Aston Martin cuts 2025 volume and profit guidance amid weak demand, tariff risks

Introduction & Market Context

First BanCorp (NYSE:FBP), the bank holding company for FirstBank Puerto Rico, presented its second quarter 2025 financial results on July 22, showing continued profitability growth amid favorable economic conditions in its primary market. The stock experienced mixed trading, with premarket gains of 4.07% giving way to a 1.69% decline during the regular session, closing at $21.49.

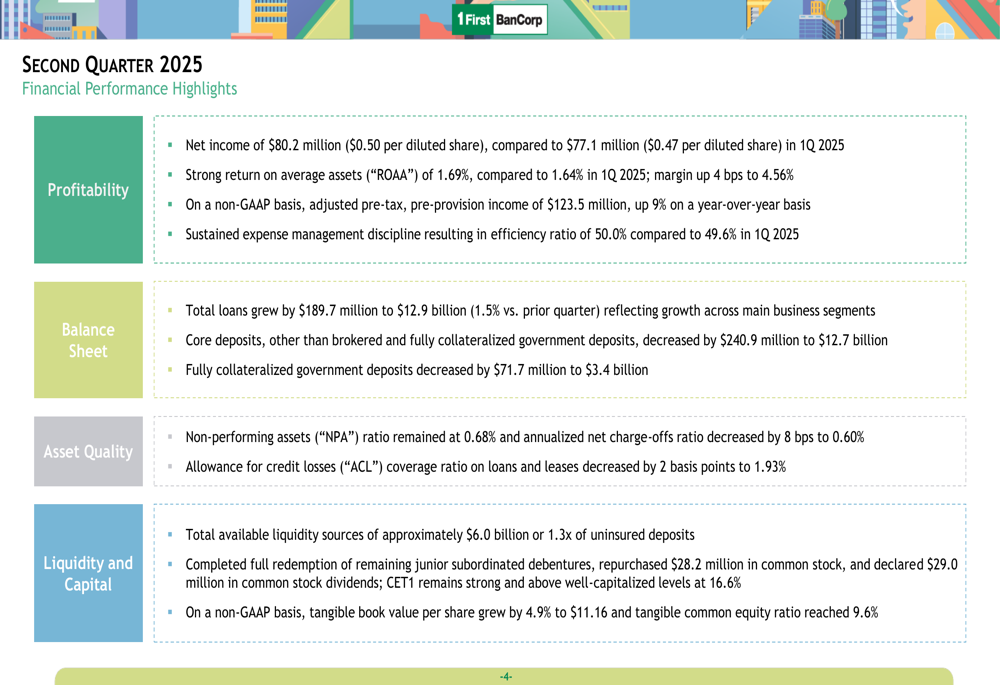

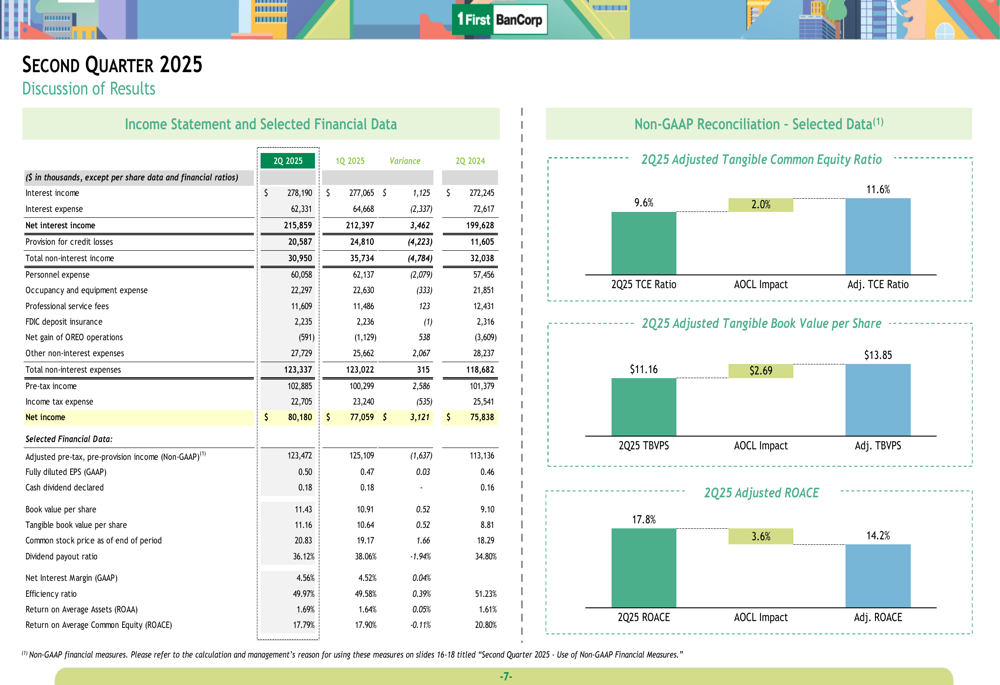

The bank reported net income of $80.2 million ($0.50 per diluted share) for Q2 2025, exceeding both the previous quarter’s $77.1 million ($0.47 per diluted share) and analyst expectations. This performance builds on the momentum from Q1 2025, when the company also beat forecasts with EPS of $0.46 against a projected $0.43.

Quarterly Performance Highlights

First BanCorp delivered strong financial results across key metrics, with notable improvements in profitability, asset quality, and capital position. The bank achieved a return on average assets (ROAA) of 1.69%, up from 1.64% in the previous quarter, while maintaining an efficiency ratio of 50.0%.

As shown in the following comprehensive overview of the quarter’s performance:

Loan growth was a significant driver of the quarter’s success, with total loans increasing by $189.7 million to $12.9 billion, representing a 1.5% growth compared to the prior quarter. This expansion occurred across the bank’s main business segments, supporting the company’s previously stated mid-single-digit loan growth target for 2025.

Despite the positive loan growth, core deposits decreased by $240.9 million to $12.7 billion, while fully collateralized government deposits declined by $71.7 million to $3.4 billion. This deposit contraction reflects broader industry challenges in maintaining deposit levels in the current rate environment.

Detailed Financial Analysis

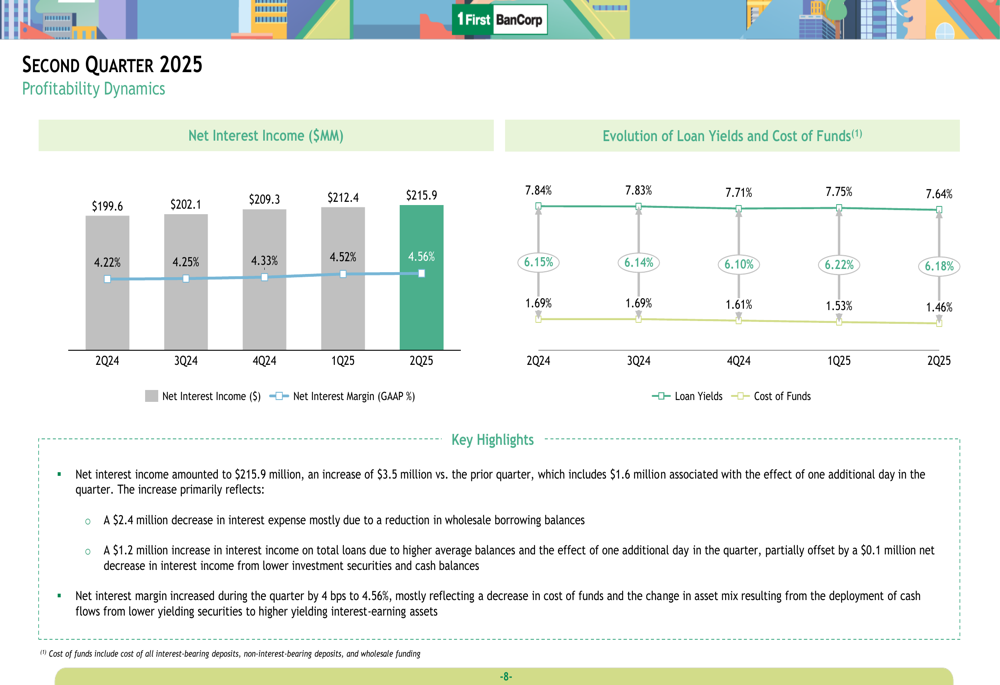

The bank’s income statement reveals solid performance with net interest income of $215.9 million in Q2 2025, compared to $199.6 million in the same quarter last year, representing an 8.2% year-over-year increase. On a non-GAAP basis, adjusted pre-tax, pre-provision income reached $123.5 million, up 9% year-over-year.

The following income statement details provide a comprehensive view of the bank’s financial performance:

Net interest margin expanded by 4 basis points to 4.56% during the quarter, primarily reflecting a decrease in the cost of funds. This improvement was driven by a $2.4 million decrease in interest expense mostly due to reduced wholesale borrowing balances, and a $1.2 million increase in interest income on total loans due to higher average balances.

As illustrated in the following chart showing the evolution of net interest income and margin:

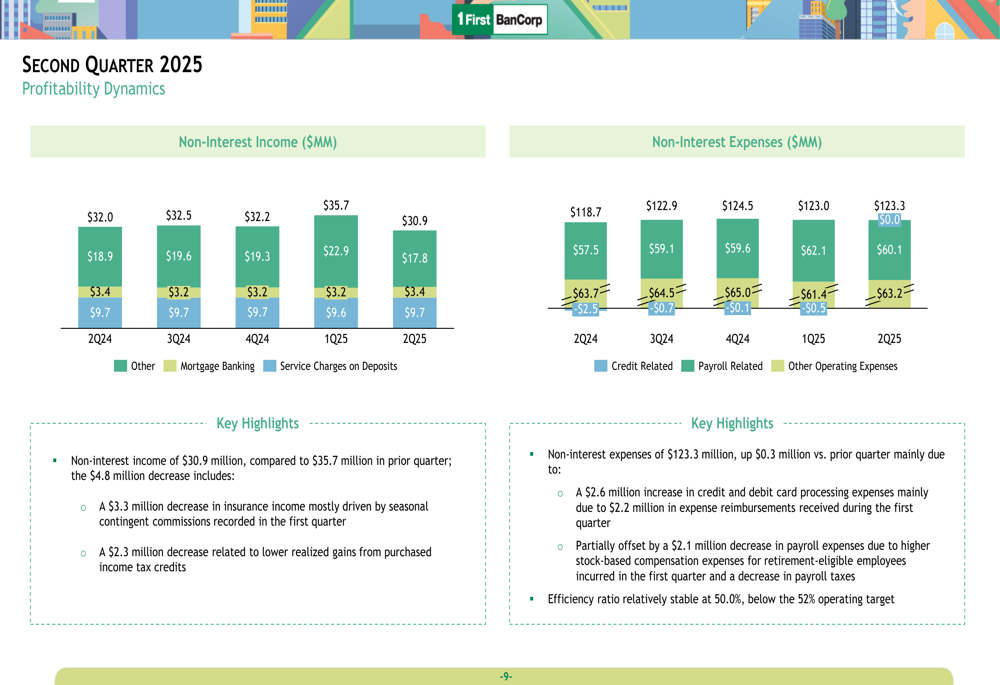

Non-interest income amounted to $30.9 million, compared to $35.7 million in the prior quarter. The $4.8 million decrease was primarily attributed to a $3.3 million reduction in insurance income, mostly driven by seasonal contingent commissions recorded in the first quarter, and a $2.3 million decrease related to lower realized gains from purchased income tax credits.

Non-interest expenses remained well-controlled at $123.3 million, up slightly by $0.3 million compared to the previous quarter. This increase was mainly due to a $2.6 million rise in credit and debit card processing expenses, partially offset by a $2.1 million decrease in payroll expenses.

The following breakdown illustrates the components of non-interest income and expenses:

Asset Quality & Capital Position

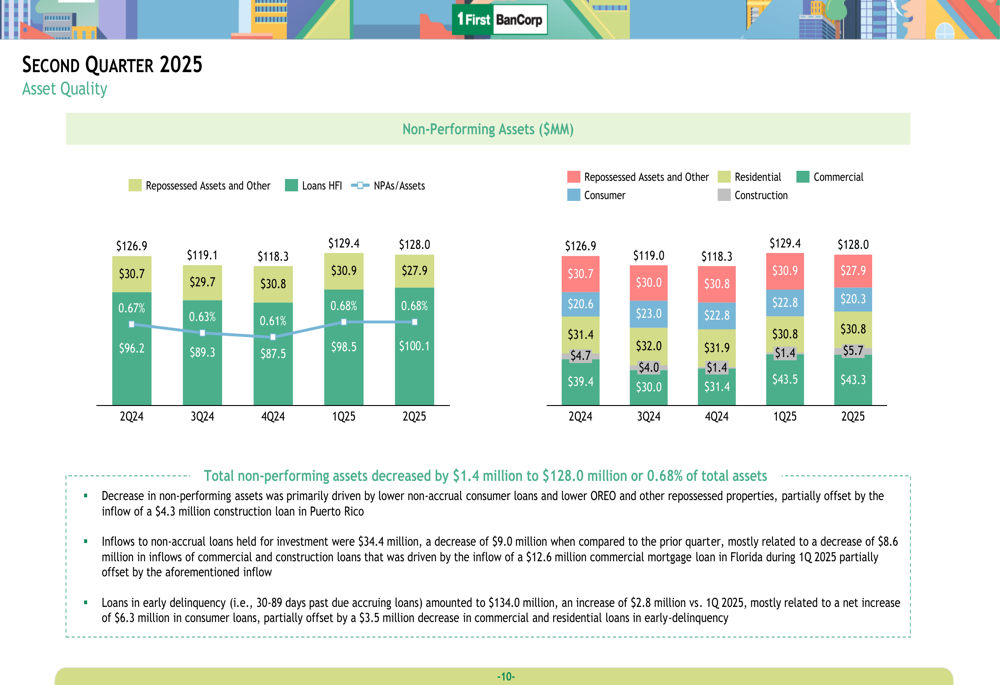

First BanCorp maintained stable asset quality metrics during the quarter, with the non-performing assets (NPA) ratio remaining unchanged at 0.68%. The annualized net charge-offs ratio improved by 8 basis points to 0.60%, indicating strengthening credit performance.

The following chart details the composition of non-performing assets:

Inflows to non-accrual loans held for investment were $34.4 million, a decrease of $9.0 million compared to the prior quarter. The decrease in non-performing assets was primarily driven by lower non-accrual consumer loans and reduced OREO (Other Real Estate Owned) and repossessed properties, partially offset by the inflow of a $4.3 million construction loan in Puerto Rico.

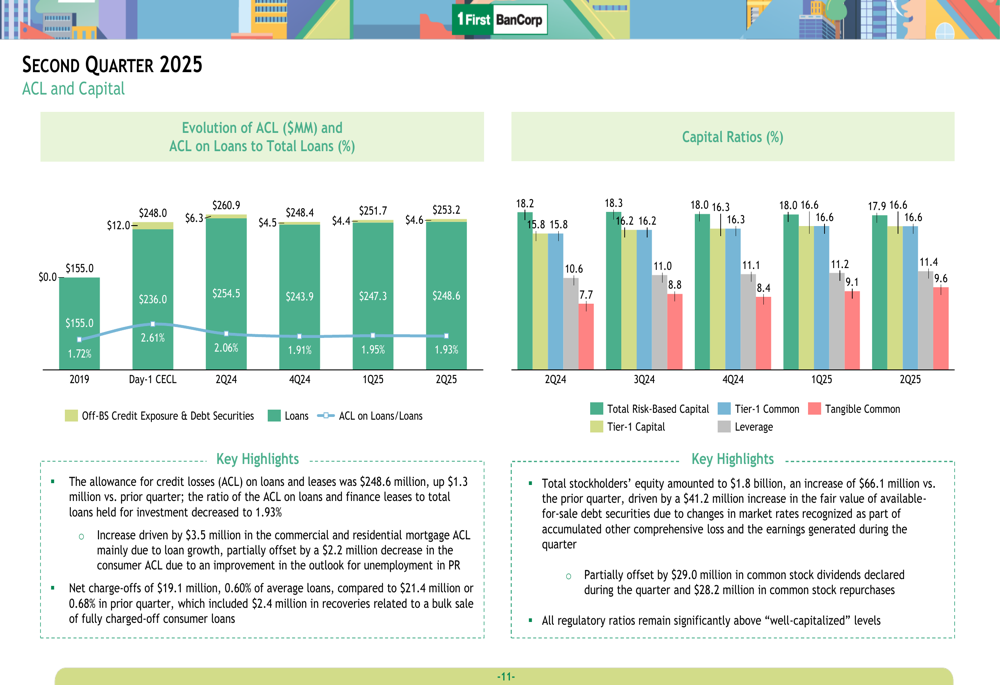

The bank’s capital position remains robust, with all regulatory ratios significantly above "well-capitalized" levels. The Common Equity Tier 1 (CET1) ratio stood at 16.6%, providing substantial flexibility for capital deployment and growth initiatives.

As shown in the following chart of capital ratios and allowance for credit losses:

The allowance for credit losses (ACL) on loans and leases was $248.6 million, a slight increase of $1.3 million compared to the previous quarter. However, the ratio of ACL to total loans held for investment decreased by 2 basis points to 1.93%, reflecting the bank’s confidence in its loan portfolio quality.

Strategic Initiatives & Economic Environment

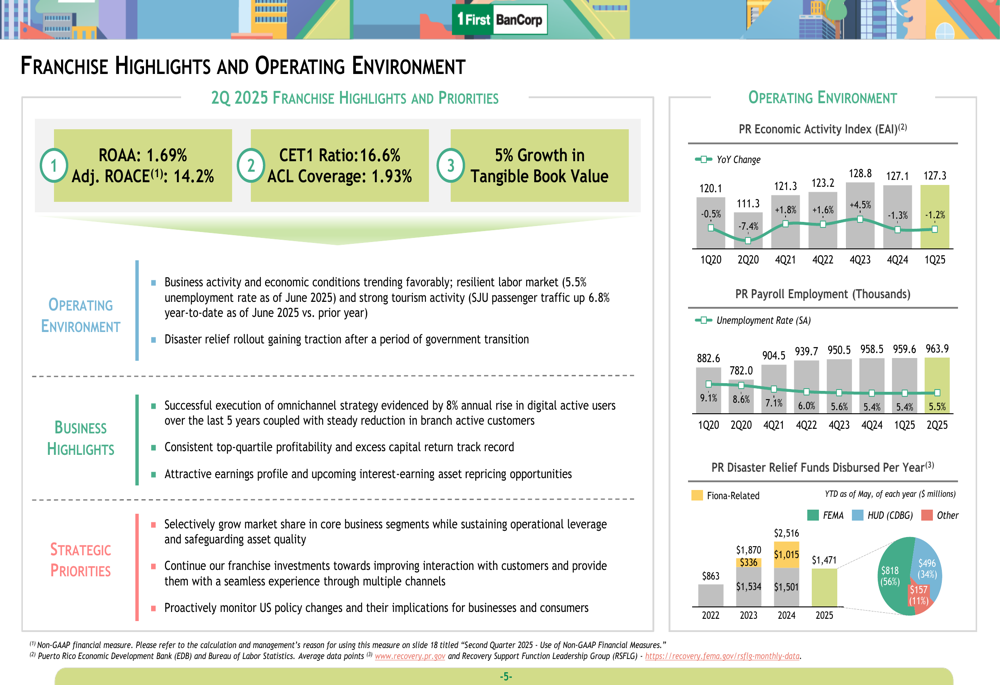

First BanCorp operates in a favorable economic environment in Puerto Rico, with improving economic indicators supporting business activity. The unemployment rate stood at 5.5% as of June 2025, and tourism activity remains strong with San Juan airport passenger traffic up 6.8% year-to-date compared to the prior year.

The following chart illustrates key economic indicators and strategic priorities:

The bank’s strategic priorities focus on selective market share growth while maintaining operational leverage and safeguarding asset quality. Management also emphasized continued investments in the franchise to improve customer interaction and provide seamless experiences across multiple channels.

Disaster relief funding in Puerto Rico is gaining traction after a period of government transition, with significant funds being disbursed across various programs. This influx of capital is expected to further stimulate economic activity in the bank’s primary market.

First BanCorp completed several capital management initiatives during the quarter, including the full redemption of remaining junior subordinated debentures, repurchase of $28.2 million in common stock, and declaration of $29.0 million in common stock dividends. These actions, combined with the 4.9% growth in tangible book value per share to $11.16, demonstrate the bank’s commitment to enhancing shareholder value while maintaining strong capital levels.

As First BanCorp moves into the second half of 2025, it remains well-positioned to capitalize on favorable economic conditions in Puerto Rico while navigating potential challenges from U.S. policy changes and their implications for businesses and consumers.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.