Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

First Solar, Inc. (NASDAQ:FSLR) presented its first quarter 2025 earnings results on April 29, revealing mixed performance and a significant downward revision to its full-year guidance primarily due to tariff impacts and policy uncertainties. The solar manufacturer’s stock plunged 9.79% in after-hours trading to $123.80, reflecting investor concerns about the revised outlook despite the company’s substantial project backlog.

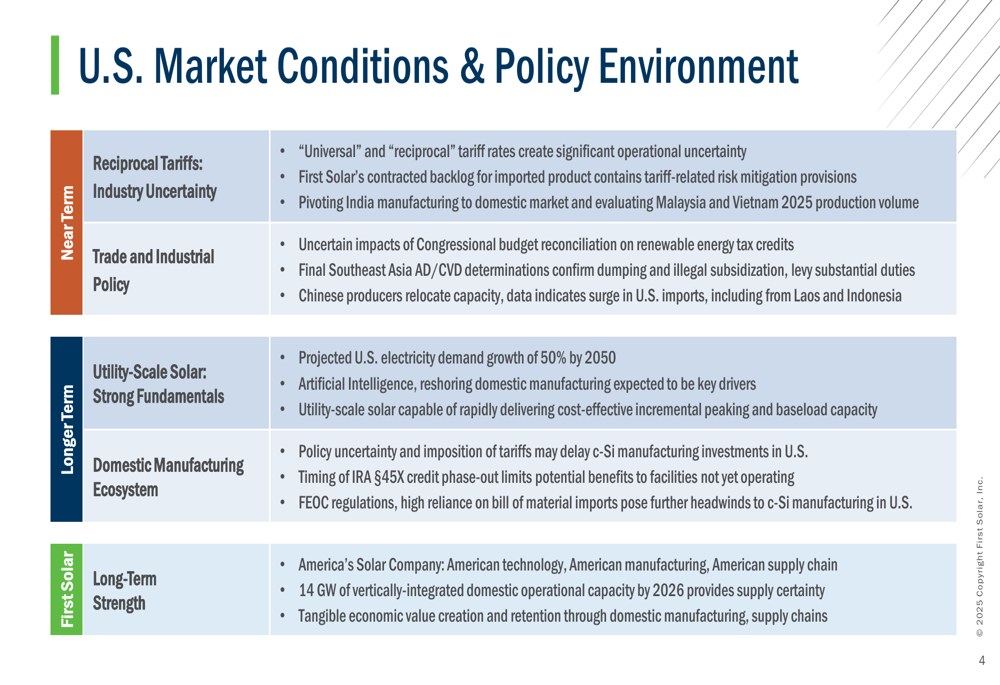

The company highlighted increasing challenges from reciprocal tariffs set to take effect on July 9, 2025, creating operational uncertainty across its global manufacturing footprint. These policy headwinds come at a time when First Solar continues to position itself as "America’s Solar Company (WA:SOLP)" with expanding domestic manufacturing capacity.

Quarterly Performance Highlights

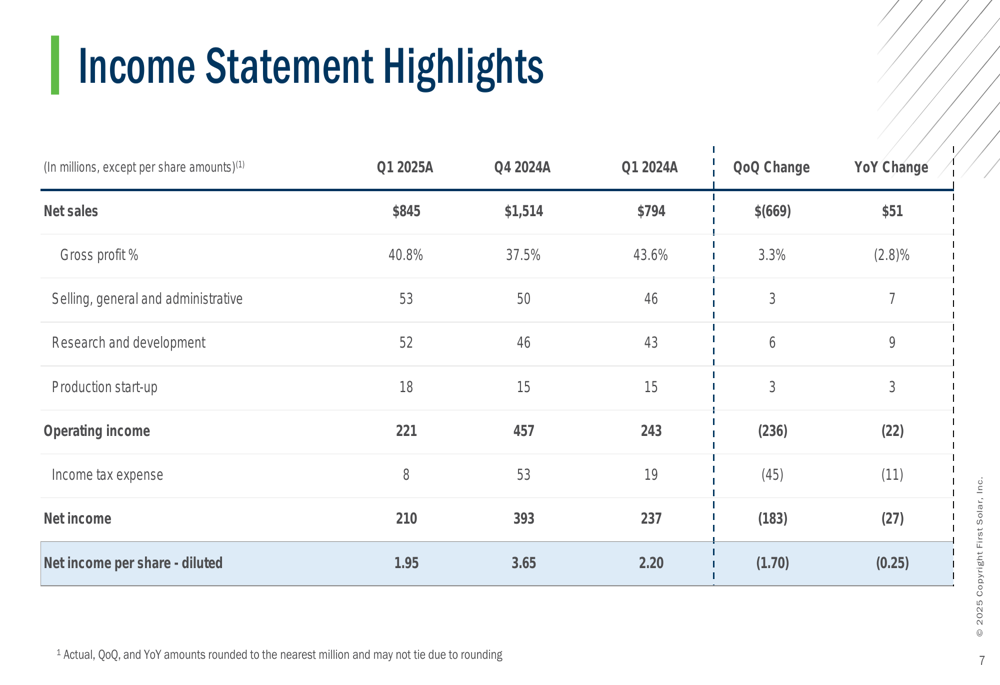

First Solar reported Q1 2025 net sales of $845 million, representing a 6.4% increase year-over-year from $794 million, but a substantial 44.2% decrease from Q4 2024’s $1,514 million. Diluted earnings per share came in at $1.95, down from $2.20 in the year-ago quarter and $3.65 in the previous quarter.

As shown in the company’s quarterly summary:

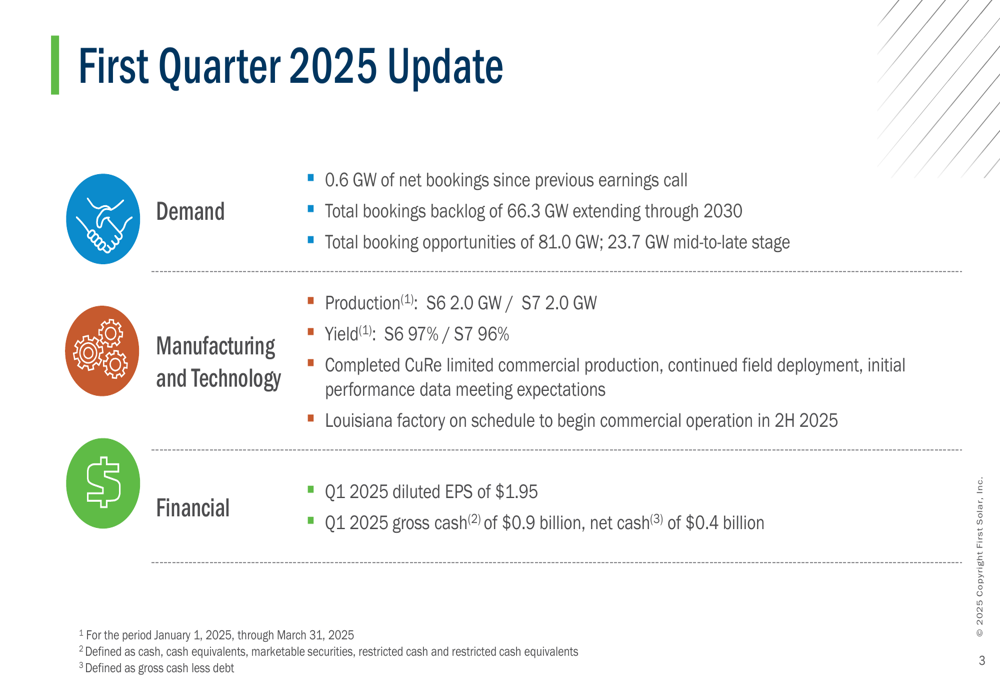

The company maintained strong production volumes, manufacturing 4.0 GW in the quarter, evenly split between Series 6 and Series 7 modules, with yields of 97% and 96% respectively. First Solar also reported completing limited commercial production of its CuRe technology, with initial performance data meeting expectations.

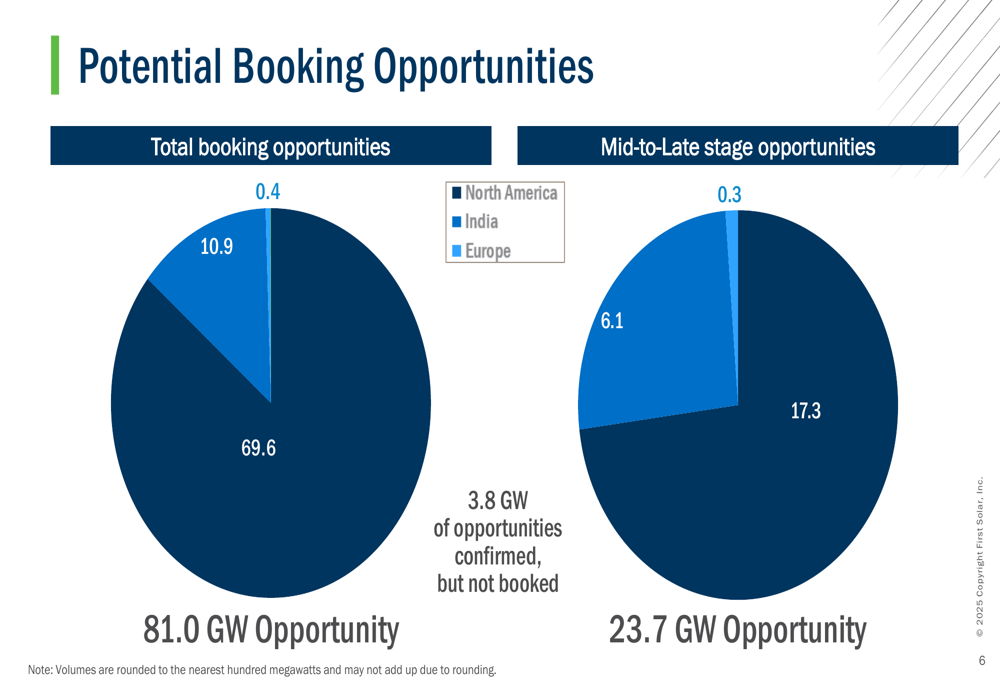

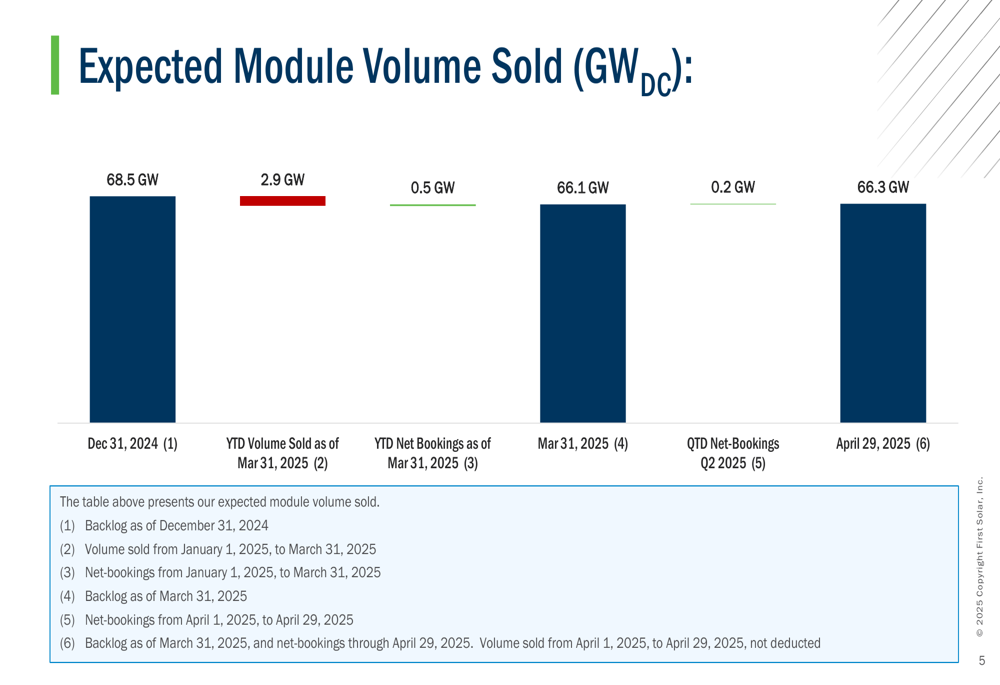

On the demand side, First Solar secured 0.6 GW of net bookings since the previous earnings call, bringing its total backlog to 66.3 GW extending through 2030. The company’s booking opportunities pipeline remains robust at 81.0 GW, with 23.7 GW in mid-to-late stage negotiations.

Detailed Financial Analysis

The company’s income statement revealed mixed results across key metrics. While gross profit margin improved sequentially to 40.8% from 37.5% in Q4 2024, it declined year-over-year from 43.6% in Q1 2024. Operating income fell to $221 million from $243 million a year ago and $457 million in the previous quarter.

The detailed income statement highlights illustrate these trends:

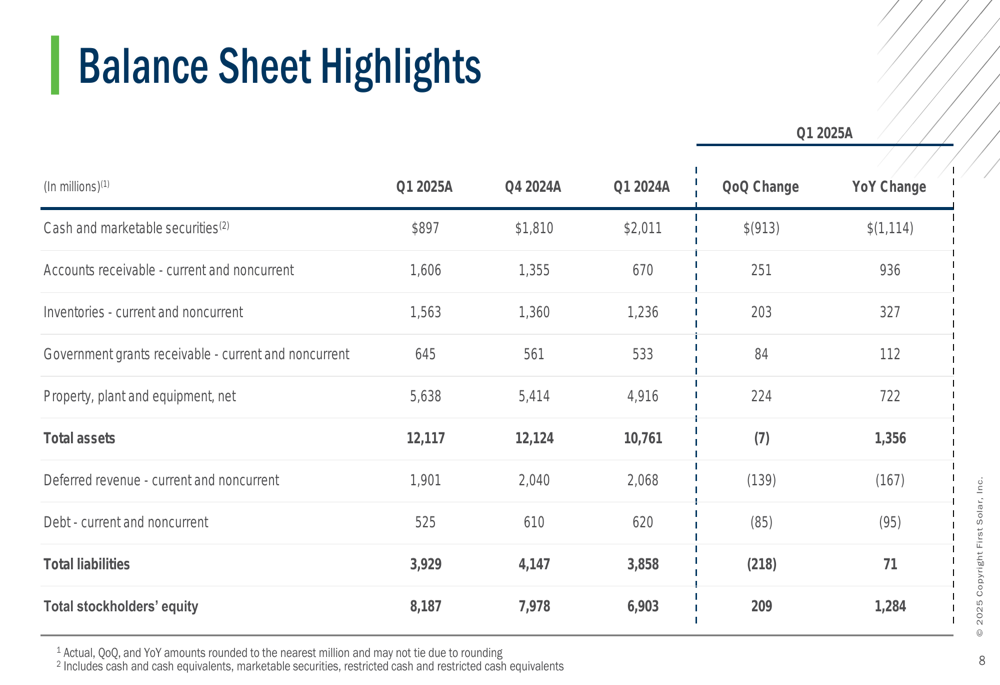

First Solar’s balance sheet showed significant changes year-over-year, with cash and marketable securities declining to $897 million from $2,011 million a year earlier. Accounts receivable more than doubled to $1,606 million from $670 million, while property, plant and equipment increased to $5,638 million from $4,916 million, reflecting ongoing capacity expansion.

The balance sheet highlights demonstrate these shifts:

Forward-Looking Statements & Guidance

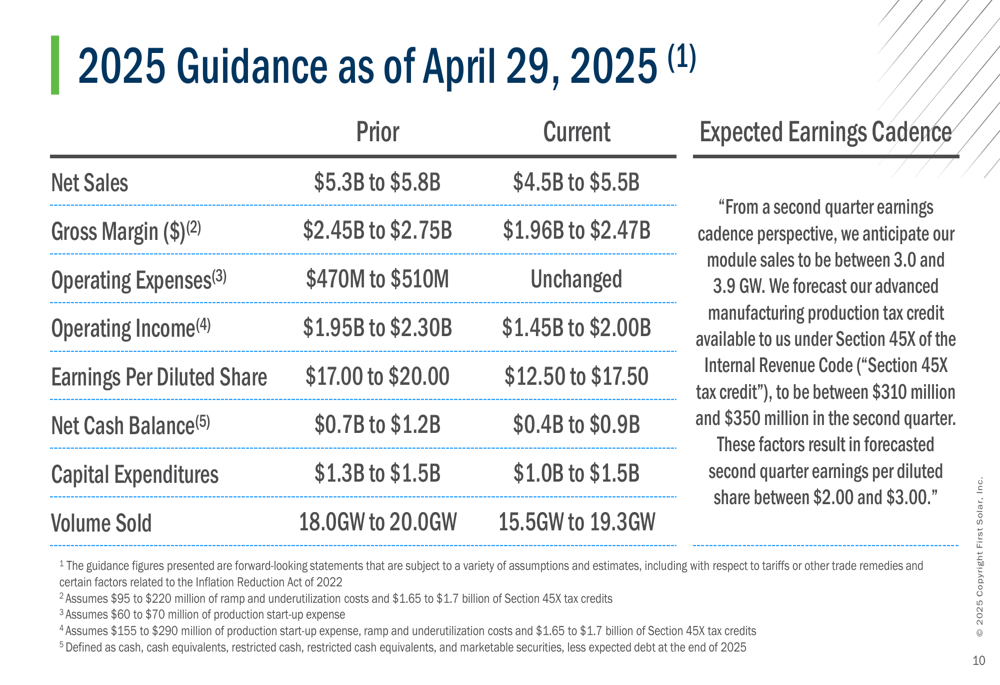

In the most significant development from the presentation, First Solar substantially reduced its 2025 guidance across all key metrics. The company now expects net sales of $4.5-$5.5 billion (down from $5.3-$5.8 billion) and diluted EPS of $12.50-$17.50 (down from $17.00-$20.00).

The guidance revision reflects increased tariff impacts, with the company estimating potential revenue impacts of $100-$375 million, along with additional costs from import duties on finished goods ($90-$70 million), raw material imports ($25-$55 million), and period costs ($65-$270 million). First Solar also indicated it may temporarily idle production in Malaysia and Vietnam due to tariff impacts.

The full guidance revision is detailed in this slide:

For Q2 2025, First Solar expects module sales between 3.0 and 3.9 GW, with Section 45X tax credits of $310-$350 million, resulting in forecasted diluted EPS of $2.00-$3.00.

Strategic Positioning & Challenges

Despite near-term challenges, First Solar continues to emphasize its long-term strategic advantages, particularly its domestic manufacturing capacity, which is expected to reach 14 GW by 2026. The company’s Louisiana factory remains on schedule to begin commercial operations in the second half of 2025.

The company highlighted both near-term challenges and long-term opportunities in the U.S. market:

First Solar’s booking opportunities remain heavily weighted toward Europe, which represents 69.6 GW of its total 81.0 GW opportunity pipeline. The regional breakdown of potential bookings shows:

The company’s backlog evolution shows relatively stable total commitments, with 66.3 GW in backlog as of April 29, 2025, despite 2.9 GW of volume sold year-to-date:

While First Solar faces significant near-term headwinds from tariffs and policy uncertainty, its substantial backlog, expanding domestic manufacturing capacity, and technological advancements position it to potentially benefit from projected long-term growth in U.S. electricity demand, which the company expects to increase by 50% by 2050, driven by artificial intelligence applications and reshoring of domestic manufacturing.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.