Trump administration authorizes CIA for covert action in Venezuela - Bloomberg

Introduction & Market Context

Forestar Group Inc (NYSE:FOR), a residential lot developer focused on the affordably-priced single-family home market, recently presented its Q2 2025 investor slides highlighting the company’s performance and strategic direction. Despite reporting revenue growth, the company missed analyst expectations, leading to mixed market reactions.

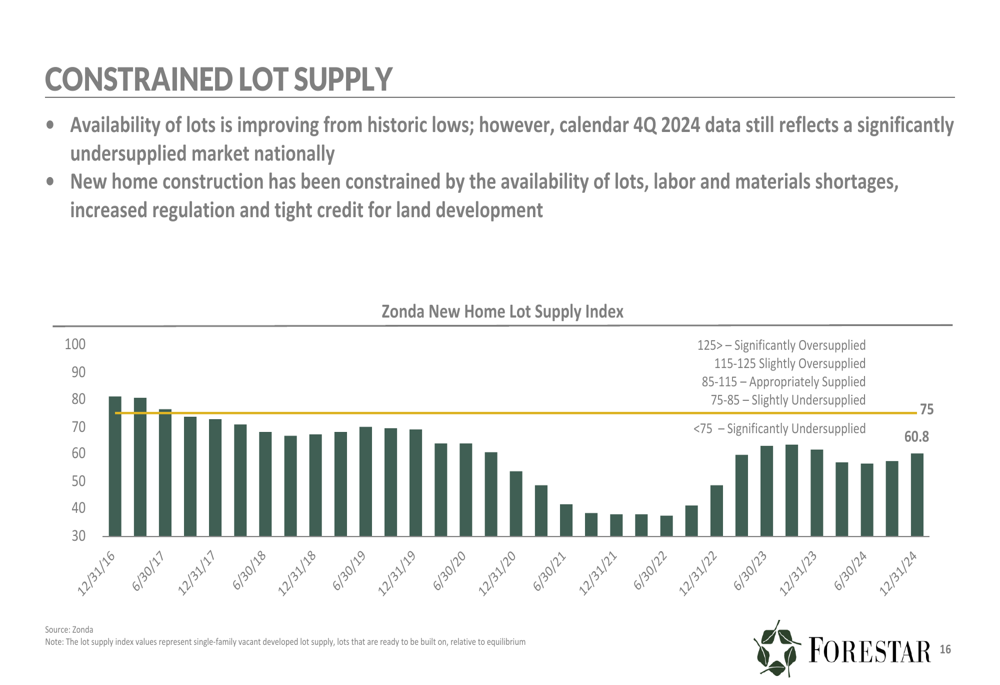

The company operates in a market characterized by constrained lot supply, with the Zonda New Home Lot Supply Index at 60.8 as of December 2024, significantly below the 75 level that would indicate adequate supply. This environment creates both challenges and opportunities for Forestar as homebuilders increasingly shift toward "land lighter" models.

As shown in the following chart illustrating the constrained lot supply situation:

Quarterly Performance Highlights

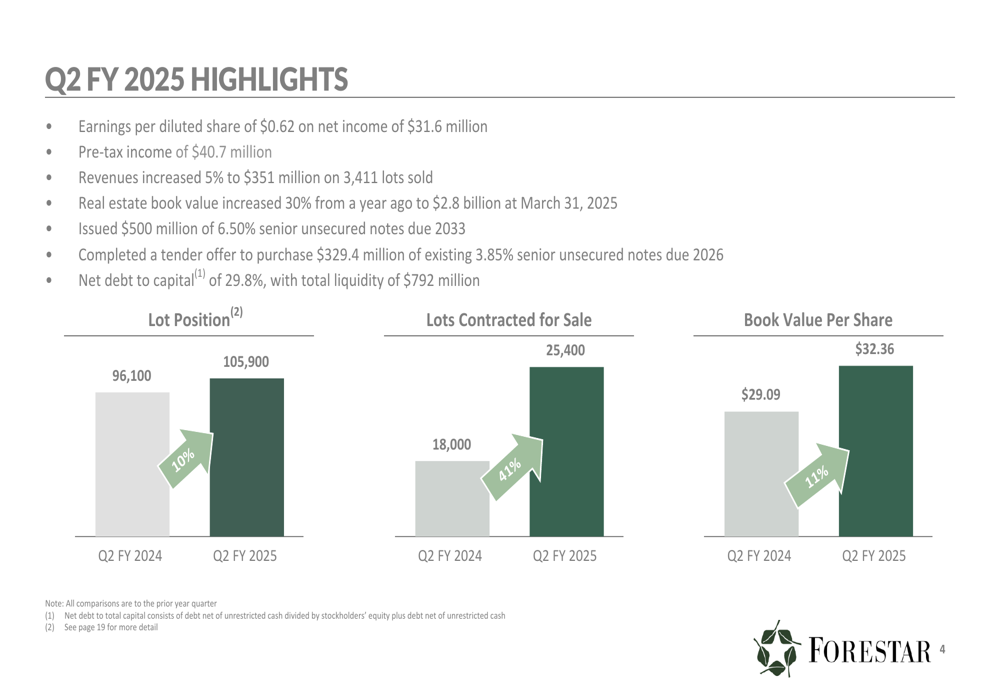

Forestar reported Q2 FY 2025 earnings per diluted share of $0.62 on net income of $31.6 million, falling short of analyst expectations of $0.67. Revenue increased 5% year-over-year to $351 million on 3,411 lots sold, but missed the forecasted $386.14 million. This underperformance contributed to a 4.2% drop in Forestar’s stock following the earnings release, though premarket trading on July 22, 2025, showed signs of recovery with a 5.53% increase to $23.30.

The company’s real estate book value increased 30% year-over-year to $2.8 billion, while book value per share grew 11% to $32.36. However, the presentation did not highlight the decline in gross profit margin from 24.9% to 22.6% year-over-year or the 32% increase in SG&A expenses that impacted profitability.

The following slide summarizes Forestar’s Q2 FY 2025 key performance metrics:

Strategic Positioning

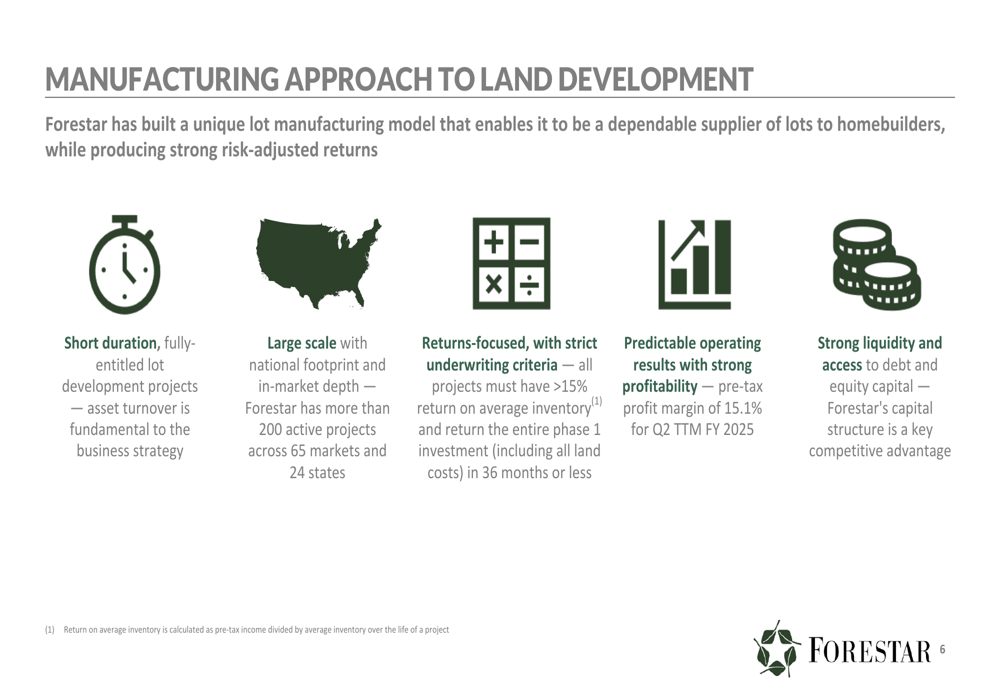

Forestar’s business model centers on a manufacturing approach to land development, emphasizing short-duration, fully-entitled lot development projects with strict underwriting criteria. The company requires projects to deliver at least 15% return on average inventory and return the entire phase 1 investment within 36 months.

This approach has yielded strong financial metrics compared to industry peers, with Forestar reporting a pre-tax profit margin of 15.1%, return on equity of 10.7%, and asset turnover of 1.03 for Q2 TTM FY 2025.

The company’s manufacturing approach to land development is illustrated in this slide:

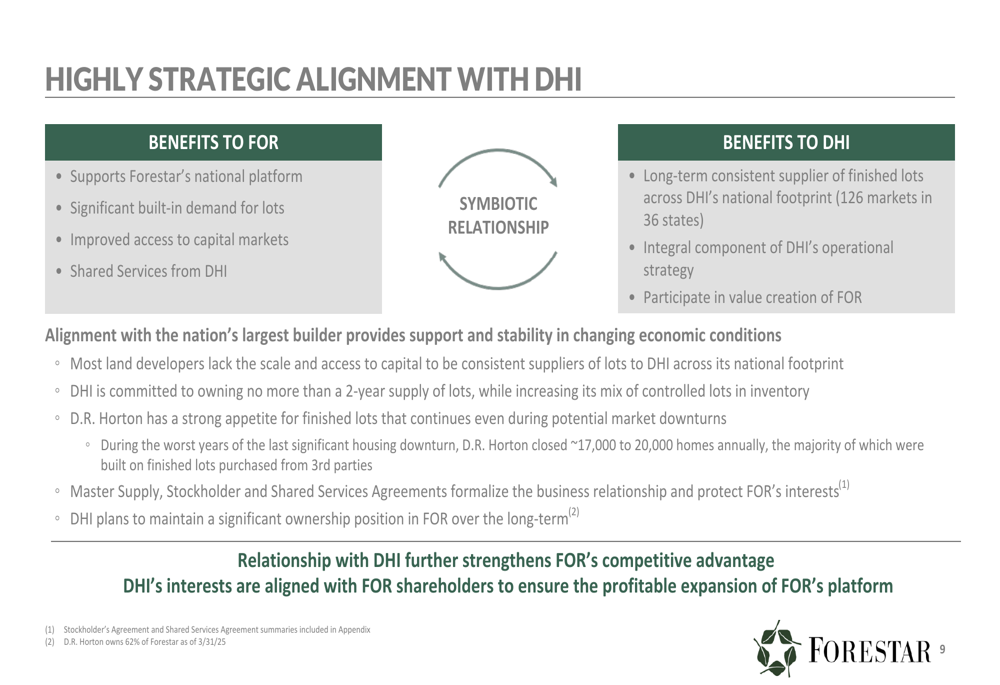

A critical component of Forestar’s strategy is its relationship with D.R. Horton (NYSE:DHI), the nation’s largest homebuilder. This strategic alignment provides Forestar with significant built-in demand for lots, improved access to capital markets, and shared services, while giving D.R. Horton a consistent supplier of finished lots across its national footprint.

The following diagram illustrates the strategic relationship between Forestar and D.R. Horton:

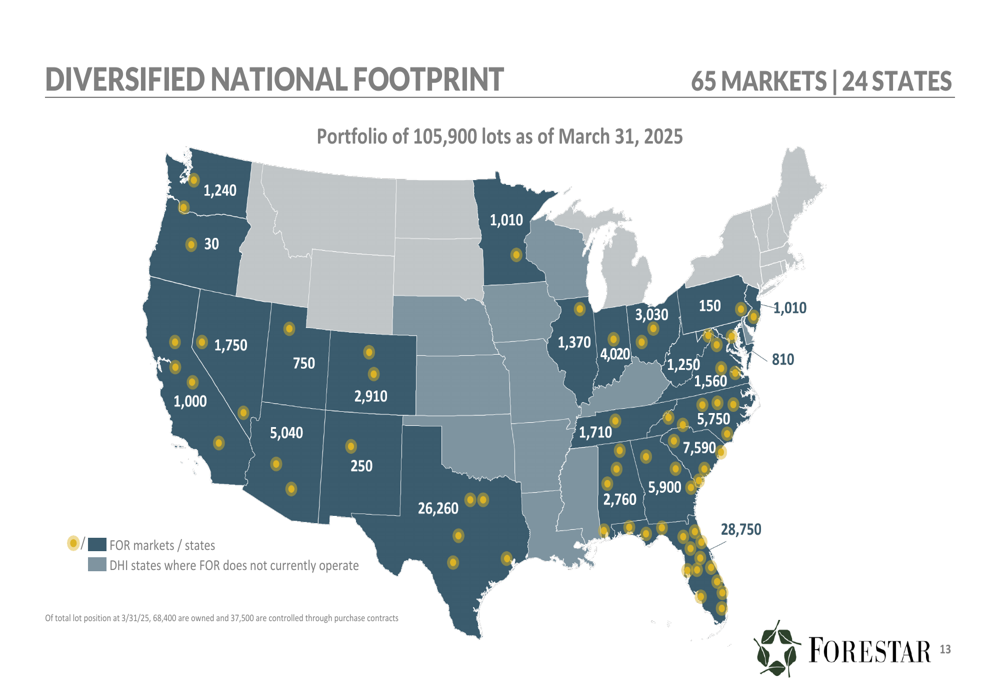

Geographic Diversification & Risk Management

Forestar operates across 65 markets in 24 states, with a portfolio comprising 105,900 lots (68,400 owned and 37,500 controlled through purchase contracts). This geographic diversification helps mitigate local and regional economic cycles, though the earnings call Q&A revealed some regional market softness, particularly in Florida.

The company’s national footprint is visualized in this map:

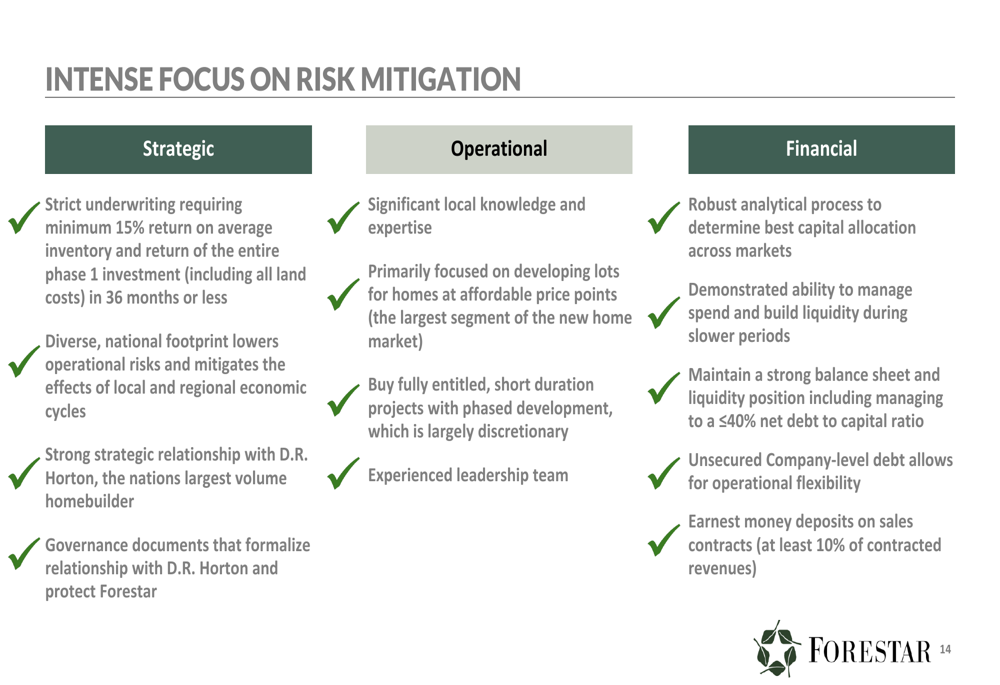

Risk mitigation is a core focus for Forestar, with strategies categorized as strategic, operational, and financial. These include strict underwriting criteria, phased development, maintaining a strong balance sheet with a target net debt to capital ratio of ≤40%, and securing earnest money deposits on sales contracts (at least 10% of contracted revenues).

The company’s comprehensive approach to risk management is outlined here:

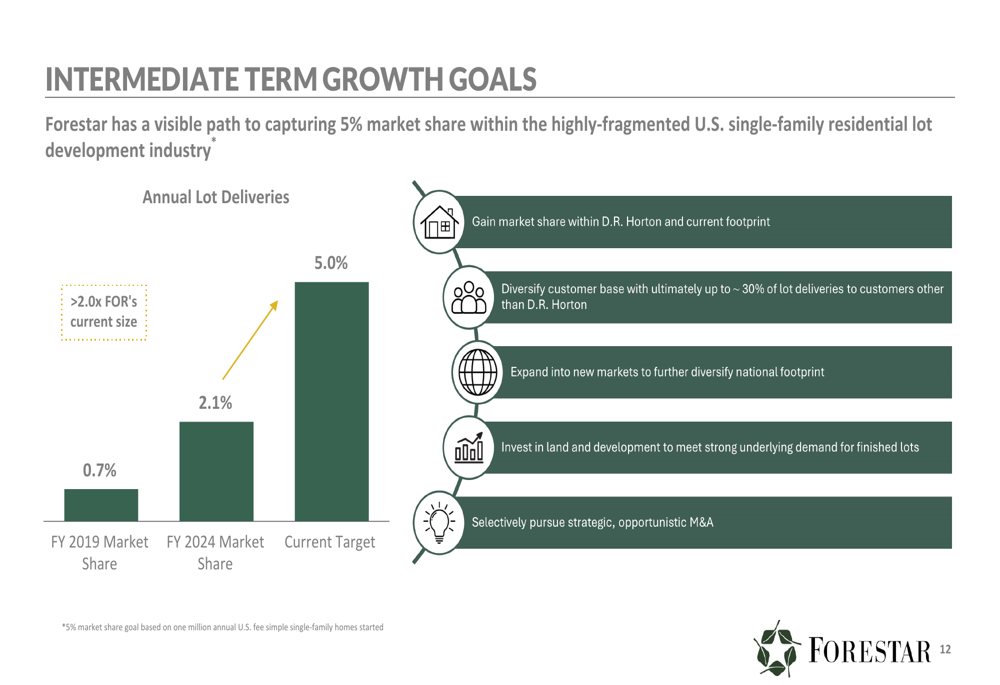

Growth Strategy & Outlook

Forestar has set ambitious intermediate-term growth goals, aiming to capture 5% market share within the U.S. single-family residential lot development industry, up from 2.1% in FY 2024. Key strategies include gaining market share within D.R. Horton and current footprint, diversifying the customer base, expanding into new markets, and pursuing strategic M&A opportunities.

The following slide illustrates Forestar’s market share growth targets:

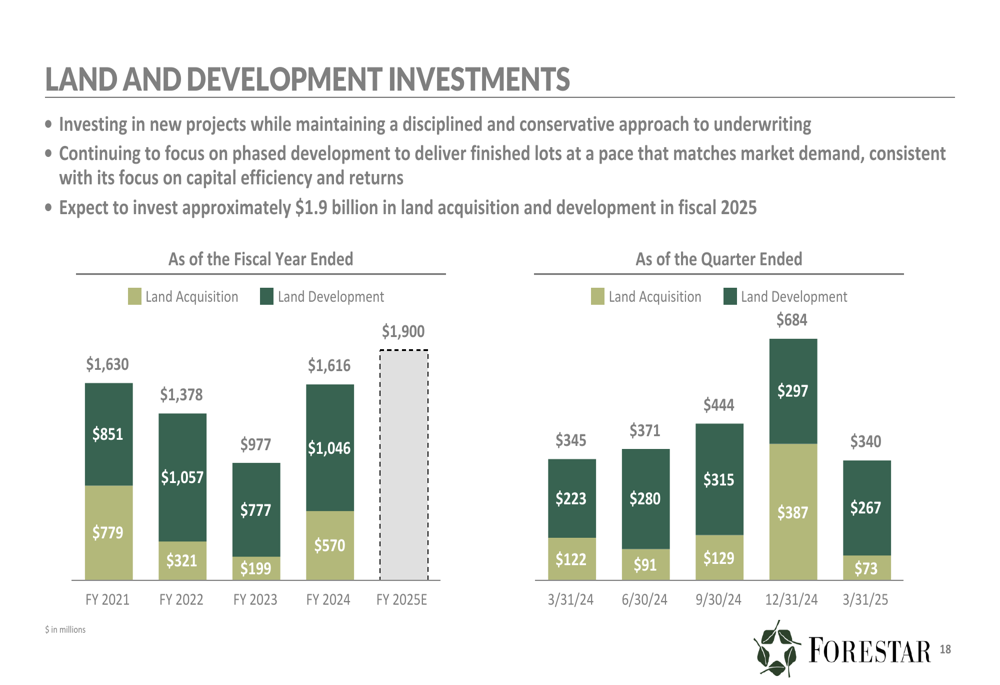

To support this growth, Forestar plans to invest approximately $1.9 billion in land acquisition and development in fiscal 2025. The company’s owned lots under contract increased 41% year-over-year to 25,400 lots, representing 37% of Forestar’s owned lot position. These contracts are secured by $212 million in hard earnest money deposits and are expected to generate approximately $2.3 billion in future revenue.

The company’s land and development investment plans are shown here:

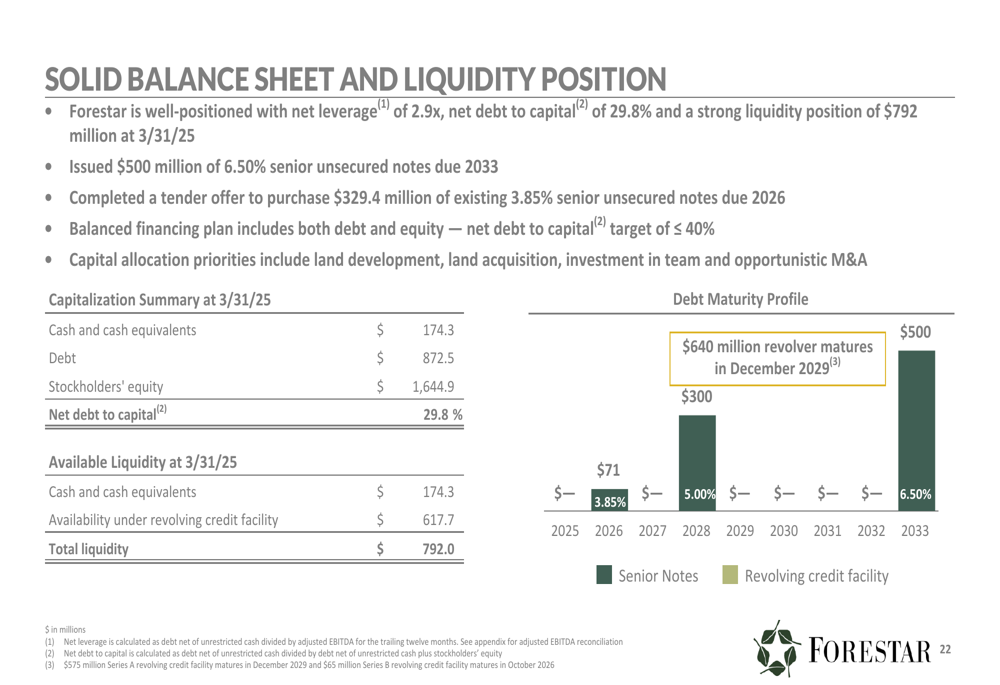

Financial Position

Forestar maintains a solid balance sheet with net debt to capital of 29.8% and a strong liquidity position of $792 million as of March 31, 2025. During Q2, the company issued $500 million of 6.50% senior unsecured notes due 2033 and completed a tender offer to purchase $329.4 million of existing 3.85% senior unsecured notes due 2026.

The company’s debt maturity profile and financial position are illustrated in this slide:

Despite the quarterly earnings miss, Forestar’s long-term financial trends remain positive, with book value per share showing a 5-year CAGR of approximately 13%. Return on average inventory improved from 5.8% in Q2 FY 2020 to 9.2% in Q2 FY 2025, while return on equity increased from 6.0% to 10.7% over the same period.

Conclusion

While Forestar’s Q2 2025 results fell short of analyst expectations, the company continues to demonstrate revenue growth and strategic positioning in a market with constrained lot supply. The strategic relationship with D.R. Horton, geographic diversification, and focus on risk management provide a foundation for pursuing ambitious market share growth.

However, investors should monitor rising SG&A expenses, regional market softness, and the impact of affordability issues on demand for new homes. With a current P/E ratio of 5.11 according to the earnings report, Forestar may represent an attractive valuation for investors who believe in the company’s long-term growth strategy despite recent challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.