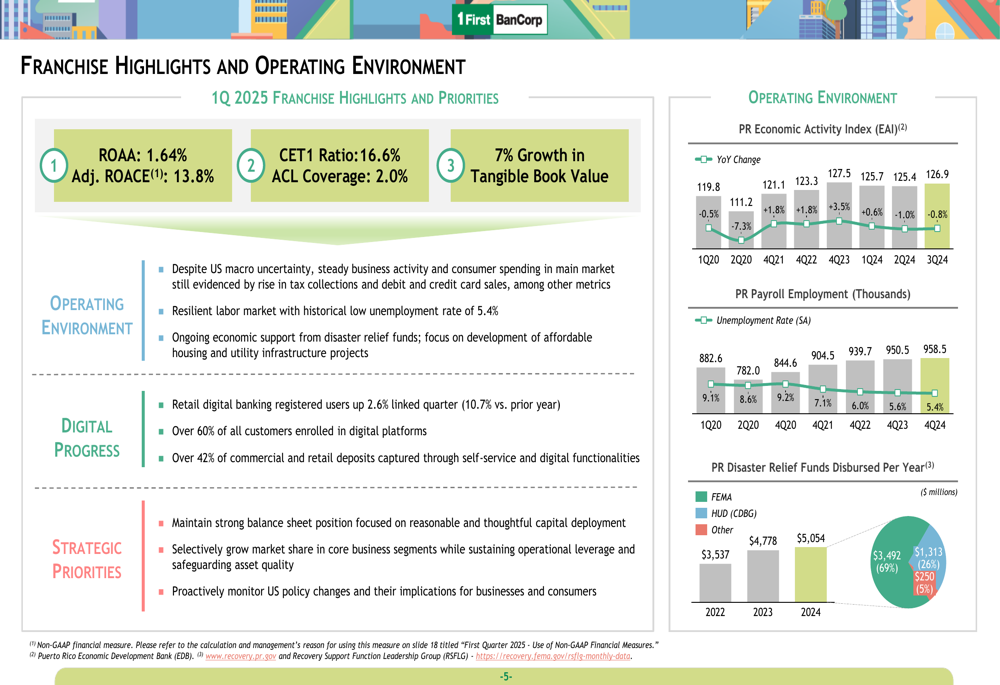

The bank’s performance comes amid a resilient Puerto Rican economy, which continues to show steady business activity and consumer spending despite broader U.S. macroeconomic uncertainties. Puerto Rico’s unemployment rate remains at a historically low 5.4%, with ongoing economic support from disaster relief funds bolstering local economic conditions.

Quarterly Performance Highlights

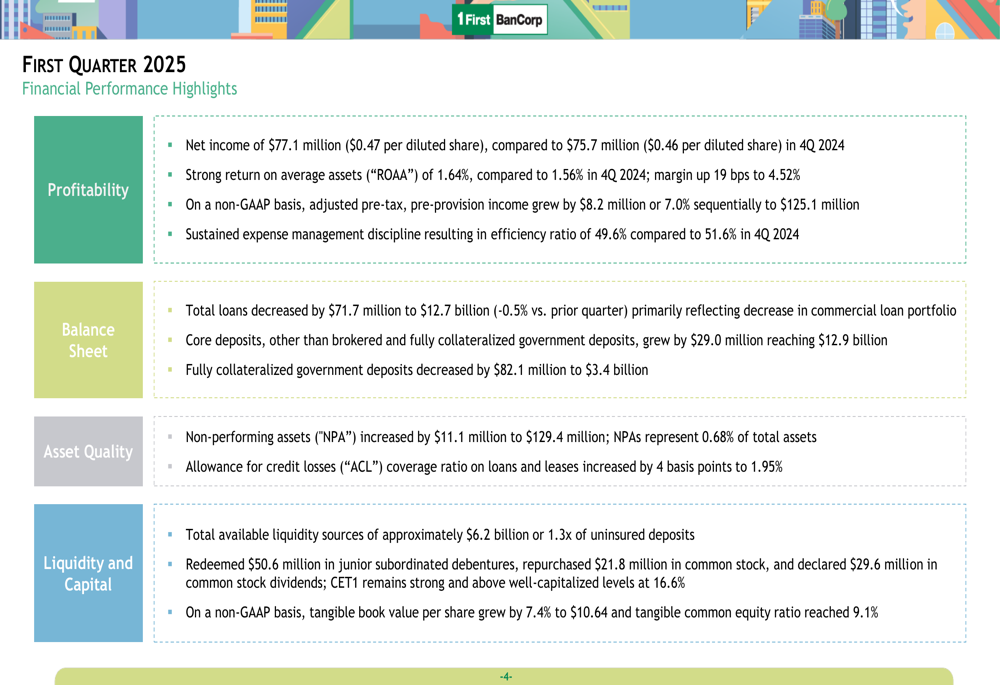

First BanCorp reported net income of $77.1 million ($0.47 per diluted share) for Q1 2025, an increase from $75.7 million ($0.46 per diluted share) in the previous quarter. Return on average assets (ROAA) improved to 1.64% from 1.56% in Q4 2024, while the net interest margin expanded by 19 basis points to 4.52%.

As shown in the following quarterly financial performance highlights:

The bank’s efficiency ratio improved to 49.6% compared to 51.6% in the previous quarter, reflecting sustained expense management discipline. On a non-GAAP basis, adjusted pre-tax, pre-provision income grew by $8.2 million or 7.0% sequentially to $125.1 million.

The franchise continues to benefit from a stable operating environment in Puerto Rico, with digital banking adoption increasing steadily. Retail digital banking registered users grew by 2.6% compared to the previous quarter and 10.7% year-over-year, with over 60% of all customers now enrolled in digital platforms.

As illustrated in the following franchise highlights and economic indicators:

Detailed Financial Analysis

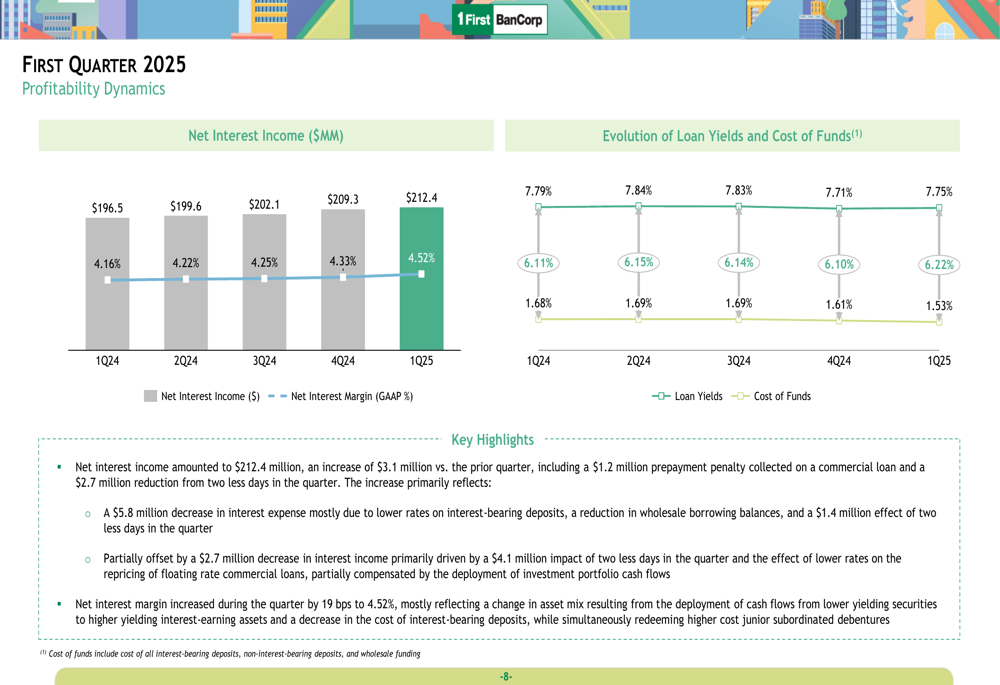

First BanCorp’s net interest income continued its upward trajectory, reaching $212.4 million in Q1 2025, compared to $209.3 million in Q4 2024 and $196.5 million in Q1 2024. This represents an 8.1% increase year-over-year, driven primarily by higher loan yields and improved net interest margin.

The evolution of net interest income and margin is depicted in the following chart:

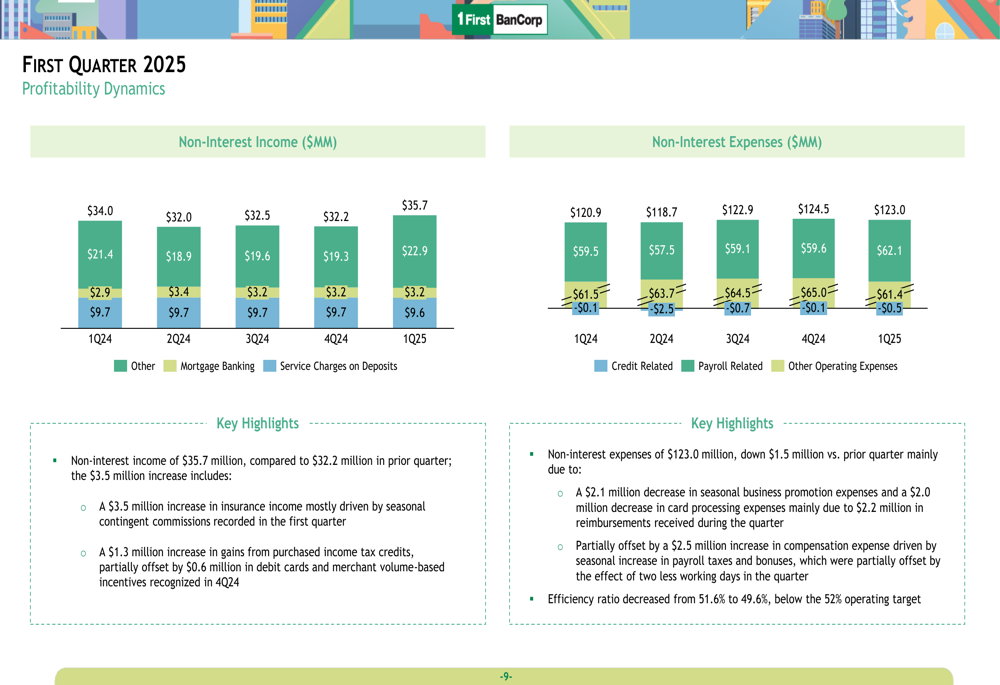

Non-interest income and expenses also showed favorable trends. The bank maintained disciplined expense management while continuing to invest in digital infrastructure. The following chart illustrates these trends:

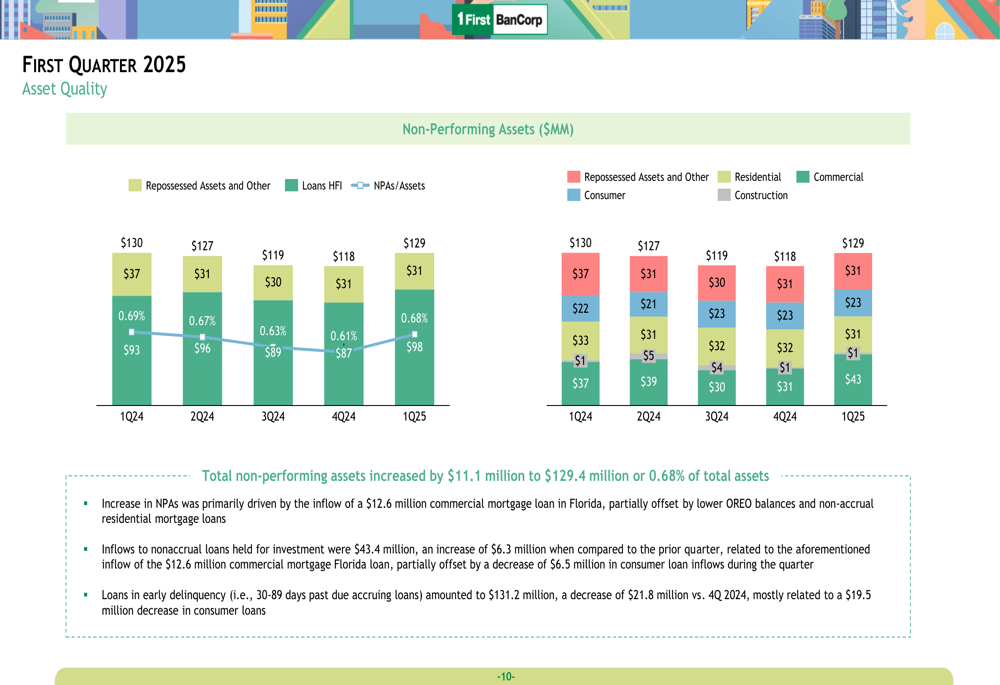

Asset quality metrics showed a slight increase in non-performing assets, which rose by $11.1 million to $129.4 million, representing 0.68% of total assets. This increase was primarily driven by residential mortgage loans. The following chart shows the evolution of non-performing assets:

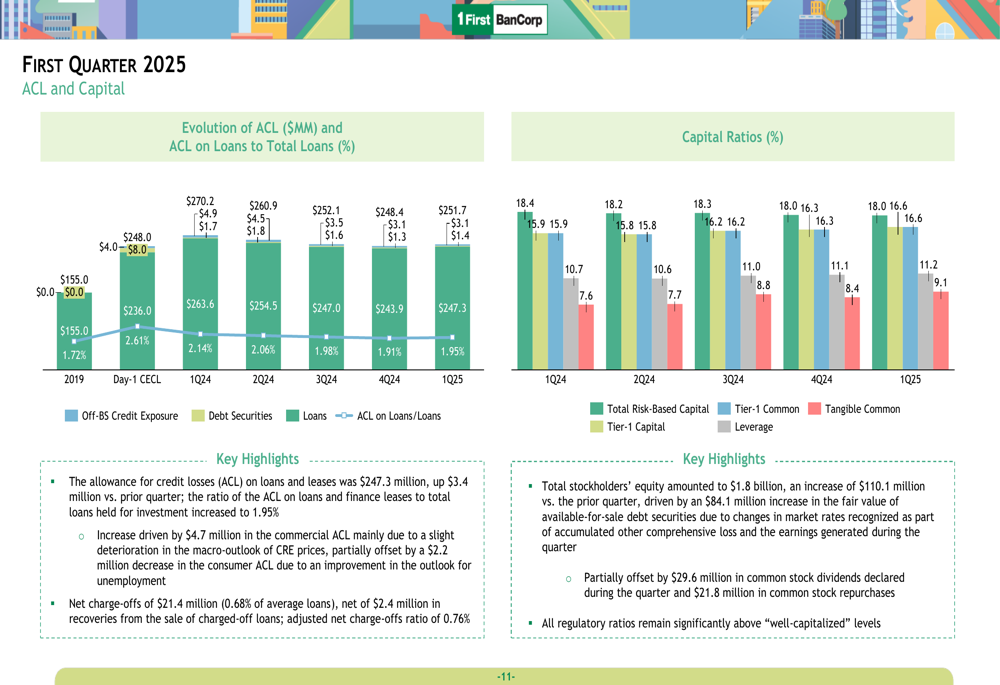

The bank’s allowance for credit losses (ACL) stood at $247.3 million, representing 1.95% of total loans, a slight increase from 1.91% in the previous quarter. Capital ratios remained strong, with Common Equity Tier 1 (CET1) at 16.6%, well above regulatory requirements.

The following chart illustrates the evolution of ACL and capital ratios:

Strategic Initiatives & Capital Management

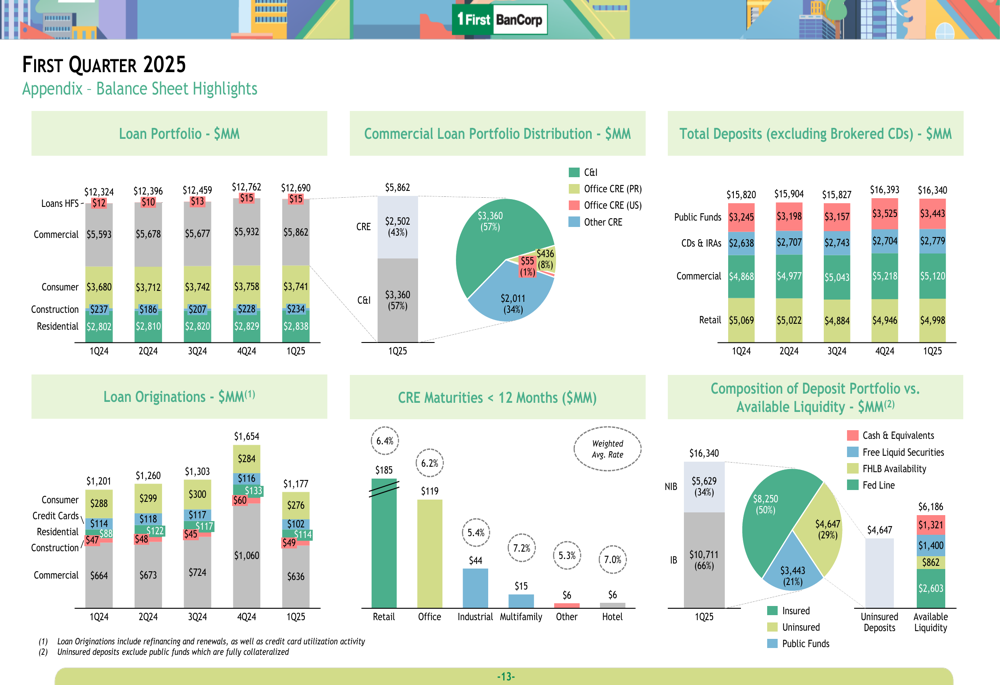

First BanCorp continues to focus on digital transformation, with significant progress in customer adoption of digital banking platforms. The bank’s balance sheet remains well-positioned, with a diversified loan portfolio and strong deposit base.

The bank’s loan portfolio composition and deposit distribution are shown in the following balance sheet highlights:

During the quarter, First BanCorp executed several capital management initiatives, including the redemption of $50.6 million in junior subordinated debentures, repurchase of $21.8 million in common stock, and declaration of $29.6 million in common stock dividends. Despite these actions, the bank’s capital position remains strong, with tangible book value per share growing by 7.4% to $10.64 and the tangible common equity ratio reaching 9.1%.

Forward-Looking Statements

First BanCorp management maintains a positive outlook for 2025, despite some caution regarding U.S. macroeconomic uncertainties. The bank expects to benefit from Puerto Rico’s continued economic resilience, supported by disaster relief funds and a stable labor market.

CEO Aurelio Alemán highlighted stability in the Florida market during the earnings call and expressed optimism regarding consumer credit metrics. "We continue to see Florida as a healthy portfolio," he noted, while emphasizing expectations for improvement in consumer credit charge-offs.

The bank maintains its mid-single-digit loan growth target for 2025, with expectations for more significant growth in the latter half of the year. With a P/E ratio of 10.62 and a return on equity of 19%, First BanCorp demonstrates strong fundamentals that position it well for continued performance.

Despite the positive earnings surprise, First BanCorp’s stock experienced a slight decline of 0.36% in pre-market trading, closing at $19.58, which may reflect broader economic concerns or investor caution regarding future growth prospects rather than company-specific issues.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.