Oil prices push higher amid worries over Russian supply disruptions

Introduction & Market Context

Flywire Corporation (NASDAQ:FLYW) released its second quarter 2025 earnings presentation on August 5, highlighting stronger-than-expected performance despite regional challenges in its education vertical. The company’s stock closed at $10.33 before the earnings release, with a modest 1.74% gain in aftermarket trading, suggesting investors had mixed reactions to the results.

The global payments company continues to execute on its strategy of combining industry-specific software with a proprietary global payment network to deliver value across its four key verticals: education, healthcare, travel, and B2B payments.

As shown in the following strategic framework, Flywire’s business model centers on its "North Star" thesis that software drives value in payments, supported by differentiated core assets and deep vertical expertise:

Quarterly Performance Highlights

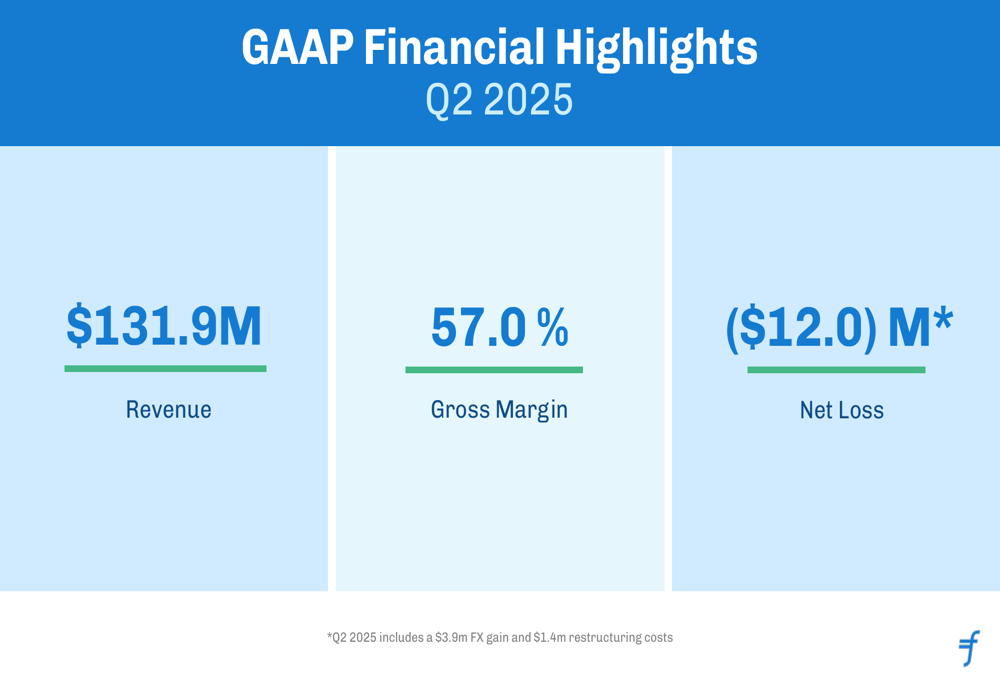

Flywire reported GAAP revenue of $131.9 million for Q2 2025, with a gross margin of 57.0% and a net loss of $12.0 million. The net loss included a $3.9 million foreign exchange gain and $1.4 million in restructuring costs related to the company’s operational review.

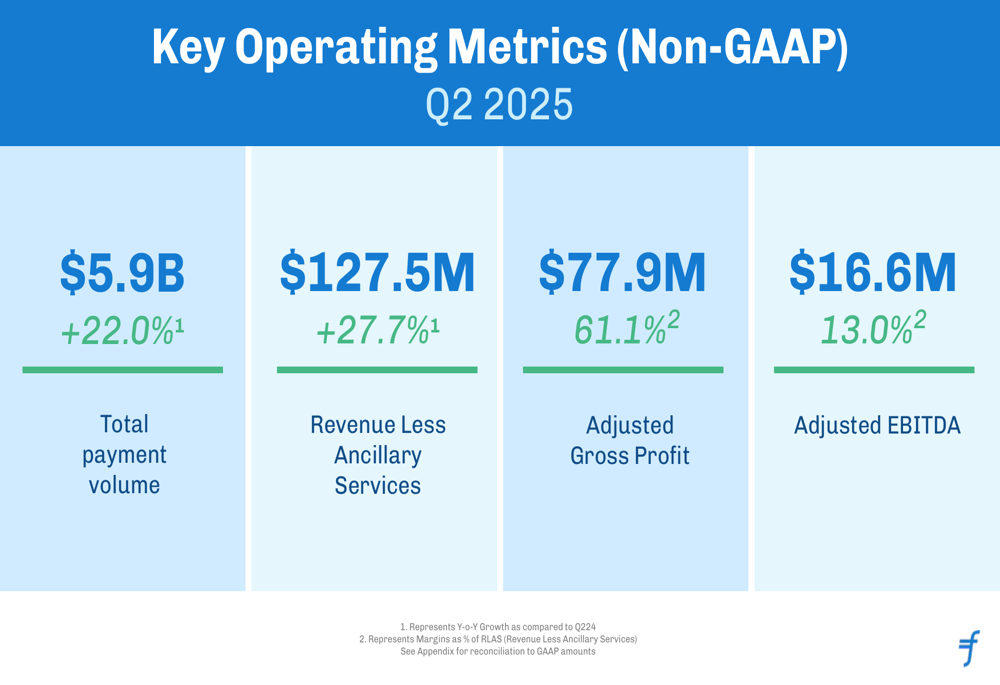

On a non-GAAP basis, Flywire’s key operating metrics showed significant year-over-year growth. Total (EPA:TTEF) payment volume reached $5.9 billion, increasing 22.0% compared to Q2 2024. Revenue Less Ancillary Services (RLAS), a key performance indicator for the company, grew 27.7% year-over-year to $127.5 million. Adjusted gross profit was $77.9 million, representing 61.1% of RLAS, while adjusted EBITDA came in at $16.6 million or 13.0% of RLAS.

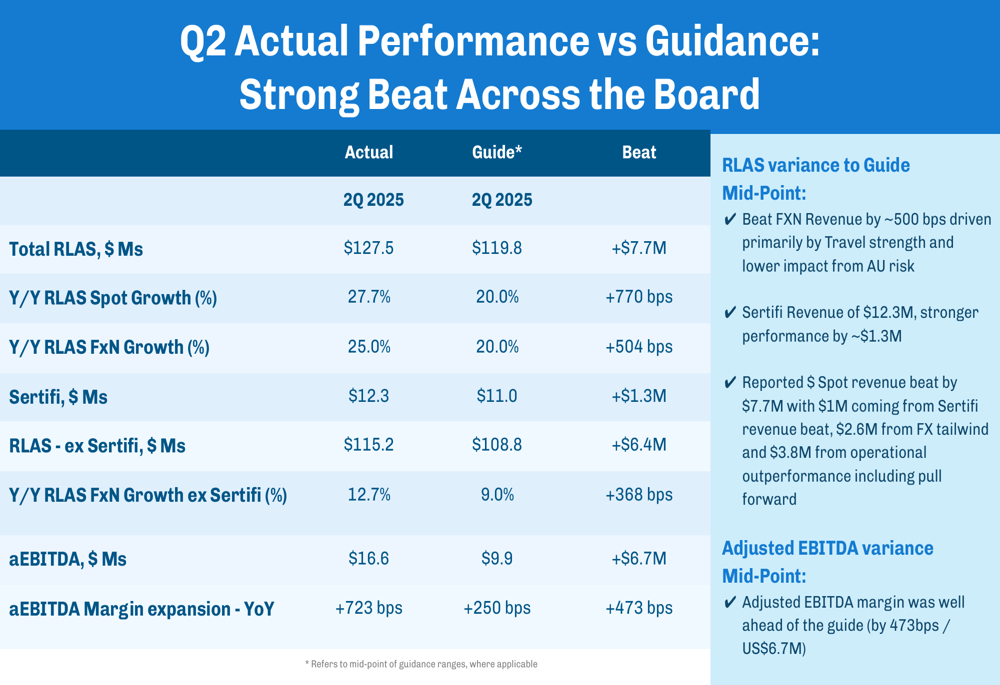

Notably, Flywire significantly outperformed its guidance across all metrics for the quarter. RLAS exceeded guidance by $7.7 million, coming in at $127.5 million versus the guided $119.8 million. Year-over-year RLAS growth was 27.7%, substantially above the guided 20.0%. Adjusted EBITDA of $16.6 million surpassed guidance by $6.7 million, with margin expansion 473 basis points ahead of expectations.

Operational Review & Restructuring

During the first half of 2025, Flywire conducted a comprehensive operational review, resulting in significant organizational changes. The company completed a restructuring that included a 10% reduction in headcount, consolidated its Payments and Product departments, removed layers of management, and realigned IT, systems, data/analytics, and digital transformation under the CFO organization.

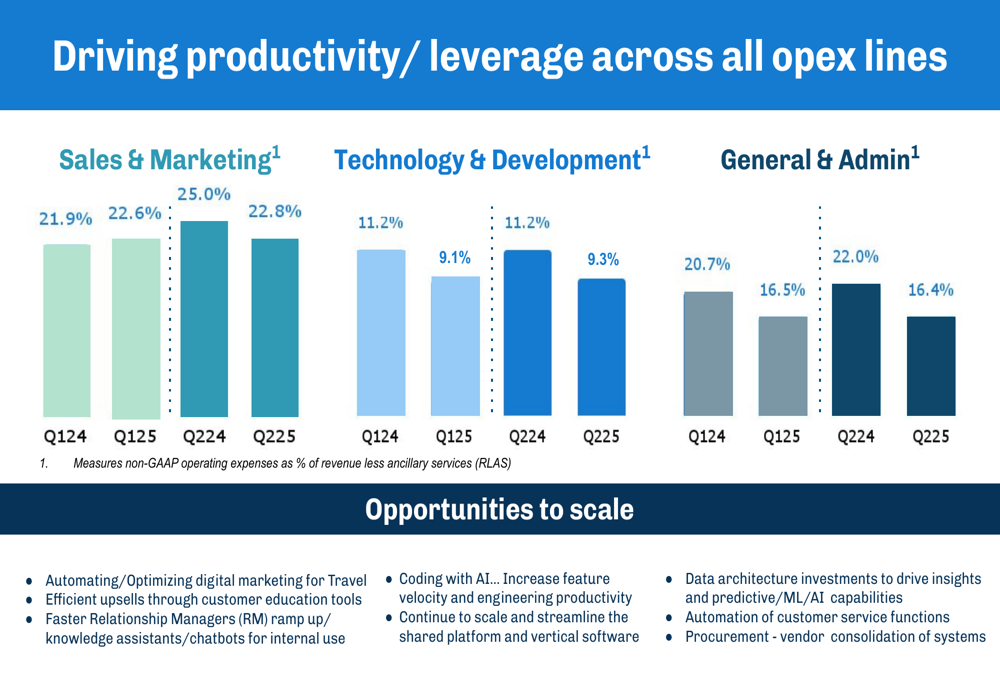

The restructuring efforts have already begun to yield results, with improved operating expense leverage across all expense lines. As shown in the following chart, Flywire has reduced expenses as a percentage of RLAS across Sales & Marketing, Technology & Development, and General & Administrative categories compared to the same quarter last year:

The company is leveraging automation and AI to drive further efficiencies, including optimizing digital marketing for travel, using AI for coding to increase feature velocity and engineering productivity, and making data architecture investments to enable predictive capabilities.

Vertical Performance

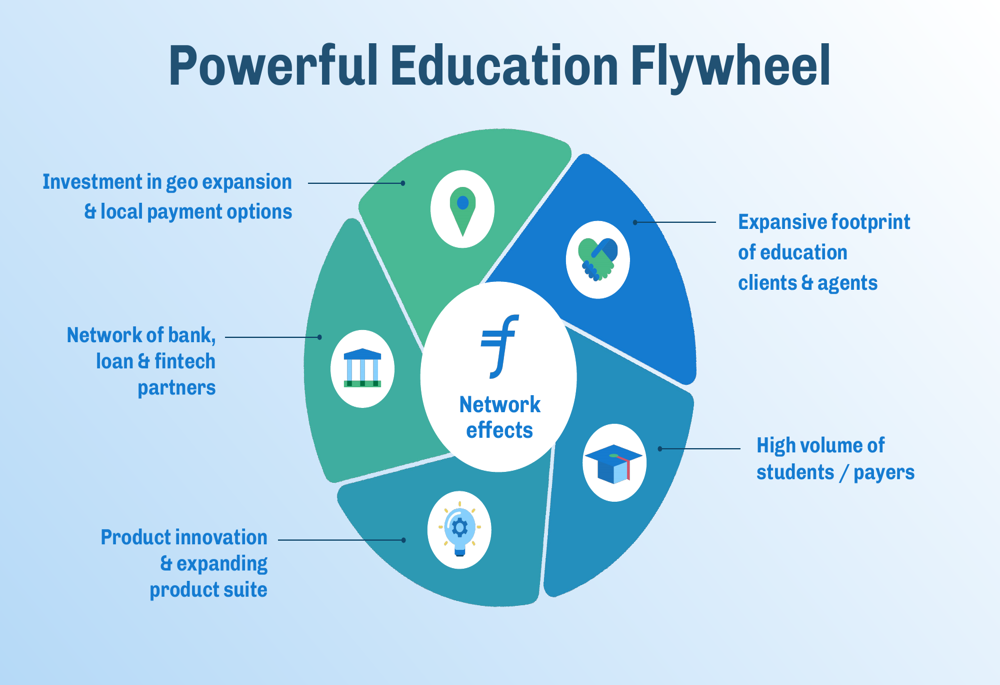

Flywire’s education vertical continues to face headwinds in certain regions, with the company expecting revenues to decline approximately 20% year-over-year in Canada and Australia. U.S. education revenue is expected to remain flat due to decreased F-1 visas. Despite these challenges, Flywire continues to invest in its education strategy, expanding its product suite and global integrations.

The company’s education flywheel demonstrates how various elements work together to create network effects and drive growth:

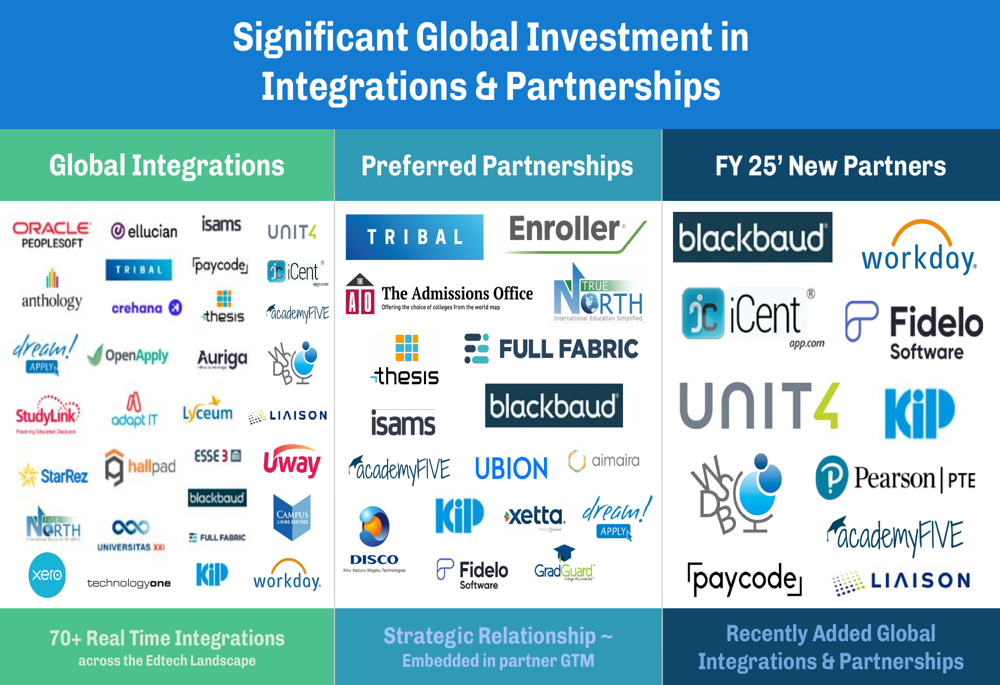

Flywire has established an impressive network of global integrations and partnerships across the education technology landscape, with over 70 real-time integrations and strategic relationships embedded in partner go-to-market strategies:

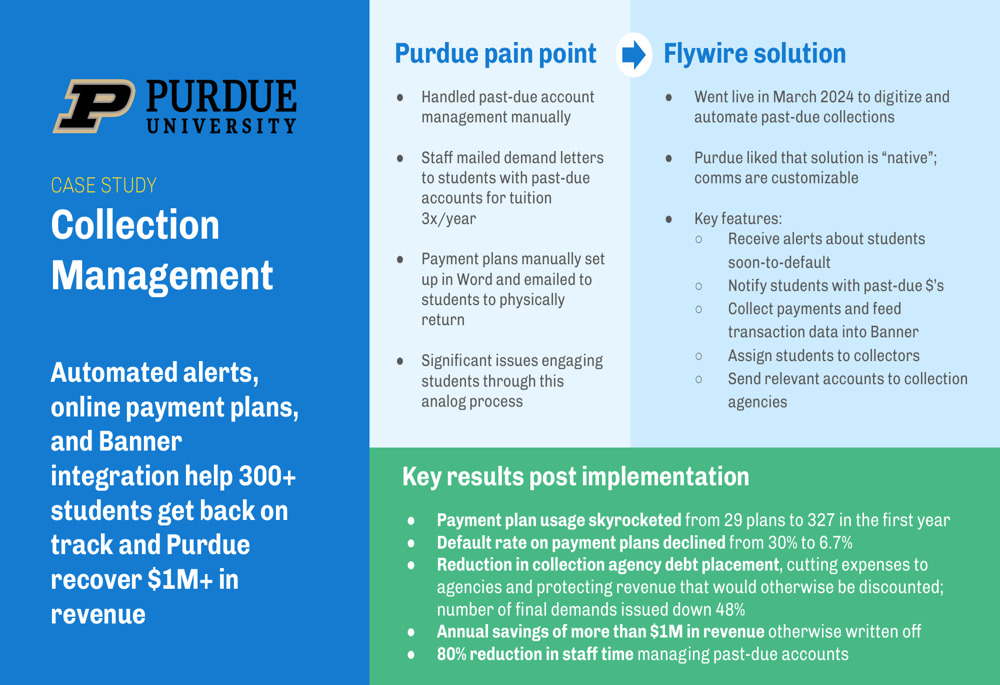

The company highlighted a successful case study with Purdue University, where its Collection Management solution delivered significant results after implementation in March 2024. Payment plan usage increased dramatically from 29 plans to 327, while the default rate declined from 30% to 6.7%. Purdue achieved annual savings of more than $1 million and an 80% reduction in staff time managing past-due accounts.

Meanwhile, the travel vertical showed particular strength in Q2, contributing significantly to the revenue outperformance versus guidance. The healthcare business is expected to grow at a high single-digit rate year-over-year, with most of that growth coming in the second half of 2025.

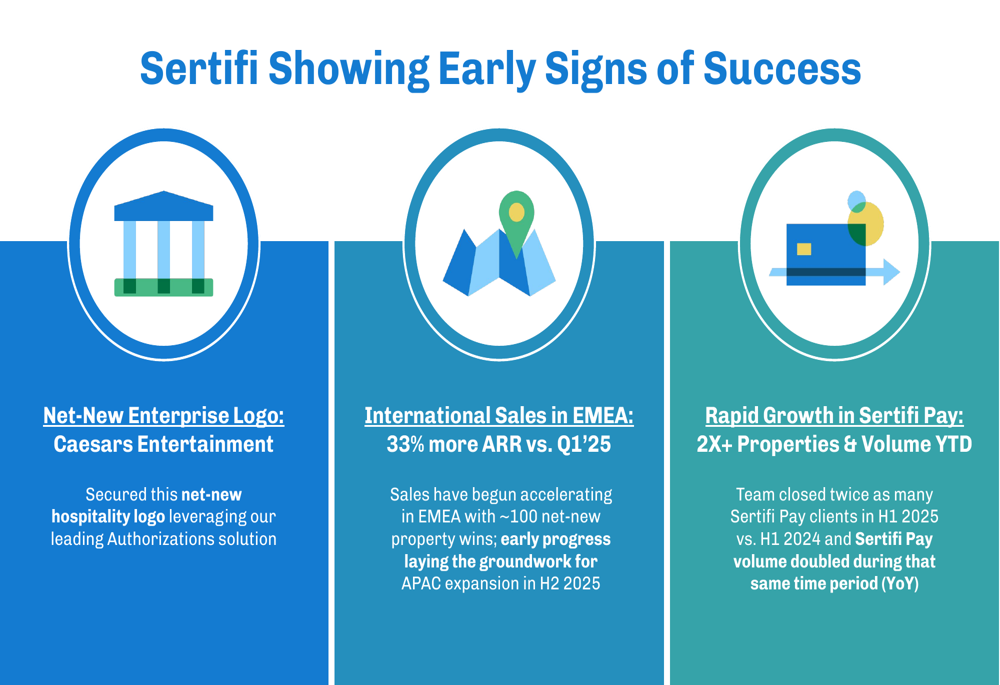

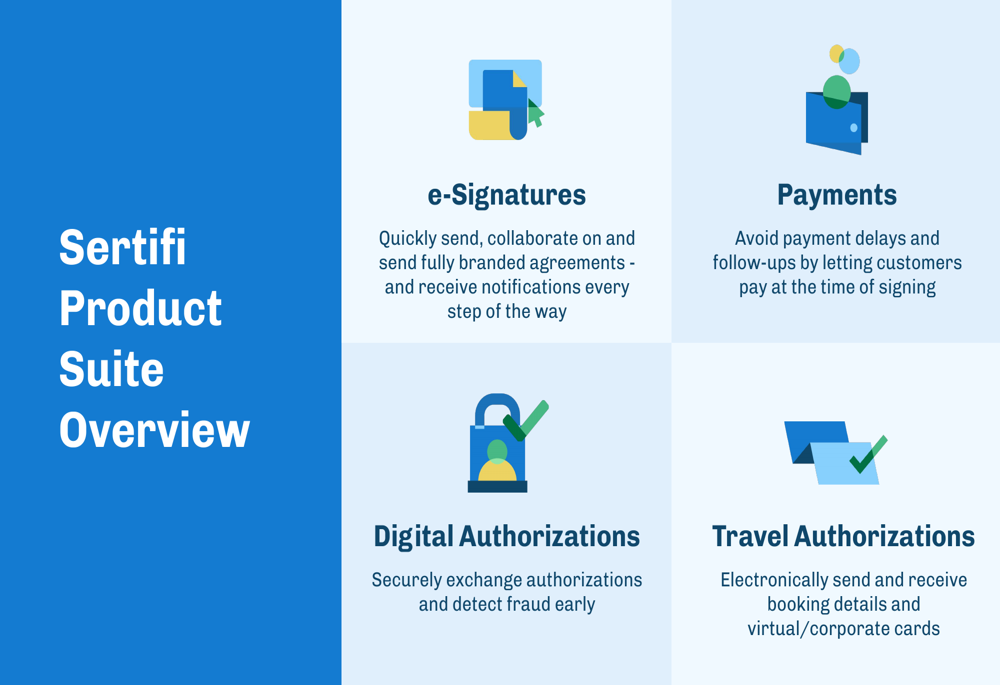

Sertifi Acquisition Integration

Flywire’s recent acquisition of Sertifi is showing early signs of success. Sertifi contributed $12.3 million to Q2 revenue, exceeding the guidance of $11.0 million. The company highlighted several early wins, including signing Caesars (NASDAQ:CZR) Entertainment as a new enterprise logo, achieving 33% more Annual Recurring Revenue (ARR) in EMEA compared to Q1 2025, and more than doubling both properties and volume year-to-date for Sertifi Pay.

The Sertifi product suite complements Flywire’s existing offerings with e-signatures, payments, digital authorizations, and travel authorizations capabilities:

Financial Outlook

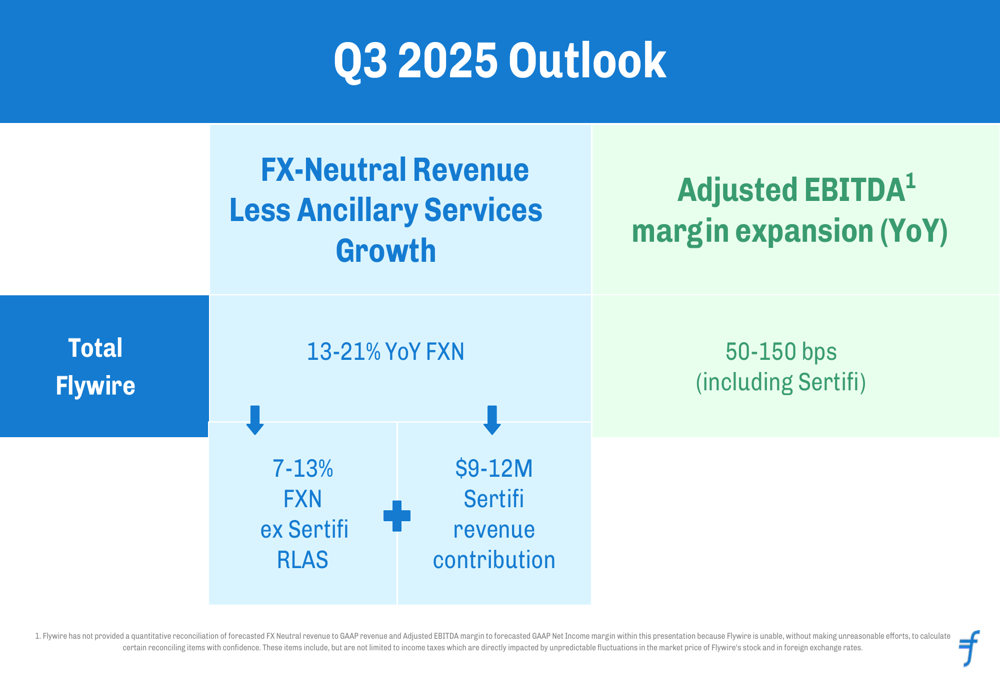

For Q3 2025, Flywire expects FX-neutral RLAS growth of 13-21% year-over-year, including 7-13% growth excluding Sertifi plus a $9-12 million Sertifi revenue contribution. Adjusted EBITDA margin is expected to expand by 50-150 basis points, including Sertifi.

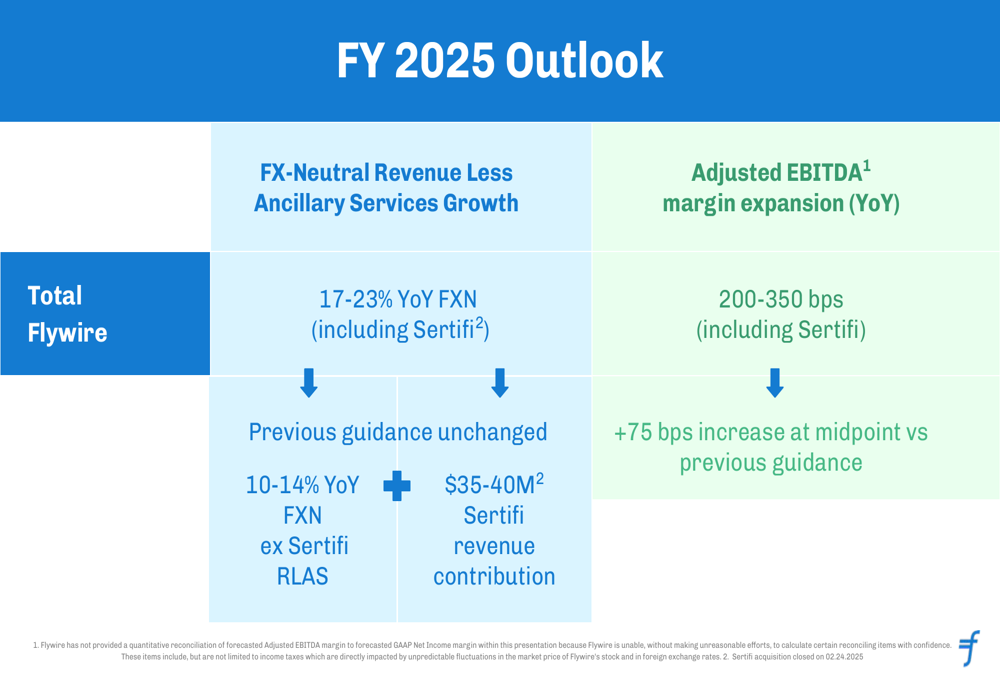

For the full fiscal year 2025, Flywire has maintained its RLAS growth guidance of 17-23% year-over-year on an FX-neutral basis, including Sertifi. Excluding Sertifi, the company expects 10-14% growth plus a $35-40 million Sertifi revenue contribution. The company raised its adjusted EBITDA margin expansion guidance to 200-350 basis points, a 75 basis point increase at the midpoint compared to previous guidance.

Capital Allocation & Balance Sheet

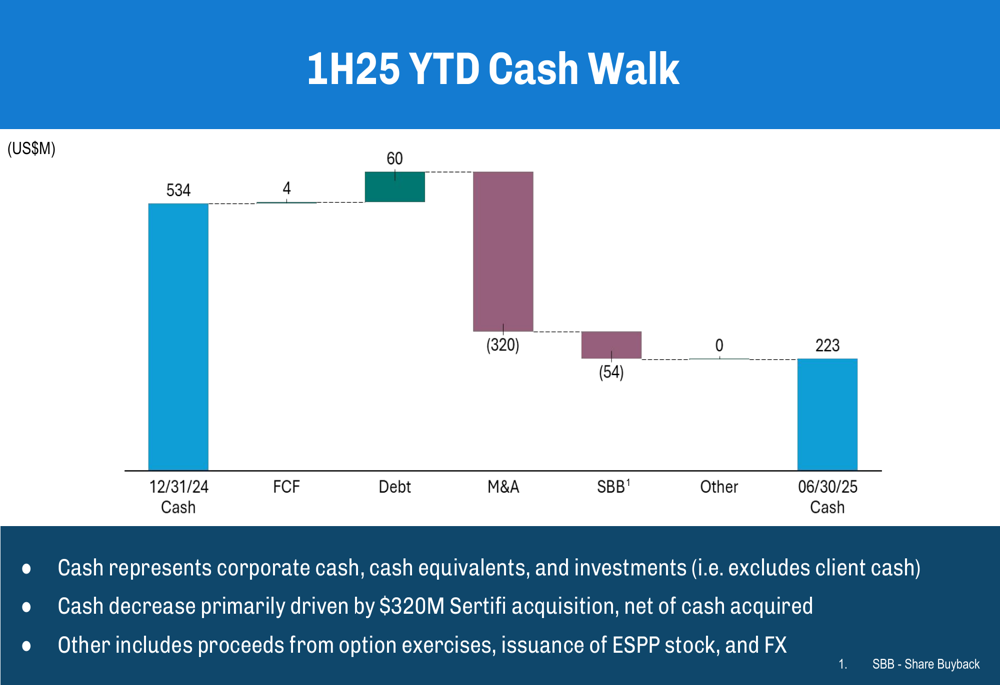

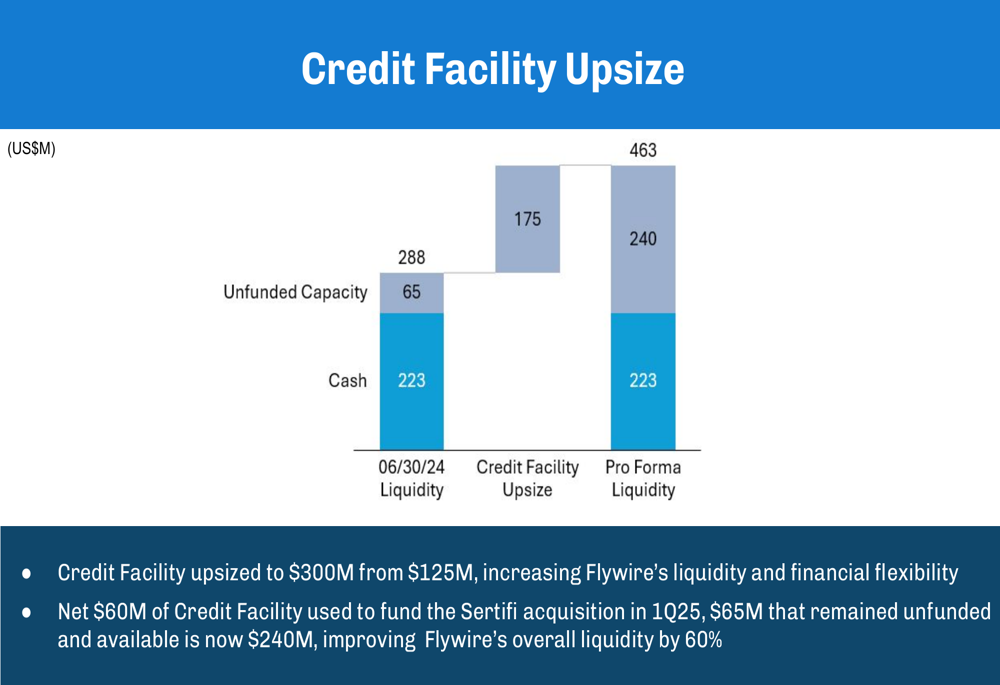

Flywire’s cash position decreased from $534 million at the end of 2024 to $223 million as of June 30, 2025, primarily due to the $320 million Sertifi acquisition. The company also repurchased $54 million worth of shares during the first half of 2025.

To enhance financial flexibility, Flywire upsized its credit facility to $300 million, with $60 million used to fund part of the Sertifi acquisition. The company’s pro forma liquidity now stands at $463 million, consisting of $223 million in cash and $240 million in unfunded capacity.

Flywire has $202 million remaining in its share repurchase authorization after spending approximately $98 million since initiating the program in Q3 2024. The company recently increased the authorization by $150 million, demonstrating confidence in its long-term prospects despite near-term challenges in certain verticals.

This balanced capital allocation approach aligns with Flywire’s three-pronged strategy of investing in organic growth, pursuing strategic acquisitions, and returning capital to shareholders through share buybacks.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.