Trump/Putin summit, UnitedHealth and Japan’s GDP - what’s moving markets

Introduction & Market Context

Forward Air Corporation (NASDAQ:FWRD) presented its second quarter 2025 earnings results on August 11, 2025, highlighting sequential improvements in margins and pricing despite ongoing challenges in the freight market. The presentation showcased the company’s progress following its merger with Omni Logistics, which created a combined entity with global logistics capabilities.

The logistics provider reported its results against a backdrop of continued freight market weakness, with the stock closing down 5.55% at $30.25 before the presentation. In aftermarket trading, however, the stock showed signs of recovery, rising 1.98% to $30.85.

Quarterly Performance Highlights

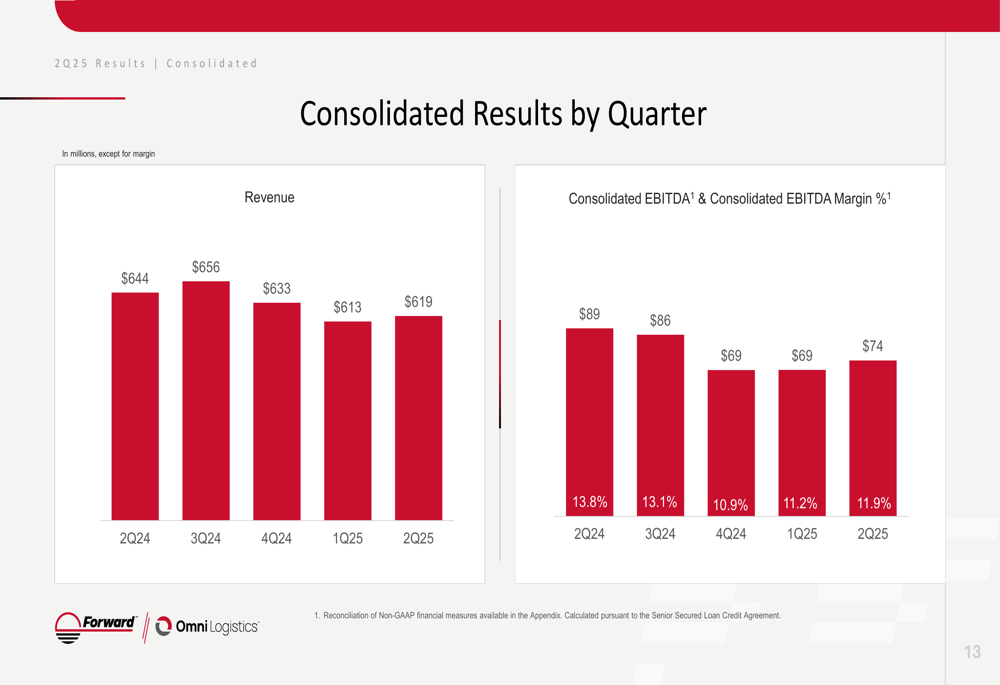

Forward Air reported Q2 2025 revenue of $619 million, down from $644 million in the same quarter last year but showing a slight sequential improvement from $613 million in Q1 2025. Consolidated EBITDA reached $74 million with an 11.9% margin, representing a sequential improvement from 11.2% in the previous quarter, though still below the 13.8% achieved in Q2 2024.

As shown in the following financial highlights slide, the company generated $20 million in operating income and maintained $368 million in liquidity:

The quarterly trend shows stabilization in revenue after several quarters of decline, with EBITDA margins beginning to recover:

Segment Performance Analysis

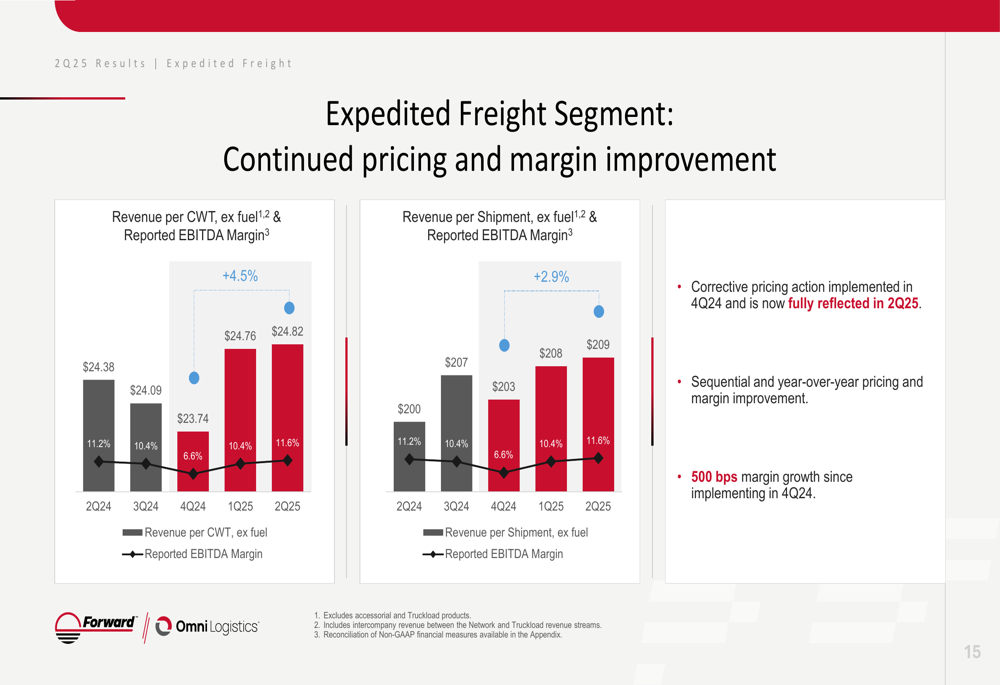

The Expedited Freight segment, which represents Forward Air’s core business, showed encouraging signs of recovery. Revenue for this segment reached $258 million in Q2 2025, up from $249 million in Q1 2025, though still below the $291 million reported in Q2 2024. More importantly, the segment’s EBITDA margin improved to 11.6%, compared to 10.4% in Q1 2025 and 11.2% in Q2 2024.

The company attributed this improvement to corrective pricing actions implemented in Q4 2024, which are now fully reflected in the results. As illustrated in the following chart, Revenue per CWT (excluding fuel) increased 4.5% year-over-year, while Revenue per Shipment rose 2.9%:

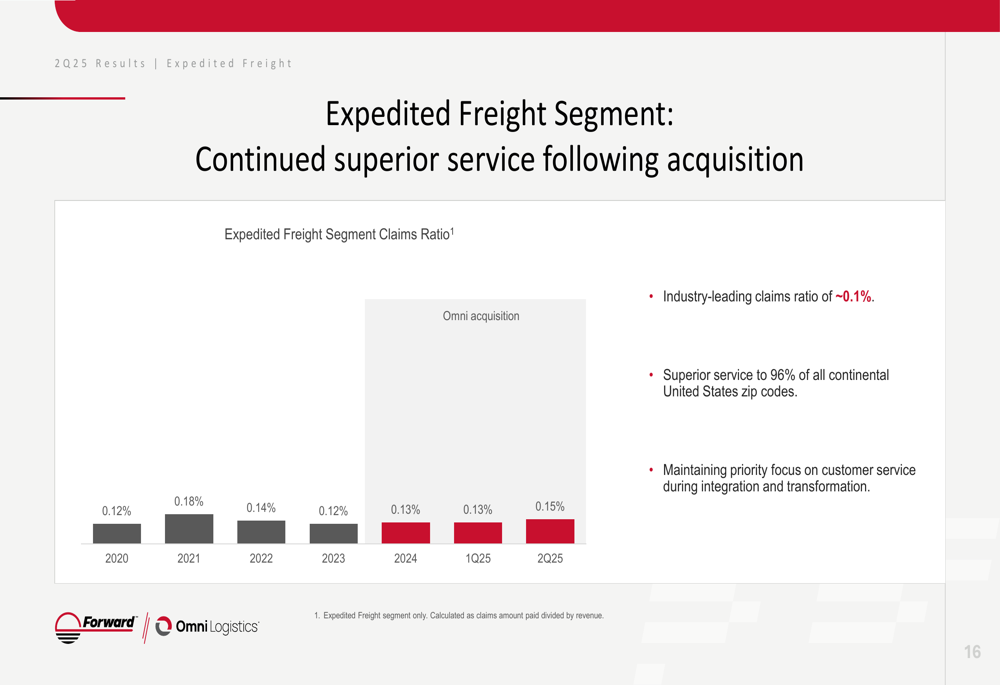

Forward Air has maintained its industry-leading service quality with a claims ratio of just 0.15% in Q2 2025, reinforcing its value proposition to customers:

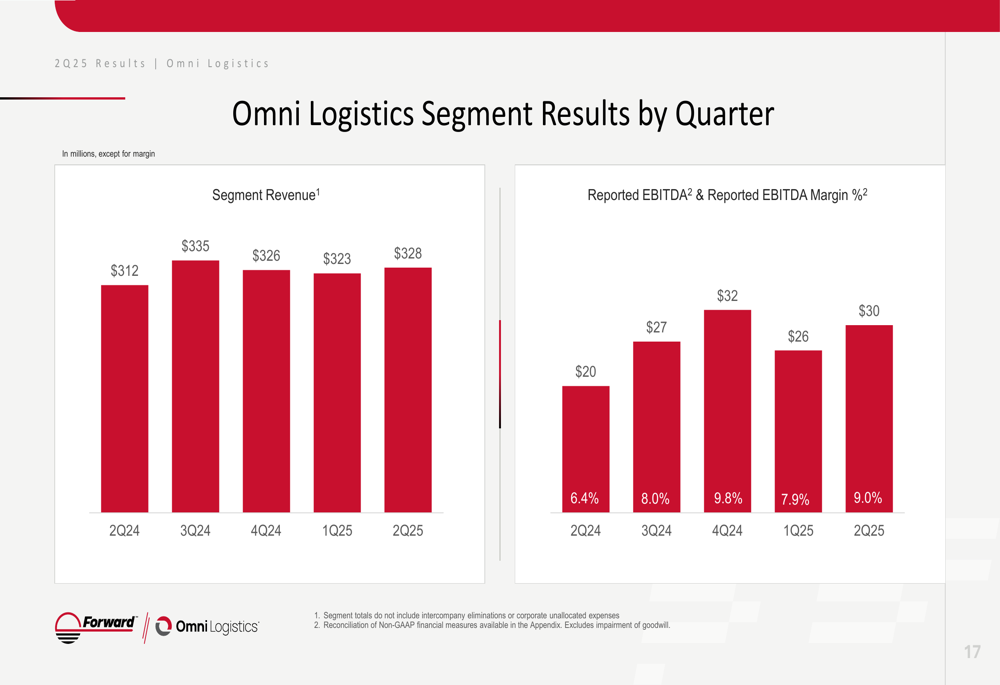

The Omni Logistics segment, which represents the company’s international forwarding and logistics operations, generated $328 million in revenue for Q2 2025, with a reported EBITDA margin of 9.0%. This marks an improvement from 7.9% in Q1 2025 and 6.4% in Q2 2024:

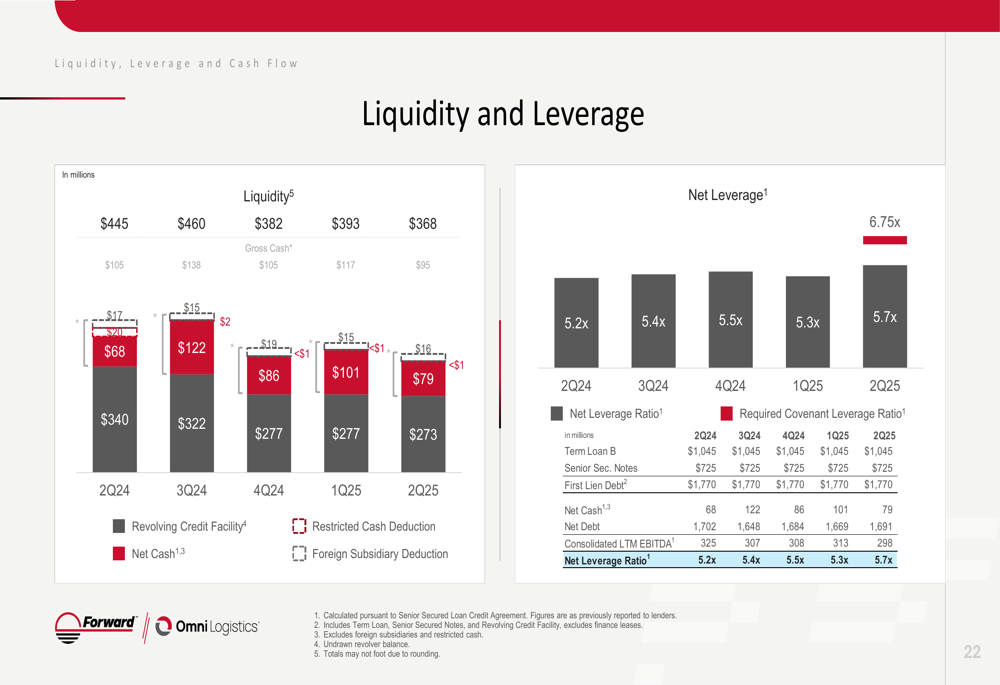

Liquidity and Leverage Position

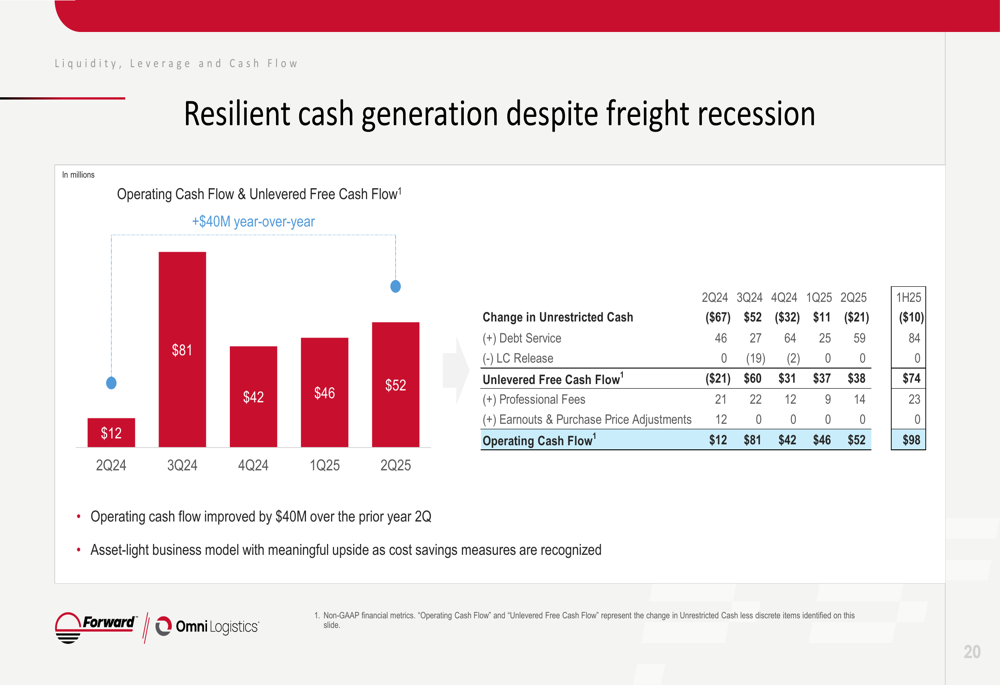

Despite the challenging freight environment, Forward Air reported improved cash generation in Q2 2025. Operating cash flow improved by $40 million compared to the prior year’s second quarter, highlighting the resilience of the company’s asset-light business model:

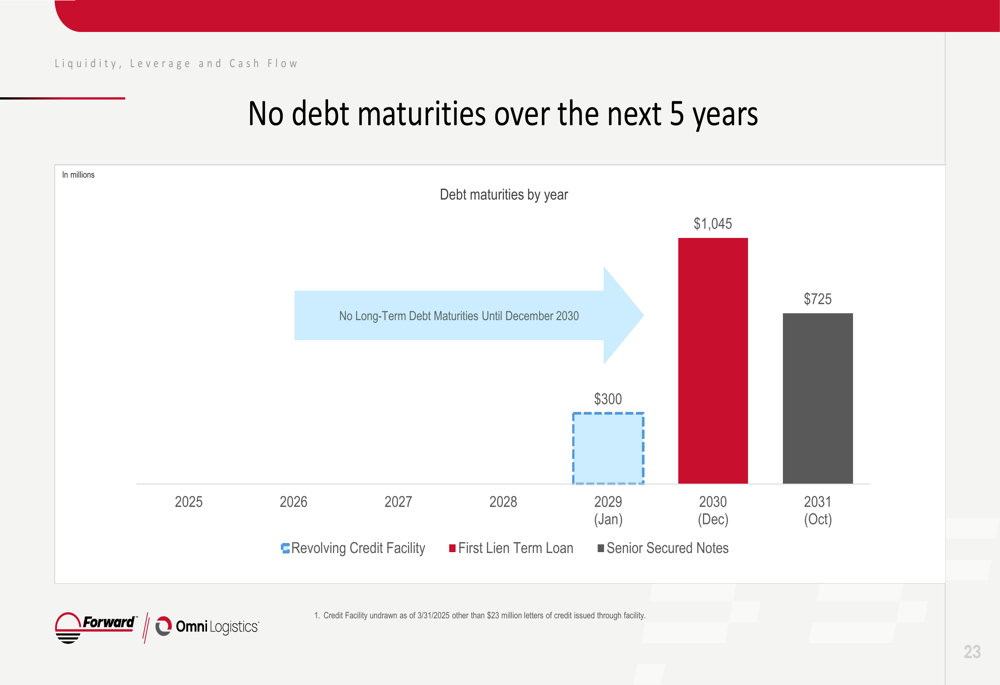

However, the company’s leverage position remains elevated, with a net leverage ratio of 5.7x as of Q2 2025, up from 5.2x in Q2 2024. This high leverage continues to be a concern for investors, though the company emphasized that it has no debt maturities over the next five years:

Strategic Outlook and Investment Rationale

Forward Air’s presentation emphasized its positioning as a logistics provider with both domestic and international capabilities following the Omni acquisition. The company highlighted its diversified service offerings across ground transportation (70% of revenue), air and ocean forwarding (12%), intermodal drayage (9%), and warehousing/value-added services (9%).

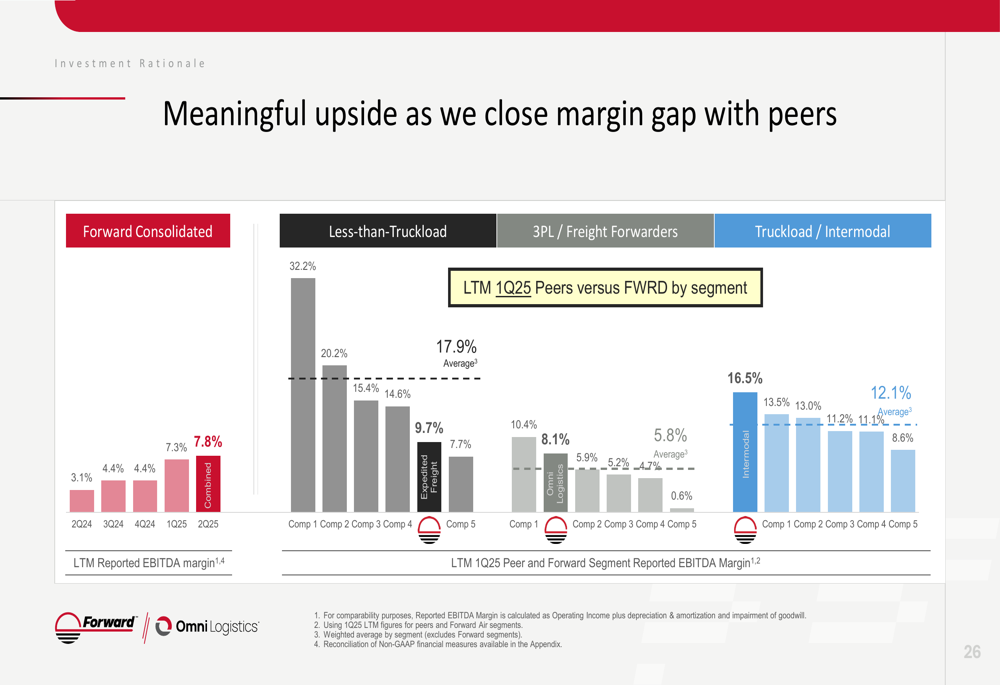

The company sees significant upside potential in closing the margin gap with industry peers. As shown in the following competitive analysis, Forward Air’s LTM reported EBITDA margin of 7.8% lags behind peers in the LTL, 3PL/Freight Forwarding, and Truckload/Intermodal segments:

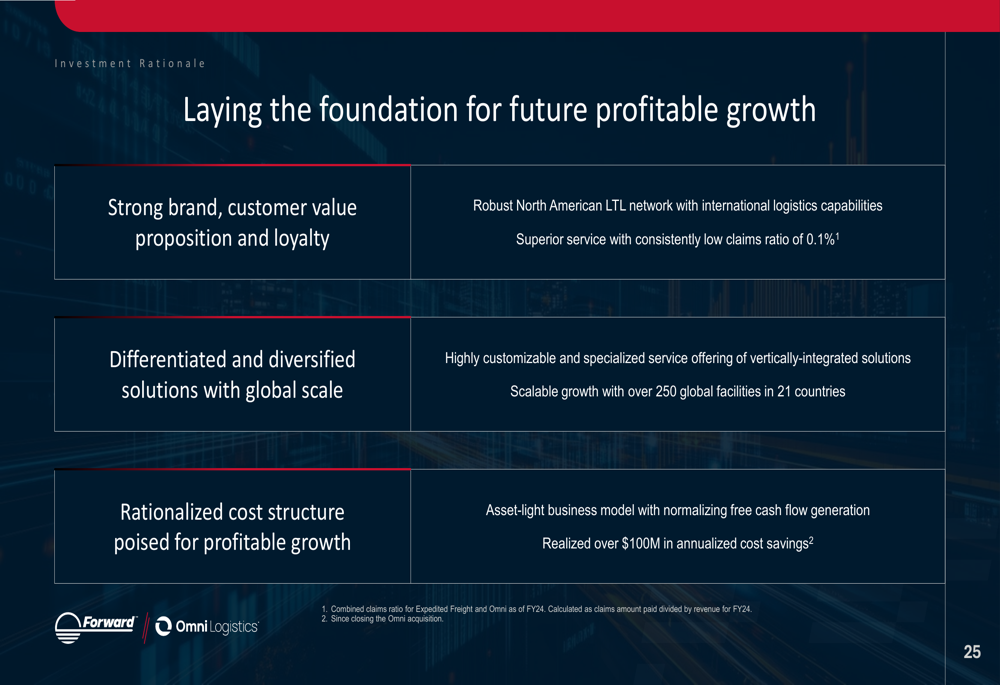

Management outlined several key elements of its investment rationale, including its strong brand and customer value proposition, differentiated solutions with global scale, and a rationalized cost structure positioned for profitable growth:

Forward-Looking Statements

While Forward Air’s Q1 2025 results had shown a significant earnings miss with an EPS of -$1.68 versus a forecast of -$0.44, the Q2 presentation focused on sequential improvements and the path forward. The company maintains its ambitious goal to double revenue to $5 billion within five years, building on its current annual revenue of approximately $2.5 billion.

The company’s strategy centers on organic growth, strengthening customer relationships, and enhancing sales force effectiveness. However, challenges remain, including the elevated debt burden of $2.1 billion and continued pressure in the freight market.

Forward Air’s presentation emphasized the benefits of its diversified product portfolio and the quality of earnings improvement, suggesting that the company believes it is on the right track despite the ongoing freight recession. Investors will be watching closely to see if these sequential improvements can be sustained and accelerated in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.