IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

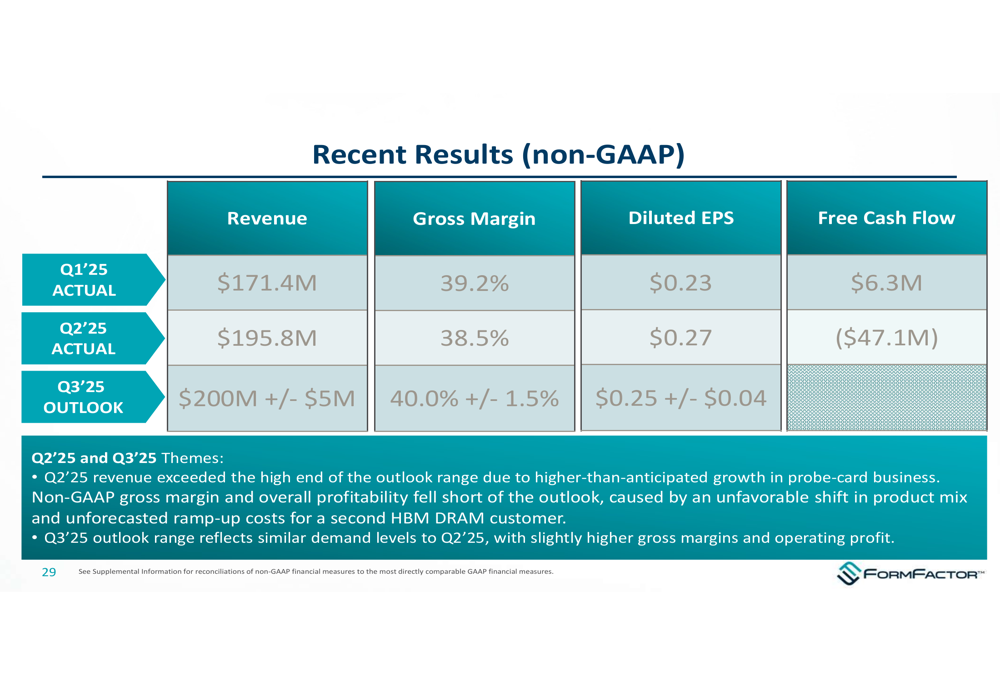

FormFactor , Inc. (NASDAQ:FORM) released its Q2 2025 investor presentation on July 30, showcasing better-than-expected quarterly performance and an optimistic outlook for the remainder of the year. The semiconductor test and measurement leader reported Q2 revenue of $195.8 million, exceeding the high end of its guidance range, with sequential growth expected to continue into Q3.

The presentation comes as FormFactor’s stock closed at $34.70, down 0.81% in regular trading but showing strength with a 3.17% gain in after-hours trading. Despite a 26.51% decline over the past six months, the company’s latest results and forward-looking statements suggest potential for recovery as it capitalizes on semiconductor industry trends.

Q2 2025 Performance Highlights

FormFactor reported Q2 2025 revenue of $195.8 million, representing a significant improvement from Q1’s $171.4 million. The company achieved a non-GAAP gross margin of 38.5% and diluted earnings per share of $0.27, though free cash flow was negative at ($47.1M) for the quarter.

As shown in the company’s recent results slide, FormFactor exceeded the high end of its outlook range due to stronger-than-anticipated growth in its probe-card business:

The Q2 performance marks a continuation of recovery from Q1 2025, when the company reported an EPS of $0.23 that missed analyst forecasts of $0.33. Despite this earlier miss, revenue has shown consistent sequential growth, reflecting increasing demand for the company’s advanced testing solutions.

Strategic Growth Initiatives

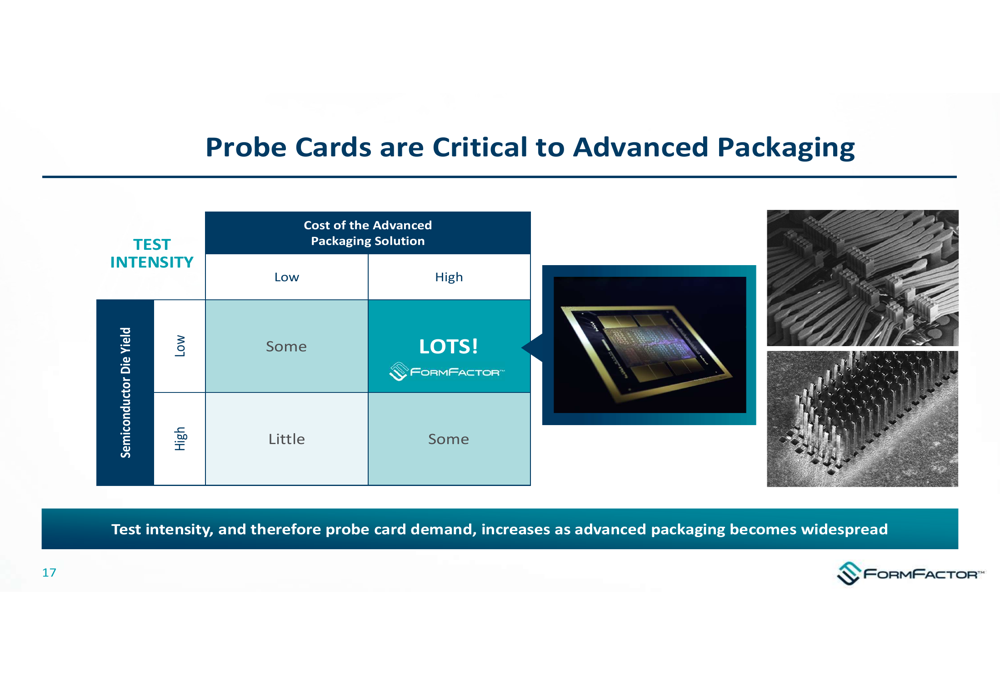

FormFactor’s presentation emphasized its strategic positioning in high-growth semiconductor segments, particularly highlighting the critical role of probe cards in advanced packaging applications. The company noted that as advanced packaging becomes more prevalent due to the slowing of Moore’s Law, the need for sophisticated testing solutions increases dramatically.

As illustrated in the following slide, probe cards are essential for ensuring yield in advanced packaging applications, with the value proposition becoming even more compelling when semiconductor die yields are low:

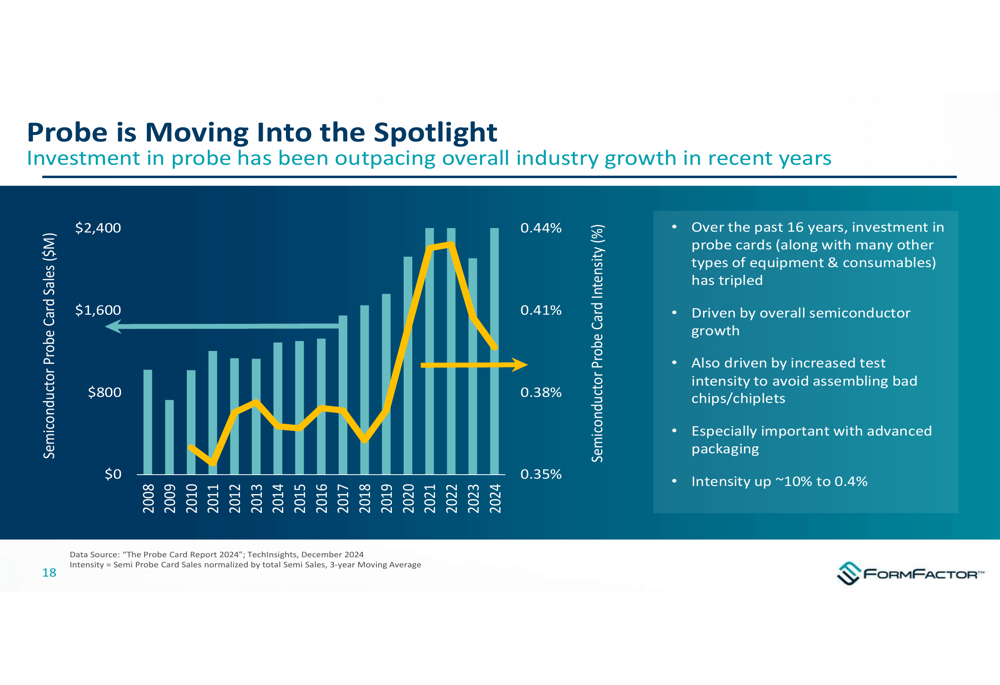

The company also highlighted how investment in probe technology has been outpacing overall semiconductor industry growth, tripling over the past 16 years:

FormFactor’s strategic focus on artificial intelligence applications appears well-timed, as the presentation emphasized how AI is accelerating the exponential growth in silicon devices. The company’s testing solutions are particularly relevant for high bandwidth memory (HBM) applications, which CEO Mike Slescher highlighted as a significant driver of test and probe card spending during the recent earnings call.

Competitive Industry Position

FormFactor emphasized its industry leadership position through multiple customer recognitions, including awards from Intel (NASDAQ:INTC) and SK Hynix. The company’s approach to maintaining market leadership is built around early customer engagement, technology leadership, and the largest R&D budget in its segment.

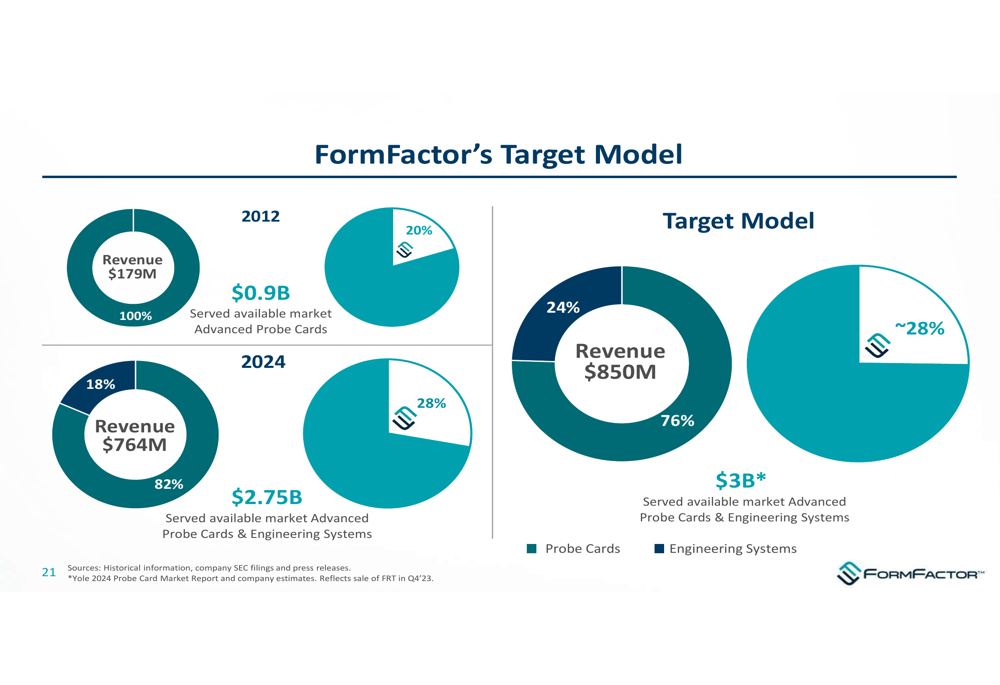

The presentation highlighted FormFactor’s unique positioning in the semiconductor manufacturing process, focusing on wafer test and measurement within a $2.75 billion addressable market growing at 8% CAGR for advanced probe cards and 3% CAGR for engineering systems.

FormFactor’s compelling investment thesis is summarized in the following slide, emphasizing its market leadership, exposure to powerful secular trends, technology leadership, profitable financial model, and active acquisition strategy:

Long-Term Financial Targets

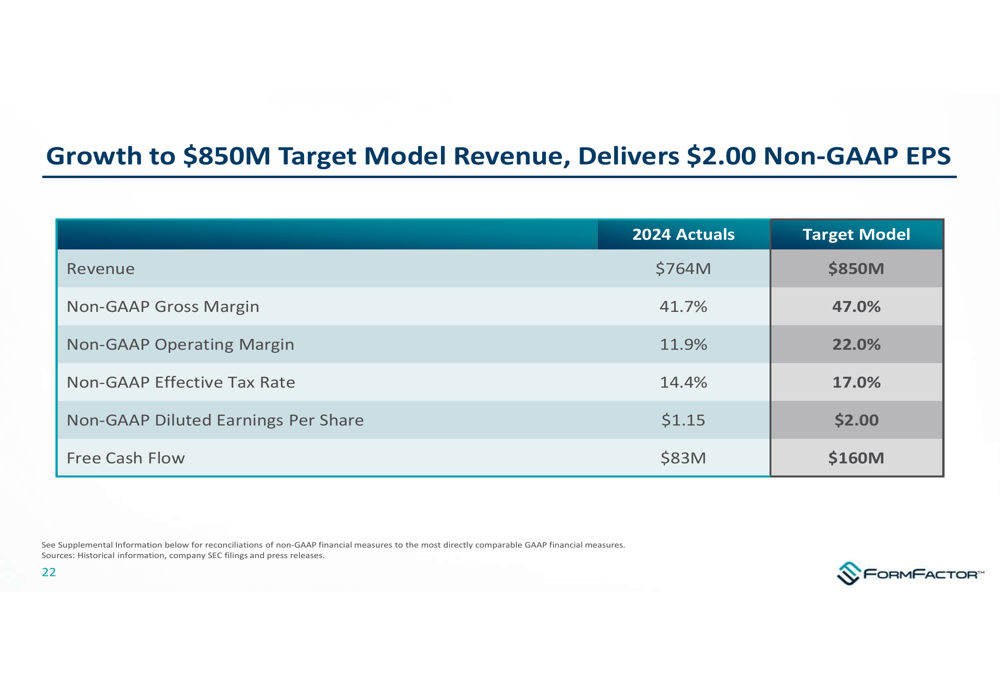

A significant portion of the presentation was dedicated to FormFactor’s ambitious long-term financial targets. The company outlined a path to $850 million in revenue, up from $764 million in 2024, with substantial improvements in profitability metrics.

As shown in the target model slide, FormFactor has steadily expanded its served available market from $0.9 billion in 2012 to $2.75 billion in 2024, with further growth anticipated:

The company’s detailed financial targets include significant margin expansion and earnings growth:

These targets represent substantial improvements from current performance, with non-GAAP gross margin expected to increase from 41.7% to 47.0%, operating margin from 11.9% to 22.0%, and EPS from $1.15 to $2.00. Free cash flow is targeted to nearly double from $83 million to $160 million.

Challenges and Outlook

While FormFactor’s presentation painted an optimistic picture, several challenges were evident. The company’s current gross margins (38.5% in Q2’25) remain well below the target model of 47%, and the negative free cash flow in Q2 contrasts with the long-term cash generation goals.

For Q3 2025, FormFactor provided an outlook of $200 million in revenue (±$5 million), with gross margin of 40.0% (±1.5%) and diluted EPS of $0.25 (±$0.04). This guidance suggests continued sequential revenue growth but potential margin and earnings pressure.

The earnings call revealed that tariffs are expected to reduce Q3 revenue by mid-single-digit millions, a challenge not prominently addressed in the presentation materials. Additionally, while FormFactor is positioning itself to benefit from AI and advanced packaging trends, it faces increasing competition in these high-growth segments.

Acquisition Strategy

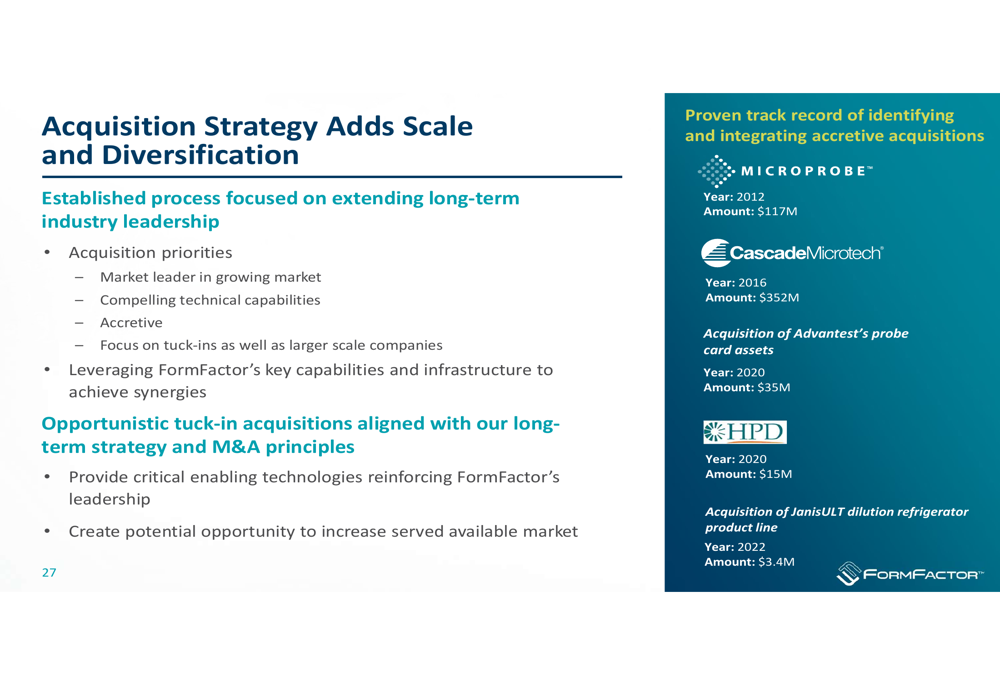

FormFactor highlighted its proven track record of strategic acquisitions as a key element of its growth strategy. The company’s approach focuses on adding scale and diversification through targeted acquisitions, with Cascade Microtech being a notable example.

As shown in the acquisition strategy slide, FormFactor has demonstrated success in identifying and integrating accretive acquisitions:

This strategy aligns with the company’s goal of reaching $850 million in revenue, suggesting that while organic growth remains important, strategic acquisitions will likely play a role in achieving the target model.

Conclusion

FormFactor’s Q2 2025 presentation reveals a company navigating a challenging semiconductor market environment while positioning itself for longer-term growth through strategic focus on high-value segments. The sequential revenue improvement and positive Q3 outlook suggest momentum is building, though the gap between current performance and ambitious long-term targets remains significant.

As the semiconductor industry continues to evolve with increasing emphasis on AI, advanced packaging, and high bandwidth memory, FormFactor appears strategically positioned to benefit from these trends. However, investors should monitor the company’s progress toward its margin expansion and free cash flow goals, as well as its ability to mitigate challenges such as tariff impacts and competitive pressures in key growth segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.