Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Introduction & Market Context

Forestar Group Inc (NYSE:FOR), a residential lot developer for affordably-priced single-family homes, reported mixed second-quarter fiscal 2025 results that fell short of market expectations despite showing year-over-year growth. The company’s stock declined 4.2% following the earnings release, reflecting investor disappointment with the financial performance.

According to the presentation materials, Forestar achieved a 5% increase in revenue to $351 million, while earnings per share came in at $0.62. However, these figures missed analyst forecasts of $386.14 million in revenue and $0.67 in EPS, as noted in recent earnings coverage.

The company operates in a market characterized by constrained lot supply and challenging financing conditions for land development, which presents both opportunities and challenges for Forestar’s business model.

Quarterly Performance Highlights

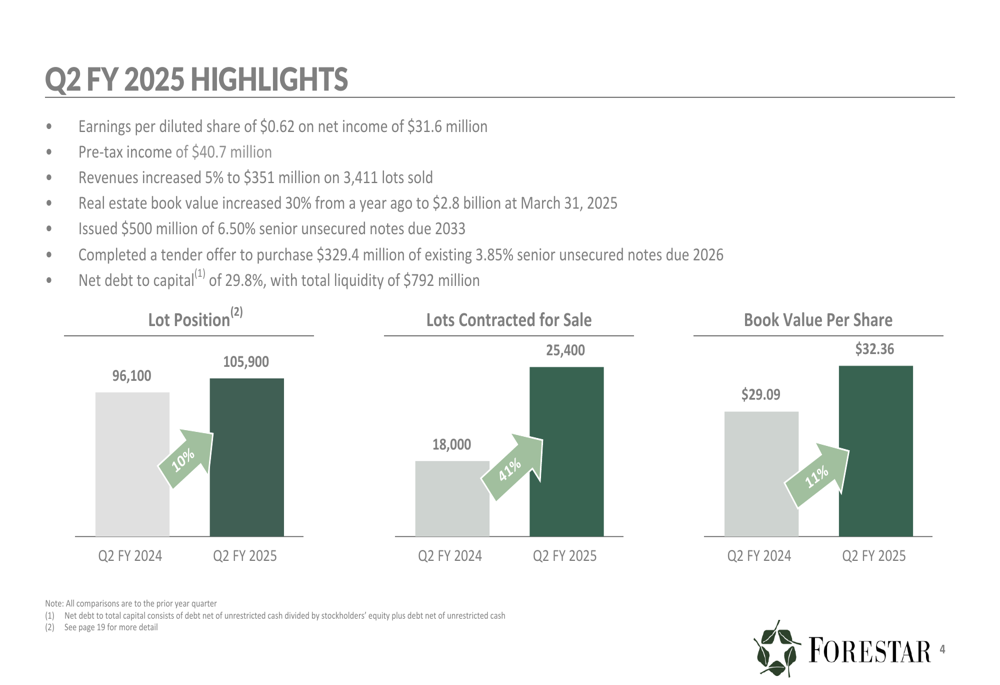

Forestar’s Q2 FY 2025 results showed modest growth across several key metrics. The company sold 3,411 lots during the quarter, generating $351 million in revenue. Net income reached $31.6 million, with pre-tax income of $40.7 million.

As shown in the following financial highlights slide, Forestar’s lot position increased from 96,100 in Q2 FY 2024 to 105,900 in Q2 FY 2025, while lots contracted for sale grew significantly from 18,000 to 25,400 over the same period:

The company’s book value per share also showed solid growth, increasing from $29.09 in Q2 FY 2024 to $32.36 in Q2 FY 2025. However, the presentation doesn’t address the 32% increase in SG&A expenses noted in earnings coverage, which impacted profit margins and contributed to the earnings miss.

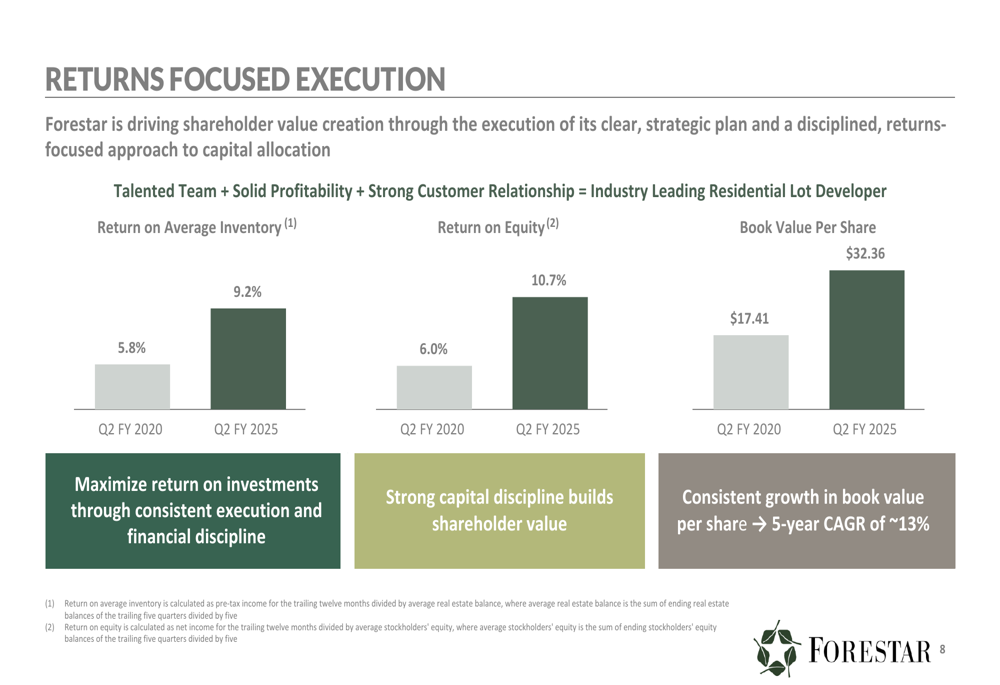

Forestar’s return-focused execution has driven consistent improvements in key financial metrics over the past five years, as illustrated in this performance chart:

Despite these positive long-term trends, the company’s gross profit margin declined to 22.6% in Q2 FY 2025 from 24.9% in the previous year, according to earnings reports, indicating some pressure on profitability in the current market environment.

Strategic Initiatives

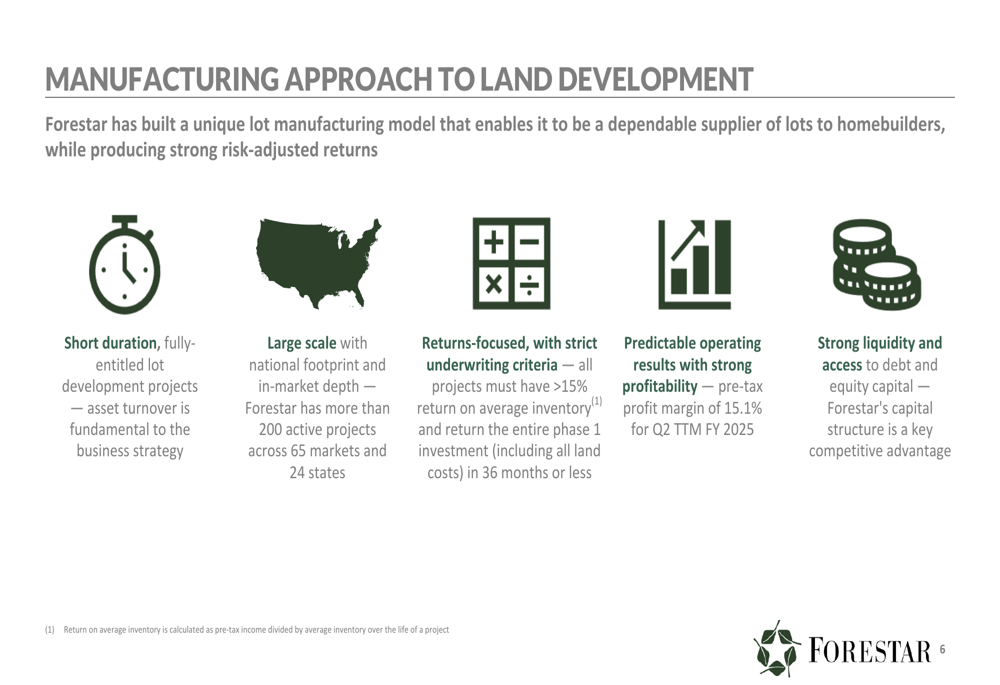

Forestar’s business model centers on a manufacturing approach to land development, focusing on short-duration, fully-entitled projects with strict underwriting criteria. This approach has enabled the company to achieve a 15.1% pre-tax profit margin for the trailing twelve months ended Q2 FY 2025.

The company’s strategy is clearly outlined in the following slide:

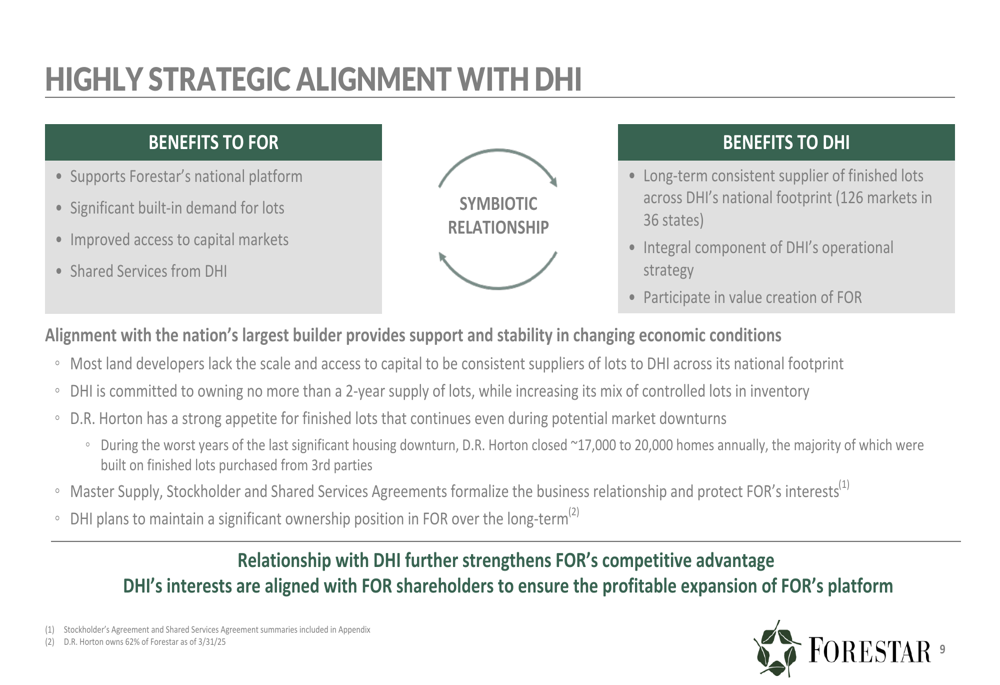

A cornerstone of Forestar’s strategy is its strategic relationship with D.R. Horton (NYSE:DHI), which provides built-in demand for lots and supports the company’s national platform. This relationship is formalized through Master Supply, Stockholder, and Shared Services Agreements.

The following illustration highlights the mutual benefits of this strategic alignment:

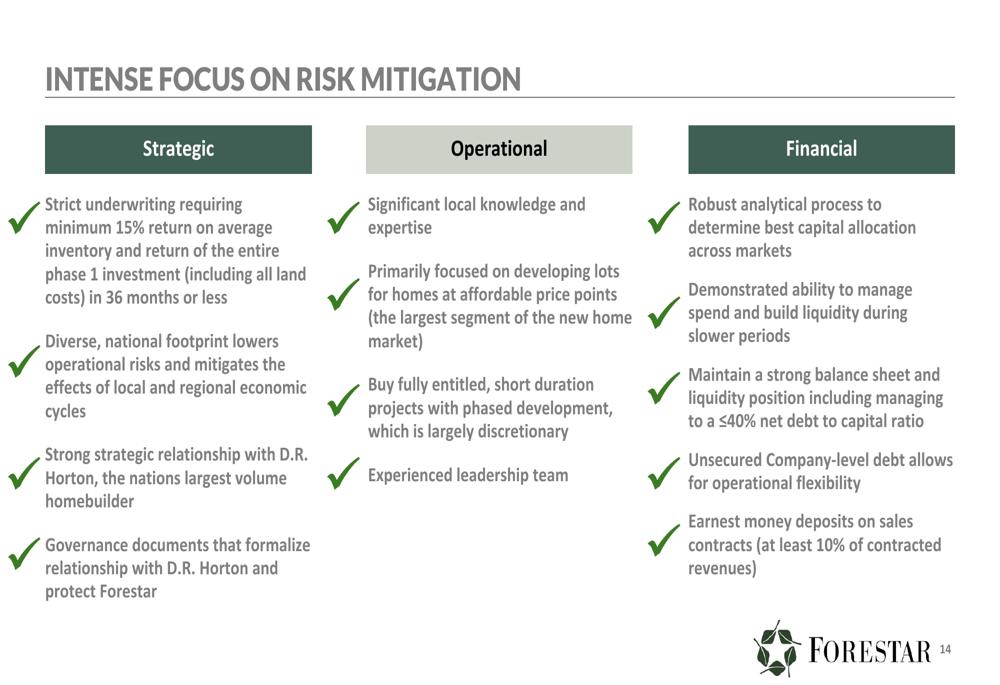

Forestar has also implemented comprehensive risk mitigation strategies across strategic, operational, and financial dimensions. These include maintaining a diversified national footprint, focusing on affordable price points, and employing strict underwriting criteria.

The company’s risk management approach is detailed in this slide:

Forward-Looking Statements

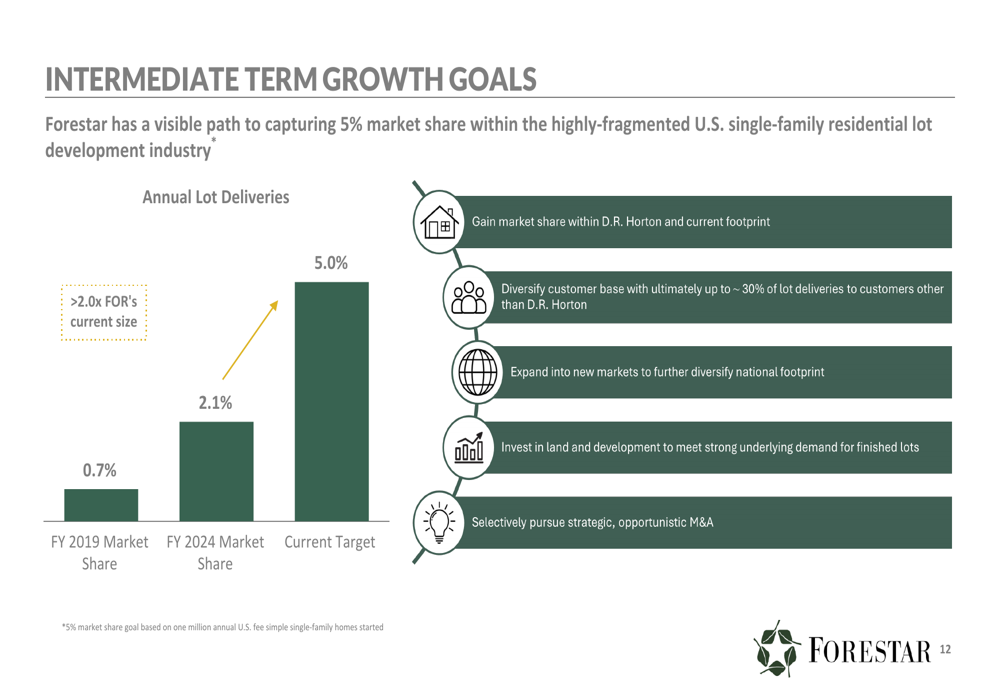

Forestar has set ambitious growth targets, aiming to capture 5% market share within the U.S. single-family residential lot development industry, up from 2.1% in FY 2024. This expansion strategy includes gaining market share within D.R. Horton and current markets, diversifying the customer base, and pursuing strategic M&A opportunities.

The company’s growth goals are illustrated in the following slide:

To support these growth initiatives, Forestar expects to invest approximately $1.9 billion in land acquisition and development in fiscal 2025. However, during the earnings call, management indicated they would moderate land acquisition investments while focusing on affordable lot development, suggesting some adjustment to near-term capital allocation in response to current market conditions.

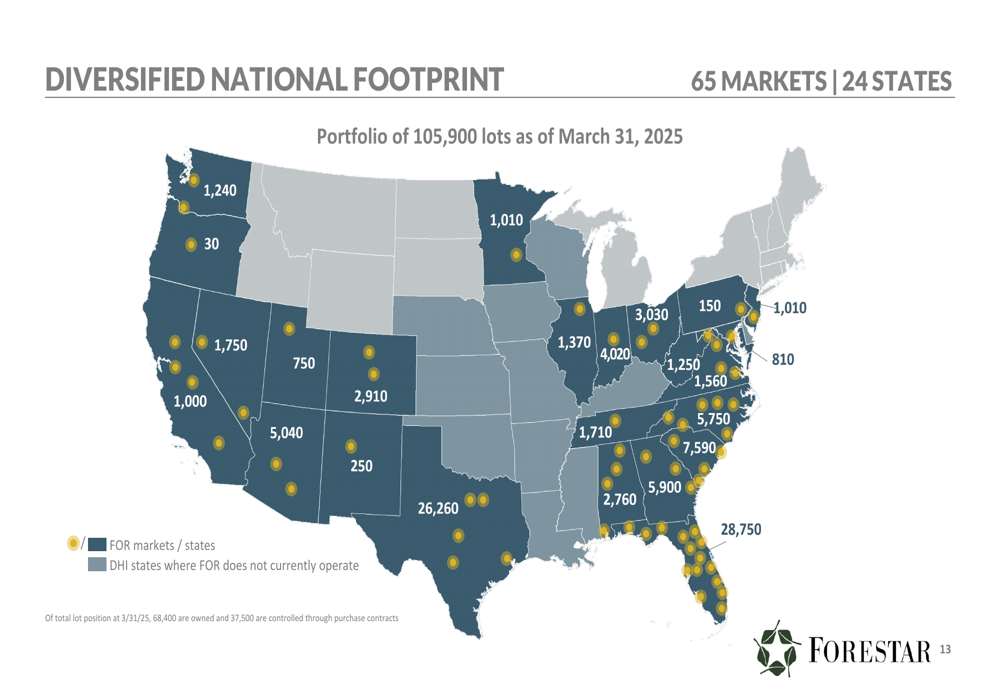

Forestar’s geographic diversification strategy is evident in its operations across 65 markets in 24 states, as shown in this national footprint map:

Detailed Financial Analysis

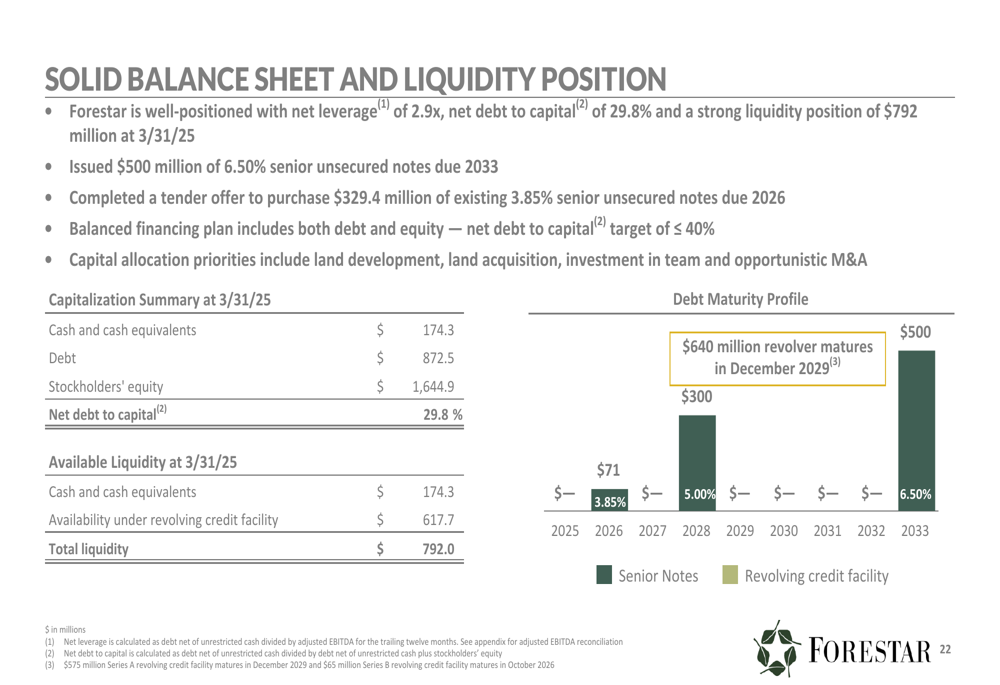

Forestar maintains a strong balance sheet with net debt to capital of 29.8% and total liquidity of $792 million as of March 31, 2025. During the quarter, the company issued $500 million of 6.50% senior unsecured notes due 2033 and completed a tender offer to purchase $329.4 million of existing 3.85% senior unsecured notes due 2026.

The company’s financial position is summarized in this slide:

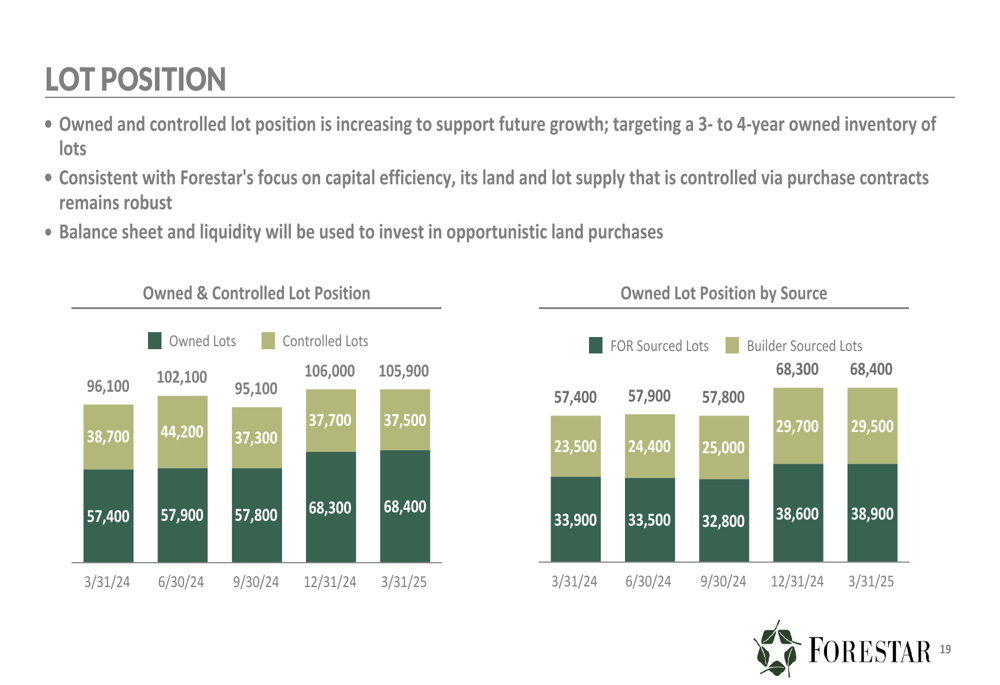

Forestar’s lot inventory continues to grow, with 68,400 owned lots and 37,500 controlled lots through purchase contracts as of March 31, 2025. This represents a strategic investment to support future growth, with the company targeting a 3- to 4-year owned inventory of lots.

The lot position trends are illustrated in the following chart:

The company’s contracted backlog provides visibility into future revenue streams. Owned lots under contract to sell increased 41% year-over-year to 25,400 lots, representing 37% of Forestar’s owned lot position. These contracts are secured by $212 million in hard earnest money deposits and are expected to generate approximately $2.3 billion in future revenue.

Despite these positive indicators, Forestar faces challenges in the current market environment. The stock has declined 44% over the past year and is trading close to its 52-week low, according to recent market data. This suggests investors remain cautious about the company’s ability to navigate current market headwinds while pursuing its ambitious growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.