Can anything shut down the Gold rally?

Introduction & Market Context

FLSmidth & Co. (CPH:FLS) shares surged 8.58% to DKK 362 on May 14, 2025, after the Danish engineering company released its Q1 2025 interim financial report showing substantial profitability improvements despite lower order intake. The company raised its full-year guidance, citing a stronger-than-anticipated start to 2025, even as it navigates mixed market conditions in its mining and cement segments.

The mining service market remained stable overall but showed relative softness in North America due to macroeconomic and tariff-related uncertainties. Meanwhile, customers continued to hesitate on larger capital expenditures while showing interest in smaller product solutions that drive efficiency or reduce maintenance costs.

Quarterly Performance Highlights

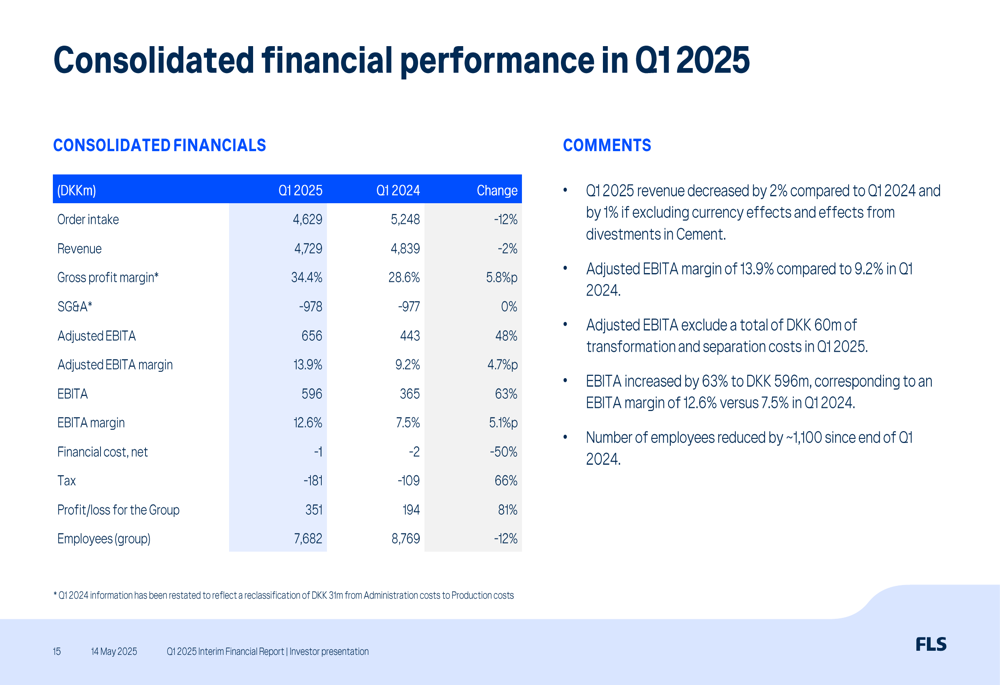

FLSmidth reported consolidated Q1 2025 revenue of DKK 4,729 million, a slight 2% decrease from Q1 2024, while order intake fell 12% to DKK 4,629 million. However, profitability metrics improved significantly, with gross profit margin expanding by 5.8 percentage points to 34.4% and adjusted EBITA increasing 48% to DKK 656 million.

As shown in the following comprehensive financial overview, the company’s profit for the period jumped 81% to DKK 351 million, driven by improved operational efficiency and strategic portfolio adjustments:

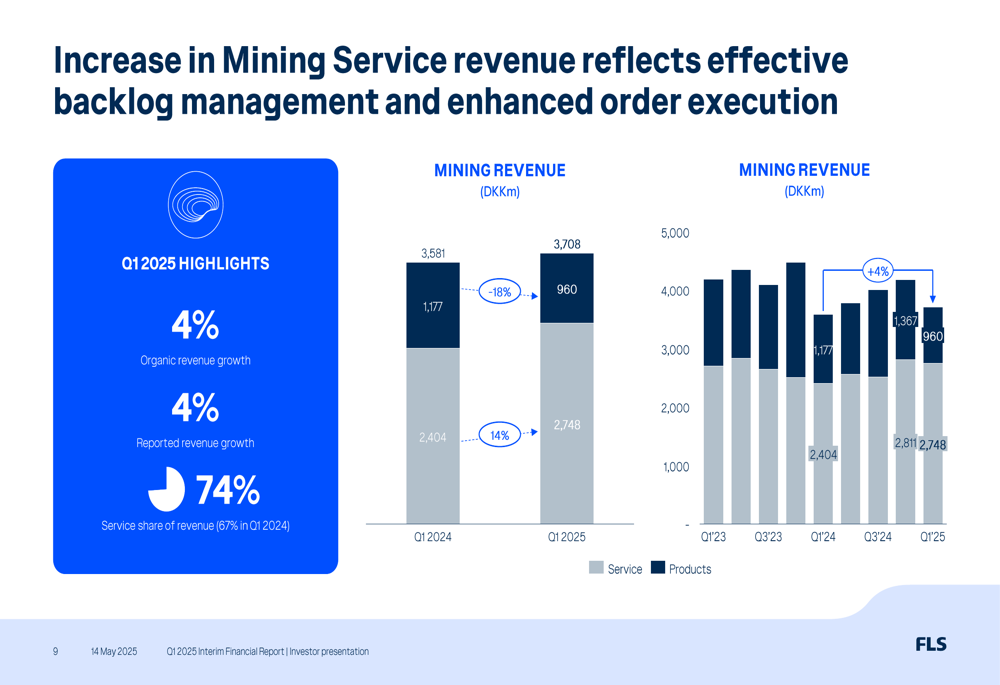

The Mining segment, which accounts for approximately 78% of group revenue, saw organic revenue growth of 4%, with service revenue increasing 14% year-over-year to DKK 2,748 million. This growth was attributed to effective backlog management and enhanced order execution. However, products revenue declined by 18% to DKK 960 million, reflecting the company’s strategic de-risking and portfolio pruning.

The following chart illustrates the Mining segment’s revenue performance:

Mining segment profitability showed substantial improvement, with adjusted EBITA margin reaching 15.1% in Q1 2025, excluding DKK 51 million in transformation and separation costs:

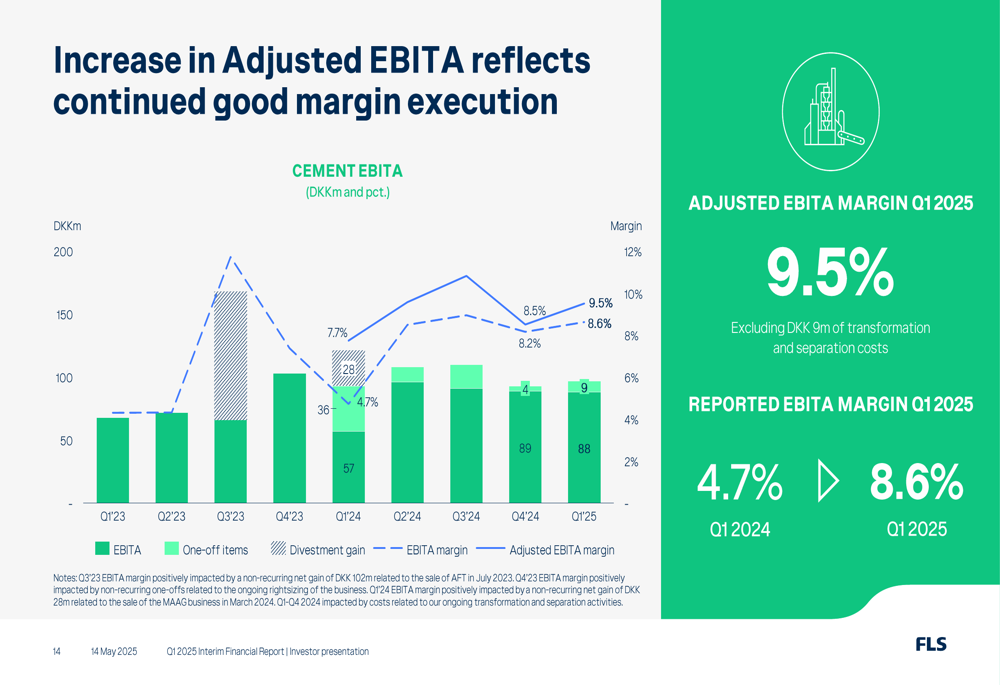

The Cement segment faced more significant challenges, with organic revenue declining 11% and reported revenue down 15% to DKK 1,021 million. Despite these headwinds, the segment achieved an adjusted EBITA margin of 9.5%, excluding DKK 9 million in transformation and separation costs, as shown below:

Strategic Initiatives

FLSmidth’s strategic shift toward a more service-oriented business model continues to yield positive results. The service share of revenue increased to 74% in Mining (up from 67% in Q1 2024) and 70% in Cement (up from 60%), contributing to the overall margin improvement.

The company made further progress toward the potential divestment of its Cement business, entering exclusive negotiations with Pacific Avenue Capital Partners (WA:CPAP), a global investment fund specializing in industrial carve-outs. While FLSmidth noted that there is no certainty a transaction will transpire, this development marks a significant step in the company’s strategic transformation.

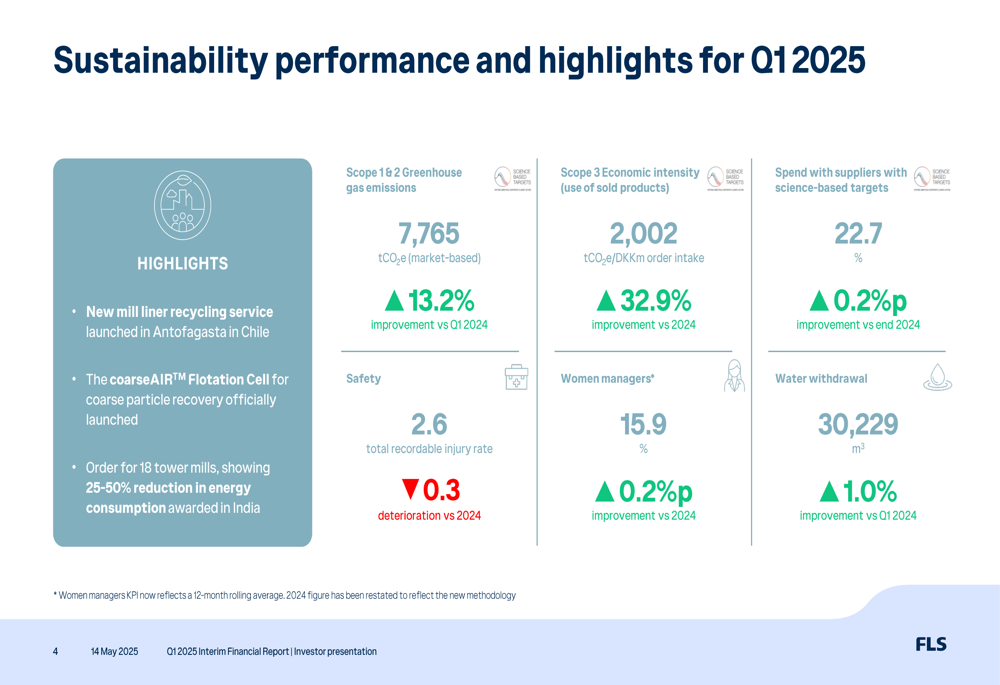

On the sustainability front, FLSmidth reported a 13.2% improvement in Scope 1 & 2 greenhouse gas emissions compared to Q1 2024 and a 32.9% improvement in Scope 3 economic intensity. The company also launched new sustainable solutions, including a mill liner recycling service and the coarseAIR™ Flotation Cell.

The following chart highlights key sustainability metrics:

FLSmidth is actively addressing potential tariff impacts, with approximately 20% of sales coming from the US and about 50% of those being imports. The company has implemented proactive mitigation measures, including leveraging its large US manufacturing footprint, reducing China-US supply flows, and optimizing supply chain efficiency.

Forward-Looking Statements

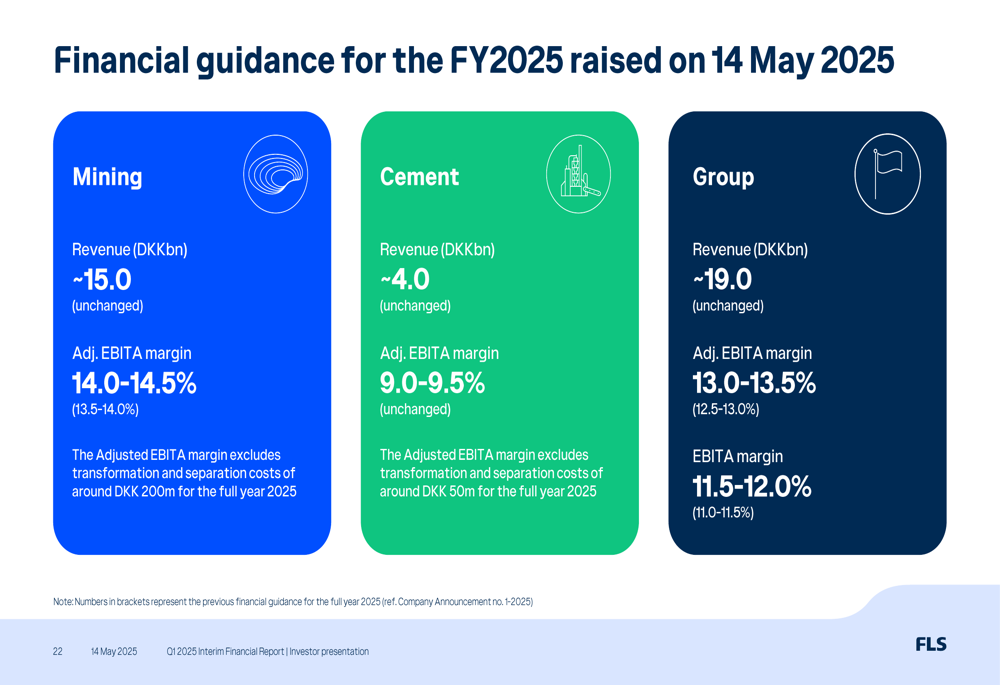

Based on the strong Q1 performance, FLSmidth raised its financial guidance for FY 2025 on May 14, 2025. While revenue targets remained unchanged at approximately DKK 19 billion for the Group, profitability expectations were increased across all segments:

The improved outlook reflects continued execution of the company’s strategic initiatives, including significant de-risking of order intake, pruning of the Mining Products portfolio, reduction of third-party content in commercial contracts, and exit from non-strategic activities.

Management noted that 2025 has started better than anticipated, with both the Mining and Cement segments showing improved profitability despite challenging market conditions. The company’s financial position remains solid, with a leverage ratio of 0.4x at the end of Q1 2025, well below its capital structure target of less than 2.0x.

With the appointment of Julian Soles as President of Mining Products on May 1, 2025, and the expected arrival of Toni Laaksonen as President of Mining Service, FLSmidth continues to strengthen its leadership team to drive its service-focused strategy forward.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.