Domo signs strategic collaboration agreement with AWS for AI solutions

Introduction & Market Context

Flywire Corporation (NASDAQ:FLYW) released its Q1 2025 earnings presentation on May 6, 2025, showcasing a strong rebound from its disappointing Q4 2024 performance. The payment solutions provider reported results that exceeded guidance across key metrics, with its stock rising 3.4% to close at $10.04, reflecting investor confidence in the company’s recovery trajectory.

The presentation highlighted Flywire’s continued execution of its three-pillar strategy focused on a strong "North Star" thesis, differentiated core assets, and vertical expertise in large markets. This quarter marks a significant turnaround following the company’s Q4 2024 earnings miss that previously sent shares tumbling 22%.

Quarterly Performance Highlights

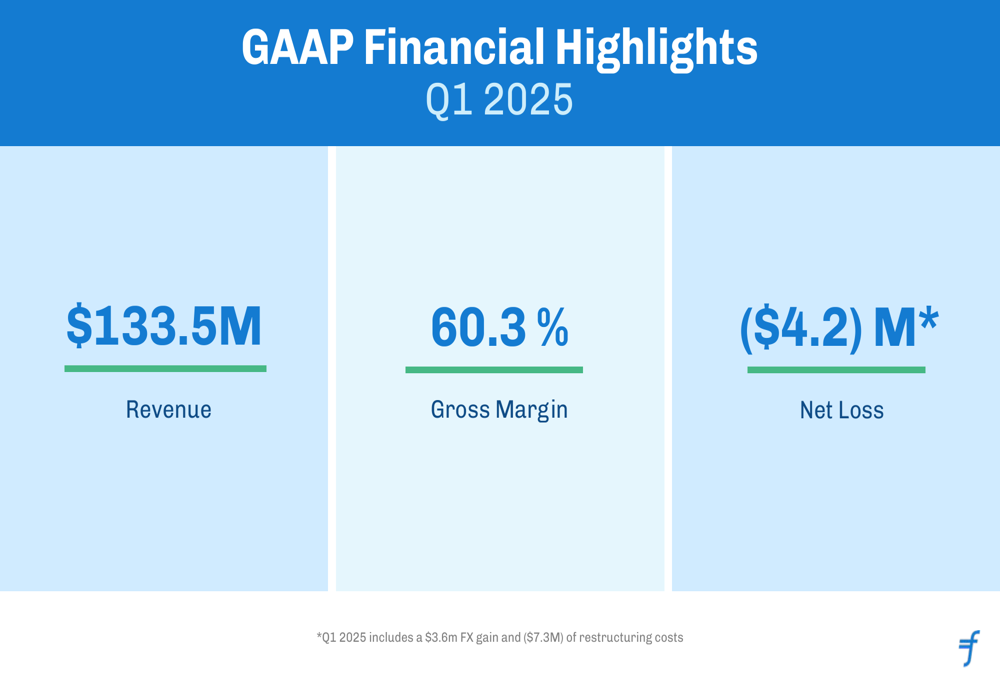

Flywire reported solid GAAP financial results for Q1 2025, with revenue reaching $133.5 million, while posting a net loss of $4.2 million. The quarter included a $3.6 million foreign exchange gain and $7.3 million in restructuring costs.

As shown in the following chart of GAAP financial highlights:

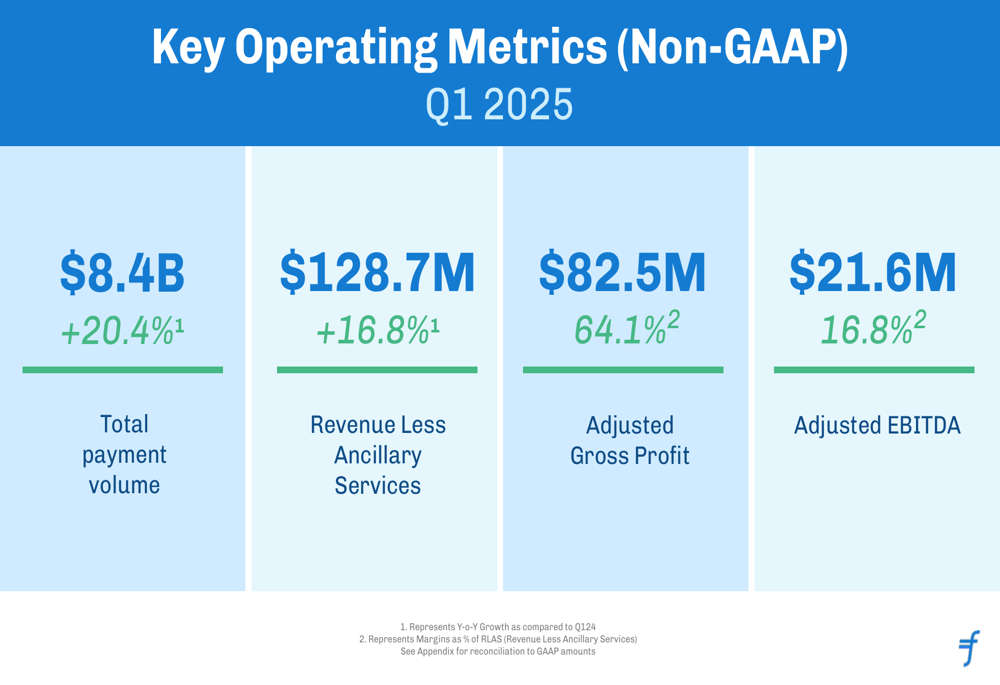

On a non-GAAP basis, Flywire demonstrated strong operational performance with Total (EPA:TTEF) Payment Volume of $8.4 billion, representing 20.4% year-over-year growth. Revenue Less Ancillary Services (RLAS) reached $128.7 million, up 16.8% compared to the same period last year. The company achieved an Adjusted Gross Profit of $82.5 million with a 64.1% margin and Adjusted EBITDA of $21.6 million, representing a 16.8% margin.

The following chart details these key non-GAAP metrics:

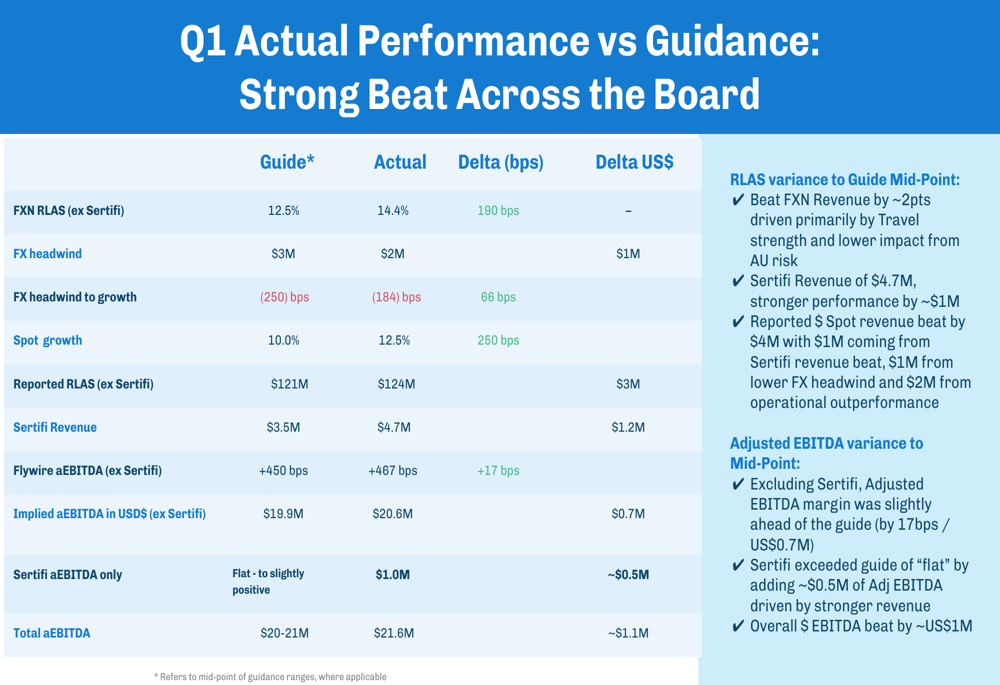

Notably, Flywire exceeded its guidance across all key metrics for the quarter. FX-Neutral Revenue Less Ancillary Services (excluding Sertifi) beat expectations by 1.9%, while Sertifi contributed $4.7 million in revenue, exceeding projections by $1.2 million. Adjusted EBITDA came in at $21.6 million, beating guidance by $1.1 million.

The company’s performance against guidance is illustrated in this comparison:

Strategic Initiatives

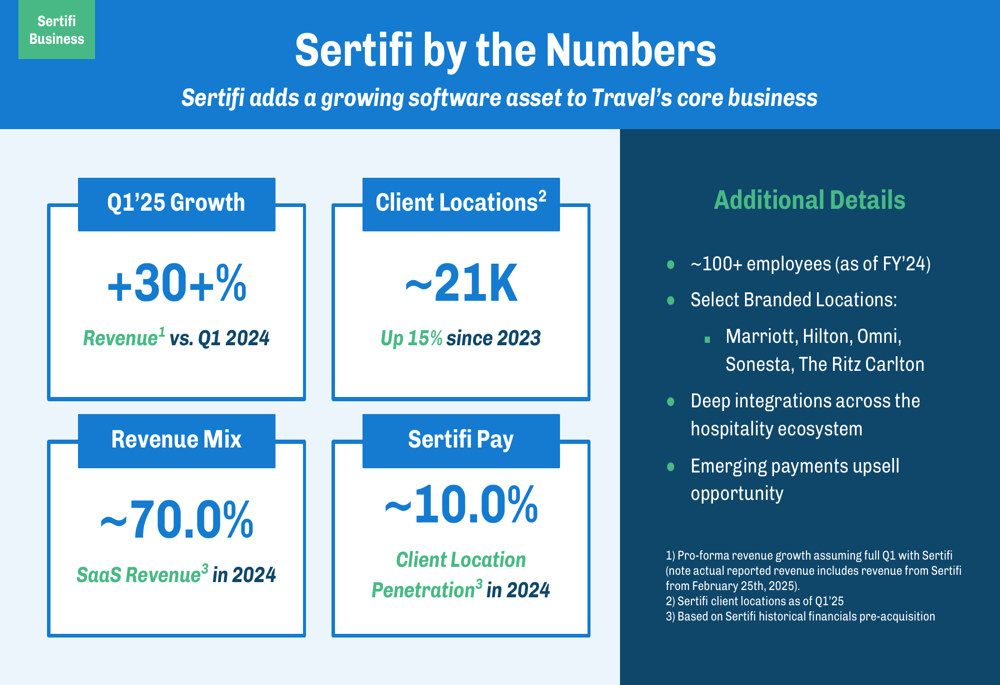

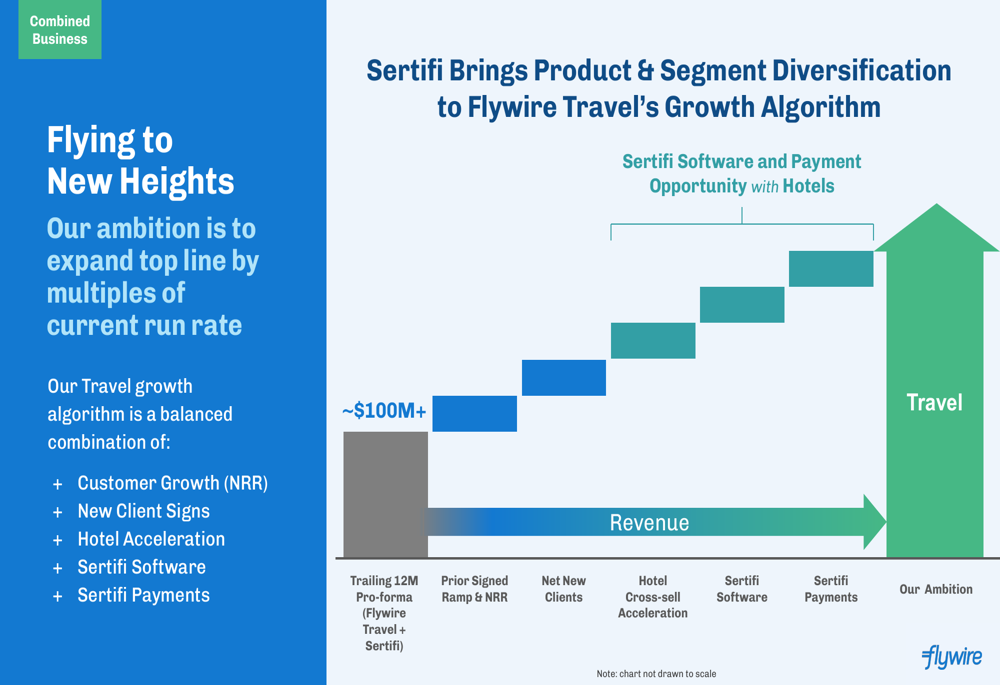

A central focus of Flywire’s Q1 presentation was the strategic acquisition of Sertifi, which closed during the quarter. Sertifi, which automates hospitality workflows by providing paperless solutions for contracts and payments, demonstrated strong performance with over 30% revenue growth compared to Q1 2024.

The acquisition brings significant scale with approximately 21,000 client locations (up 15% since 2023) and a complementary revenue mix of approximately 70% SaaS revenue. Sertifi’s payment solution currently has only about 10% client location penetration, representing a substantial growth opportunity.

The following chart provides key metrics for Sertifi:

Flywire highlighted the complementary nature of this acquisition, noting that while Flywire Travel generates approximately 90% of its revenue internationally, Sertifi derives about 90% of its revenue from the U.S. market. Additionally, Flywire Travel is almost entirely payments-focused, while Sertifi offers a more balanced mix of software (70%) and payments (30%).

The company outlined its strategy to leverage the combined strengths of Flywire Travel and Sertifi to create a comprehensive offering for the hospitality sector. Key initiatives include accelerating the SertifiPay product, expanding Sertifi’s international footprint, capitalizing on accounts receivable cross-sell opportunities, and introducing Flywire’s payables solutions to Sertifi’s customer base.

This growth strategy is illustrated in the following chart:

Detailed Financial Analysis

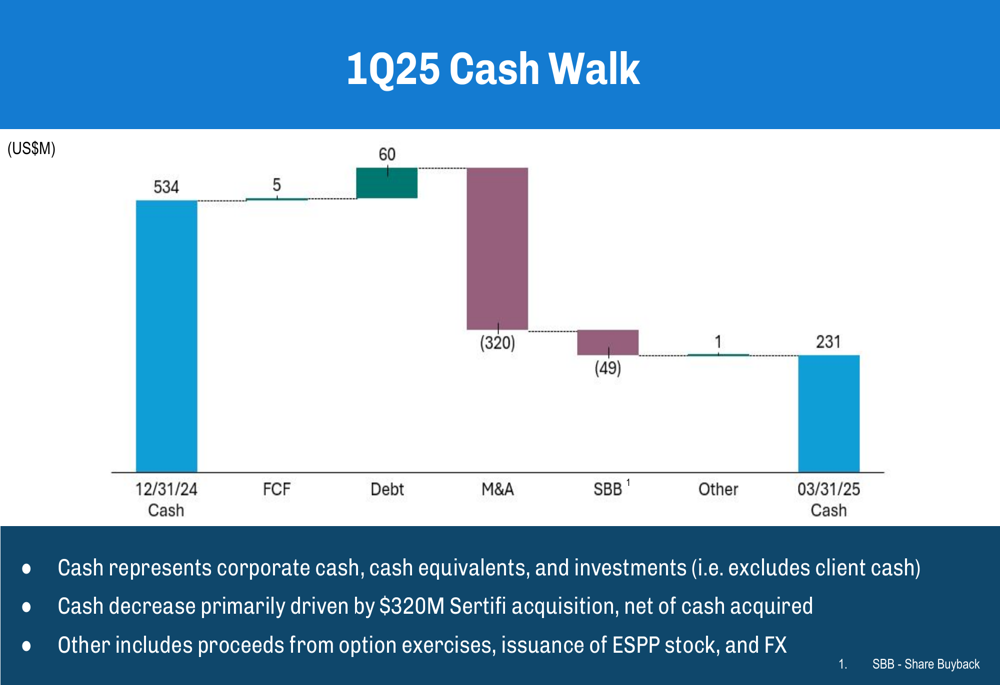

The quarter saw significant changes to Flywire’s cash position due to the Sertifi acquisition. The company’s cash balance decreased from $534 million on December 31, 2024, to $231 million on March 31, 2025, primarily due to the $320 million spent on the acquisition (net of cash acquired). This was partially offset by $60 million in debt contribution and $5 million in free cash flow.

The following cash flow walk illustrates these movements:

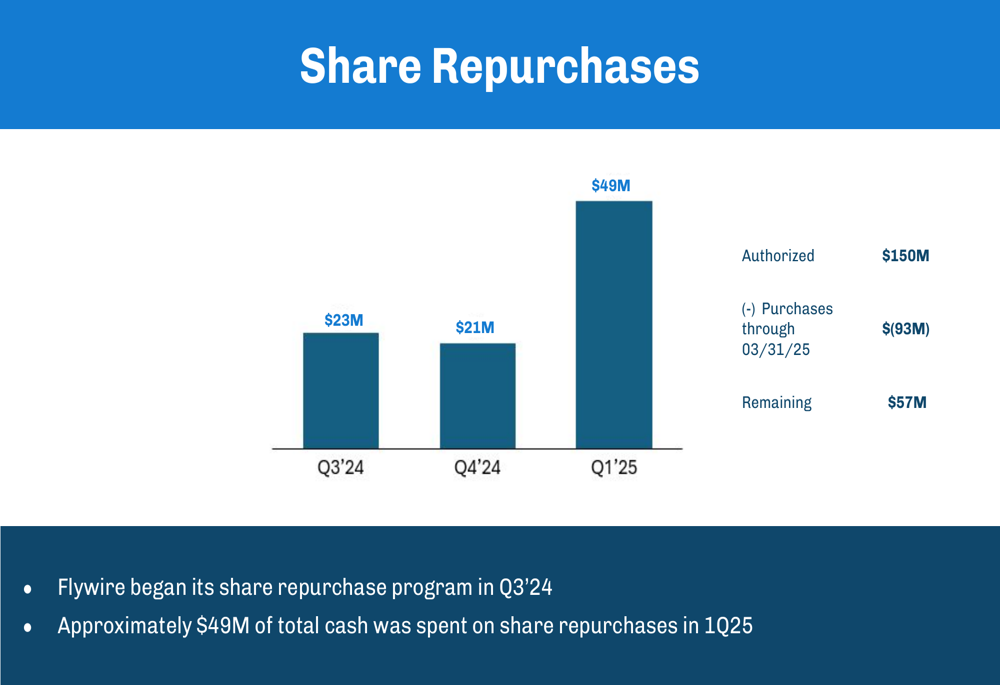

Flywire continued its share repurchase program, buying back $49 million worth of shares in Q1 2025, following $23 million in Q3 2024 and $21 million in Q4 2024. Of the total $150 million authorized for repurchases, $93 million has been used through March 31, 2025, leaving $57 million remaining.

The company’s share repurchase activity is shown in the following chart:

Forward-Looking Statements

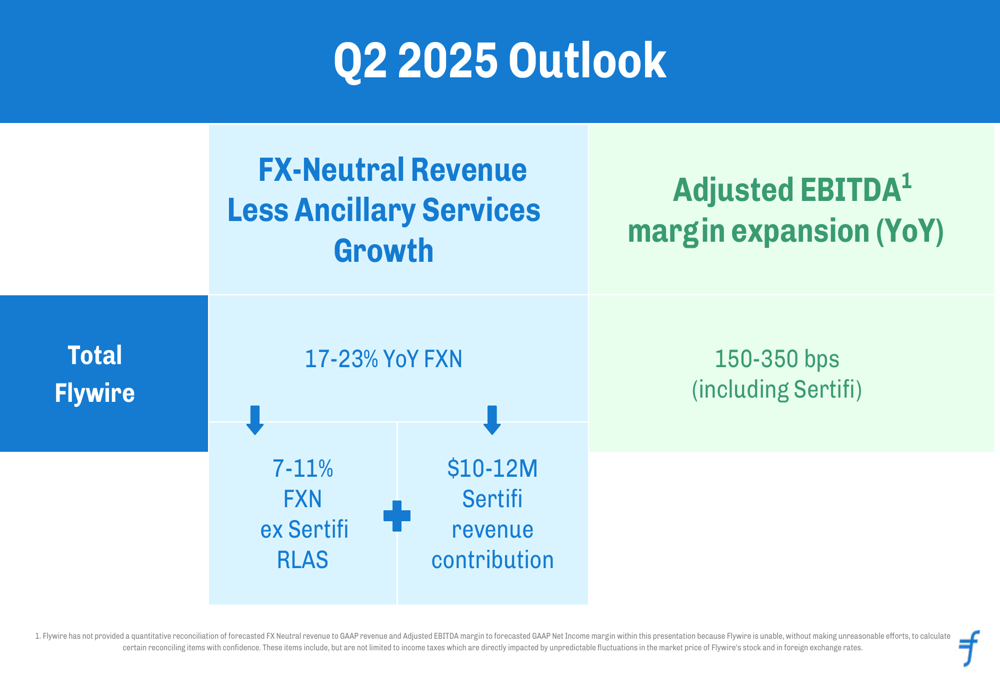

For Q2 2025, Flywire projects 17-23% year-over-year FX-Neutral Revenue Less Ancillary Services growth, comprising 7-11% growth excluding Sertifi and a $10-12 million revenue contribution from Sertifi. The company expects Adjusted EBITDA margin expansion of 150-350 basis points year-over-year.

The Q2 2025 outlook is summarized in the following chart:

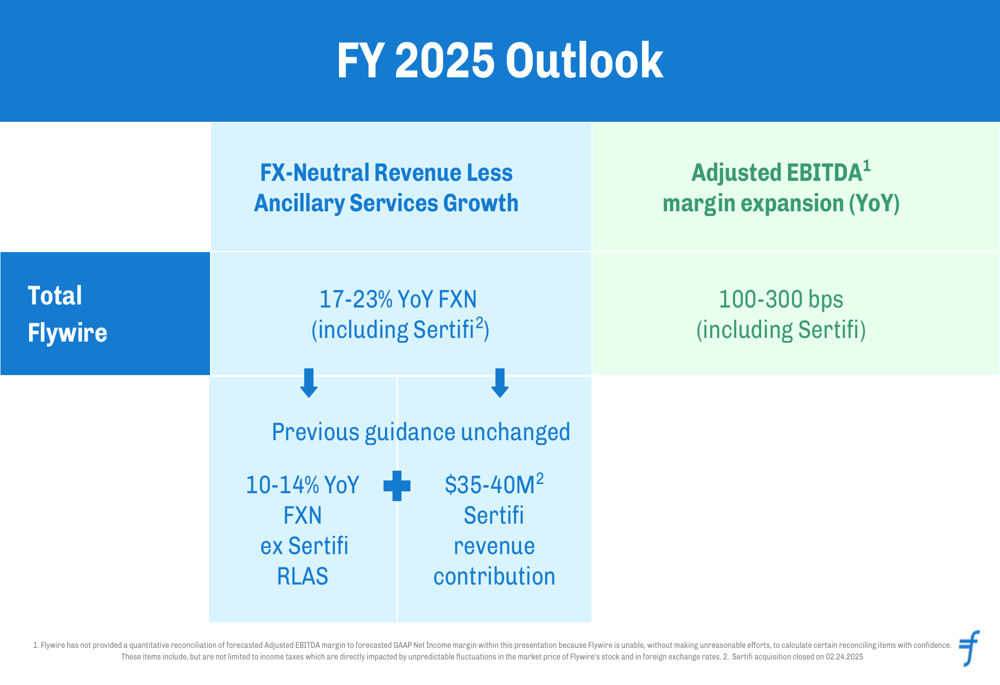

Flywire maintained its full-year 2025 outlook, projecting 17-23% year-over-year FX-Neutral Revenue Less Ancillary Services growth (including Sertifi) and 100-300 basis points of Adjusted EBITDA margin expansion. The company expects 10-14% growth excluding Sertifi and a $35-40 million revenue contribution from Sertifi.

The full-year 2025 outlook is presented in the following chart:

The company noted several factors influencing its guidance, including negative impacts from Easter timing in Q2 and FX headwinds from U.S. dollar weakness. For the full year, Flywire highlighted tougher year-over-year revenue comparisons but remained confident in its ability to deliver Adjusted EBITDA margin expansion.

With its strong Q1 performance and strategic Sertifi integration underway, Flywire appears to be successfully navigating the challenges that impacted its Q4 2024 results, positioning itself for continued growth in its core Education and Travel verticals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.