AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

First Commonwealth Financial Corporation (NYSE:FCF) presented its first quarter 2025 earnings results on April 30, showing the regional bank met analyst expectations with earnings per share of $0.32. Despite meeting forecasts, the stock experienced downward pressure, falling 2% to $15.66 as of the most recent trading data, reflecting broader market concerns about regional banks.

The Pennsylvania-based financial institution demonstrated resilience in its core banking operations with expanding net interest margin and solid loan growth, even as it navigated headwinds from decreased fee income and rising operational expenses.

Quarterly Performance Highlights

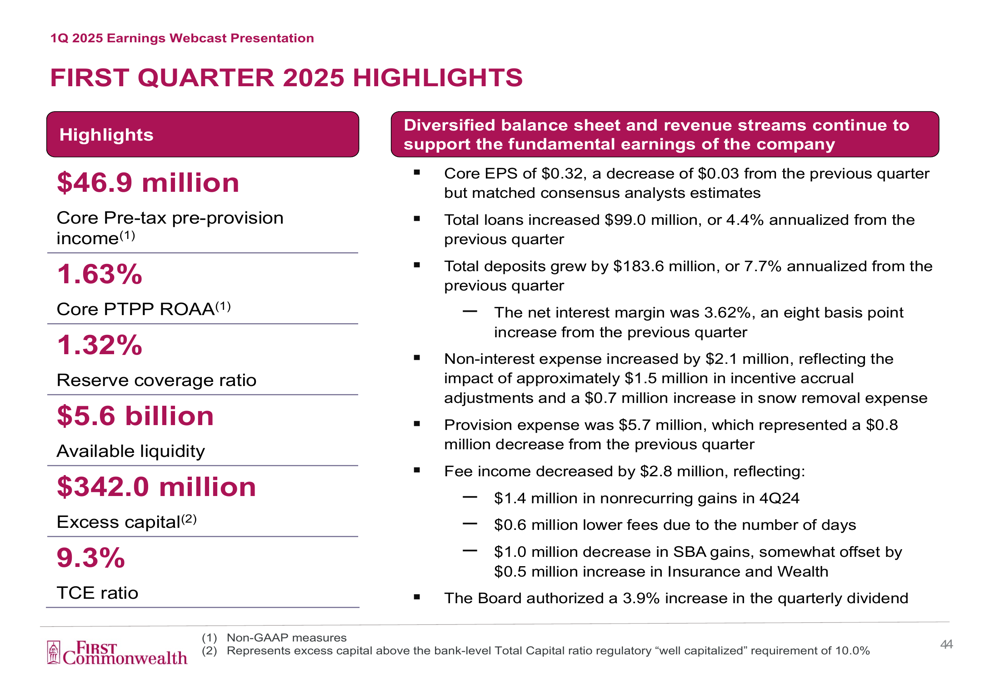

First Commonwealth reported core earnings per share of $0.32 for Q1 2025, matching analyst expectations. The bank’s loan portfolio expanded by $99.0 million (4.4% annualized), while deposits grew at an even stronger pace of $183.6 million (7.7% annualized).

As shown in the following quarterly highlights slide, the bank maintained strong capital and liquidity positions with $5.6 billion in available liquidity and $342 million in excess capital:

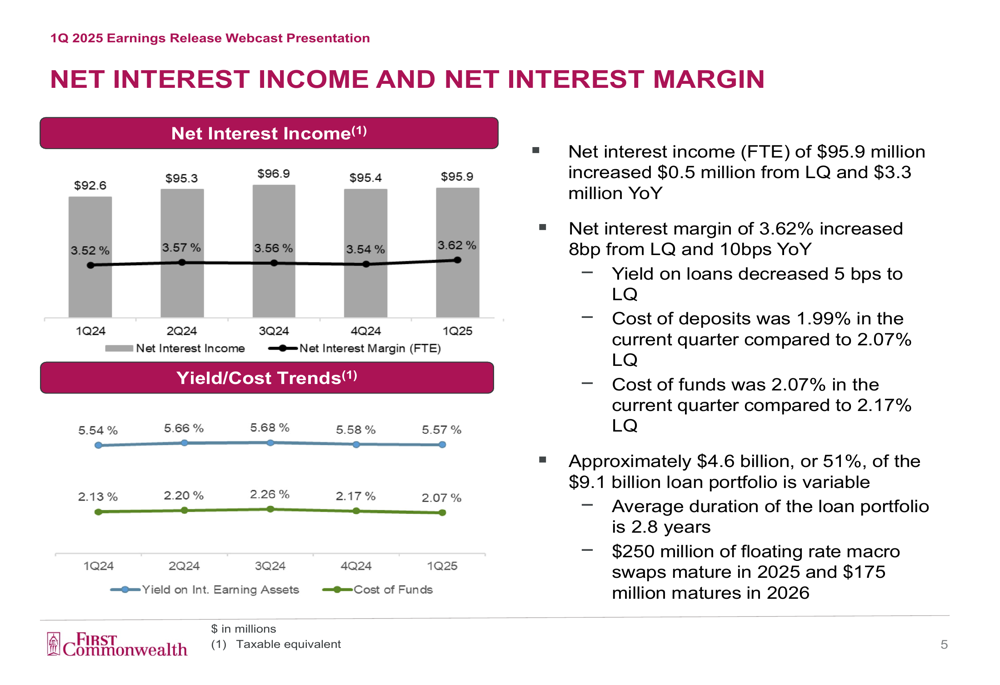

Net interest margin, a critical profitability metric for banks, improved to 3.62%, increasing 8 basis points from the previous quarter and 10 basis points year-over-year. This margin expansion helped offset challenges in non-interest income, which decreased by $2.8 million compared to the previous quarter.

The following chart illustrates the bank’s net interest income and margin trends over the past five quarters:

Detailed Financial Analysis

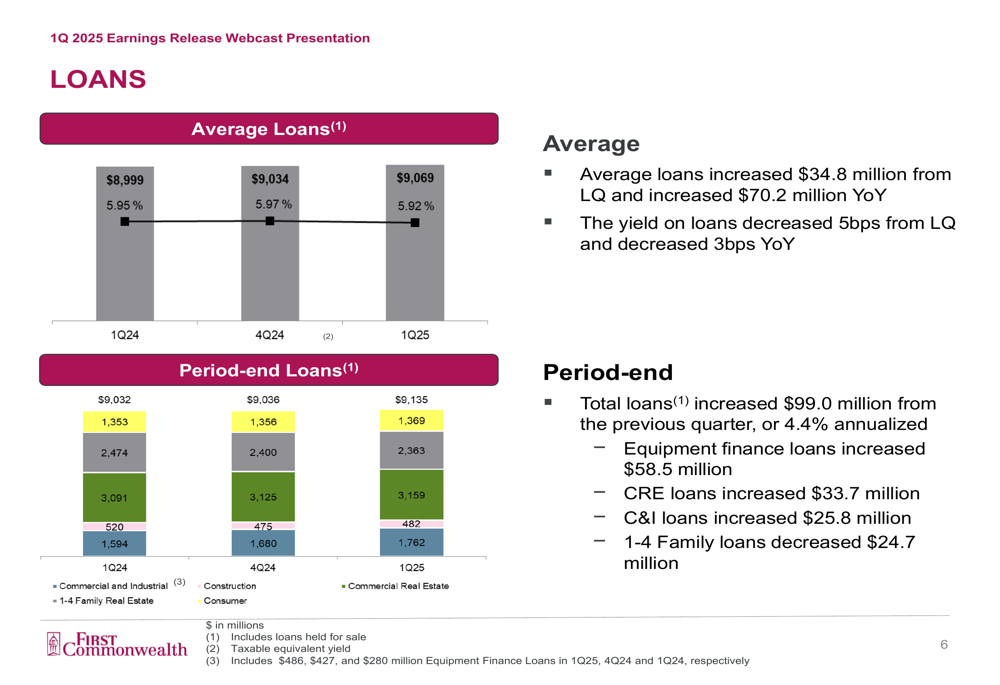

First Commonwealth’s loan growth was primarily driven by commercial lending, with equipment finance loans increasing $58.5 million and commercial real estate loans growing by $33.7 million. However, residential mortgage loans decreased by $24.7 million, reflecting the challenging interest rate environment for housing.

The loan portfolio breakdown and growth trends are illustrated in this slide:

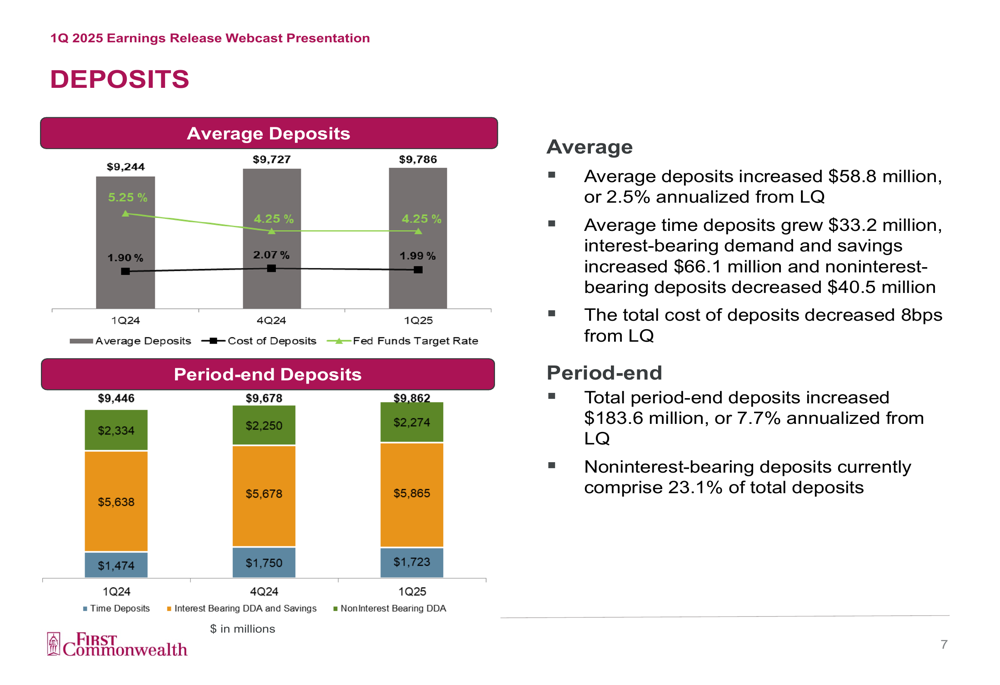

On the funding side, the bank’s deposit base showed healthy growth with period-end deposits increasing $183.6 million from the previous quarter. The cost of deposits decreased 8 basis points to 1.99%, contributing to the improved net interest margin. Notably, non-interest bearing deposits, which represent 23.1% of total deposits, decreased slightly, reflecting industry-wide pressure on these low-cost funding sources.

The deposit composition and trends are shown in the following slide:

Fee income represented a challenging area, decreasing $2.5 million from the previous quarter and $1.3 million year-over-year. A significant factor was the $3.0 million year-over-year decrease in card-related interchange revenue due to the Durbin Amendment becoming effective in July 2024. Additionally, gain on sale of SBA (LON:SBA) loans decreased $1.0 million from the previous quarter.

Non-interest expenses increased $2.0 million from the previous quarter, primarily due to a $2.4 million increase in salaries and benefits, including $1.5 million attributed to finalizing prior year incentive payouts. Occupancy expenses also rose by $0.9 million, with $0.7 million related to increased snow removal costs.

Strategic Initiatives

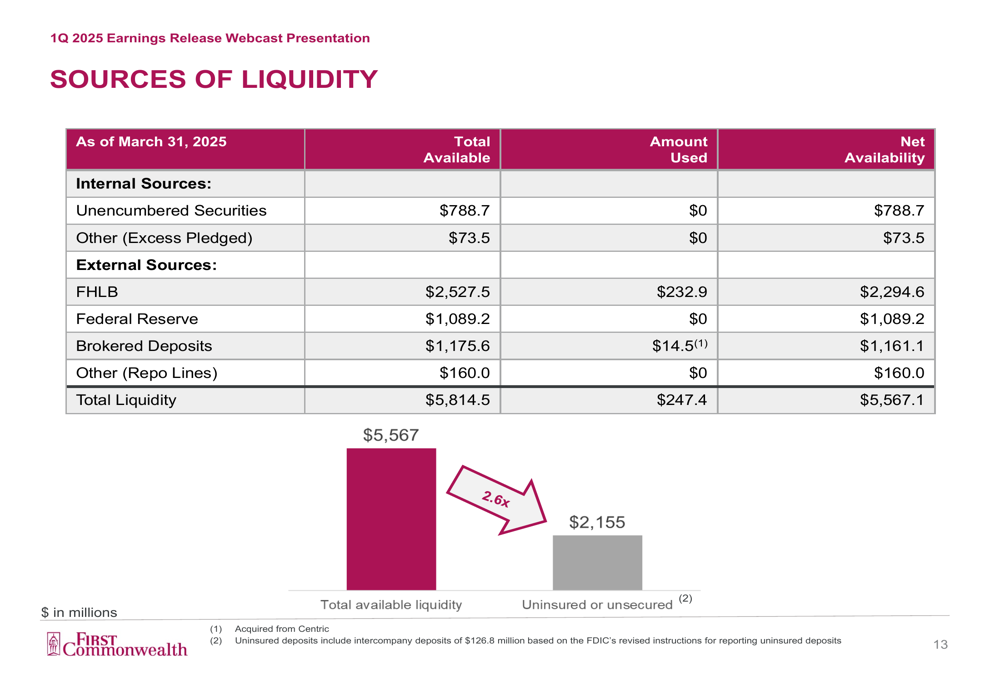

First Commonwealth maintains a strong focus on credit quality and liquidity management. The bank’s provision expense decreased $0.8 million from the previous quarter to $5.7 million, primarily due to a $10.6 million decrease in net charge-offs. The allowance for credit losses remained stable at 1.32% of total loans.

The bank’s liquidity position remains robust with $5.6 billion in available liquidity against $2.2 billion in uninsured deposits, as illustrated in this slide:

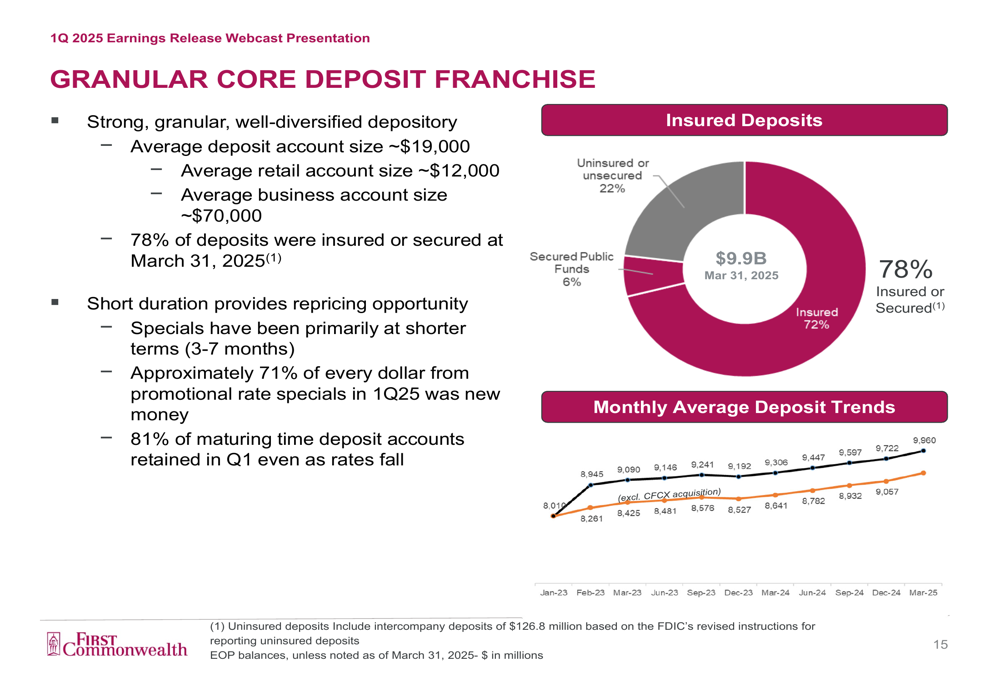

First Commonwealth emphasized its granular and well-diversified deposit base, with an average deposit account size of approximately $19,000. The bank reported that 78% of deposits were insured or secured as of March 31, 2025, providing stability to its funding structure.

The deposit franchise characteristics are shown in the following slide:

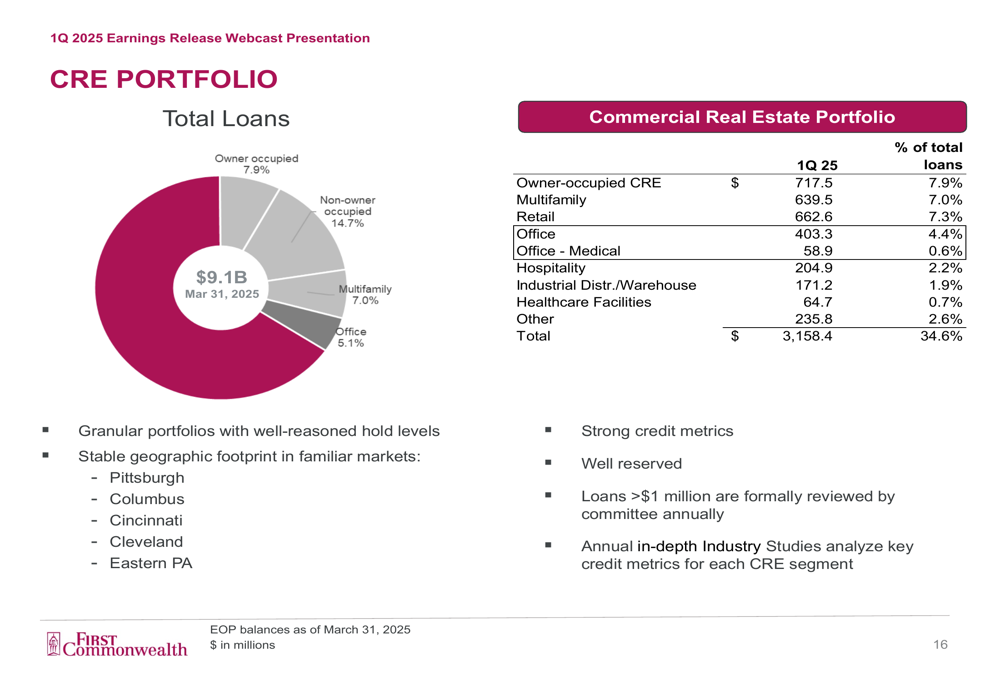

The bank’s commercial real estate portfolio, representing 34.6% of total loans, remains well-diversified across property types and geographies. The office segment, which has been a concern for many banks given post-pandemic occupancy challenges, comprises just 4.4% of First Commonwealth’s total loan portfolio.

The detailed breakdown of the CRE portfolio is illustrated here:

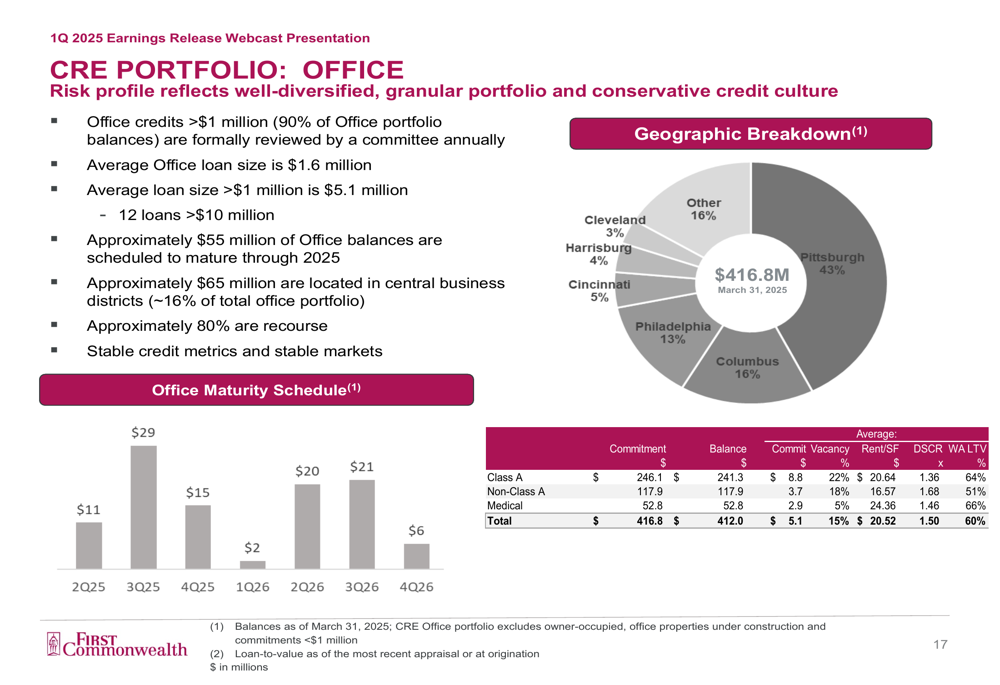

First Commonwealth provided additional details on its office portfolio, noting that 90% of office loans (by balance) undergo formal committee review annually. The portfolio is geographically diversified across the bank’s markets, with Pittsburgh representing the largest concentration at 43%.

Forward-Looking Statements

The bank’s board of directors authorized a 3.9% increase in the quarterly cash dividend, reflecting confidence in First Commonwealth’s capital position and earnings outlook. The bank reported no share repurchases during Q1 2025, with $6.7 million remaining capacity under its current program.

According to the earnings call transcript, management projects mid-single-digit loan growth and expects the net interest margin to expand to the high 3.70s by year-end. The bank is also factoring in potential Federal Reserve rate cuts, which could influence its interest income and lending activities.

CEO Mike Price emphasized the company’s strategic focus on commercial and industrial businesses in its regions, highlighting the bank’s "granular depository" with numerous household relationships as a competitive advantage.

First Commonwealth faces some challenges ahead, including tariff uncertainty and market volatility that may impact client sectors, particularly in manufacturing. The increase in operating expenses and pressure on fee income also present headwinds that management will need to navigate in coming quarters.

With its strong capital position, improving net interest margin, and solid loan growth, First Commonwealth appears positioned to maintain stable performance despite these challenges, provided credit quality remains benign and deposit competition doesn’t intensify unexpectedly.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.