Functional Brands closes $8 million private placement and completes Nasdaq listing

Introduction & Market Context

Flex Ltd. (NASDAQ:FLEX) presented its fourth quarter and full fiscal year 2025 results on May 7, 2025, highlighting record margins and continued earnings growth despite mixed revenue performance. The global manufacturing and supply chain solutions provider saw its stock drop 4.49% to $35.12 following the announcement, suggesting investors may have been concerned about the company’s cautious revenue outlook amid macroeconomic uncertainties.

The presentation showcased Flex’s strategic focus on higher-margin businesses, particularly in data center power and cloud solutions, which helped drive profitability improvements despite challenging market conditions in some segments. The company’s diversified portfolio appears to be successfully mitigating end-market cycles, with strength in data center and networking offsetting weakness in areas like renewables and consumer devices.

Quarterly Performance Highlights

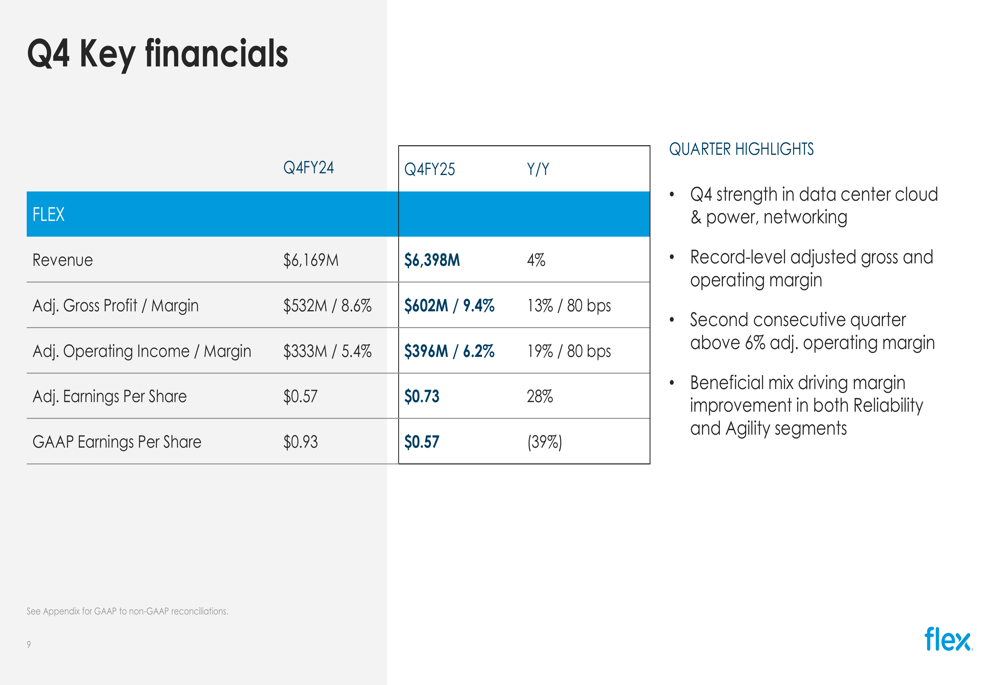

Flex reported Q4 FY25 revenue of $6.4 billion, representing a 4% year-over-year increase. More impressively, adjusted operating income grew 19% to $396 million, with adjusted operating margin expanding 80 basis points to 6.2%. Adjusted earnings per share reached $0.73, up 28% compared to the same period last year.

The company’s performance was particularly strong in its Agility segment, which saw revenue growth of 8.2% year-over-year to $3.5 billion and adjusted operating income increase of 27.3% to $230 million. The segment’s operating margin expanded 100 basis points to 6.6%. The Reliability segment, while experiencing a slight revenue decline of 1.3% to $2.9 billion, still managed to grow adjusted operating income by 5.4% to $180 million, with margins improving 40 basis points to 6.2%.

As shown in the following quarterly financial summary:

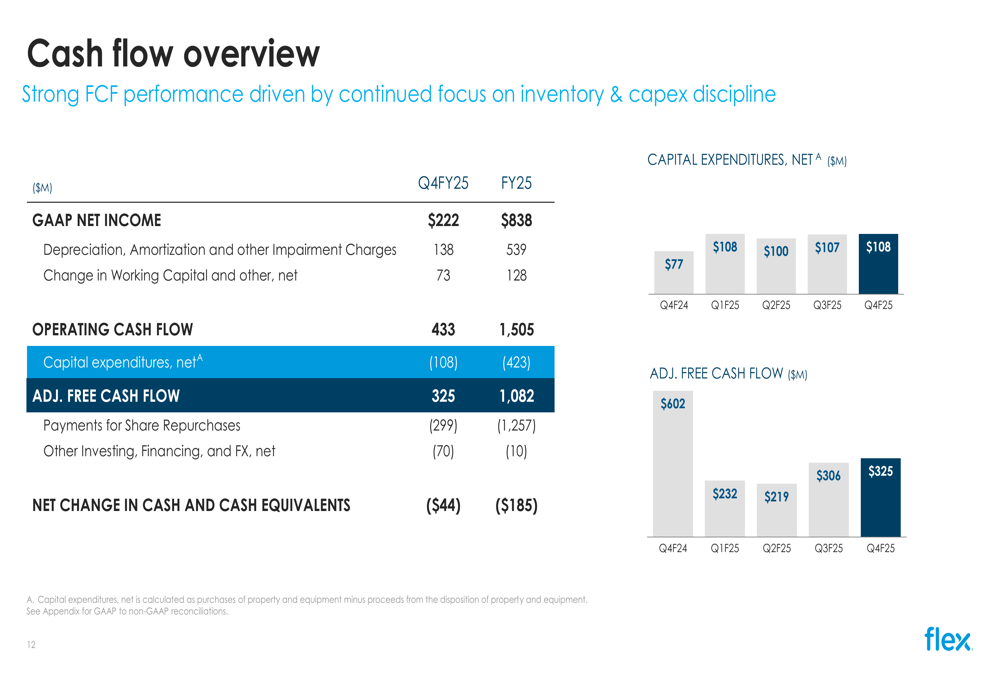

The company generated $433 million in operating cash flow during the quarter, with adjusted free cash flow of $325 million. Capital expenditures for the quarter were $108 million, consistent with previous quarters as the company continues to invest in growth opportunities.

Full-Year Financial Analysis

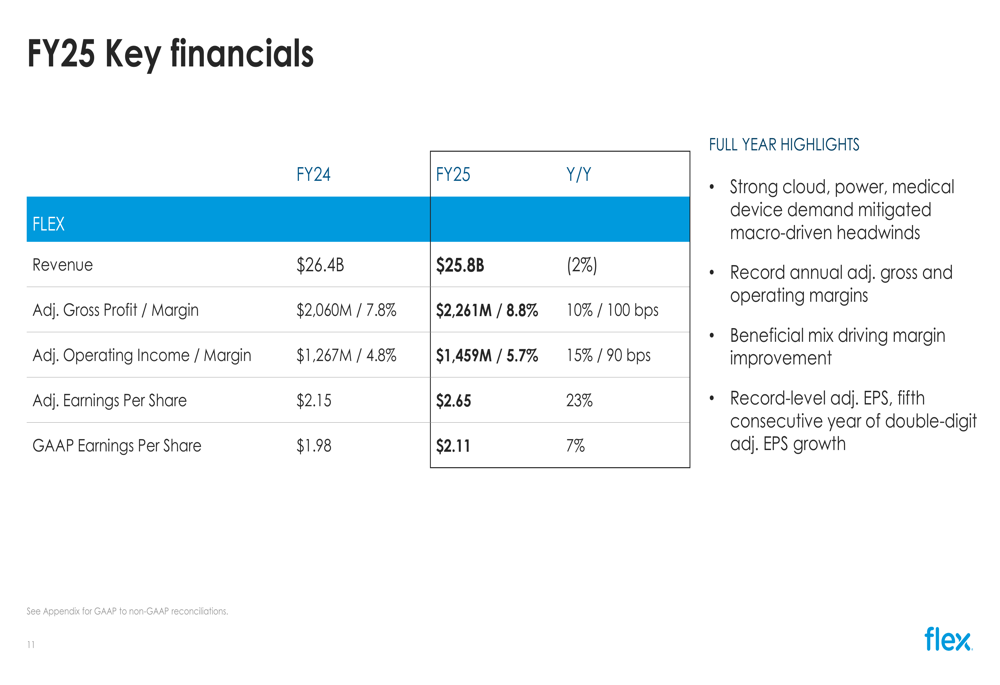

For the full fiscal year 2025, Flex reported revenue of $25.8 billion, a 2% decrease from the previous year. However, the company significantly improved profitability, with adjusted operating income increasing 15% to $1.46 billion and adjusted operating margin expanding 90 basis points to 5.7%. Adjusted earnings per share grew 23% to $2.65, marking the fifth consecutive year of double-digit EPS growth.

The company’s full-year performance is summarized in the following slide:

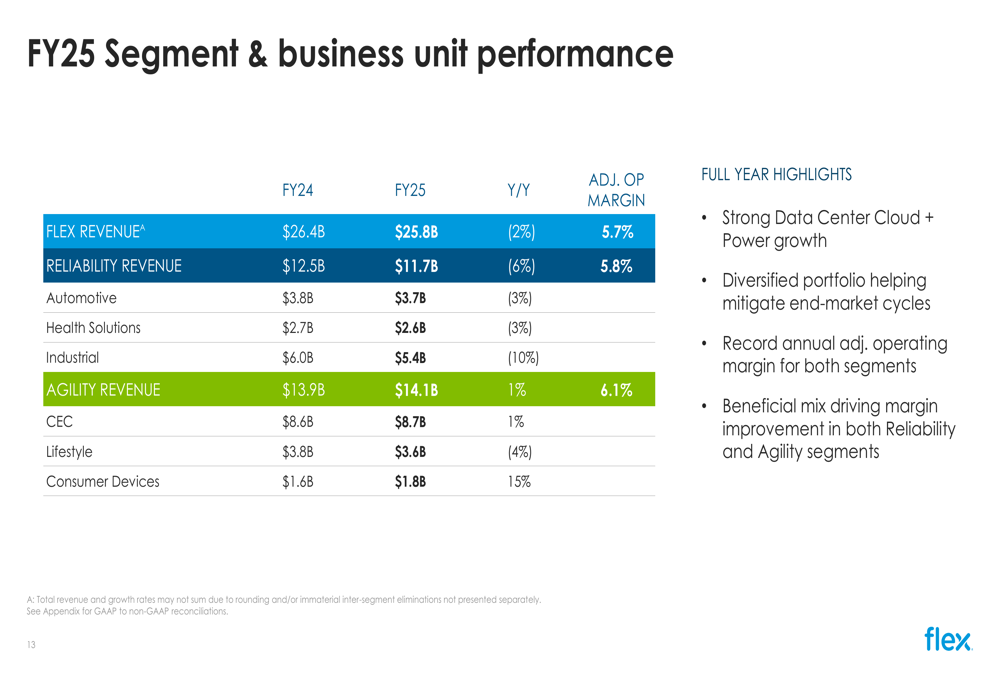

Flex’s segment performance for FY25 showed the Reliability segment generating $11.7 billion in revenue (down 6% year-over-year) with a 5.8% adjusted operating margin, while the Agility segment delivered $14.1 billion in revenue (up 1% year-over-year) with a 6.1% adjusted operating margin. Within these segments, the data center cloud and power business stood out with approximately 50% year-over-year growth, helping to offset weakness in other areas.

The breakdown of Flex’s business units shows varied performance across different markets:

Strategic Initiatives & Growth Areas

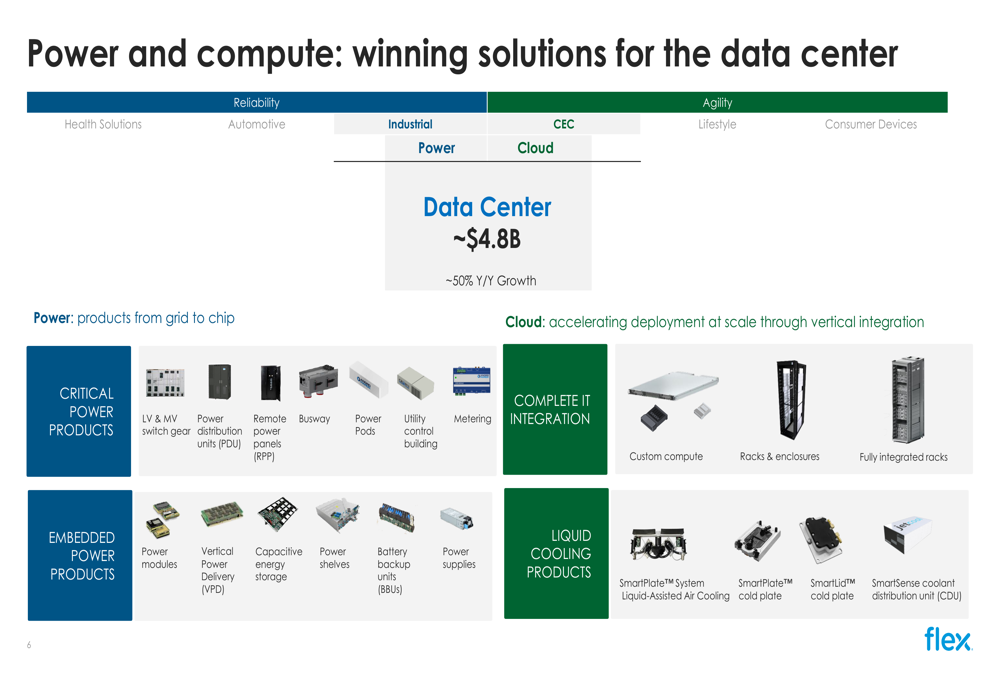

Flex’s presentation emphasized its strategic focus on expanding its value-added services and product portfolio, particularly in the data center power and cloud computing markets. The company highlighted its unique position as the only provider with a complete grid-to-chip power portfolio, addressing the growing demand for power solutions in AI and data center applications.

The company’s data center-focused offerings span both power and compute solutions, targeting a market worth approximately $4.8 billion with ~50% year-over-year growth:

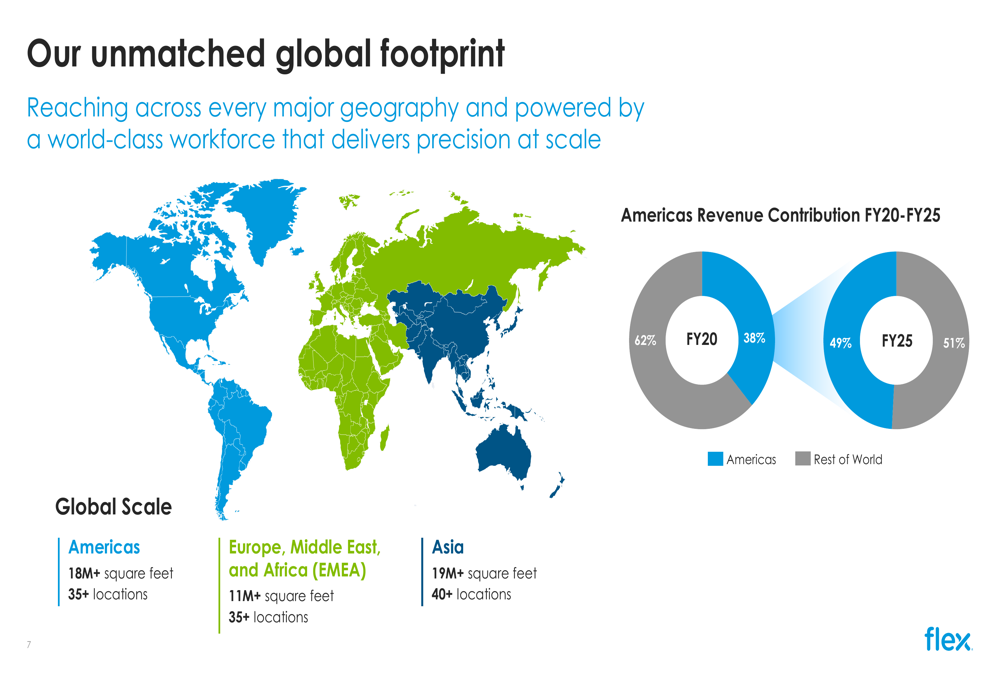

Flex also showcased its global manufacturing footprint, which includes over 110 locations across the Americas, Europe, Middle East, Africa, and Asia. Notably, the company has been diversifying its geographic revenue mix, with Americas revenue contribution decreasing from 62% in FY20 to 49% in FY25.

The company’s value proposition centers on three key pillars: advanced manufacturing and services, product portfolio expansion, and delivering profitable growth. Flex aims to achieve low-to-mid single-digit revenue CAGR, 6%+ adjusted operating margin, low-teens adjusted EPS CAGR, and 80% adjusted free cash flow conversion by FY27.

Forward Guidance & Outlook

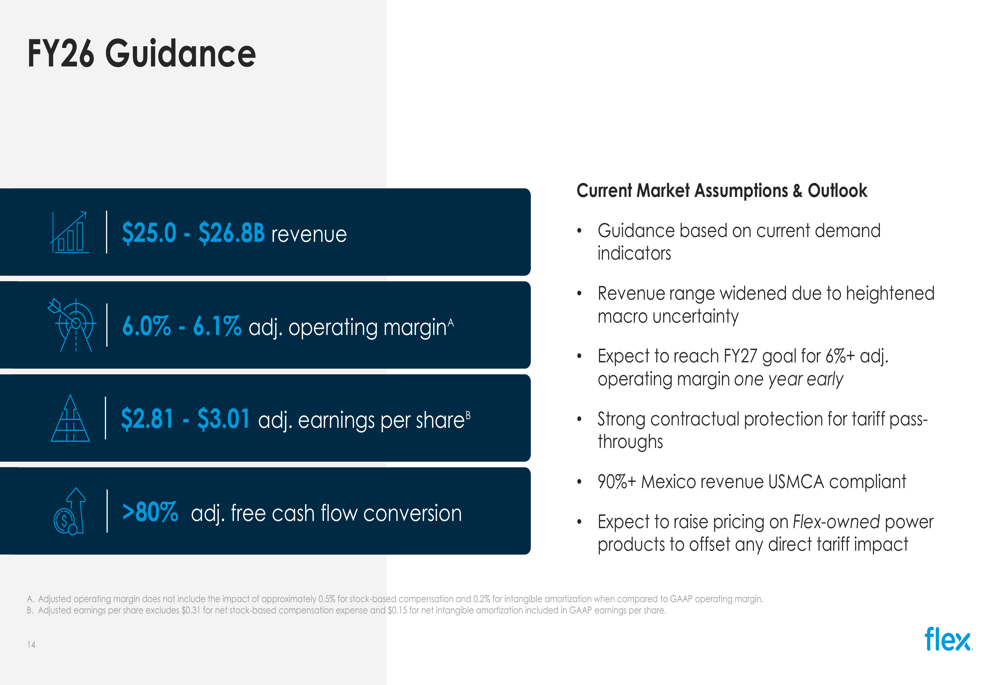

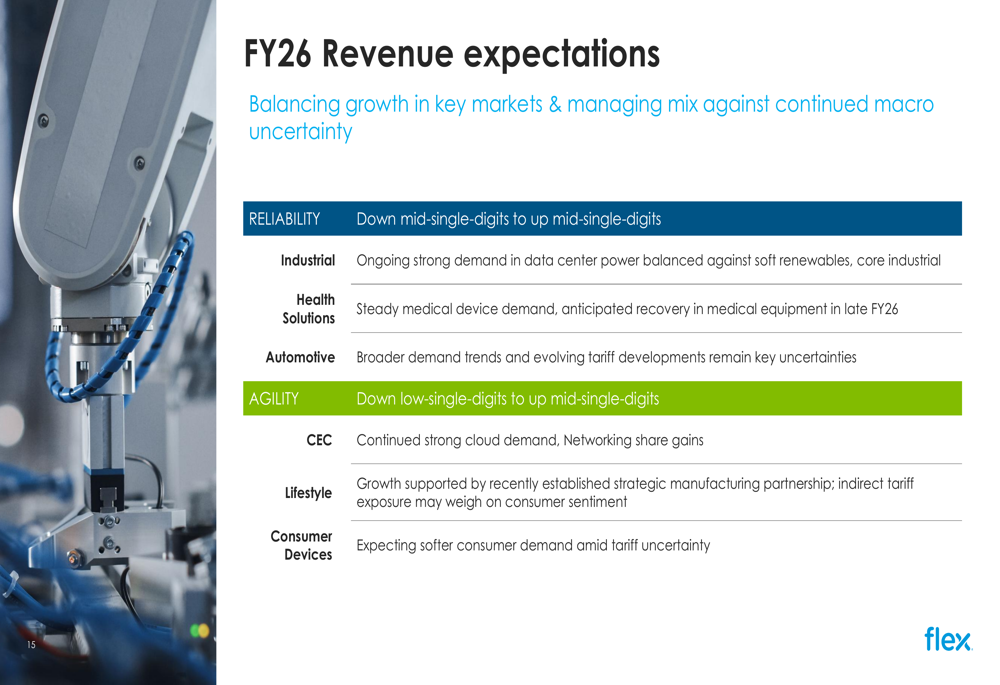

Looking ahead to fiscal year 2026, Flex provided guidance that reflects confidence in continued margin expansion but caution on revenue growth due to macroeconomic uncertainties and potential tariff impacts. The company expects revenue between $25.0 billion and $26.8 billion, adjusted operating margin of 6.0-6.1% (reaching its FY27 goal of 6%+ one year early), and adjusted earnings per share of $2.81-$3.01.

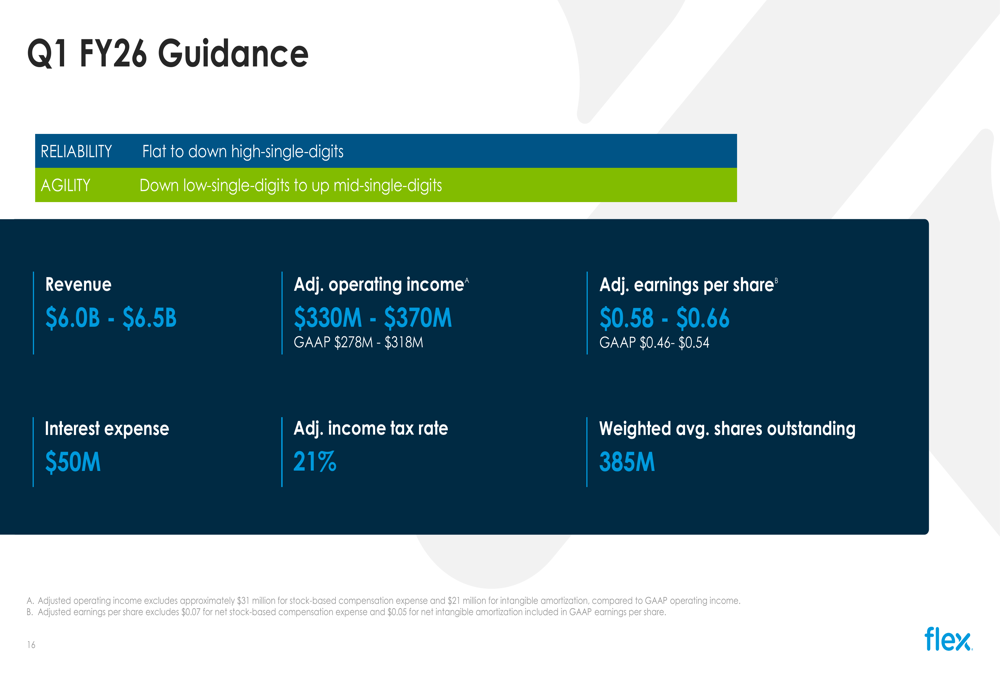

For the first quarter of FY26, Flex projects revenue of $6.0-$6.5 billion and adjusted earnings per share of $0.58-$0.66. The company noted that it has strong contractual protection for tariff pass-throughs, with over 90% of its Mexico revenue being USMCA compliant.

Segment-level guidance for FY26 shows a mixed outlook, with continued strength expected in data center power and cloud, balanced against challenges in other areas:

The cautious revenue outlook, particularly in consumer-facing segments, may have contributed to the stock’s negative reaction despite the strong margin and earnings performance. However, Flex’s strategic focus on higher-margin businesses and its growing presence in the rapidly expanding data center and AI infrastructure markets position the company well for long-term profitable growth, even as it navigates near-term macroeconomic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.