Domo signs strategic collaboration agreement with AWS for AI solutions

Introduction & Market Context

Flowers Foods , Inc. (NYSE:FLO) released its first quarter 2025 financial results on May 16, 2025, revealing a challenging period marked by sales and profit declines amid ongoing consumer pressures. The company, one of the largest producers of packaged bakery foods in the United States, reported results for the 16-week period ended April 19, 2025, highlighting both operational challenges and strategic developments, including the recent acquisition of Simple Mills.

The results come as Flowers Foods navigates a difficult market environment, with the stock trading near its 52-week low of $15.27. Following the earnings release, which missed analyst expectations, FLO shares dropped 4.22% in pre-market trading, reflecting investor concerns about the company’s near-term outlook.

Quarterly Performance Highlights

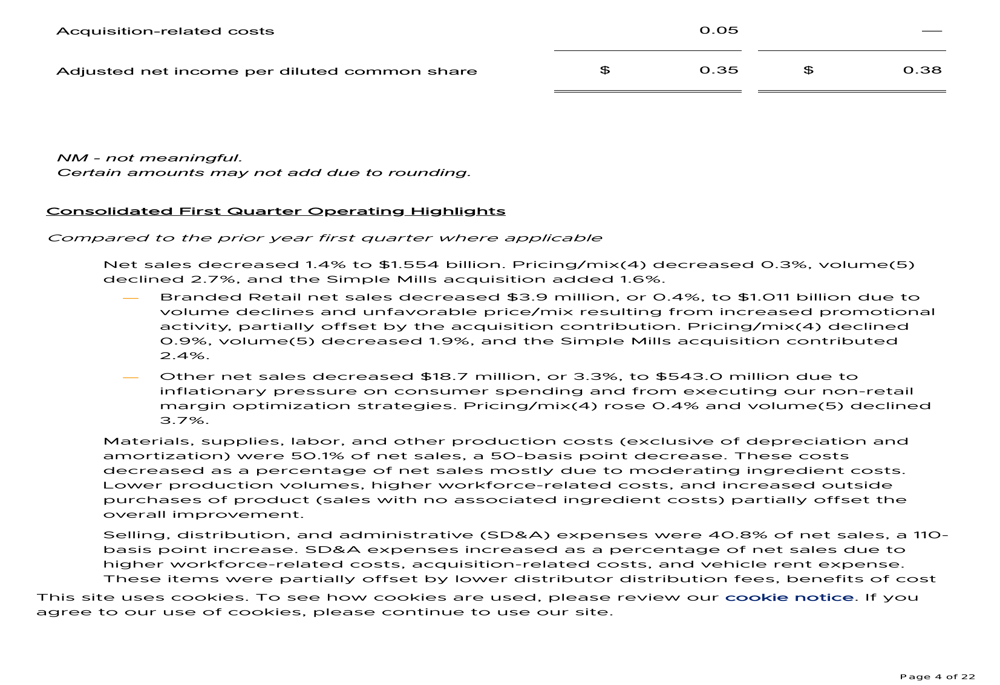

Flowers Foods reported a 1.4% decrease in net sales to $1.554 billion for the first quarter, falling short of the $1.6 billion expected by analysts. This decline was attributed to a combination of pricing/mix decrease of 0.3% and volume decline of 2.7%, partially offset by a 1.6% contribution from the Simple Mills acquisition.

Net income decreased significantly by 27.4% to $53.0 million, representing 3.4% of sales—a 120-basis point decrease from the prior year. Adjusted net income, which excludes certain one-time items, decreased 8.2% to $73.7 million. Diluted earnings per share fell $0.09 to $0.25, while adjusted diluted EPS decreased $0.03 to $0.35, missing the analyst forecast of $0.38.

Despite these challenges, adjusted EBITDA showed modest improvement, increasing 1.6% to $162.0 million and representing 10.4% of net sales—a 30-basis point increase from the prior year.

Detailed Financial Analysis

The company’s sales performance varied across segments. Branded Retail net sales decreased marginally by 0.4% to $1.011 billion, with pricing/mix declining 0.9% and volume decreasing 1.9%. This was partially offset by a 2.4% contribution from the Simple Mills acquisition. The "Other" category, which includes foodservice and private label products, saw a more significant decline of 3.3% to $543.0 million.

On the cost side, Flowers Foods showed some improvement in production efficiency, with materials, supplies, labor, and other production costs decreasing 50 basis points to 50.1% of net sales. However, selling, distribution, and administrative expenses increased 110 basis points to 40.8% of net sales, reflecting higher costs associated with the Simple Mills acquisition and integration.

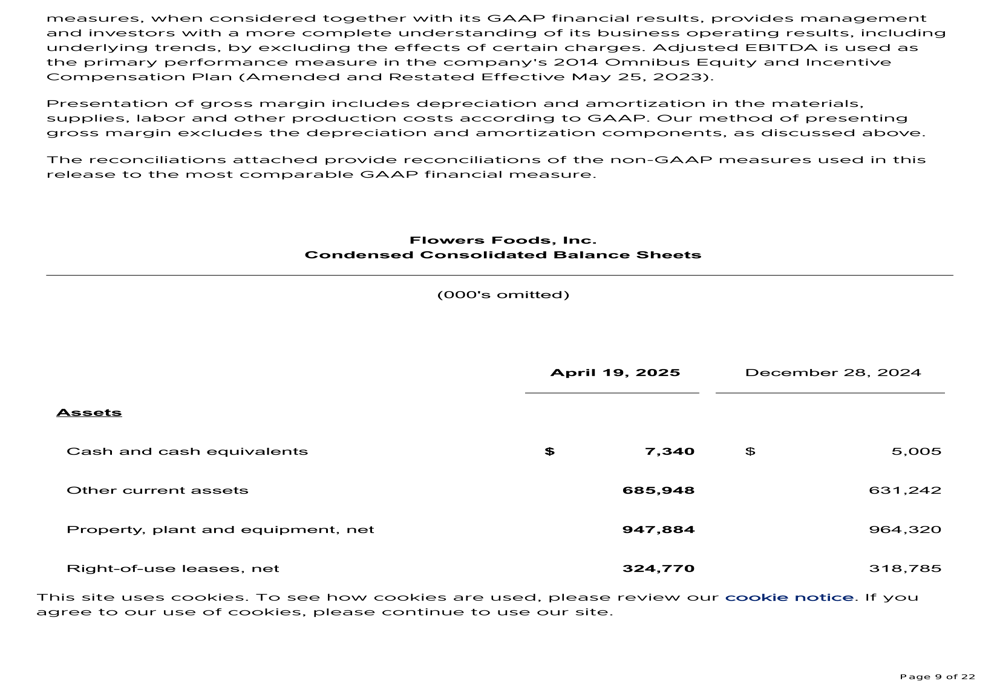

The company’s balance sheet underwent significant changes during the quarter, primarily due to the Simple Mills acquisition. Long-term debt increased from $1.02 billion to $1.79 billion, while total assets grew from $3.40 billion to $4.33 billion, with a substantial increase in goodwill and intangible assets.

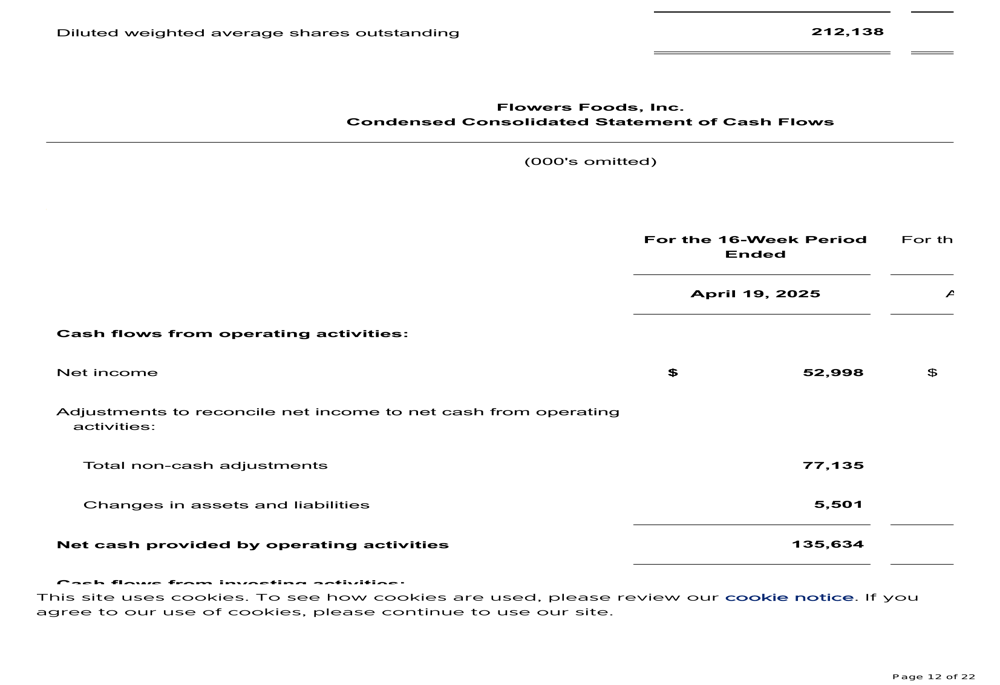

Cash flow from operating activities showed improvement, increasing $30.5 million to $135.6 million. Capital expenditures decreased $7.8 million to $25.6 million, while dividends paid to shareholders increased slightly to $52.3 million. The company ended the quarter with $7.3 million in cash and cash equivalents.

Strategic Initiatives & Acquisition Impact

The acquisition of Simple Mills represents a significant strategic move for Flowers Foods as it seeks to expand its presence in the premium, health-focused segment of the bakery market. During the first quarter, Simple Mills contributed $24.3 million in net sales and $3.6 million to adjusted EBITDA, though it resulted in a net loss of $4.2 million and was dilutive to EPS by $0.02.

CEO Ryals McMullen emphasized the company’s commitment to innovation during the earnings call, stating, "We’re continuing to invest in on-trend innovation and targeting significant opportunities." This aligns with the company’s portfolio strategy, which includes established brands like Nature’s Own, Dave’s Killer Bread, Canyon Bakehouse, Wonder, and Tastykake, alongside the newly acquired Simple Mills.

The company noted it is gaining additional shelf space and winning new business, which could help offset some of the volume challenges in future quarters. However, the earnings call revealed concerns about the broader bread category, which is experiencing declining sales due to changing consumer preferences and potentially the impact of GLP-1 weight loss drugs on food consumption patterns.

Forward-Looking Statements

Despite current challenges, Flowers Foods provided a cautiously optimistic outlook for fiscal 2025, which will include 53 weeks. The company expects net sales of approximately $5.297 billion to $5.395 billion, representing 3.8% to 5.7% growth compared to the prior year.

It’s worth noting that excluding the Simple Mills acquisition, which is expected to contribute $218 million to $225 million, organic net sales growth would be between -0.5% and 1.3%. The additional 53rd week is expected to contribute $70 million to $80 million to net sales.

For profitability, Flowers Foods projects adjusted EBITDA in the range of $534 million to $562 million and adjusted diluted EPS of approximately $1.05 to $1.15. Excluding Simple Mills, adjusted diluted EPS would be higher at $1.13 to $1.22, indicating the near-term dilutive effect of the acquisition.

The company acknowledged potential headwinds, including the challenging consumer environment and increased tariff costs, which CFO Steve Kinsey addressed during the earnings call, noting, "We’re taking a fairly conservative view on tariffs." Management expects performance to improve as consumer health recovers, with more significant improvements potentially not materializing until 2026.

Capital expenditures for the year are projected at $140 million to $150 million, with $4 million to $6 million related to an ERP system upgrade. The company also anticipates an effective tax rate of approximately 25% and weighted average diluted share count of approximately 212.3 million shares.

As Flowers Foods navigates these challenges and integrates its strategic acquisition, investors will be closely watching whether the company can reverse the volume declines and leverage its expanded portfolio to drive sustainable growth in an increasingly competitive and evolving bakery market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.