Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Flowers Foods (NYSE:FLO) presented its first quarter 2025 financial results on May 16, revealing a challenging consumer environment that has led to greater-than-expected category declines. The bakery products company’s stock fell 7.5% in premarket trading to $15.79 following the release, as investors reacted to decreased sales and adjusted guidance.

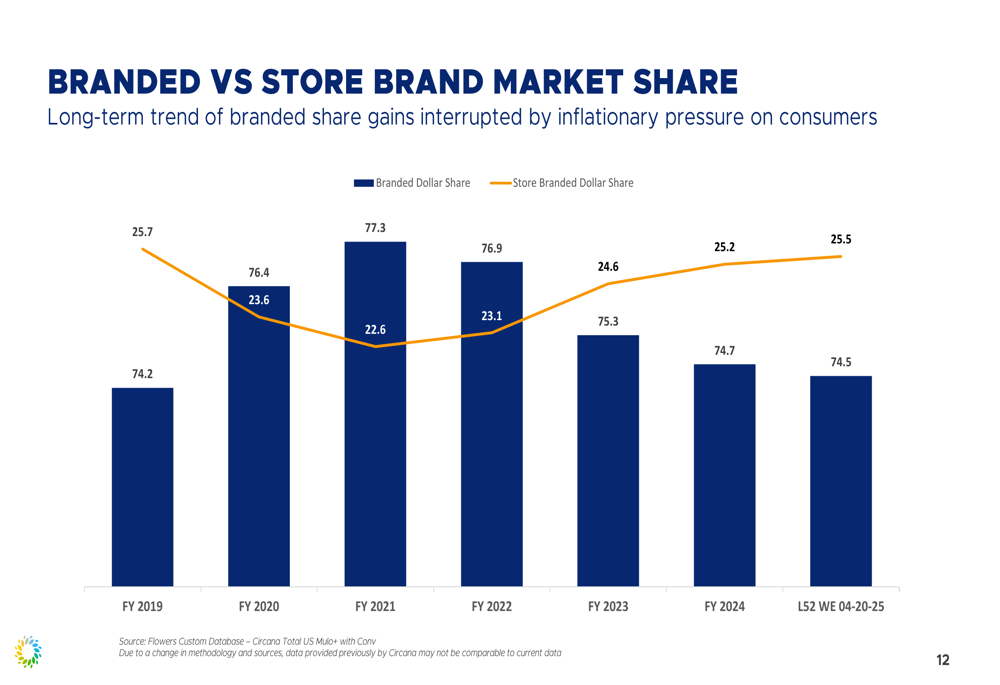

Despite these headwinds, the company highlighted its strong market share performance, with each of its leading brands gaining or holding unit and dollar share in tracked channels. This performance comes amid a broader trend where branded bakery products have been facing pressure from private label alternatives during the inflationary environment.

As shown in the following market share analysis, branded products have maintained a dominant position but have seen a slight erosion in recent years:

Quarterly Performance Highlights

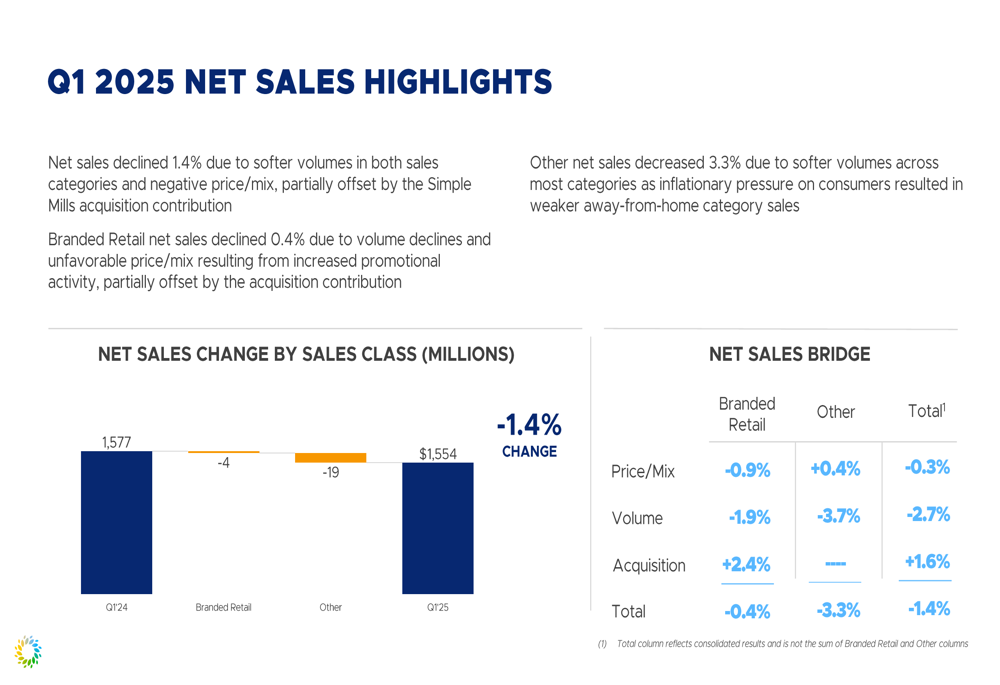

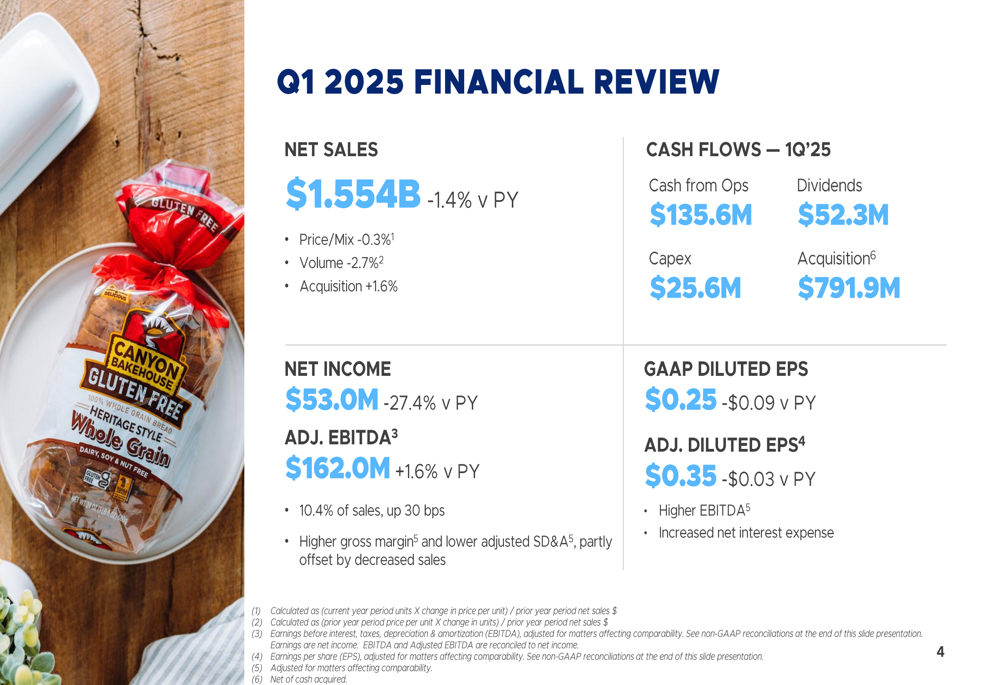

For the first quarter of 2025, Flowers Foods reported net sales of $1.554 billion, representing a 1.4% decrease year-over-year. This decline was attributed to volume decreases of 2.7% and price/mix decreases of 0.3%, partially offset by a 1.6% contribution from acquisition.

Net income fell 27.4% to $53.0 million, primarily due to lower operating income, higher net interest expense, and a higher income tax rate. GAAP diluted earnings per share came in at $0.25, down $0.09 from the prior year, while adjusted diluted EPS was $0.35, down $0.03 year-over-year.

Despite these declines, the company achieved a bright spot with adjusted EBITDA, which increased 1.6% to $162.0 million. The EBITDA margin expanded by 30 basis points to 10.4% of sales, driven by improved gross margin and lower adjusted selling, distribution, and administrative expenses.

The following chart illustrates this EBITDA improvement:

The company’s financial review provides a comprehensive breakdown of these metrics:

Detailed Financial Analysis

Cash flow generation remained solid with $135.6 million from operations during the quarter. Capital expenditures totaled $25.6 million, while the company paid $52.3 million in dividends, maintaining its commitment to shareholder returns. Notably, Flowers Foods spent $791.9 million on acquisition during the period, which appears to be related to the Simple Mills purchase.

The company’s focus on higher-margin branded products continues to be a key strategy, though the challenging economic environment has pressured consumers. This is evident in the branded versus store brand market share trends, which show that after years of branded share gains, inflationary pressures have slightly reversed the trend, with store brands gaining modest share in recent periods.

Strategic Initiatives & Acquisition

Flowers Foods emphasized its strategic investments in innovation and targeting significant opportunities in faster-growing categories and adjacencies to mitigate category weakness. The acquisition of Simple Mills represents a significant move in this direction, with the specialty food company expected to contribute between $218 million and $225 million in partial-year net sales for fiscal 2025.

The company’s key messages highlight its focus on product quality and innovation:

This strategic shift comes at a time when consumer preferences continue to evolve, with increasing demand for healthier, specialty, and premium bakery products. The Simple Mills acquisition appears to be central to Flowers Foods’ strategy to capture growth in these segments, though the integration will impact earnings in the short term, with Simple Mills expected to contribute negatively to adjusted diluted EPS by $0.07 to $0.08 in fiscal 2025.

Forward-Looking Statements

Flowers Foods adjusted its fiscal 2025 guidance to reflect the more challenging consumer environment and potential for increased tariff costs. The company now projects total net sales of $5.297 billion to $5.395 billion, including Simple Mills’ contribution.

Adjusted EBITDA is expected to range from $534 million to $562 million, with total adjusted diluted EPS projected at $1.05 to $1.15. The guidance includes the impact of a 53rd week, which is expected to contribute $70-80 million in net sales and approximately $0.02 to adjusted EPS.

Notably, the company increased its expected tariff impact from $10 million to $31-36 million, highlighting growing concerns about trade policies affecting input costs. Other considerations mentioned include consumer resiliency, the promotional environment, Simple Mills integration, and the timing and effectiveness of cost-saving initiatives.

The detailed fiscal 2025 guidance is presented below:

The adjusted guidance and premarket stock decline suggest investors may be concerned about the company’s ability to navigate the challenging consumer environment and successfully integrate the Simple Mills acquisition. However, Flowers Foods’ ability to improve margins and maintain market share for its leading brands indicates resilience in its core business despite the headwinds.

As the company moves through 2025, its focus on innovation, strategic acquisitions, and margin improvement will be critical to offsetting category weakness and delivering value to shareholders in an increasingly competitive and cost-pressured bakery market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.