Figma Shares Indicated To Open $105/$110

Introduction & Market Context

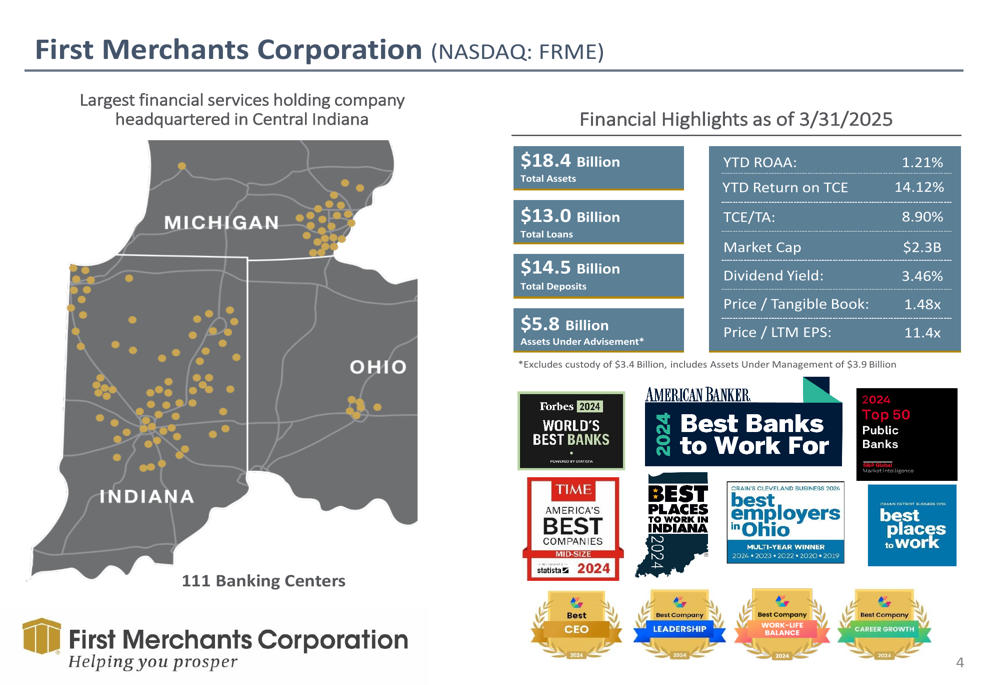

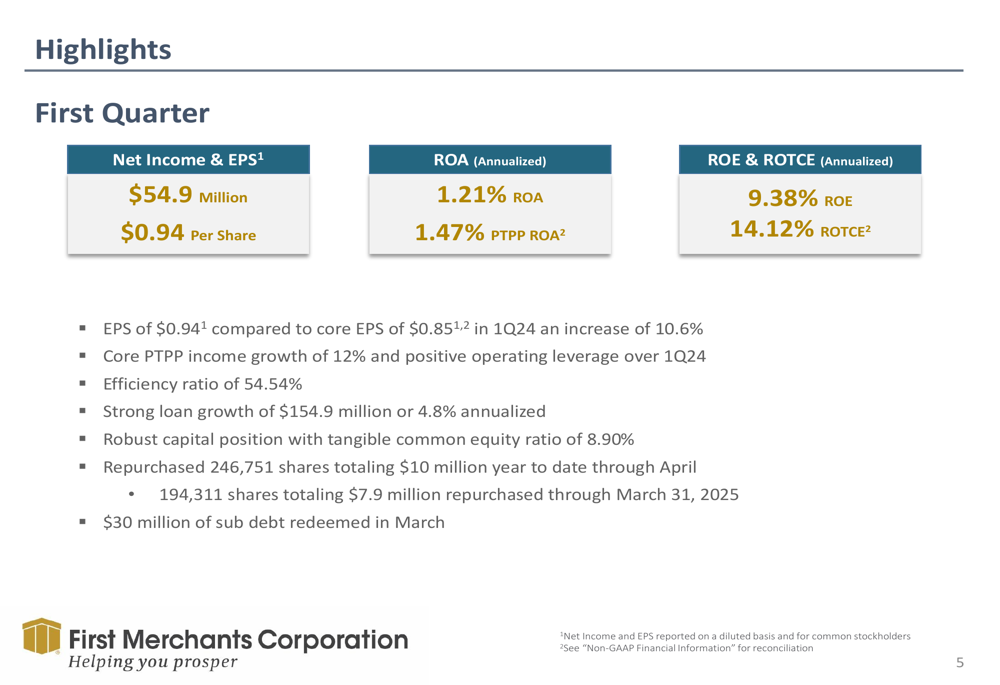

First Merchants Corporation (NASDAQ:FRME) released its first quarter 2025 investor presentation on April 24, revealing year-over-year earnings growth despite facing deposit challenges. The regional bank, which operates primarily in Indiana, Ohio, and Michigan, reported net income of $54.9 million or $0.94 per share, representing a 10.6% increase compared to the first quarter of 2024.

The results come amid a challenging environment for regional banks, with First Merchants shares closing at $36.92 on April 23 and showing premarket weakness with a 4.82% decline to $35.14 ahead of the presentation. The stock has been trading in a 52-week range of $30.55 to $46.13.

Quarterly Performance Highlights

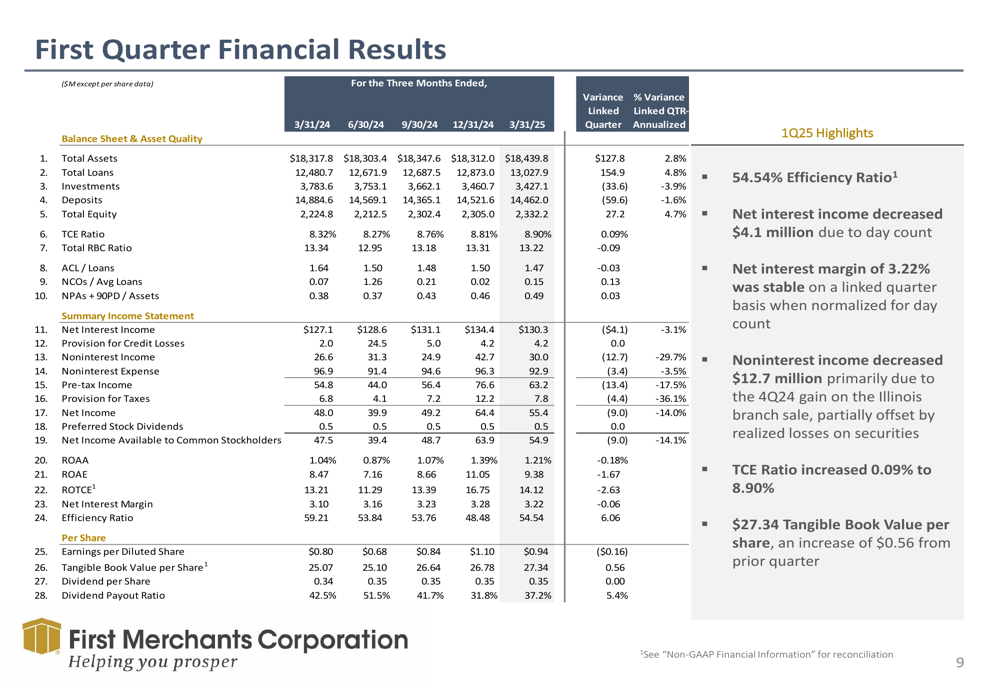

First Merchants reported solid financial metrics for Q1 2025, with return on assets (ROA) of 1.21%, pre-tax pre-provision ROA of 1.47%, and return on tangible common equity (ROTCE) of 14.12%. The bank maintained an efficiency ratio of 54.54%, demonstrating cost discipline amid revenue pressures.

As shown in the following overview of the company’s financial position:

Total (EPA:TTEF) assets reached $18.4 billion, supported by $13.0 billion in loans and $14.5 billion in deposits. The bank also manages $5.8 billion in assets under advisement through its wealth management division. With a market capitalization of $2.3 billion, First Merchants trades at 1.48x tangible book value and 11.4x last twelve months earnings, offering a dividend yield of 3.46%.

The first quarter highlights demonstrate the company’s continued profitability and growth:

Loan and Deposit Trends

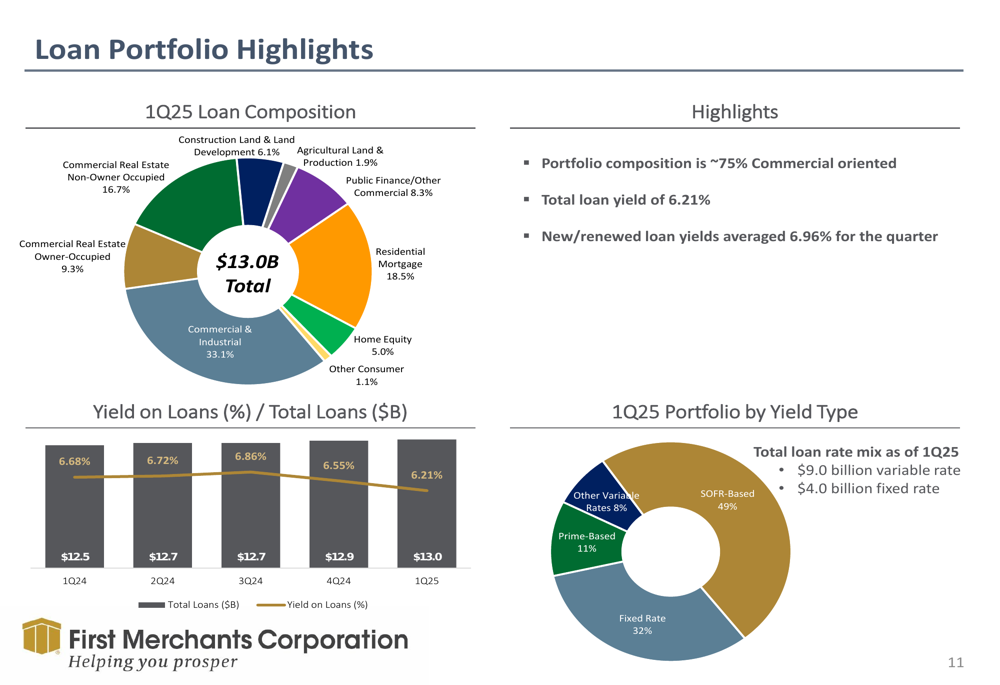

First Merchants reported annualized loan growth of 4.8% for the quarter, adding $154.9 million to its portfolio. This growth was driven primarily by the commercial segment, which expanded at a 7.0% annualized rate with $169 million in new loans. However, consumer balances declined by $14 million, representing a 1.8% annualized contraction.

The loan portfolio remains predominantly commercial-oriented at approximately 75% of total loans, with new and renewed loans yielding an average of 6.96% during the quarter.

The following chart illustrates the composition of the bank’s loan portfolio:

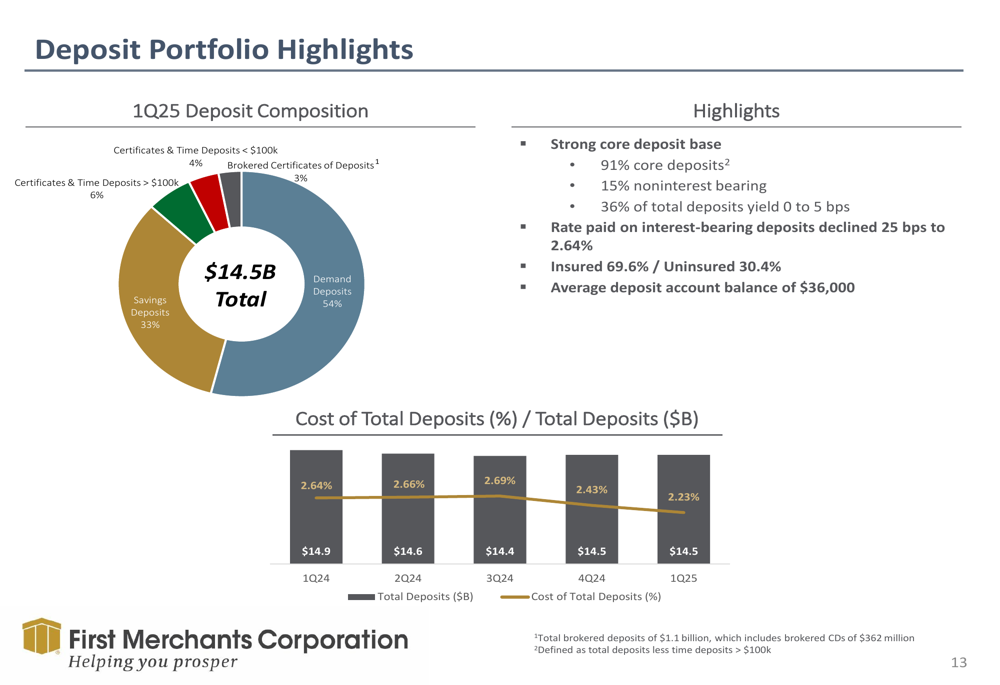

On the funding side, First Merchants experienced a 1.6% decline in total deposits during the quarter. Commercial deposits fell by $228 million (12.4% annualized), while consumer deposits decreased slightly by $9 million (0.6% annualized). Despite these declines, the bank maintains a strong core deposit base, with 91% of deposits classified as core.

The deposit portfolio breakdown shows the bank’s funding composition:

Financial Results Analysis

First Merchants’ first quarter financial results show mixed performance across key metrics. Net interest income decreased by $4.1 million compared to the previous quarter, primarily due to fewer days in the period. The net interest margin remained stable at 3.22% on a linked-quarter basis when normalized for day count.

Noninterest income decreased by $12.7 million from the previous quarter, primarily due to a gain on the Illinois branch sale recorded in Q4 2024. This decline was partially offset by realized losses on securities. The bank’s wealth management division continues to be the largest contributor to fee income.

The detailed financial results table provides a comprehensive view of the bank’s performance:

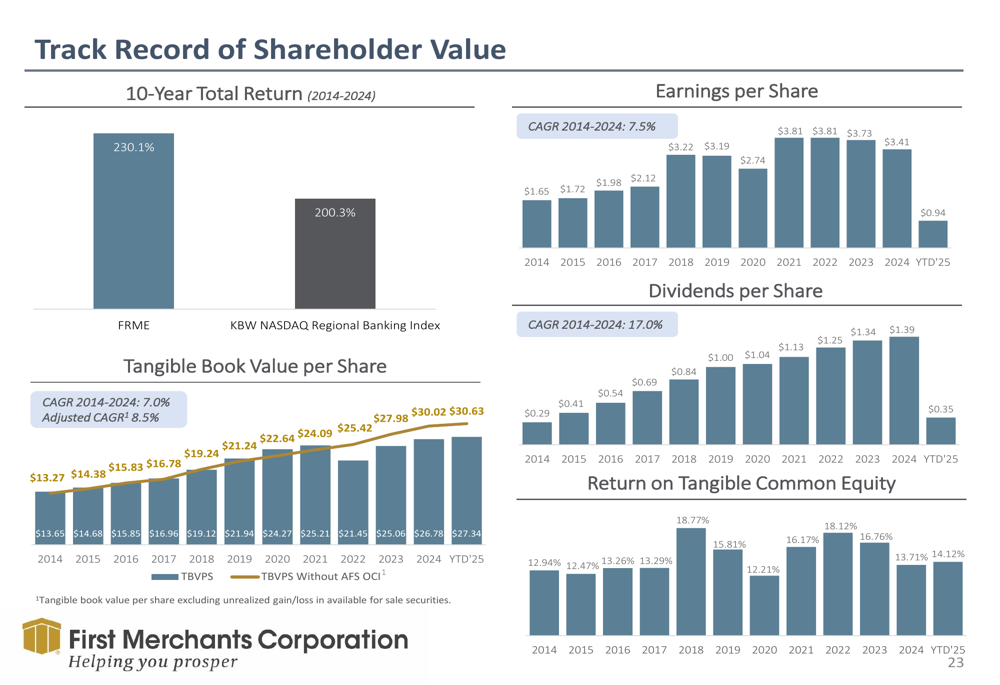

Capital Position and Shareholder Value

First Merchants maintained a strong capital position in the first quarter, with the tangible common equity (TCE) ratio increasing by 0.09 percentage points to 8.90%. Tangible book value per share grew to $27.34, representing an increase of $0.56 from the previous quarter.

The bank continued its shareholder-friendly capital allocation strategy, repurchasing 246,751 shares during the quarter while also redeeming $30 million of subordinated debt in March. These actions reflect management’s confidence in the bank’s financial strength and commitment to returning capital to shareholders.

The following chart illustrates First Merchants’ track record of creating shareholder value:

Asset Quality and Risk Management

Asset quality metrics remained generally stable during the quarter. The bank’s allowance for credit losses on loans totaled $166.7 million, with a $4.2 million provision recorded in the first quarter. Classified loans declined to 2.78% of total loans, indicating improved credit quality.

The largest non-accrual loans in the portfolio include a $22 million multi-family property and an $8.7 million nursing facility. Management noted that the largest new non-accrual relationship added during the quarter totaled $6.8 million, while the bank received a $2.4 million paydown on existing non-accrual loans.

Forward Outlook

First Merchants’ management team, led by CEO Mark Hardwick, outlined a vision focused on enhancing financial wellness for clients while maintaining the bank’s position as an attentive, knowledgeable, and high-performing financial institution.

The bank’s strategic imperatives include continuing to focus on commercial banking, consumer banking, mortgage banking, and private wealth advisory services. Management expects to leverage its strong capital position to pursue both organic growth and potential acquisition opportunities in its core markets.

This outlook aligns with previous guidance provided in the Q4 2024 earnings call, where management projected mid-single-digit loan growth and mid to high single-digit fee income growth for 2025. The bank also anticipated potential interest rate cuts by the Federal Reserve, which could impact net interest margin performance in the coming quarters.

While First Merchants faces challenges from deposit competition and margin pressure, its diversified business model and strong capital position provide a solid foundation for navigating the evolving banking landscape in 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.