Can anything shut down the Gold rally?

Introduction & Market Context

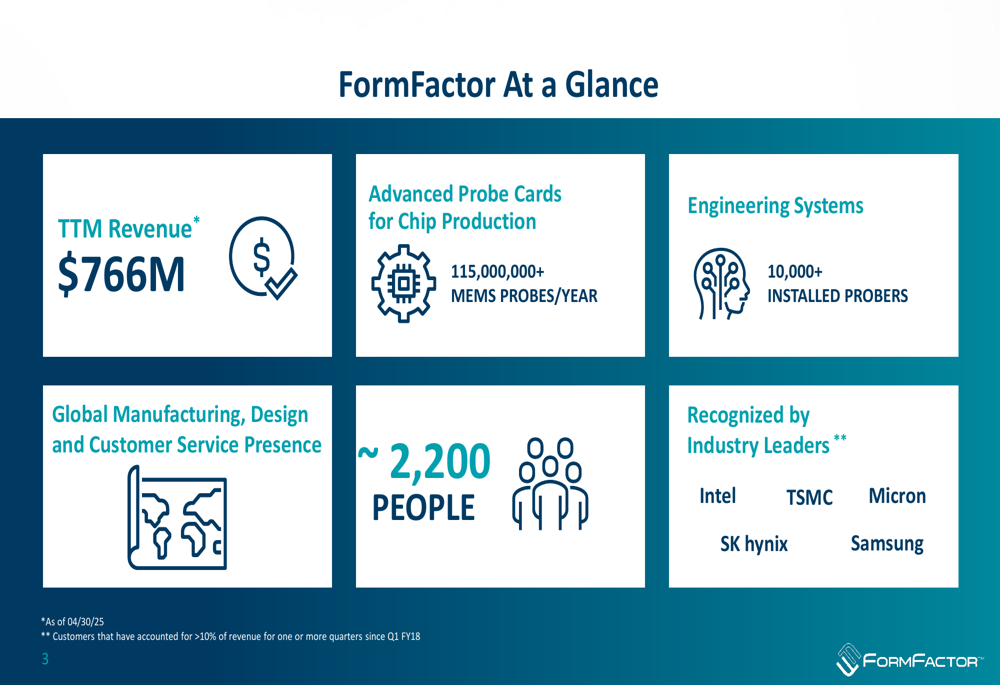

FormFactor , Inc. (NASDAQ:FORM), a leading provider of semiconductor test and measurement solutions, presented its investor outlook on April 30, 2025, highlighting the company’s strategic position in the growing semiconductor test market. The presentation comes as the company reported Q1 2025 revenue of $171.4 million and provided an outlook for Q2 2025, projecting revenue of $190 million (±$5 million).

The company operates in a unique position within the semiconductor industry value chain, focusing on wafer test and measurement with its advanced probe cards and engineering systems. FormFactor benefits from two key industry dynamics: the secular growth in semiconductor usage, particularly accelerated by AI applications, and the slowing of Moore’s Law, which has increased demand for advanced packaging solutions.

As shown in the following snapshot of FormFactor’s key metrics:

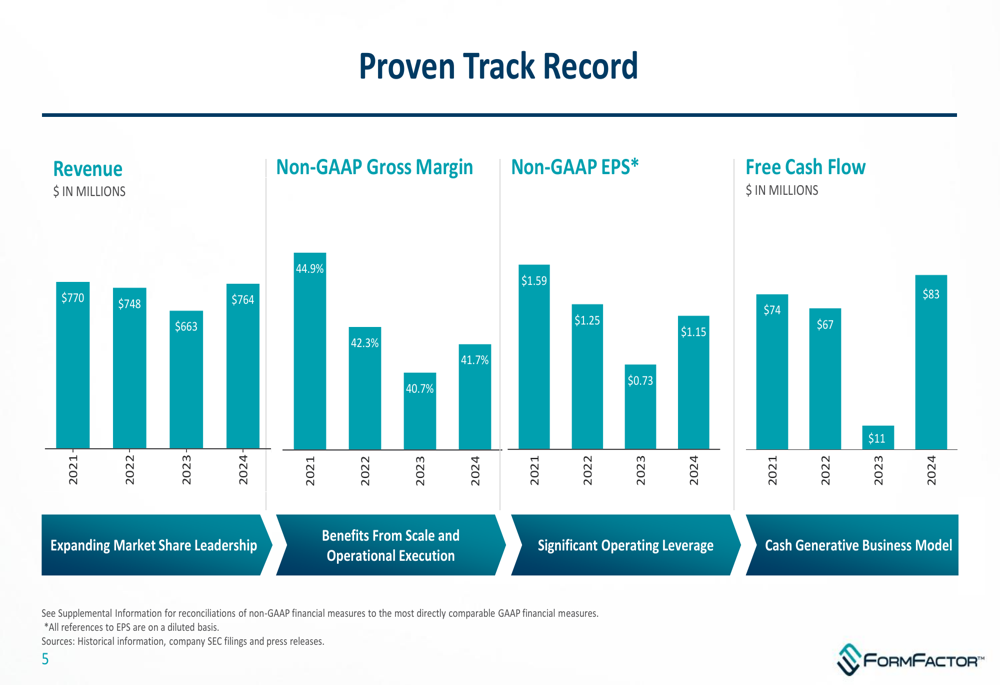

Financial Performance Highlights

FormFactor’s financial performance has shown resilience despite industry cyclicality. The company generated $764 million in revenue for 2024, recovering from a dip in 2023 when revenue fell to $663 million. This represents a significant improvement from the previous year and approaches the company’s 2021 peak of $770 million.

The following chart illustrates FormFactor’s financial performance over the past four years:

Non-GAAP gross margin has remained relatively stable, ranging from 40.7% to 44.9% over the four-year period, while non-GAAP EPS recovered to $1.15 in 2024 after dropping to $0.73 in 2023. Free cash flow showed particularly strong improvement, reaching $83 million in 2024 compared to just $11 million in 2023.

Recent quarterly results show some fluctuation, with Q1 2025 revenue of $171.4 million representing a decline from Q4 2024’s $189.5 million. However, the company projects a return to growth in Q2 2025:

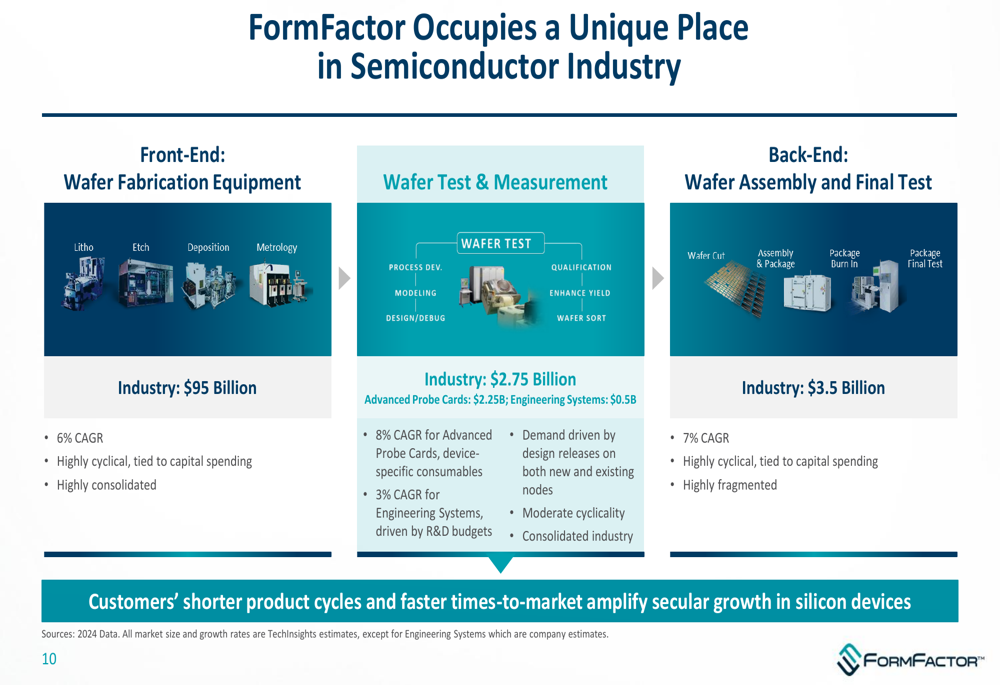

Strategic Industry Position

FormFactor occupies a strategic position in the semiconductor industry, operating in the wafer test and measurement segment that sits between front-end wafer fabrication and back-end assembly and testing. This $2.75 billion market segment is experiencing moderate cyclicality compared to the highly cyclical front-end and back-end segments.

The following diagram illustrates FormFactor’s unique position in the semiconductor value chain:

The company’s advanced probe cards segment, which represents approximately 82% of its revenue, serves a $2.25 billion market growing at an 8% CAGR. The engineering systems segment addresses a $0.5 billion market growing at a 3% CAGR. FormFactor aims to outpace market growth in both segments.

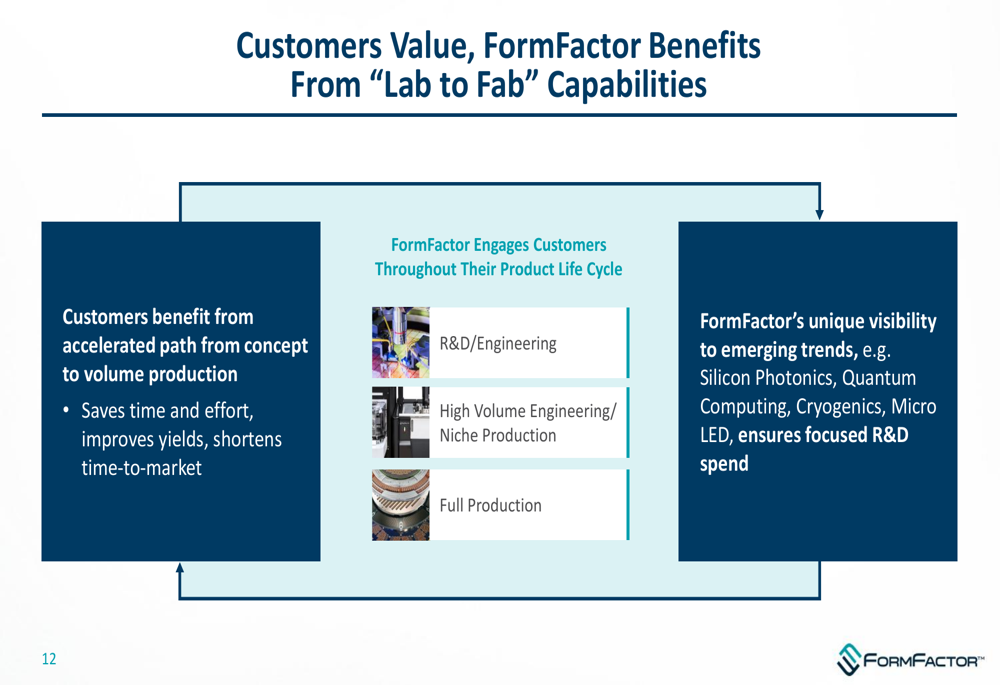

FormFactor’s competitive advantage stems from its early customer engagement and technology leadership, creating high barriers to entry. The company’s "Lab to Fab" capabilities enable it to support customers throughout their product lifecycle, from R&D through high-volume production:

Growth Strategy and Target (NYSE:TGT) Model

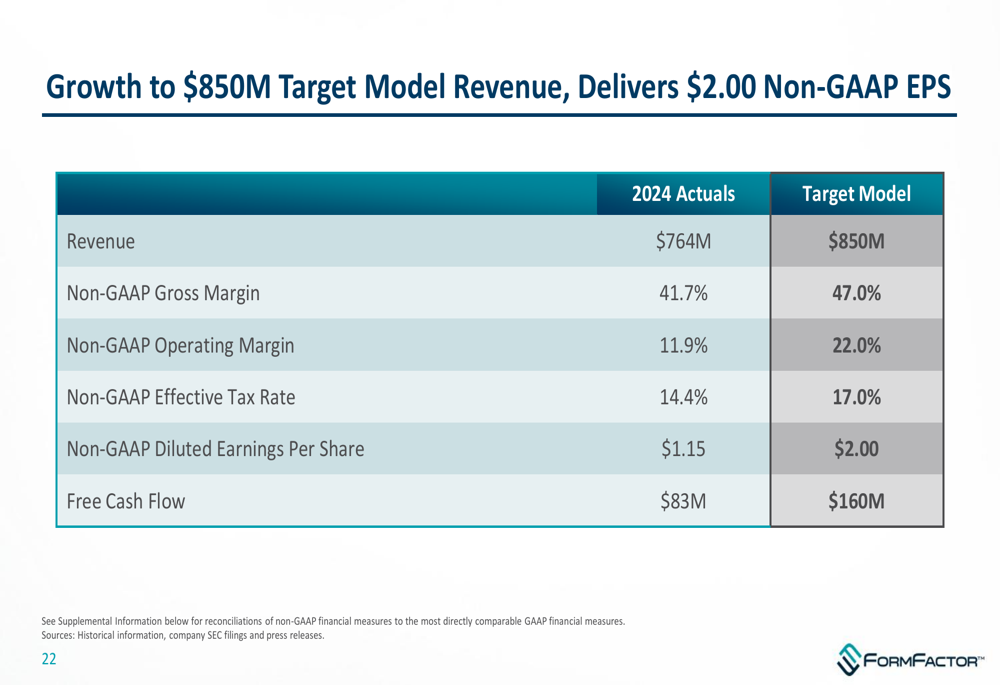

FormFactor has outlined a clear path to reach its target model of $850 million in revenue, which would deliver $2.00 in non-GAAP EPS. This represents significant improvement from 2024 actuals of $764 million in revenue and $1.15 in non-GAAP EPS.

The following table details the company’s financial targets compared to 2024 performance:

Key drivers for reaching these targets include expanding gross margins from 41.7% to 47.0% and increasing operating margins from 11.9% to 22.0%. The company also expects to generate $160 million in free cash flow at the target model, nearly double the $83 million achieved in 2024.

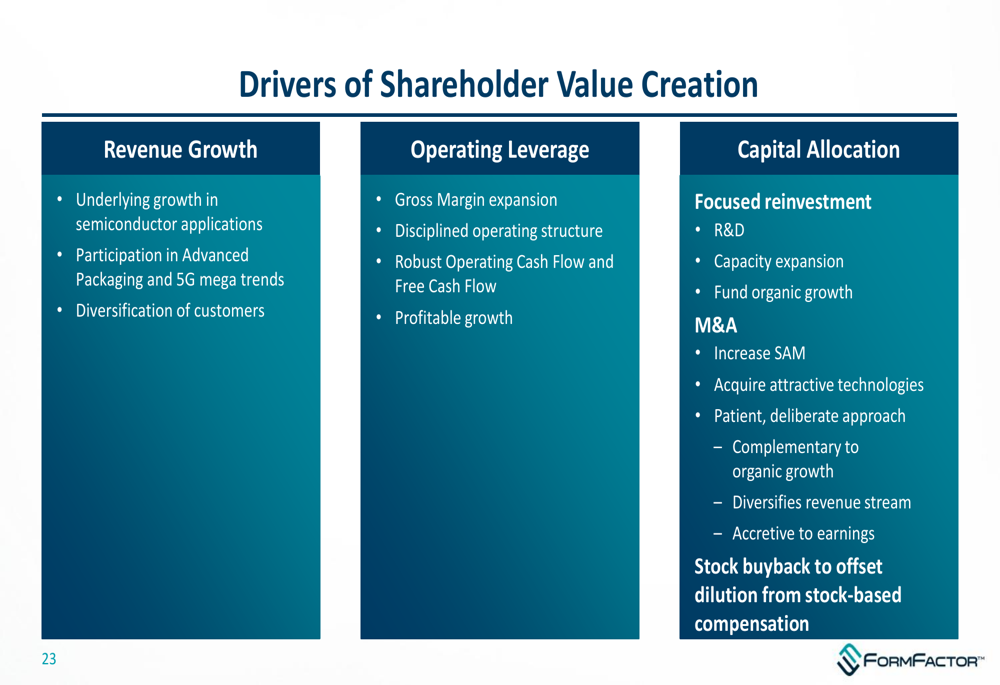

FormFactor’s growth strategy focuses on several key drivers of shareholder value:

The company’s capital allocation strategy balances investments in R&D and capacity expansion with strategic acquisitions and stock buybacks to offset dilution. FormFactor has a proven track record of successful acquisitions, including Microprobe (2012), Cascade Microtech (2016), and several smaller acquisitions in recent years.

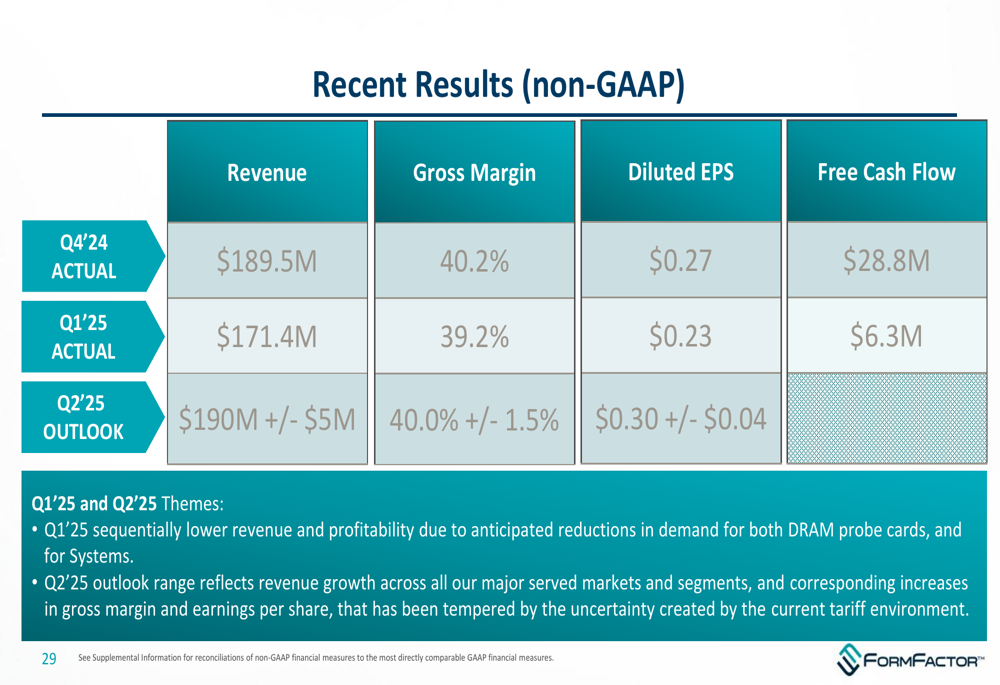

Recent Results and Outlook

FormFactor’s Q1 2025 results showed some sequential decline from Q4 2024, with revenue dropping from $189.5 million to $171.4 million and non-GAAP gross margin decreasing slightly from 40.2% to 39.2%. The company attributed this decline to "anticipated reductions in demand for both DRAM probe cards, and for Systems."

For Q2 2025, FormFactor projects revenue growth to $190 million (±$5 million) with improved gross margin of 40.0% (±1.5%) and EPS of $0.30 (±$0.04). The company noted that its Q2 outlook "reflects revenue growth across all our major served markets and segments," but has been "tempered by the uncertainty created by the current tariff environment."

This outlook aligns with the company’s previous earnings call, where it reported record Q3 2024 revenue of $207.9 million but anticipated some reduction in Foundry and Logic probe-card demand due to weak mobile and client PC markets. The company’s focus on diversification and preparation for future growth opportunities in areas like co-packaged optics positions it to navigate these market fluctuations.

FormFactor continues to receive industry recognition for its technology leadership and customer service, having been named one of "THE BEST (NYSE:BEST) Suppliers" in the semiconductor industry for ten consecutive years (2014-2023). The company also recently received Intel (NASDAQ:INTC)’s 2024 EPIC Distinguished Supplier Award, highlighting its strategic importance to key customers.

As the semiconductor industry continues to evolve with increased AI adoption and advanced packaging requirements, FormFactor’s position as a critical enabler of semiconductor testing and measurement provides a foundation for long-term growth despite near-term market fluctuations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.