Spain’s credit rating upgraded to ’A+’ by S&P on strong growth

Introduction & Market Context

First BanCorp (NYSE:FBP) presented its first quarter 2025 financial results on April 24, 2025, showcasing improved profitability metrics despite a challenging macroeconomic environment. The Puerto Rico-based financial institution reported steady business activity in its main market, even as the Puerto Rico Economic Activity Index showed a slight year-over-year decline of 0.8%.

The presentation highlighted the bank’s ability to maintain strong performance amid U.S. economic uncertainty, supported by continued disaster relief fund disbursements in Puerto Rico, which reached $3,492 million in 2024.

Quarterly Performance Highlights

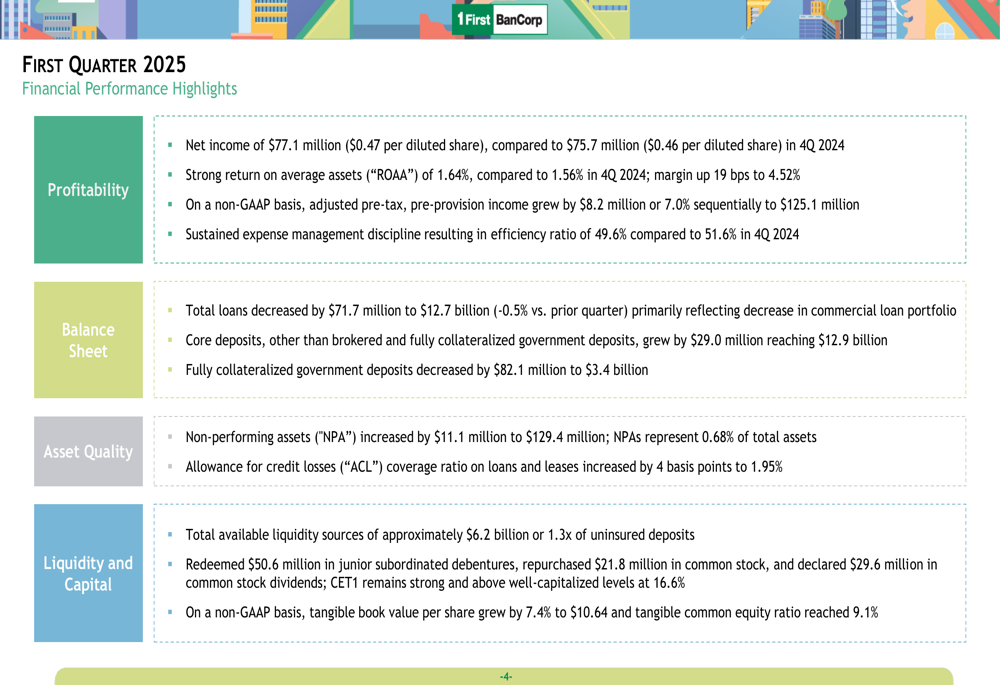

First BanCorp reported net income of $77.1 million ($0.47 per diluted share) for Q1 2025, an improvement from $75.7 million ($0.46 per diluted share) in Q4 2024. The bank achieved a strong return on average assets (ROAA) of 1.64%, up from 1.56% in the previous quarter, while its net interest margin expanded by 19 basis points to 4.52%.

As shown in the following comprehensive performance summary:

The bank’s efficiency ratio improved to 49.6% from 51.6% in the previous quarter, reflecting better operational performance. Adjusted pre-tax, pre-provision income grew by $8.2 million or 7.0% sequentially to $125.1 million, demonstrating the bank’s underlying earnings power before accounting for credit provisions.

Detailed Financial Analysis

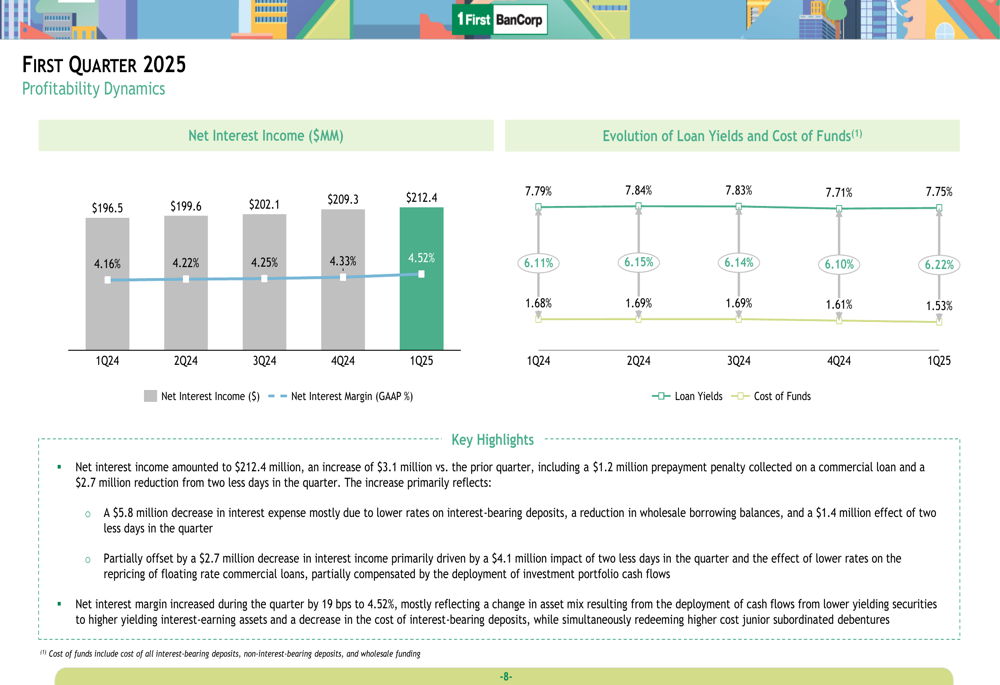

First BanCorp’s net interest income increased to $212.4 million in Q1 2025, up from $209.3 million in Q4 2024 and $196.5 million in Q1 2024. This improvement was partly driven by a $1.2 million prepayment penalty collected on a commercial loan, partially offset by a $2.7 million reduction from having two fewer days in the quarter.

The following chart illustrates the bank’s net interest income trend and the evolution of loan yields versus cost of funds:

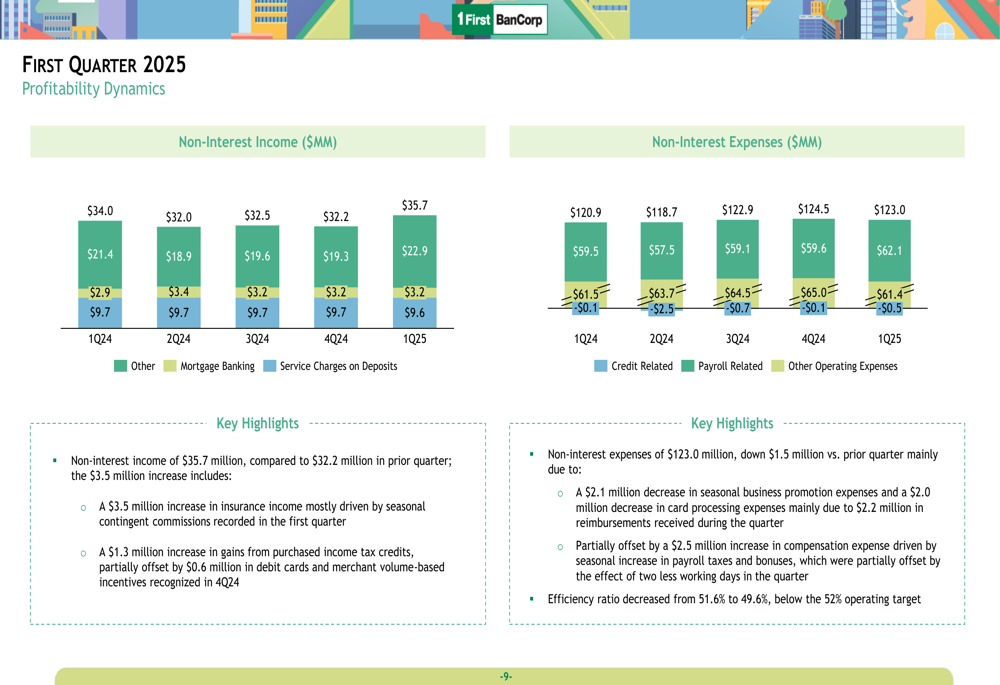

Non-interest income rose to $35.7 million in Q1 2025 from $32.2 million in the previous quarter, while non-interest expenses decreased by $1.5 million to $123.0 million. The expense reduction was primarily due to a $2.1 million decrease in seasonal business promotion expenses and a $2.0 million decrease in card processing expenses.

The breakdown of non-interest income and expenses is shown below:

Asset Quality and Capital Position

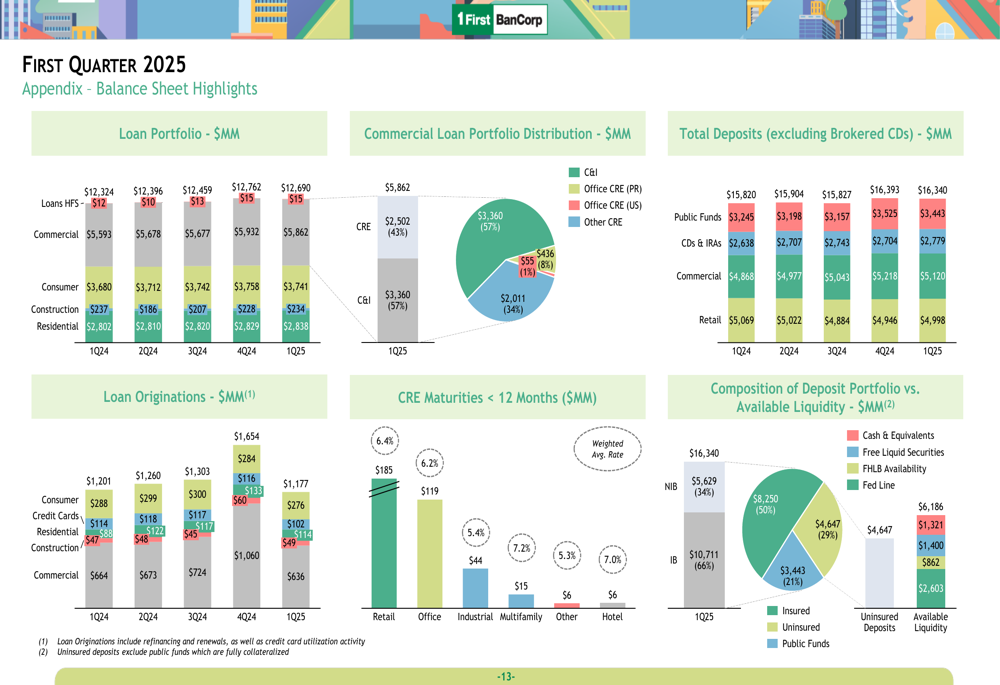

Total (EPA:TTEF) loans decreased slightly by $71.7 million to $12.7 billion, representing a 0.5% reduction compared to the previous quarter. However, core deposits grew by $29.0 million, reaching $12.9 billion.

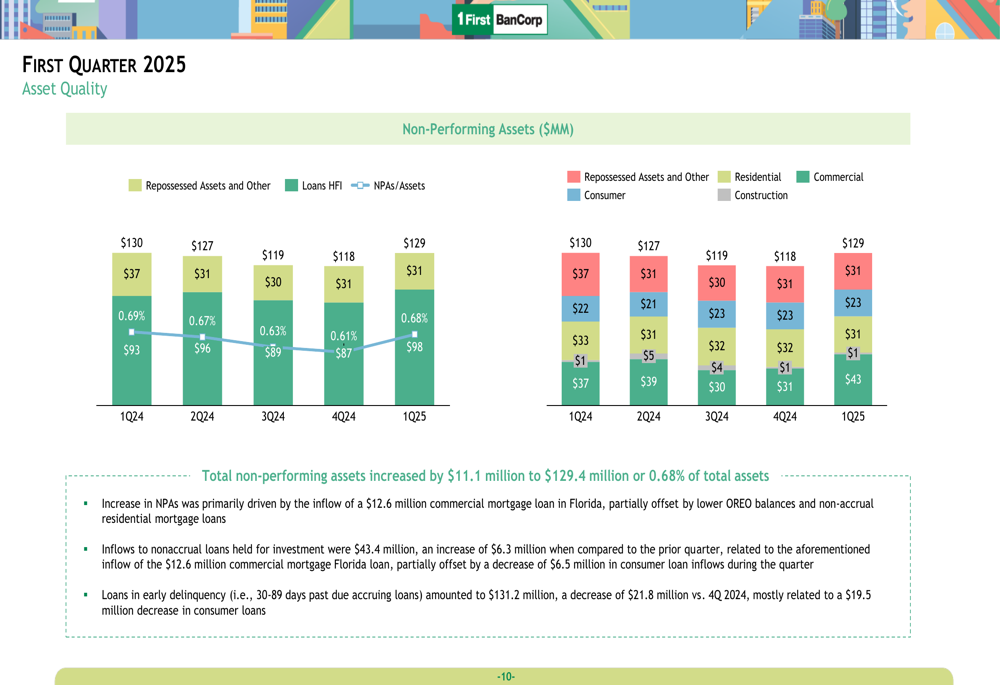

Non-performing assets increased by $11.1 million to $129.4 million, representing 0.68% of total assets. This increase was primarily driven by the inflow of a $12.6 million commercial mortgage loan in Florida, as illustrated in the following chart:

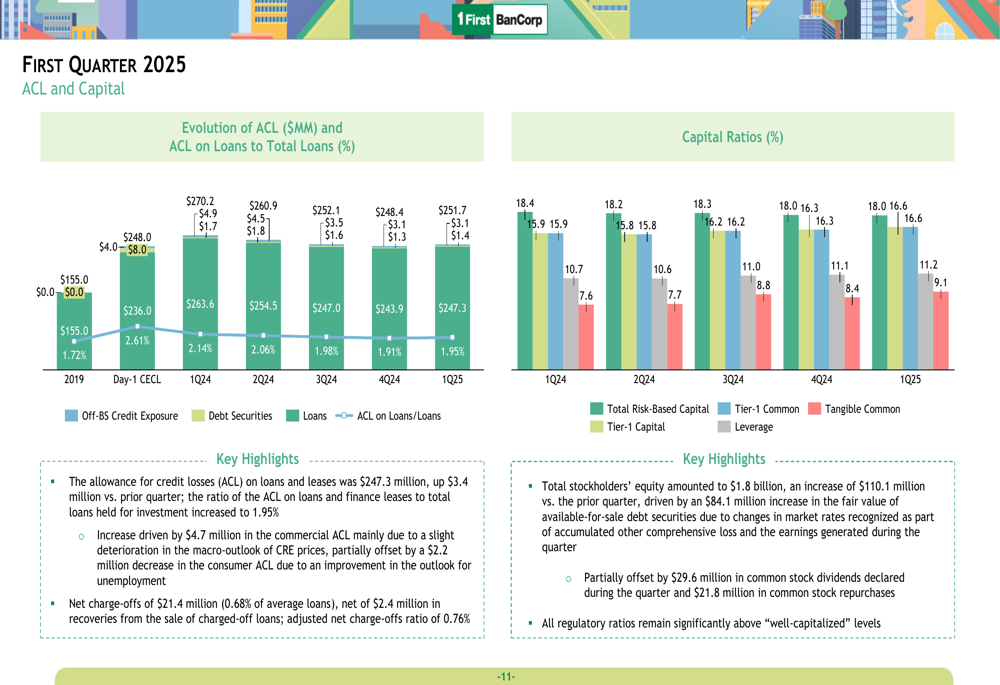

The bank maintained a strong capital position, with a CET1 ratio of 16.6%. During the quarter, First BanCorp redeemed $50.6 million in junior subordinated debentures, repurchased $21.8 million in common stock, and declared $29.6 million in common stock dividends. The tangible book value per share grew by 7.4% to $10.64, while the tangible common equity ratio reached 9.1%.

The evolution of the Allowance for Credit Losses (ACL) and key capital ratios is shown below:

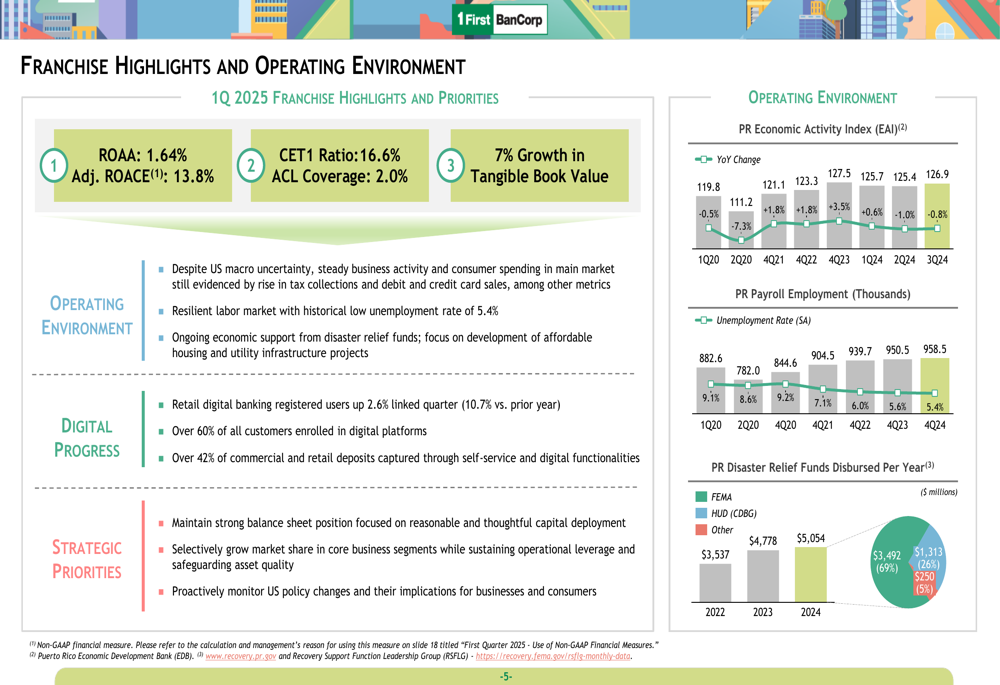

Puerto Rico Market Conditions

First BanCorp operates primarily in Puerto Rico, where economic conditions have remained relatively stable despite some challenges. The bank’s franchise highlights showed continued growth in digital banking, with registered users increasing by 2.6% quarter-over-quarter and 10.7% year-over-year.

The following slide illustrates key economic indicators for Puerto Rico, including the Economic Activity Index, payroll employment, and disaster relief fund disbursements:

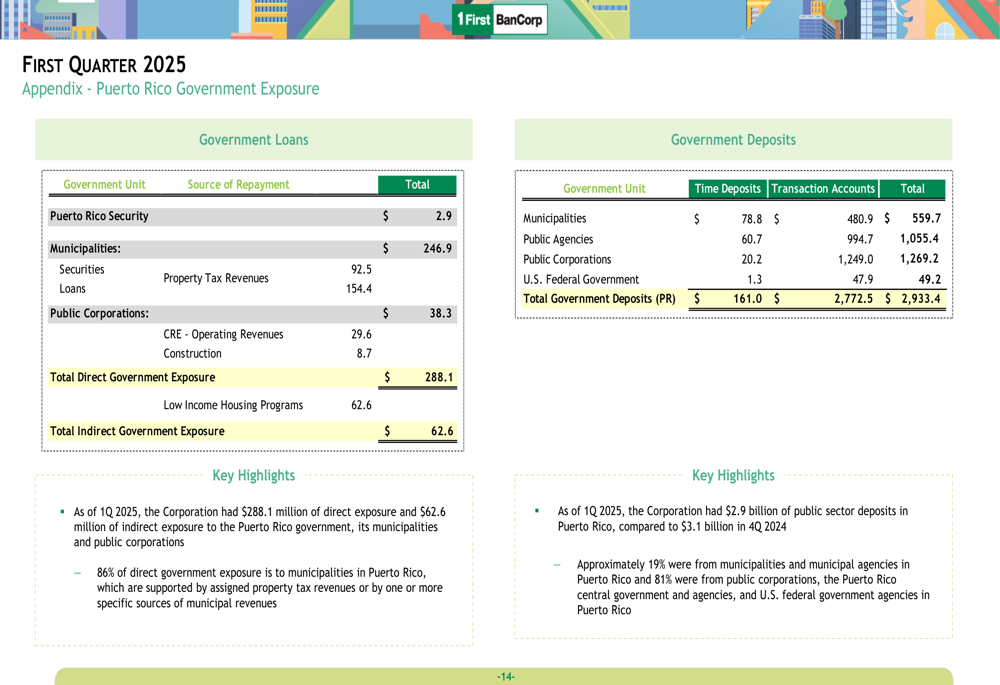

The bank maintains significant exposure to the Puerto Rico government, with $288.1 million in direct exposure and $62.6 million in indirect exposure as of Q1 2025. Public sector deposits in Puerto Rico totaled $2.9 billion, down from $3.1 billion in the previous quarter.

The breakdown of government exposure is detailed below:

Balance Sheet and Liquidity Position

First BanCorp’s balance sheet remains robust, with a well-diversified loan portfolio and strong liquidity position. The bank’s commercial real estate (CRE) portfolio had a weighted average rate of 6.4%, while its deposit portfolio provided substantial available liquidity of $6.2 billion.

The following slide provides a comprehensive overview of the bank’s balance sheet highlights:

Forward-Looking Statements

While First BanCorp did not provide specific forward guidance in the presentation, the bank’s strong capital position and improving profitability metrics suggest it is well-positioned to navigate potential economic challenges. The continued disbursement of disaster relief funds in Puerto Rico is expected to provide ongoing support to the local economy, benefiting the bank’s operations.

The bank’s focus on efficiency improvement and digital banking growth indicates a strategic emphasis on operational excellence and technological advancement. With a tangible book value per share that grew 7.4% and a robust capital base, First BanCorp appears well-equipped to pursue both organic growth opportunities and potential capital returns to shareholders in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.