SoFi shares rise as record revenue, member growth drive strong Q3 results

Introduction & Market Context

FLSmidth & Co. (CPH:FLS) presented its Q2 2025 interim report on August 20, 2025, highlighting the company’s successful transformation into a pure-play mining industry supplier following the divestment of its Cement business. Despite an 11.7% year-over-year revenue decline, the company reported significant margin improvement, with adjusted EBITA margin reaching 15.2% for continuing operations. This performance has contributed to FLSmidth’s stock price strength, which has increased by 2.15% to DKK 408.4 as of August 19, 2025, approaching its 52-week high of DKK 411.2.

The company’s strategic shift follows its Q1 2025 performance, which saw group revenue of DKK 12.6 billion and an adjusted EBITDA margin of 13.9%. The continued margin improvement in Q2 demonstrates FLSmidth’s successful execution of its simplification initiatives and operational efficiency programs.

Quarterly Performance Highlights

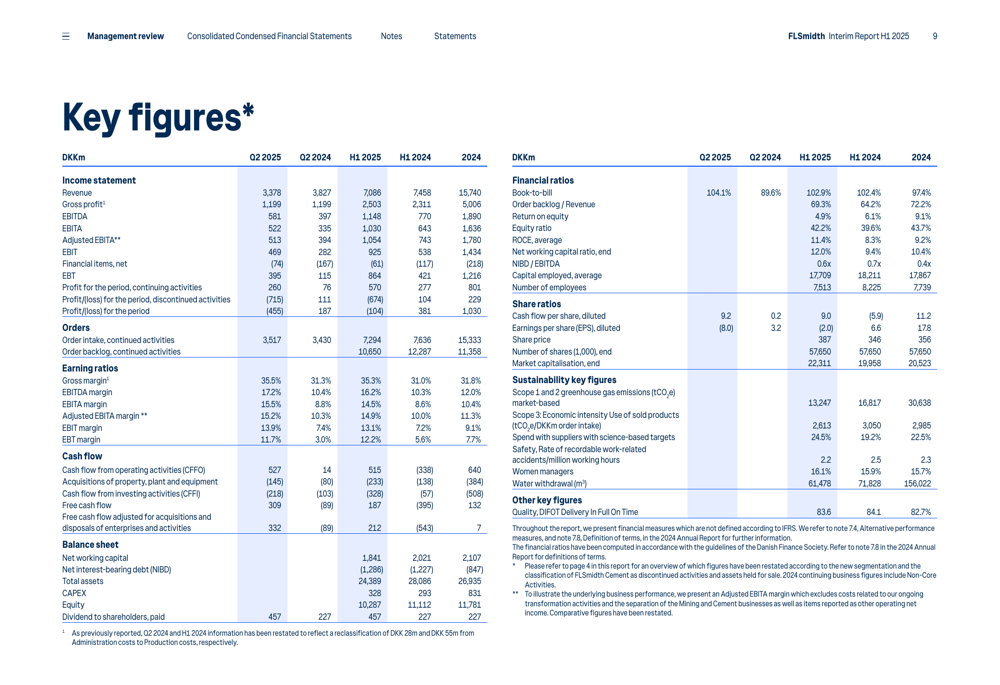

FLSmidth’s Q2 2025 results show a company in transition, with mixed performance across its newly defined segments. Order intake for continuing operations increased by 2.5% to DKK 3,517 million, while revenue decreased by 11.7% to DKK 3,378 million compared to Q2 2024. Despite the revenue decline, profitability improved significantly, with adjusted EBITA margin reaching 15.2%, driven by disciplined execution of strategic priorities and cost reduction initiatives.

As shown in the following financial performance breakdown:

The company’s performance varied significantly by segment. The Service segment, which represents the largest portion of the business, saw a 7.5% decrease in order intake to DKK 2,068 million and a 2.5% decrease in revenue to DKK 2,063 million, but maintained a strong EBITA margin of 19.9%. The Products segment experienced a 44.3% increase in order intake to DKK 681 million, though revenue declined by 42.8% to DKK 607 million, resulting in a negative EBITA margin of -8.1%. The Pumps, Cyclones & Valves (PC&V) segment was the standout performer, with order intake up 7.4% to DKK 768 million and revenue growth of 16.8% to DKK 708 million, achieving an impressive EBITA margin of 22.6%.

Cash flow from operating activities reached DKK 385 million, while earnings per share stood at DKK 4.5. The company maintained a healthy balance sheet with a net working capital ratio of 12.0% and a NIBD/EBITDA ratio of 0.6x.

Strategic Initiatives

Following the company’s strategic pivot to focus exclusively on the mining industry, FLSmidth has reorganized its reporting structure into three segments: Service, Products, and Pumps, Cyclones & Valves (PC&V). This new structure reflects the company’s go-to-market strategy and provides greater transparency into segment performance.

The updated segment reporting structure is illustrated below:

Key strategic developments during Q2 2025 included:

1. The signing of an agreement with Pacific Capital Avenue Partners for the divestment of FLSmidth Cement, completing the company’s transformation into a pure-play mining industry supplier

2. Divestment of corporate headquarters for DKK 730 million, optimizing the company’s real estate footprint

3. Acquisition of a South African manufacturing facility, strengthening regional capabilities

4. Launch of the first share buy-back program since 2012, reflecting confidence in future performance

5. Selection to deliver full flotation technology to an Indian iron ore mine, demonstrating continued commercial success

The company also reported solid progress on its simplification initiatives, with SG&A costs down by approximately 16% compared to Q2 2024, contributing to the improved profitability.

Detailed Financial Analysis

FLSmidth’s comprehensive financial performance is reflected in the key figures table below, which provides a comparison across multiple periods:

The financial data reveals several important trends:

1. While revenue has declined year-over-year, profitability metrics have improved significantly, with adjusted EBITA margin increasing from 11.7% in Q2 2024 to 15.2% in Q2 2025

2. Book-to-bill ratio of 1.04 indicates healthy order intake relative to revenue

3. Return on capital employed (ROCE) has improved to 13.4% from 12.2% in Q2 2024

4. Net interest-bearing debt remains low at DKK 1,508 million, with a NIBD/EBITDA ratio of 0.6x

5. Earnings per share increased to DKK 4.5 in Q2 2025 from DKK 3.9 in Q2 2024

These figures demonstrate that while FLSmidth is experiencing revenue challenges, particularly in the Products segment, the company’s focus on operational efficiency and cost reduction is yielding significant improvements in profitability and cash flow generation.

Sustainability Performance

FLSmidth continues to make progress on its sustainability initiatives, with improvements across key metrics as shown in the following sustainability performance highlights:

The company reported a 21.2% improvement in Scope 1 & 2 greenhouse gas emissions, which reached 13,247 tCO2e (market-based) in Q2 2025. Scope 3 economic intensity improved by 12.5% to 2,613 tCO2e/DKKm order intake. The percentage of spend with suppliers with science-based targets increased by 2.0 percentage points to 24.5%.

Safety performance also improved, with the rate of recordable work-related accidents per million working hours decreasing to 2.2, a 0.1 improvement. The percentage of women managers increased by 0.4 percentage points to 16.1%, and water withdrawal decreased by 14.4% to 61,478 m3.

These sustainability improvements were supported by various initiatives, including:

The company’s sustainability efforts were recognized with a silver medal from EcoVadis in June 2025, highlighting FLSmidth’s commitment to responsible business practices.

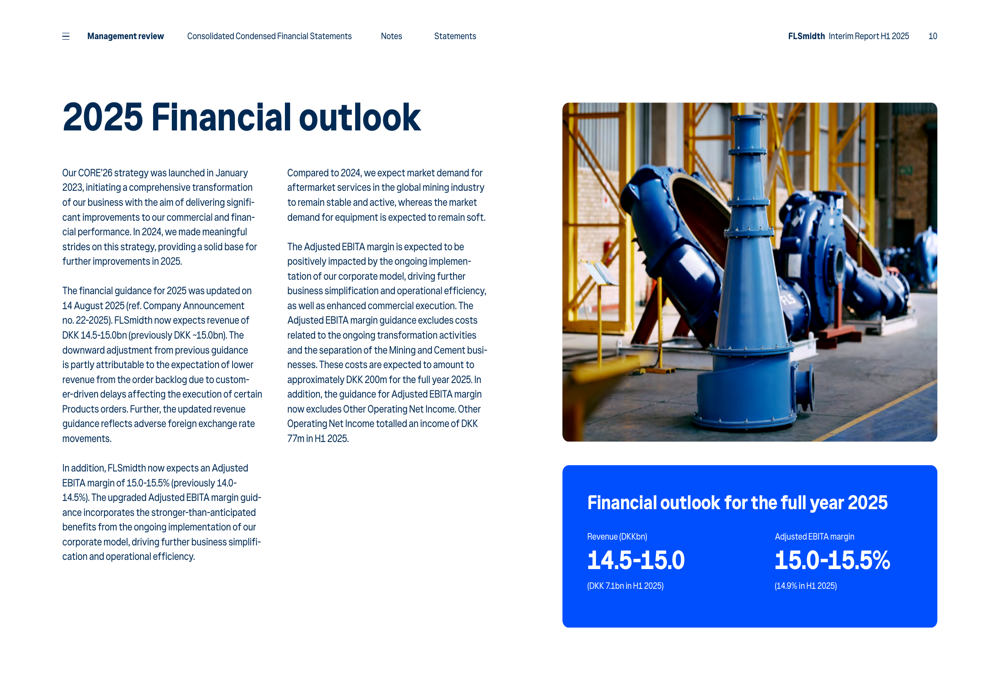

Forward-Looking Statements

FLSmidth has updated its financial guidance for 2025, reflecting both challenges and opportunities in the current market environment:

The company now expects revenue of DKK 14.5-15.0 billion for 2025, slightly lower than the previous guidance of approximately DKK 15.0 billion. This reduction is attributed to lower revenue from the order backlog and adverse foreign exchange rate movements.

Despite the lower revenue guidance, FLSmidth has increased its adjusted EBITA margin guidance to 15.0-15.5%, up from the previous 14.0-14.5%. This improvement reflects stronger-than-anticipated benefits from the ongoing implementation of the company’s corporate model, driving further business simplification and operational efficiency.

The market outlook remains mixed, with demand for aftermarket services in the global mining industry expected to remain stable and active, while demand for equipment is anticipated to remain soft. This aligns with the company’s segment performance, where Service and PC&V (which is 75% aftermarket-related) are outperforming the Products segment.

Conclusion

FLSmidth’s Q2 2025 results demonstrate the company’s successful transformation into a focused mining industry supplier with improved profitability despite revenue challenges. The divergent performance across segments highlights both opportunities and areas requiring attention, with the Service and PC&V segments delivering strong results while the Products segment continues to struggle.

The company’s updated guidance reflects confidence in its ability to continue improving margins through operational efficiency and business simplification, even as revenue growth faces headwinds from market conditions and currency effects. With a solid balance sheet, strong cash flow generation, and strategic initiatives progressing as planned, FLSmidth appears well-positioned to navigate the current market environment while building long-term value for shareholders.

Investors will likely focus on the company’s ability to improve performance in the Products segment while maintaining the strong results in Service and PC&V, as well as the successful completion of the Cement business divestment and the realization of anticipated cost synergies.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.