JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

First Citizens BancShares Inc (NASDAQ:FCNCA) presented its first quarter 2025 earnings results on April 24, showing solid deposit growth that exceeded expectations, while net interest margin continued to compress. The bank reported adjusted earnings per share of $37.79, down from $45.10 in the previous quarter, reflecting the challenging interest rate environment.

The stock has shown resilience in 2025, trading at $1,772.04 as of April 23, up 2.16% on the day and well above its 52-week low of $1,473.62, though still below its 52-week high of $2,412.93. In premarket trading on April 24, shares were up 0.45% to $1,780.

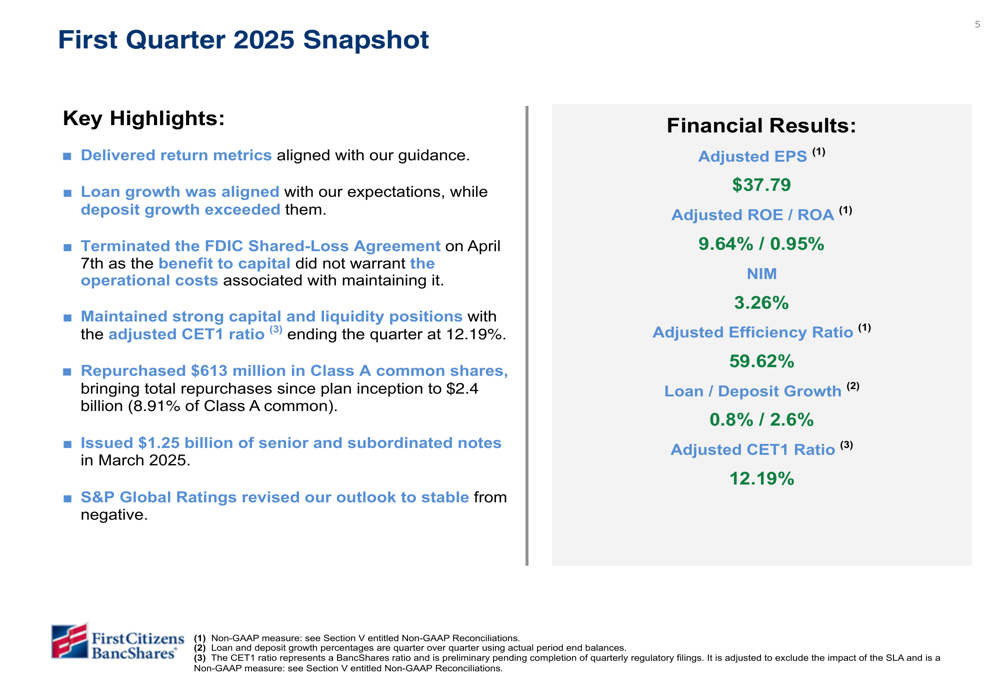

As shown in the following snapshot of the quarter’s performance, First Citizens maintained solid return metrics while continuing to execute on its share repurchase program:

Quarterly Performance Highlights

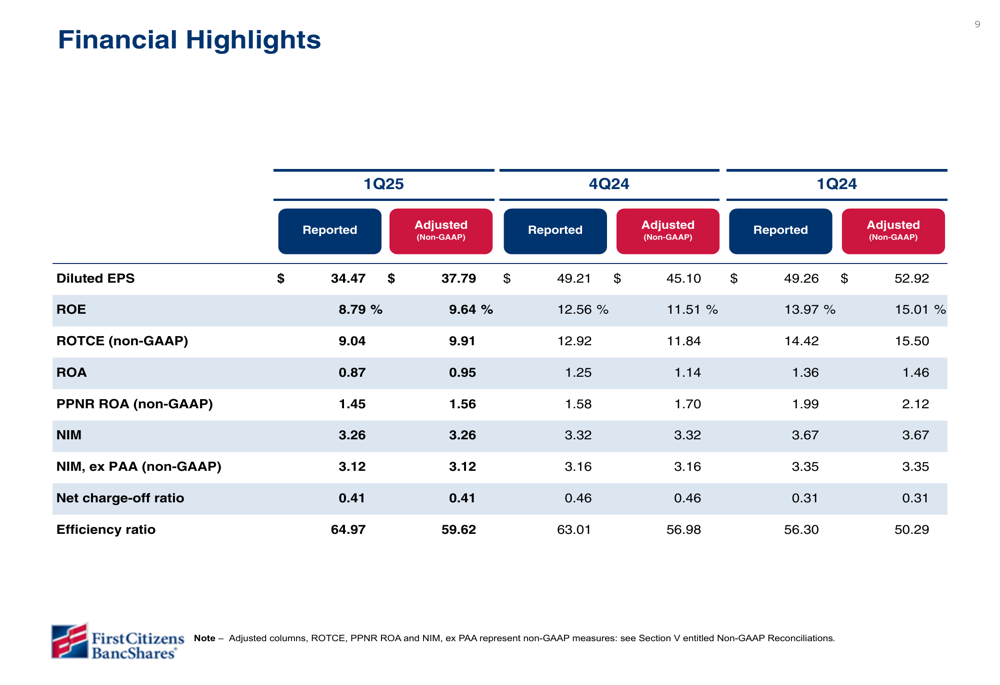

First Citizens reported adjusted earnings per share of $37.79 for Q1 2025, representing a decline from $45.10 in Q4 2024 and $52.92 in Q1 2024. The company’s adjusted return on equity was 9.64%, down from 11.51% in the previous quarter and 15.01% in the same quarter last year.

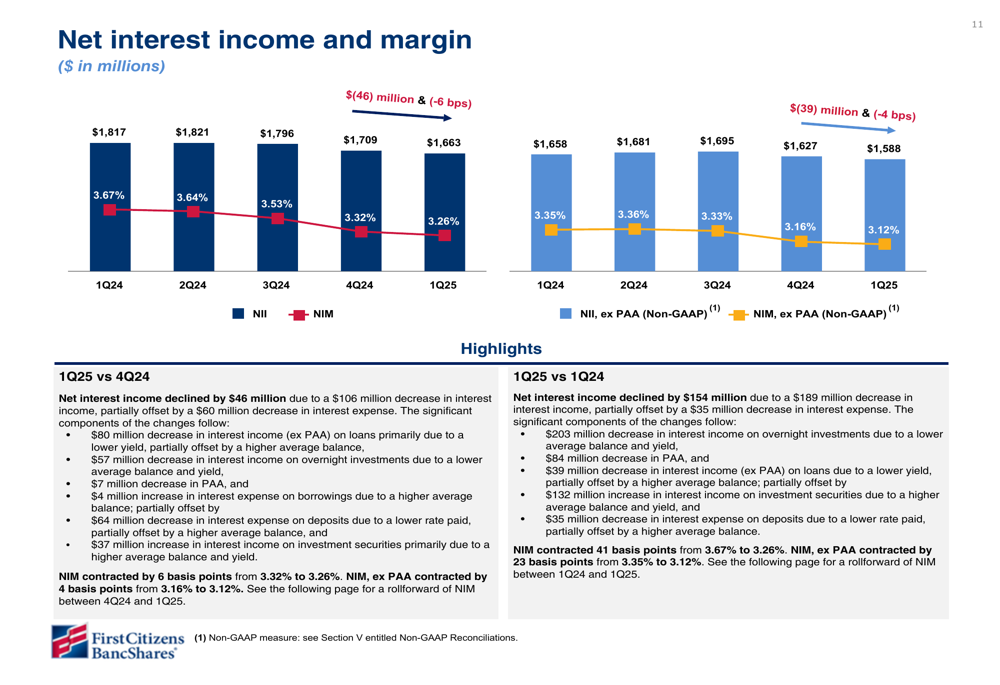

Net interest income decreased to $1.66 billion from $1.71 billion in Q4 2024 and $1.82 billion in Q1 2024, reflecting continued margin pressure. The net interest margin was 3.26%, down from 3.32% in Q4 2024 and 3.67% in Q1 2024.

The following table highlights key financial metrics compared to previous quarters:

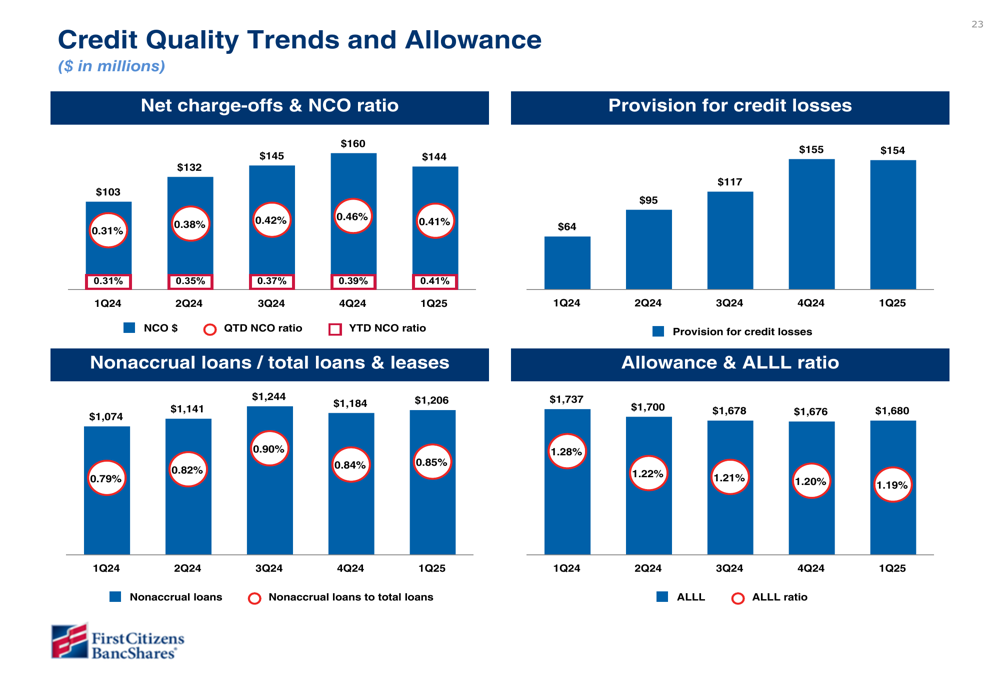

Despite the challenging interest rate environment, First Citizens maintained a solid efficiency ratio of 59.62% on an adjusted basis. The company’s net charge-off ratio improved to 0.41% from 0.46% in the previous quarter.

The bank’s net interest income and margin trends reflect the ongoing pressure from the interest rate environment, though the pace of decline has moderated:

Balance Sheet and Credit Quality

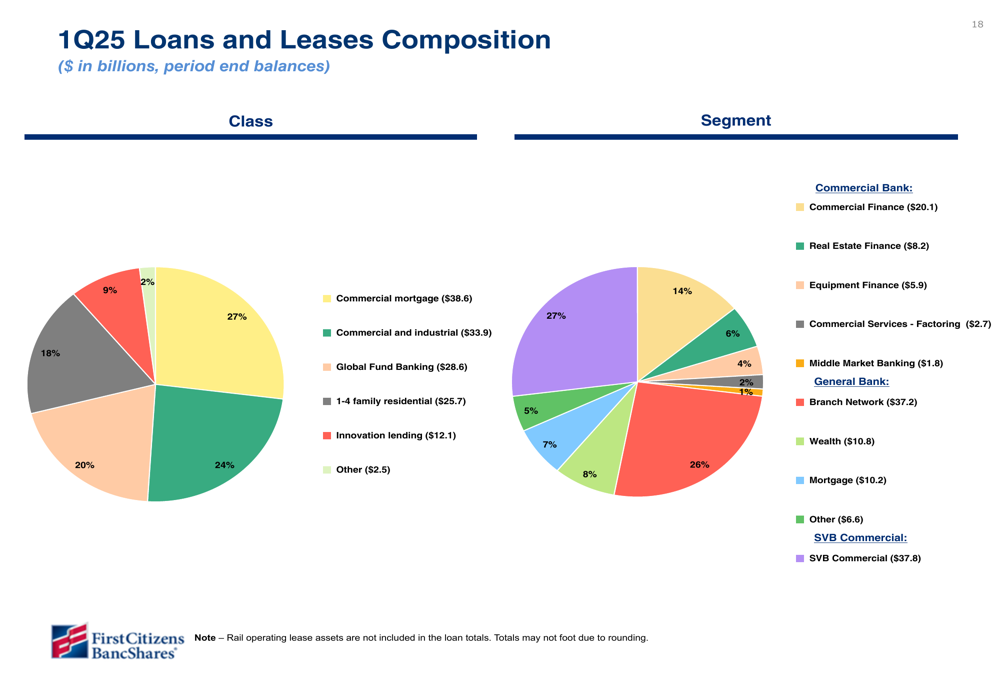

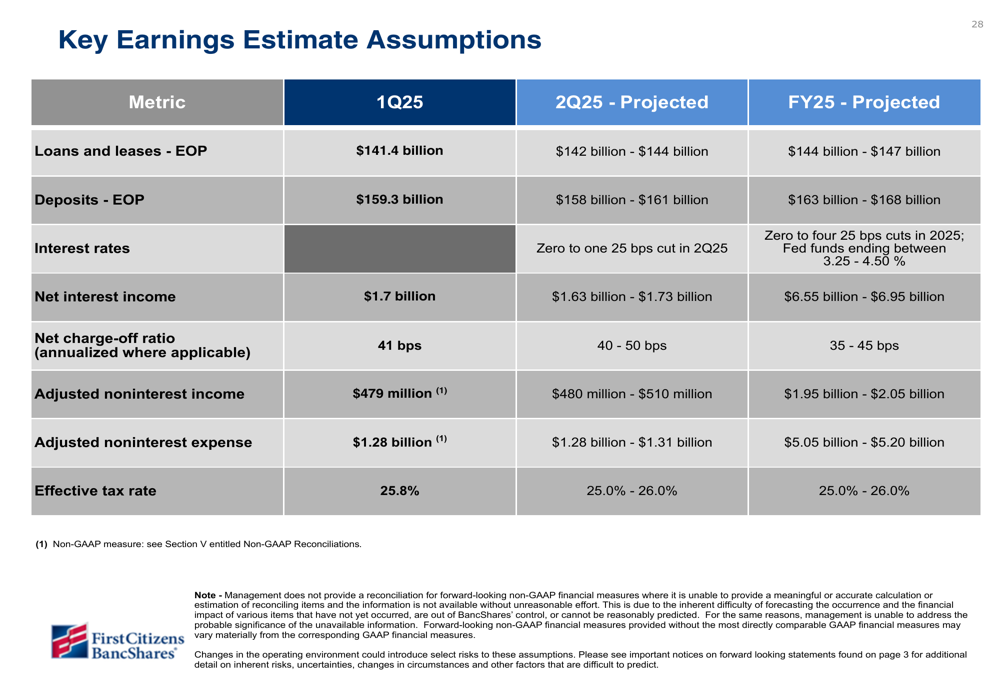

First Citizens reported loan growth of 0.8% (3.3% annualized) in Q1 2025, with total loans reaching $141.4 billion. The growth was primarily driven by the Commercial Bank segment, which increased by $733 million, and the SVB Commercial segment, which grew by $444 million.

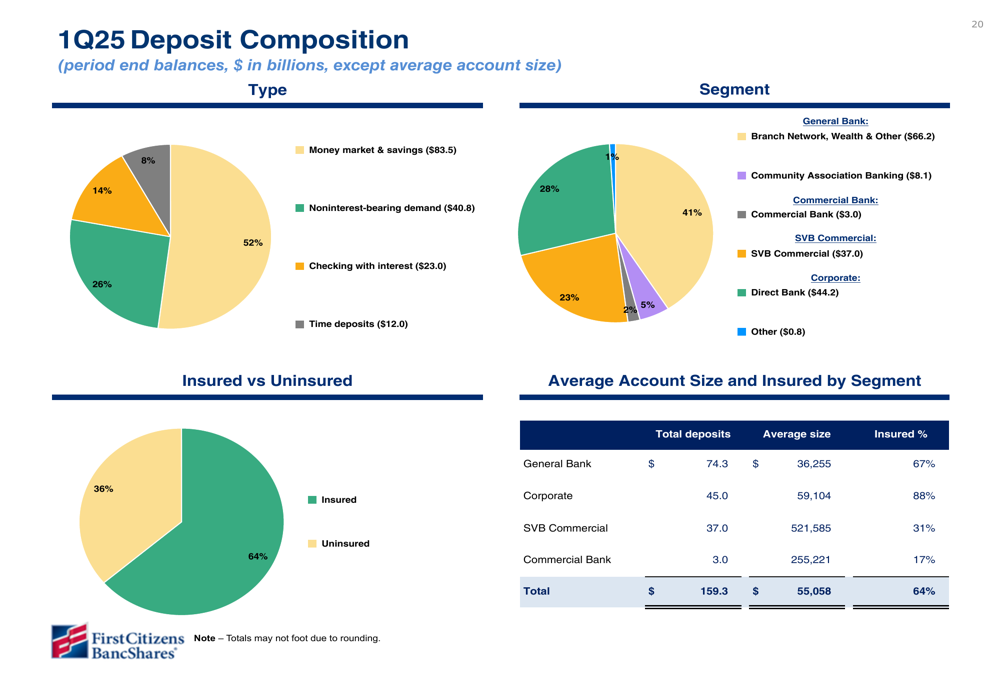

Deposit growth was particularly strong at 2.6% (10.7% annualized), exceeding management’s guidance. Total (EPA:TTEF) deposits reached $159.3 billion, with growth driven by a $3.1 billion increase in the Direct Bank and a $1.4 billion increase in the General Bank segment.

The following chart shows the composition of the bank’s loan portfolio as of Q1 2025:

Deposit composition remained healthy with 64% of deposits insured. The bank’s deposit mix shows a strong foundation of stable funding sources:

Credit quality remained stable in Q1 2025, with nonaccrual loans at 0.85% of total loans, slightly up from 0.84% in Q4 2024. The allowance for loan and lease losses stood at $1.68 billion, representing 1.19% of total loans. The following chart illustrates the bank’s credit quality trends:

Capital Management and Share Repurchases

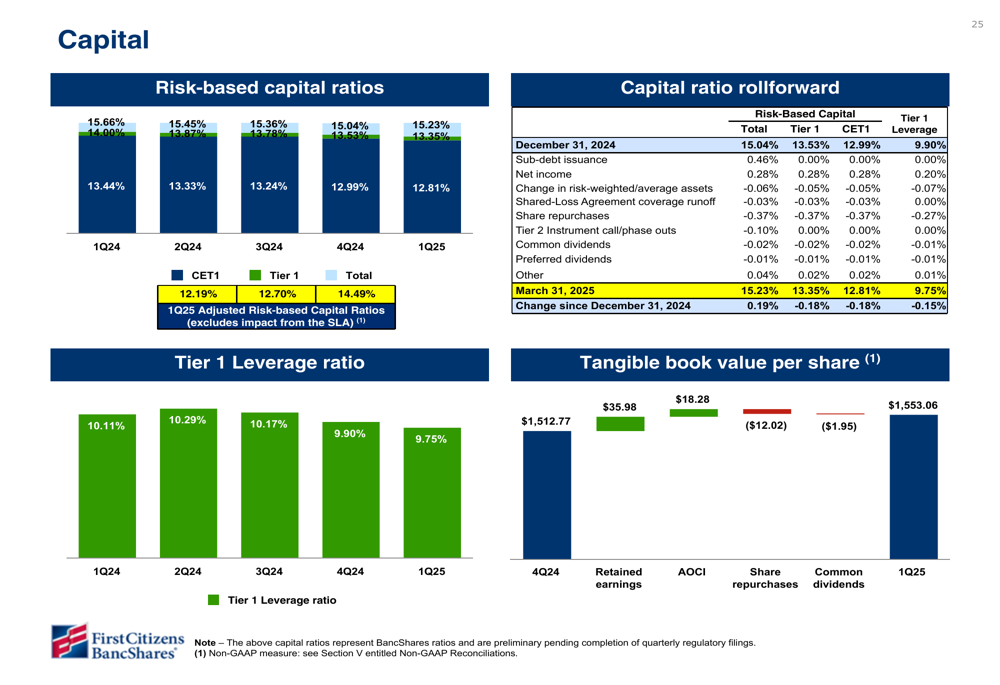

First Citizens maintained strong capital levels with a CET1 ratio of 12.81%, though this represents a slight decline from 12.99% in Q4 2024 and 13.44% in Q1 2024. The bank’s total risk-based capital ratio was 15.23%, up from 15.04% in the previous quarter.

The following chart shows the bank’s capital position over time:

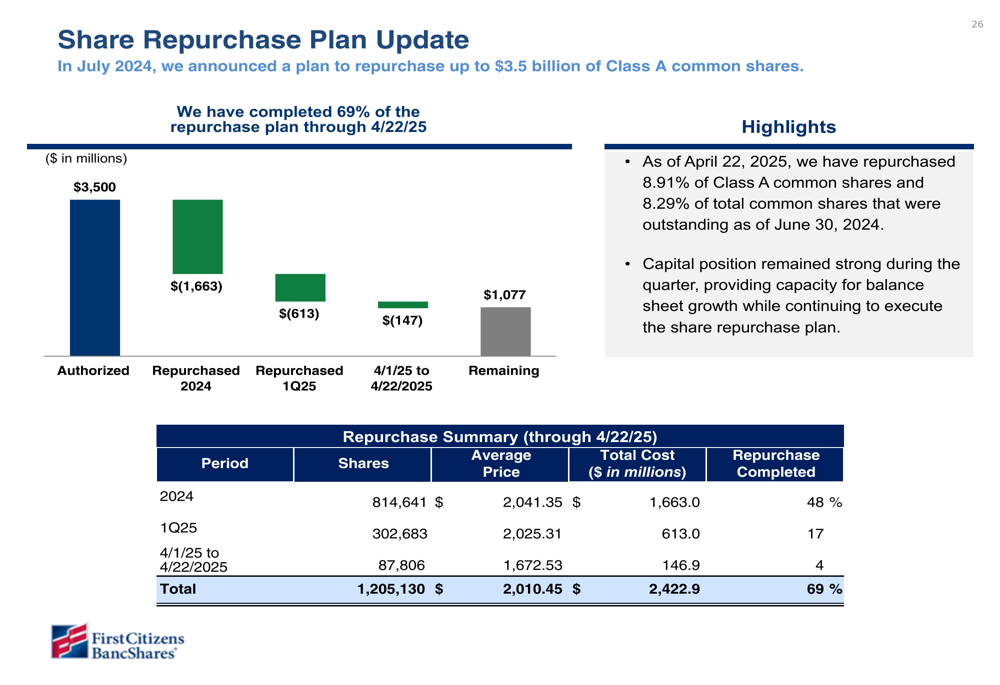

The company continued its share repurchase program, buying back $613 million in Class A common shares during Q1 2025. As of April 22, 2025, First Citizens had repurchased a total of $2.42 billion in shares, representing 69% of its authorized plan and 8.91% of Class A common shares outstanding as of June 30, 2024.

The progress of the share repurchase program is illustrated below:

Strategic Initiatives and Outlook

First Citizens outlined four strategic priorities for 2025: client focus, talent & culture, operational efficiency, and balance sheet optimization, all underpinned by risk management:

For the remainder of 2025, the bank provided guidance expecting loan growth to reach $144-147 billion by year-end, with deposits projected to grow to $163-168 billion. The company anticipates zero to four 25 basis point rate cuts in 2025, with the Federal funds rate ending between 3.25-4.50%.

Net interest income is expected to be between $6.55-6.95 billion for the full year, while the net charge-off ratio is projected to be 35-45 basis points. The following table details the bank’s key earnings assumptions:

First Citizens also noted several significant developments during the quarter, including the termination of the FDIC Shared-Loss Agreement on April 7th and the issuance of $1.25 billion of senior and subordinated notes in March 2025. Additionally, S&P Global Ratings revised the bank’s outlook to stable from negative, reflecting improved financial stability.

The bank’s solid deposit growth and stable credit quality position it well for the remainder of 2025, though margin pressure is likely to continue as the interest rate environment evolves.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.