CSL shares plunge to 7-year low on delay in US vaccine business spinoff

Introduction & Market Context

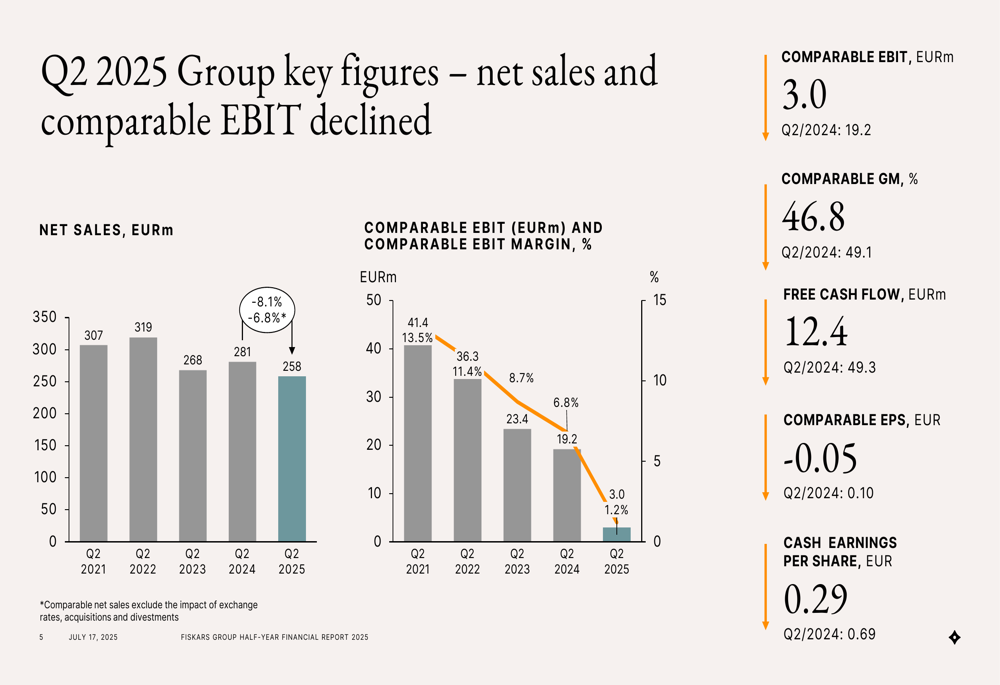

Fiskars Group (HEL:FSKRS) released its Q2 2025 financial results on July 17, revealing a significant deterioration in performance amid a challenging market environment characterized by tariff-driven uncertainty. The Finnish consumer goods company, currently trading at €14.86 near its 52-week low of €13.56, reported a sharp decline in profitability despite some bright spots in its transformation strategy.

The results mark a stark reversal from Q1 2025, when the company had reported an increase in EBIT and EBIT margin. The stock has been under pressure, trading well below its 52-week high of €16.96 as investors digest the impact of tariffs and weakening U.S. demand on the company’s outlook.

Quarterly Performance Highlights

Fiskars reported a steep 84% year-over-year decline in comparable EBIT, which fell to just €3.0 million in Q2 2025 compared to €19.2 million in Q2 2024. The comparable EBIT margin contracted dramatically to 1.2%, down from 6.8% a year earlier. This decline comes as comparable net sales decreased by 7%, driven particularly by weakness in the U.S. market.

As shown in the following chart of key financial metrics, the company has experienced a multi-year downward trend in both sales and profitability:

Free cash flow also deteriorated significantly, falling to €12.4 million from €49.3 million in Q2 2024. Comparable earnings per share turned negative at -€0.05, compared to €0.10 in the same period last year. The company’s cash earnings per share also declined to €0.29 from €0.69 year-over-year.

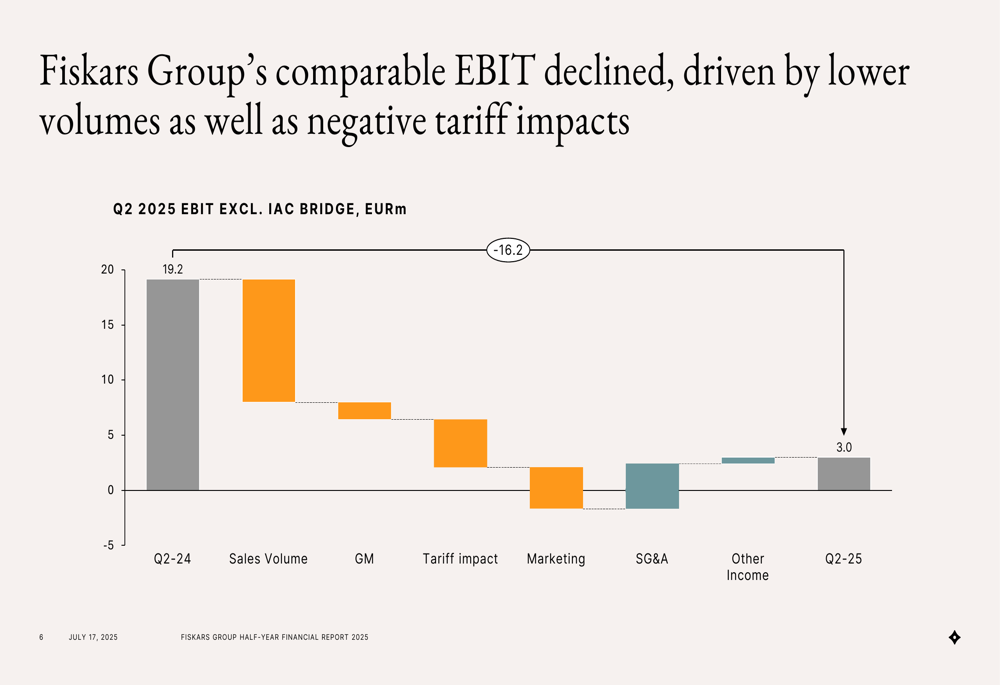

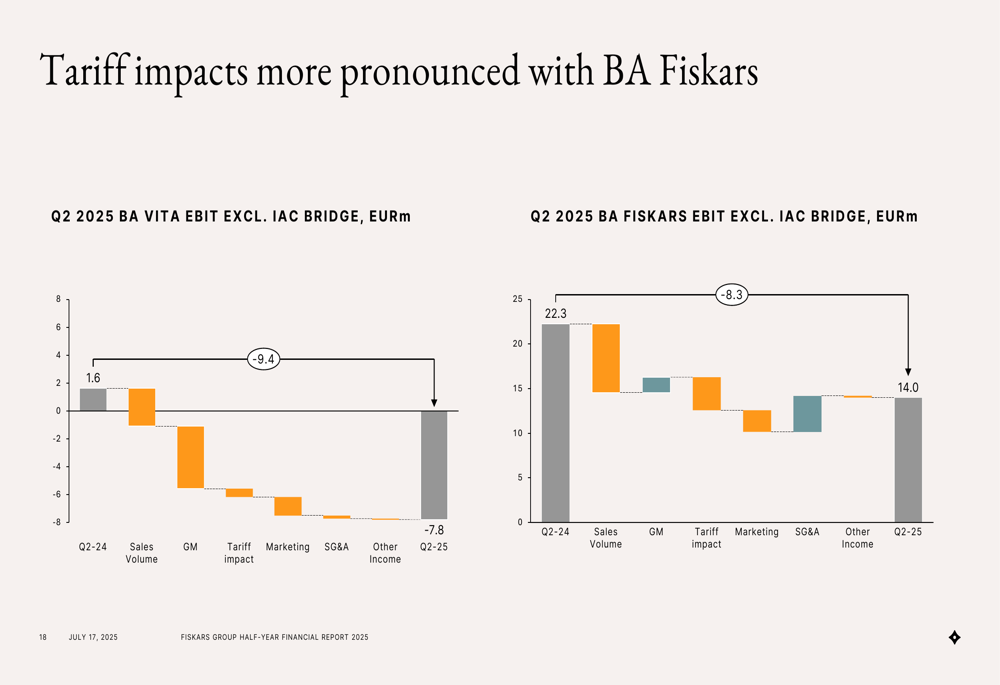

A bridge analysis reveals the factors contributing to the EBIT decline, with lower sales volumes, gross margin pressure, and tariff impacts being the primary drivers:

Detailed Financial Analysis

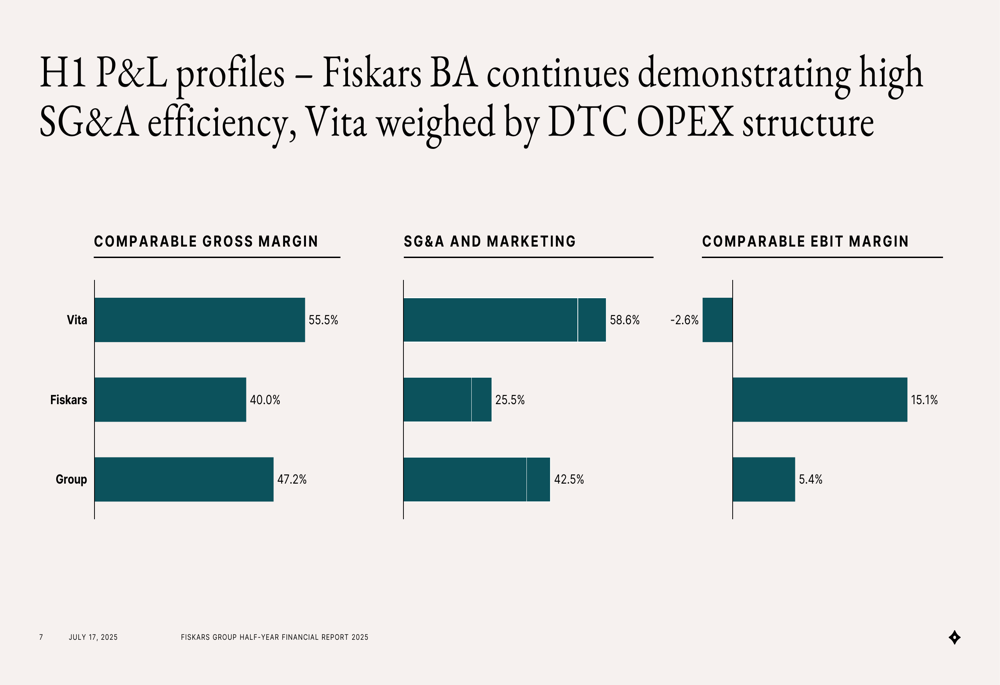

The company’s two business areas showed divergent profitability profiles in the first half of 2025. Business Area Fiskars maintained a healthy 15.1% comparable EBIT margin despite challenges, while Business Area Vita struggled with a negative 2.6% comparable EBIT margin. The stark difference in profitability is illustrated in the following chart:

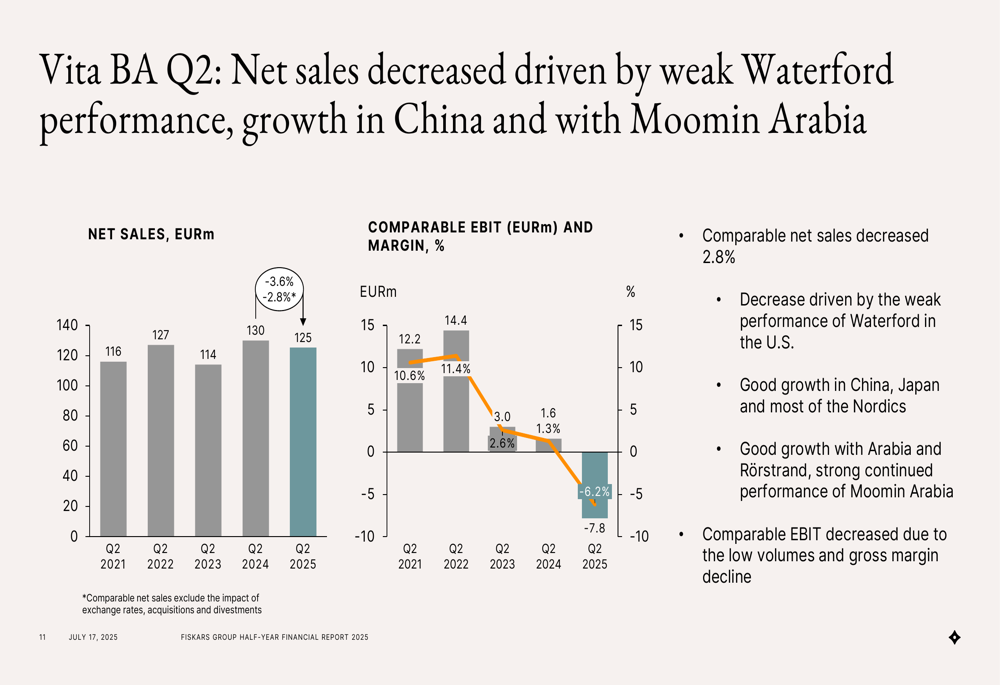

Business Area Vita saw comparable net sales decrease by 2.8%, primarily due to weak performance of Waterford in the U.S. market. However, the division reported good growth in China, Japan, and most Nordic countries, with strong continued performance of Moomin Arabia products during the brand’s 80th anniversary year.

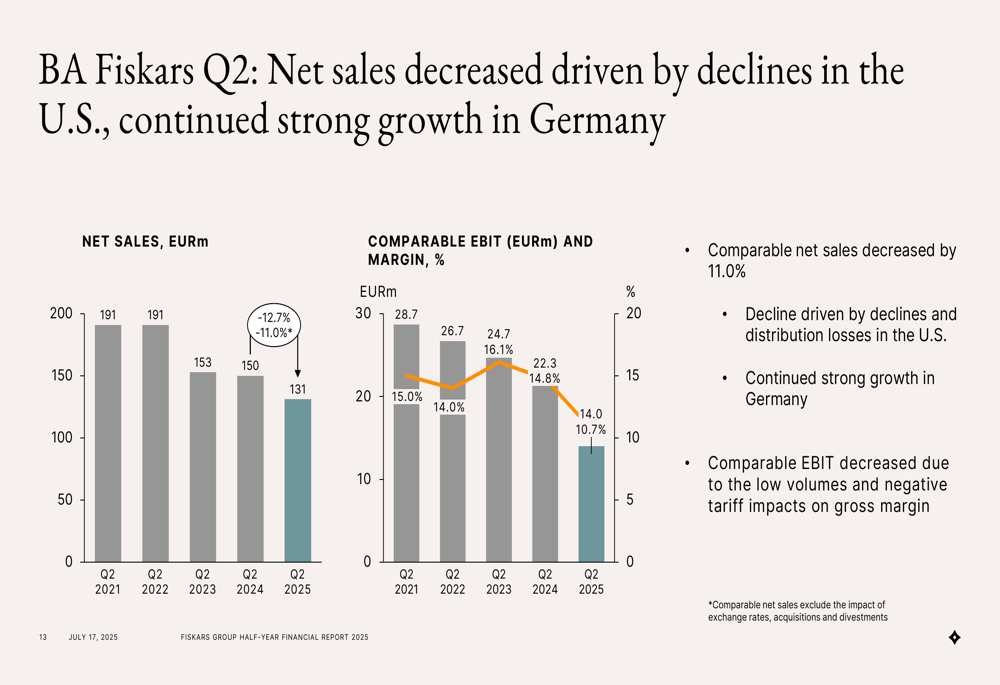

Business Area Fiskars experienced a more severe 11.0% decline in comparable net sales, driven by distribution losses and declining sales in the U.S. market. The division did report continued strong growth in Germany through distribution gains and successful campaigns. The company also highlighted the launch of its 6th generation Fiskars Classic Scissors.

Strategic Initiatives

Despite the challenging quarter, Fiskars reported progress on two of its four transformation levers. Direct-to-consumer sales grew by 4% in Q2, with the company’s own retail network increasing by 6% while e-commerce declined by 1%. DTC now represents 28% of total net sales and 58% of Business Area Vita’s sales.

China remains a bright spot with 12% comparable net sales growth in Q2, particularly with new water bottle category products and the Arabia brand. This contrasts sharply with the U.S. market, where comparable net sales declined by 14%.

The company is also making progress on its sustainability targets, as shown in the following chart:

Tariff Impact and Mitigation Strategies

Tariffs have emerged as a significant challenge for Fiskars, with both direct and indirect impacts affecting performance. The U.S. market, which represents approximately 30% of Fiskars Group’s net sales and 50% of Business Area Fiskars’ net sales, has been particularly affected.

The company noted that indirect impacts, particularly on retailer demand and inventory behavior, have materialized more rapidly and negatively than previously anticipated. The following chart illustrates the tariff impact on both business areas:

To address these challenges, Fiskars is prioritizing market share and cash flow while implementing mitigation strategies. The company expects to largely mitigate the adverse direct impacts of tariffs, although benefits are expected to materialize only from the second half of 2025 onwards.

Forward-Looking Statements

In light of the challenging operating environment, Fiskars has updated its guidance for 2025. The company now expects comparable EBIT to be in the range of €90-110 million, compared to €111.4 million in 2024. This represents a downward revision from the company’s previous outlook of improved EBIT for 2025.

The key takeaways from the Q2 2025 presentation highlight both the challenges and areas of progress:

Management noted that pricing adjustments and ongoing productivity initiatives are expected to support comparable EBIT in the second half of the year. However, the operating environment remains challenging, with tariffs expected to continue increasing sourcing costs directly and impacting demand indirectly.

The company’s net debt to EBITDA ratio has increased to 3.16x, reflecting the pressure on earnings and cash flow in the current environment.

As Fiskars navigates these challenges, its ability to leverage growth in direct-to-consumer channels and the Chinese market while mitigating tariff impacts in the U.S. will be crucial for its performance in the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.